By Joseph S. Bohrer, a manager of multi-billion-dollar endowment, pension fund, and other institutional assets for 30 years before retiring in 2020.

Double-digit returns for PE are highly unlikely the next five to ten years while massive return dispersion means many LPs will see outright losses.

Institutional investors’ love affair with private equity reached new heights in 2021 while bears are nowhere to be seen. Everyone, simply everyone, loves private equity these days. The large endowments and foundations who’ve invested a great deal in PE over many decades and have relationships with the top performing GPs are maintaining large allocations. Pension funds and endowments who were latecomers to PE are adding as much as they can as quickly as they can. The folks who are reducing allocations… mostly don’t exist. According to a December 2021 survey of global institutional investors by Probitas Partners, about half of investors plan to maintain their allocations, more than 40% are planning to add, while only 4% planned to reduce PE. However, in my view, PE investors should prepare to be disappointed.

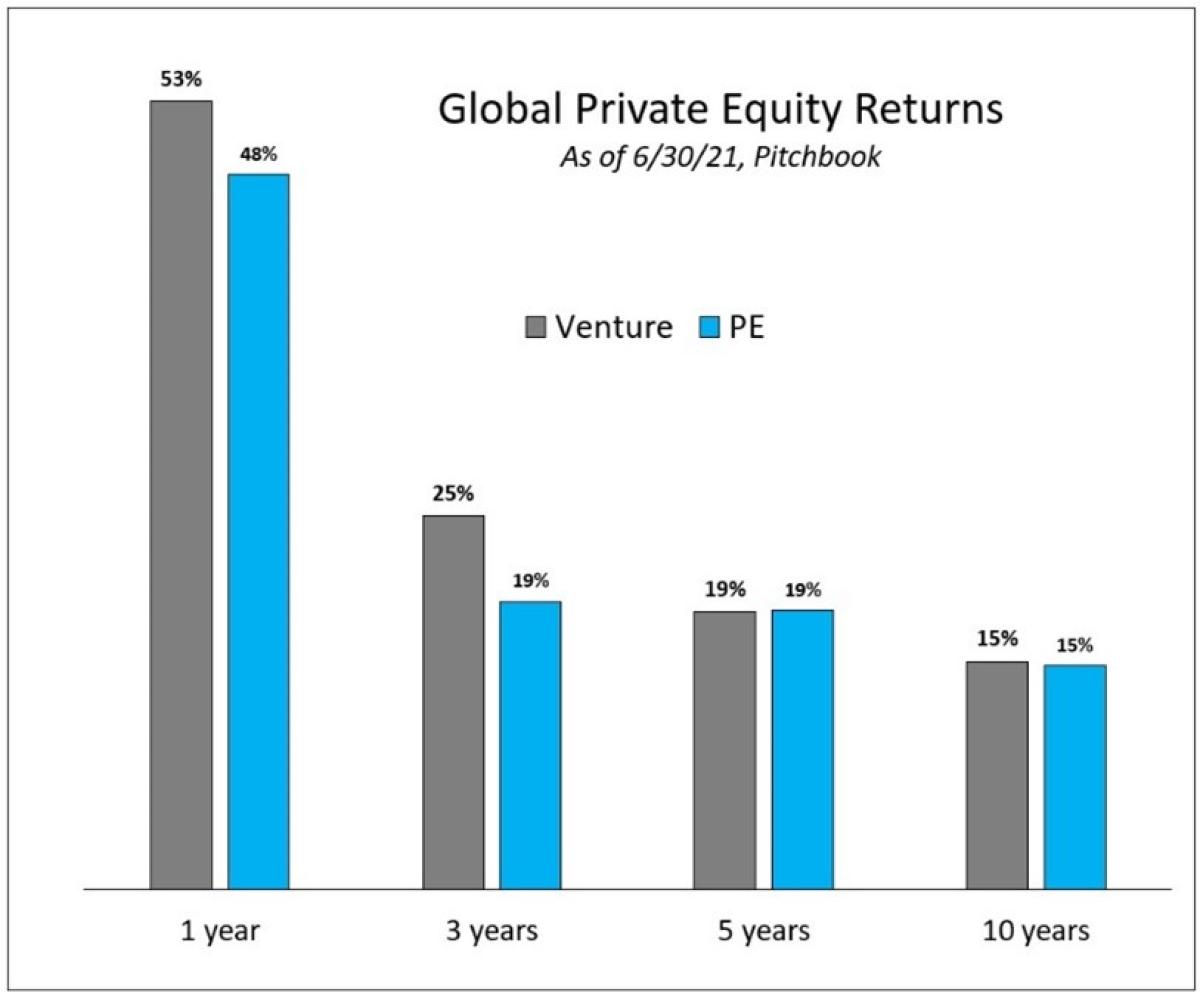

It’s easy to see why sentiment is so universally favorable: PE returns have been exceptional for a decade and positively spectacular last year (see chart below). PE returned 15% for the last ten years and 50% last year! And, not surprisingly, investors expect double-digit returns to continue into the future. When a CIO says they are increasing their PE target, invariably the rationale given is “high returns”. According to a survey of institutional investors done late last year by Coller Capital, 89% expect to earn an IRR of more than 11% while 27% of respondents expect to achieve more than a 16% IRR from their portfolios over the next three-to-five years. CIOs seem to have lost faith in all asset classes except PE, often describing private equity as “the only place where I can get high returns”.

Well, I hate to rain on the PE parade but those high returns that everyone is expecting? You just had them. The Federal Reserve front-loaded returns on risk assets so that 20 years of returns have been had in the last ten. Institutions betting on high PE returns over the next five to ten years are likely to be disappointed as the deck is stacked firmly against PE achieving anything like the 15% returns earned in the last decade. It’s hard to think of a single factor pointing towards higher returns – but there are a number of significant, obvious, near-term negatives likely to constrain PE returns in the decade ahead.

Before jumping in, let me be clear that when I say PE, I mean buyout, growth PE, and venture capital, i.e., traditional private equity.

