By Joachim Klement, Head of Strategy, Accounting, and Sustainability at Liberum Capital.

CBDC: What could possibly go wrong?

In this section, I will look at the risks involved with a CBDC, focussing mostly on the risks for users.

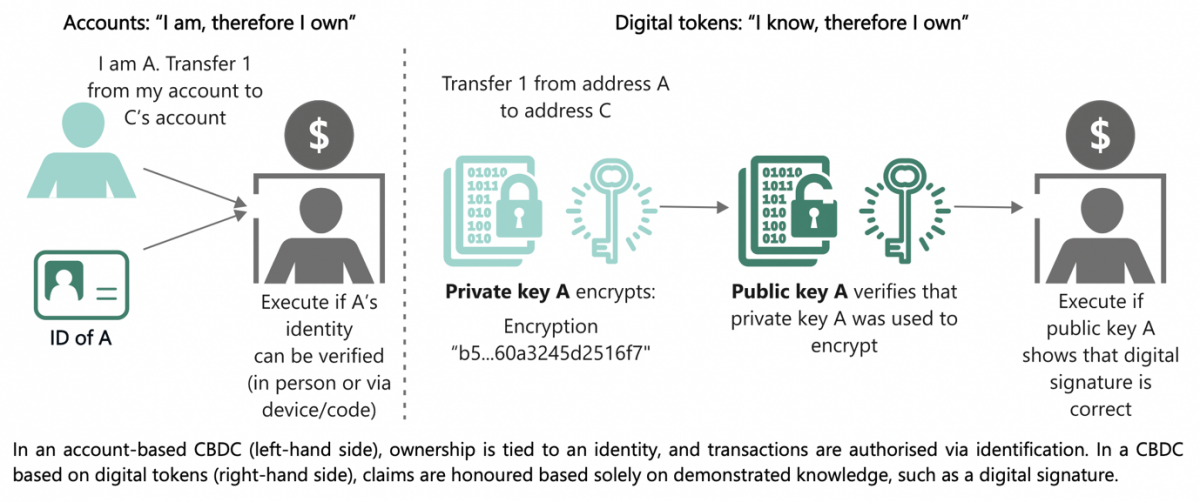

From a technology perspective, there are two ways to prove that you rightfully own a unit of CBDC. You either have stored them in an account like a bank account or a crypto exchange, or you stored them in an e-wallet that contains the ‘anonymous’ private keys to the tokens of the CBDC (or any other cryptocurrency, for that matter).

The two basic forms of ownership of a CBDC

Source: BIS.

If CBDC are stored in an account, the distributor of the account (typically a commercial bank or a cryptocurrency exchange) needs to verify your identity before they can open the account. These KYC rules are designed to prevent money laundering, terrorism financing, etc. The big advantage of account-based ownership is that it reduces criminal activities and we by now know quite well how to effectively protect these accounts from hackers. Furthermore – and this is generally an underappreciated advantage – if an account owner forgets the password to the account, the money isn’t lost. Access to the account can be restored once the rightful owner has been identified beyond doubt.

But of course, the problem with account-based ownership of CBDC is that it is not anonymous and that especially in emerging markets, millions of people do not have access to banks. There are legitimate reasons, why people want or have to use physical cash as a medium of exchange and if we want to introduce CBDC as a true alternative (or substitute) of physical cash, there needs to be some form of privacy protection.

This is where tokenisation comes in. Tokens are anonymous by design, and owners of these tokens prove their ownership by showing a private encryption key. In theory, these private keys can be stored anonymously on e-wallets. But as always, nothing is anonymous on the internet. Every transaction ever made with the token is recorded in the blockchain of cryptocurrencies and if one can link an encryption key with an individual, everything becomes traceable and identifiable. A couple of months ago, the FBI showed the world that it can trace Bitcoin and identify the owners of each Bitcoin. And if they can do it with sophisticated criminals that presumably are better at hiding their identities than most, then they can do it with everyone.

Now, some crypto fans will say that there are zerocoins that are extensions of traditional cryptocurrencies designed to preserve anonymity. Well, you might not have heard, but in 2018 it was shown how these zerocoins can be hacked and destroyed. Hackers cannot steal the zerocoins, but they can definitely destroy them and thus cause enormous damage.