One other important point: when discussing PE returns, I am talking about average industry returns. The earliest institutional investors in private equity were the big Ivy League endowments and charitable foundations. These folks and others who followed close behind dedicated significant resources over many years towards sourcing, diligencing, and gaining access to the very best buyout and VC funds. They've maintained a steady pace of commitments through thick and thin, up and down, not trying to time the market time. As a result, these PE pioneers have been able to build deep relationships with best-in-class GPs and as a result their PE investments have generated exceptional returns over long periods. In response to my bearish call on PE returns, these institutions might reasonably say, "so what?" This post is not intended for them because their PE returns are essentially untethered from the average.

But how many investors fit this description? The great majority of PE investors do not have significant resources with deep expertise dedicated to private equity and don't have relationships with the very best PE firms. These institutions are, in most cases, explicitly targeting the "PE beta", i.e., the average industry return, plus a few percent of alpha, and this post is written for them.

Here’s why I think double-digit PE returns in the next ten years are extremely unlikely:

Rates: The Punchbowl Is Leaving the Party

First and most importantly, interest rates. Since 2009, the Fed has kept short rates at zero while buying $9 trillion in bonds to effectively cap long rates. Central banks around the world have essentially done the same thing, in a number of cases pushing rates into negative territory. This had never happened before in recorded human history. Valuation of most assets is done by discounting projected future cash flows. When the discount rate approaches zero, almost any valuation becomes “reasonable”.

More than a decade of zero interest rates in all developed countries caused an extraordinary rally in all risk assets. The last decade has been favorable for PE in terms of less regulation, steady economic growth and rising profit margins – but it was rock bottom interest rates that turbocharged PE returns, just as it did public equities, residential housing, and all the rest.

Well, as we all know, interest rates are about to rise. How do we know? Because Jay Powell just told us so. And with 5% core inflation, it is quite clear the Fed is more worried about being too easy than being too tight. An increasing number of commentators are saying that the Fed made an enormous mistake in staying too easy too long and consequently is way behind the curve and needs to act aggressively to catch up. There’s no way to sugarcoat this: QE and ZIRP were a tremendously powerful force pushing valuations for public and private equities higher and higher -- and rising rates will exert a similar force for lower valuations. Lastly, higher rates will have a direct negative effect on PE returns simply by increasing financing costs.

Valuations: Sticker Shock

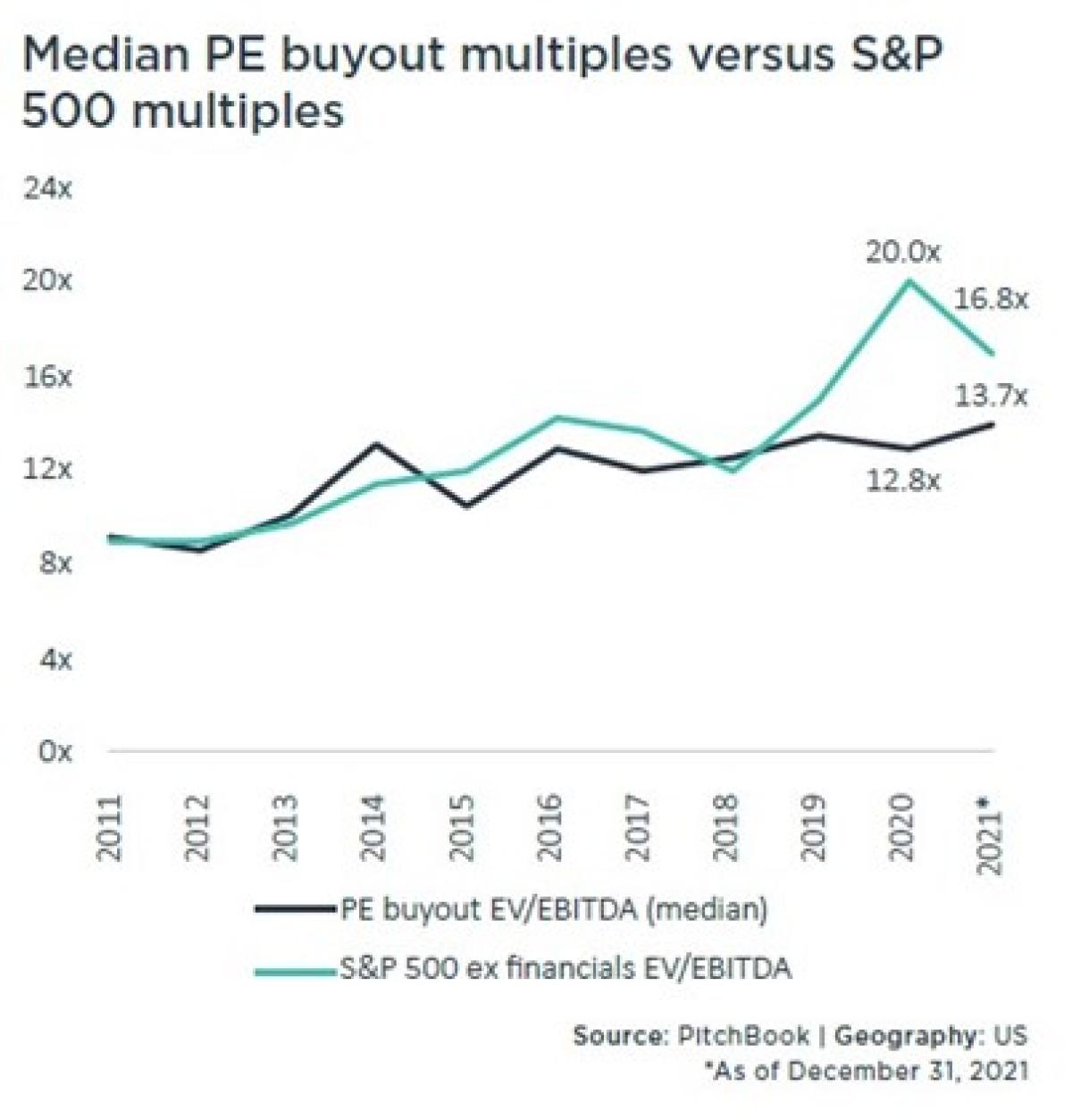

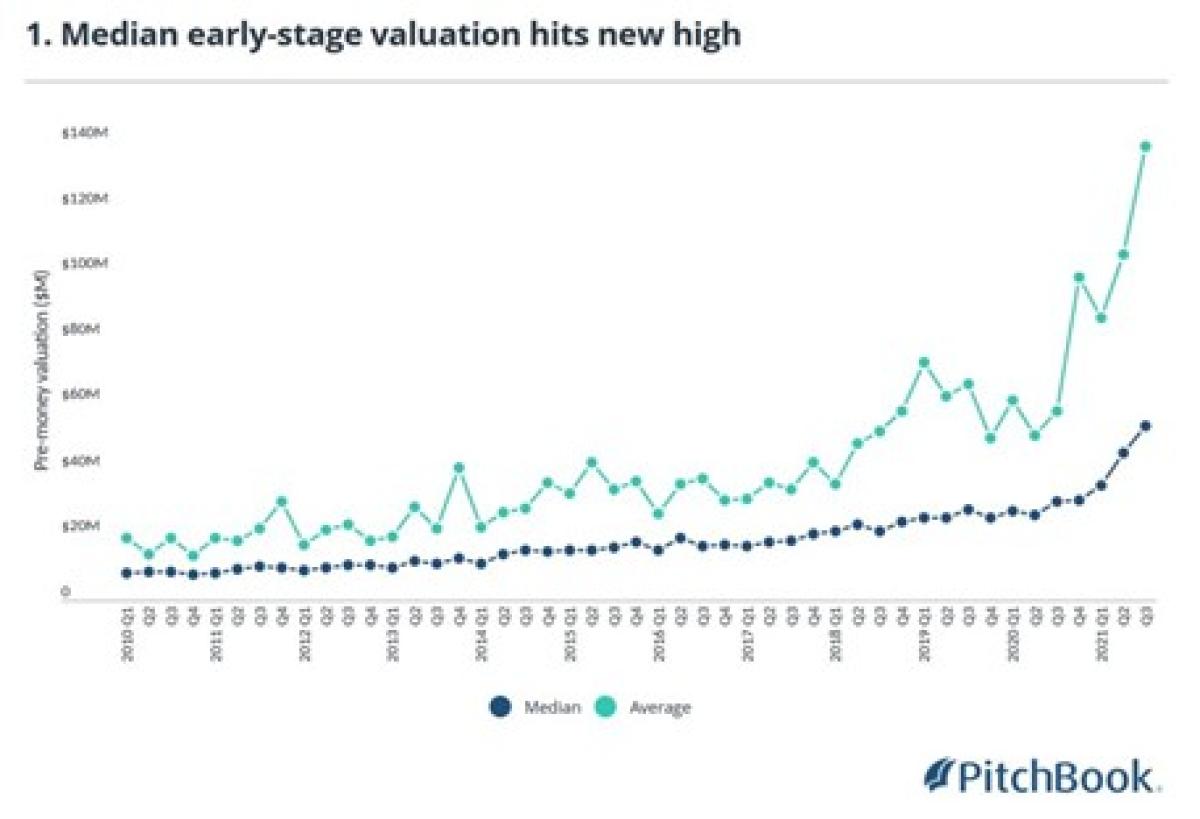

Record high buyout and venture valuations are a negative for future returns of course, even if interest rates remain low. Valuations are one of the best indicators of future longer-term returns: higher stock market valuation today tends to lead to lower returns in the years ahead. Much of the strong PE returns in recent years has been a function of rising valuations. Buy at 10x, sell at 14x, you made good money even if the company didn’t grow at all. Going forward, changes in valuation are more likely to be a negative than a positive, even if rates don’t rise much, simply because we’re starting from record high levels.

Profits: Cost Pressure

In the US over the last five or so years, PE profits and profit growth have benefited from a strong tailwind of a truly gargantuan tax cut and, until last year, low wage growth -- among other factors. This tailwind is now, as we speak, turning to a headwind. Corporate tax rates, now 21% and the lowest among all large, developed countries, may not rise but are certainly not going to be further reduced. Hence the massive one-time profit uplift of the 2017 cut in corporate rates from 39% to 21%, will not be repeated. And wages are now growing rapidly as American workers are quitting jobs in record numbers. For the first time in a generation, we’re seeing strikes and union organizing. Given a declining birthrate, reduced legal immigration, and the ongoing retirement of baby boomers, the American labor force is barely growing, hence strong wage growth seems likely to continue. Commodity prices were generally low and falling prior to 2020 but they’ve been rising ever since, and this will also be a modest negative for profits should it continue.