Finally, if we leave the privacy concerns behind, there are the usual security concerns of digital coins being stolen. The Bank of Canada has done a very good job of summarizing all the risks to a token-based CBDC. In essence, the problem is that criminals typically don’t know how much money is stored in individual wallets. Thus, they flock to the biggest pool of money and tend to focus their attacks on the largest cryptocurrency exchanges, the largest banks, or in the case of CBDC, the central bank itself. In particular state-sponsored hackers from countries like North Korea that have already successfully hacked into the central bank of Bangladesh in the past, will be targeting CBDC networks.

The simplest way to steal CBDC would be to take over the majority of nodes in a distributed ledger which would allow the criminals to control all the tokens. This is a key reason, why CBDC will likely not use a public network but be restricted to a permissioned network of participating banks and institutions that are heavily regulated and have the means to protect their computers.

Even so, computing power constantly increases, and thus what appears unhackable today may not be unhackable in a few years. In fact, we are at the cusp of quantum computing becoming reality. Quantum computing would deliver a true revolution in computing power and enable us to perform calculations in a few minutes that currently would take hundreds or thousands of years. No cryptographic protocol currently in use in any digital currency could withstand quantum computing attacks. Thus, with the emergence of quantum computers, all digital currencies will immediately become unsafe (including any CBDC), or CBDC will need to be designed in such a way that they can be made ‘quantum safe’ in no time or that they will be ‘quantum safe’ by design. But making a digital currency ‘quantum safe’ will almost inevitably reduce the number of transactions that can be made per second and thus reduce its efficacy as a medium of exchange (see last week’s discussion).

But for now, quantum computing is science fiction, yet the key security gap for any CBDC already exists. It’s you.

I tell people that modern cryptographic protocols are so safe that I am not worried they will be hacked all the time to steal digital currencies. Criminals simply don’t need to go through all that hard work when the biggest security risk to digital currencies sits in front of the computer. E-wallets and accounts of cryptocurrencies and any CBDC will be owned by normal people and secured by passwords. And people use rubbish passwords all the time. Or they forget their passwords which is not so bad if they own an account with a bank, but if they forget the password to their e-wallet where all the highly secure cryptographic keys to their CBDC are stored, then, well, they are out of luck and have lost all their money forever.

People have told me that this is the same as carrying physical cash in a wallet and then having that wallet stolen by a pickpocket. And we accept that risk as well without complaining. Yes, but the analogy is not quite the same. If you go shopping in a mall with your physical cash in a wallet there may be one or two pickpockets around that will try to steal your wallet. If you use an e-wallet to pay on the internet it is as if you are walking in a shopping mall where every pickpocket in the entire world is hanging around, ready to steal your wallet given the opportunity. How likely do you think it is that your wallet will be stolen in that environment?

And this security risk is innate in every digital currency, and it means that no matter how the CBDC is designed, it will always be less secure than physical cash for a user because it can be stolen much more easily. It will be a security risk we will have to live with.

Monetary policy meets Big Data I will now focus on the aspect that I find most interesting: The ability to change monetary policy with CBDC.

One intriguing advantage of the introduction of CBDC is that the central bank could track payments and flows of cash throughout the economy, something that is not possible with physical cash. In particular, if a CBDC is managed via a central ledger, the central bank would be able to track the use and spread of money throughout the economy. In a CBDC with distributed ledger technology, this tracing activity would be harder, but it would still be possible to trace tokens and their use throughout the economy (Note, that we are not interested in identifying who spends the tokens, so we can keep users completely anonymous). This would open up the possibility to measure extremely well how money is used in an economy and how changes in monetary and fiscal policy propagate through the economy. In effect, we could finally identify, which monetary and fiscal policy measures are effective and which ones are not and thus reduce enormous amount of wasteful government spending or ineffective monetary stimulus. As someone who has a deep love affair with data, I can’t wait for this to happen…

The challenge, of course, is that CBDC would have to become the dominant form of cash in the economy and ideally replace physical cash completely. Yet, as I have said in the first part of this series, physical cash is still in widespread use even in developed countries and simply cannot be abolished anytime soon without putting small businesses, poorer and older households at a significant disadvantage or making it impossible for them to go about their daily lives. For these reasons alone, I find it impossible to conceive that physical cash will be abolished in the next ten years even in countries like Sweden, the Netherlands, or the UK, where the use of physical cash is lowest. That does not mean that physical cash will not be abolished in specific circumstances or individual countries and eventually (maybe in 10 to 20 years) in the most forward-thinking countries. But for the foreseeable future, our working assumption should be that at least some physical cash will be in circulation next to CBDC and other forms of electronic cash. Nevertheless, it is also safe to assume that once introduced, the use of CBDC will grow rapidly and statistical analysis of the transactions will enable us to improve monetary and fiscal policy significantly and target it for more efficient and effective purposes.

Nominal, real, or interest-bearing?

Physical cash retains its value in nominal terms. A £5 note will still be worth £5 next year. That inflation might have reduced its purchasing power is of course the problem. With CBDC, we have far more design choices. A CBDC could have a stable nominal value like physical cash, but we could also design it to have a stable real value by adjusting it to CPI every month. This would create the ultimate stable currency that would never lose purchasing power, no matter what policies the central bank of the government implement. Finally, we could add any kind of interest rate (positive or negative) to a CBDC and thus turn it into an ultra-short-term security that earns similar interest as government bills. This would enable central banks to implement monetary policy far more effectively and – if the CBDC has a positive nominal interest rate – would speed up the transition from physical cash to CBDC since consumers would earn interest in holding electronic cash but not physical cash. But with each design choice come trade-offs:

Just like physical cash introduces a zero lower bound on monetary policy rates, so does a CBDC with a stable nominal value. If a central bank wants to introduce negative policy rates, these rates cannot be too far below zero because if they are, consumers and businesses would start a run on the bank and try to convert their holdings of negative interest assets (i.e. the money they hold in bank accounts and short-term securities) into cash, where they earn an interest rate of zero. This is the famous effective lower bound to monetary policy and the reason why we are in such a quagmire with monetary policy today. A CBDC with a stable nominal value would not do anything to change that.

A CBDC that is linked to inflation would likely be even worse than a CBDC that has a stable nominal value. In a recession, the central bank would now be subject to an effective lower bound of a zero real rate of interest. The moment, the nominal rate of interest would drop below the rate of inflation (or expected inflation), consumers would switch their holdings into the CBDC that is linked to inflation, thus creating a bank run just when monetary policy needs to become more expansive. It would effectively be the same as returning to the gold standard and in the first part of this series I have explained why that is a really bad idea. Even more, If a country faces significant inflation, a CBDC linked to inflation may act like the infamous Hungarian tax pengö of 1946. Few people know that the worst hyperinflation ever recorded was not the German hyperinflation of 1923 (that takes silver) or the hyperinflation in Zimbabwe 2008 (bronze). No, the worst hyperinflation of all time was recorded in Hungary in 1946. It’s a long story, but essentially, after the Second World War, the Soviets literally took Hungarian factories and the printing press of the central bank to Russia as “reparations”. Faced with a disappearing (in this case literally) industrial base, the economy collapsed, and the Hungarian currency at the time, the pengö devalued. The result was rapidly rising inflation. The Hungarian government started to fear it would collect tax payments at a time when they had become worth much less than when they were due, so it introduced a law that forced Hungarians to pay taxes with a new currency, the tax pengö which was linked to inflation. This immediately created a run on the tax pengö which was hoarded while everybody tried to get rid of the regular pengö. In short, the velocity of money for the regular pengö exploded while the velocity of money for the tax pengö dropped to zero. It was like putting lighter fluid on a raging fire and within weeks everything collapsed.

This leaves us with the option of introducing a CBDC that pays interest. This is a beautiful thing because by paying a positive rate of interest, the central bank can accelerate the use of the CBDC and reduce the use of physical cash. Once physical cash is no longer used or only in marginal circumstances, physical cash could be abolished altogether with minimum pain to small businesses and poorer and older households. And at that moment, there is no more effective lower bound on monetary policy rates. Once there is no form of money that will always pay at least zero interest (i.e. physical cash), the central bank is free to reduce policy rates to -5%, -10%, or whatever negative rate it would like. His is the wet dream of every central bank governor and would finally fulfill the promise of the old joke: “What is the difference between God and a central bank governor?” – “God doesn’t think he is a central bank governor.”

The problem in practice is that introducing extremely negative policy rates may reduce rust in the central bank and eventually create hoarding of substitute assets like gold or cryptocurrencies just like we have seen it in 2020, just more and longer-lasting.

Finally, there is another important problem with interest-bearing CBDC: taxes. As you might know, people have to pay taxes on interest income in most countries (my apologies to readers in tax havens to which this may be an alien concept). But to pay taxes on interest income generated by CBDC, the government needs to be able to identify who owns each CBDC. Thus, anonymity goes out the window if a CBDC is interest-bearing. And we are back to the issues we discussed in part 2 of this series…

A totally new form of monetary policy?

But instead of introducing extremely negative interest rates, CBDC can be used to introduce a completely new form of monetary policy. Remember that the main reason to reduce interest rates is to incentivise people to spend or invest their savings instead of keeping them in the bank. In other words, the central bank tries to increase the velocity of money, or how often the available monetary base is used in the economy for consumption or investment.

But with a CBDC, one can directly influence the velocity of money through a “demurrage fee”. Essentially, the central bank would apply a fee for CBDC that is not used within a specific time frame. For example, assume someone has 100 units of CBDC in an e-wallet on 1 January. The central bank could introduce a 1% demurrage fee per month (it would most likely be much lower, but let’s keep things simple for now). Then, on 1 February, the value of CBDC that had not been used in January would be reduced to 99% of the original face value. So, if the person who owns the 100 units has not used it by 1 February, his account would only show a balance of 99 units on 1 February. If he had used 50 units and earned 20 new units of CBDC, then only the 50 units that had not been used in January would be subject to the 1% fee. Thus, on 1 February the balance would be 50 units – 1% fees = 49.50 plus the 20 units earned in January = 69.50.

It is clear that with the help of such a demurrage fee, the central bank could directly target the velocity of money and thus inflation instead of trying to indirectly influence inflation through interest rates or money supply.

One can even think of monetary policy turning into a form of fiscal policy by targeting the demurrage fee to specific spending. For example, if the government sends out free helicopter money to every household, the demurrage fee could be much higher on these funds than on other funds, thus giving a stronger incentive for households to spend in a recession. Or the demurrage fee on your savings could be reduced if the money you spend is spent on “productive uses” like rent, food, gym memberships, but not on “unproductive uses” like gambling, alcohol, or tobacco. It’s the nanny state to perfection, giving you the incentives not only to spend your money but how to spend it.

Or one could think about nonlinear demurrage fees that increase exponentially as savings increase. Someone who has few savings would pay no demurrage fee, but people with average savings would pay 1%, while the rich with extremely large savings would have to pay 10% or 20%. Note that this would not be a penalty on high savings in the sense of the government “confiscating” saved money. Every household and every business can avoid the demurrage fee entirely by spending the money they have. This way, trickle-down economics would finally work (something it has never done before despite what Reagan and Thatcher fans would tell you). The obvious side effect would be a boon for conspicuous consumption. You think Russian oligarchs and American billionaires spending half a billion on a superyacht is extreme? Just wait until you see a nonlinear demurrage fee in action.

In summary, a CBDC could lead to a whole new form of monetary policy that is ripe with all kinds of unintended consequences, which would obviously mean that investors would have to figure out how these new policy measures would impact stocks, bonds, and other assets. Just like before, we would likely have to re-learn the rules of the game once again.

Parts 3 & 4 of the original series:

Part 3: https://klementoninvesting.substack.com/p/cbdc-part-3-what-could-possib…

Part 4: https://klementoninvesting.substack.com/p/cbdc-part-4-a-new-form-of-mon…

About the Author:

Joachim Klement is an investment strategist based in London working at Liberum Capital. Throughout his professional career, Joachim focused on asset allocation, economics, equities and alternative investments. But no matter the focus, he always looked at markets with the lens of a trained physicist who became obsessed with the human side of financial markets.

Joachim studied mathematics and physics at the Swiss Federal Institute of Technology (ETH) in Zurich, Switzerland and graduated with a master’s degree in mathematics. During his time at ETH, Joachim experienced the technology bubble of the late 1990s firsthand through his work at internet job exchange board Telejob.

Through this work, he became interested in finance and investments and studied business administration at the Universities of Zurich and Hagen, Germany, graduating with a master’s degree in economics and finance and switching into the financial services industry in time for the run-up to the financial crisis.

During his career in the financial services industry, Joachim worked as investment strategist in a Swiss private bank and as Chief Investment Officer for Wellershoff & Partners, an independent consulting company for family offices and institutional investors as well as Head of Investment Research for Fidante Partners.