Size: Nowhere to Hide

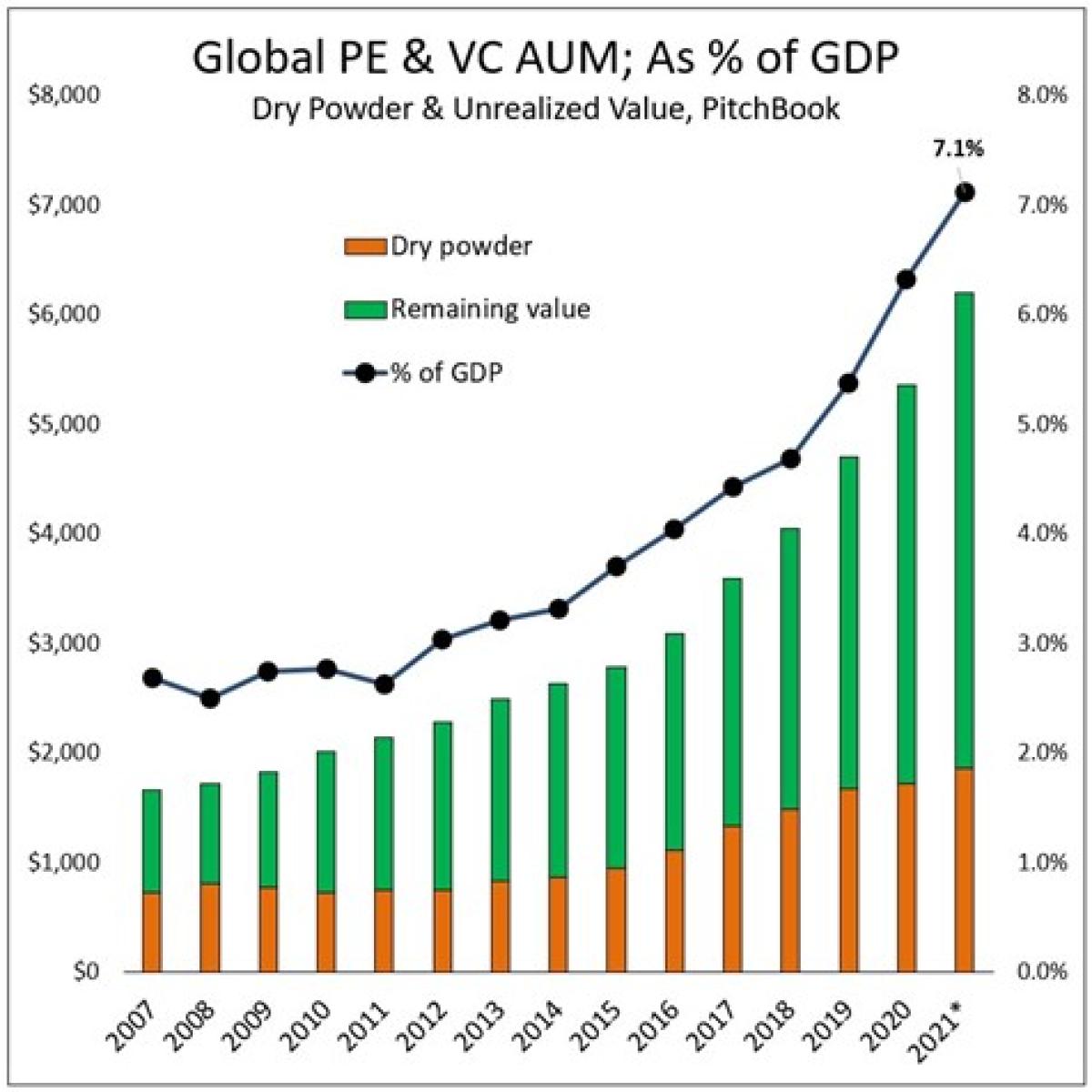

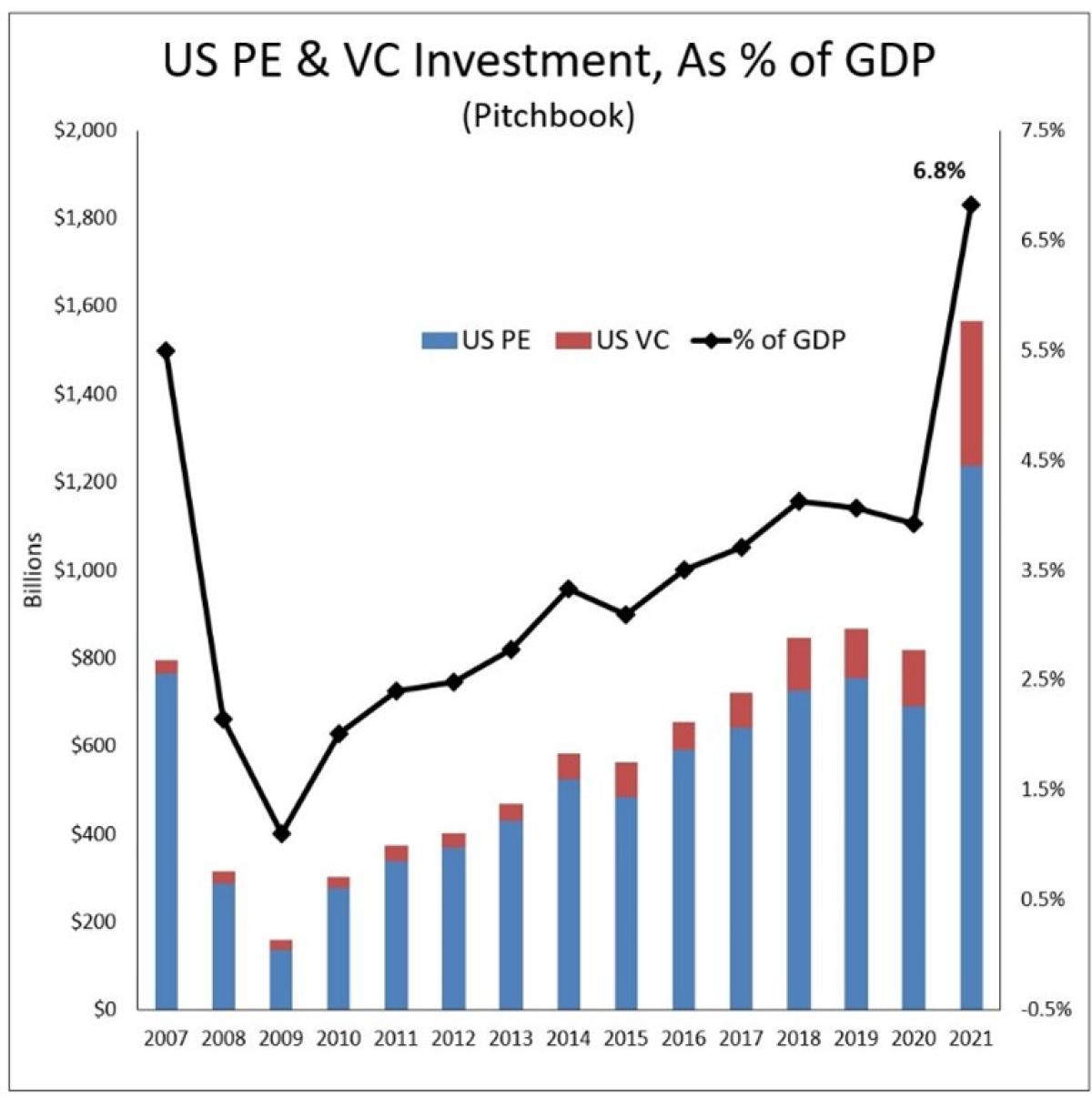

Whether you look at assets under management (unrealized plus dry powder) or annual investments, and whether you look at global PE figures or just the US, the private equity industry has grown to about 7% of GDP, up from only about 3% five years ago (see charts). Size is an issue for PE returns for three reasons. One, more capital is chasing essentially the same universe of private companies. That universe is getting increasingly picked over. For years, buyout and growth PE shops have employed armies of young professionals to cold call dozens of private companies every day to see if they might consider selling themselves. It’s hard to imagine that in 2022 there are many private companies worth investing in who’ve never been approached by PE shops. In short, the competition for deals, already fierce, will grow that much more ferocious -- which means higher purchase price multiples and, all else being equal, lower returns.

The second reason size is a problem for future PE returns is public opinion/political support. PE has grown to a size where it can no longer hide in the shadows; at $6 trillion in assets globally (dry powder plus unrealized investments), PE is now a major part of the global economy. In the US, PE collectively employs 12 million workers (9% of all US workers) and is a dominant player in many industries. As a result, the actions and tactics of GPs are visible to the American public and affect their lives to a degree that wasn’t the case even ten years ago.

Now, PE wants to continue to grow and get even bigger at the same time that the political support for PE seems to be declining. There isn’t a lot of good polling data on this, but my sense is that Democrats have gone from being sort of mixed about PE during the Obama years to today where most Democrats are outright hostile. This 2020 headline from a piece in Vox Media gives I think a sense of where rank and file Dems are on PE: What is private equity and why is it killing everything you love? In a sense this is just a reflection of the Democratic Party’s shift to the left on most economic issues. Republicans, pre-Trump, were broadly and strongly supportive of the industry but this is now in question. I’m no expert on MAGA-land but I’m guessing the folks attending Trump rallies are not big supporters of leveraged buyouts and preserving the carried interest loophole! PE professionals seem to agree that political support is an issue. In a 2021 survey of PE investor relations professionals by Coller Capital, 40% thought policy makers have a “poor impression” of private equity.

Public opinion and political support for PE hasn’t been a life-or-death issue in the past but given its growing size, it’s hard to see how diminishing public support for PE won’t be a major challenge going forward. Once GPs raise a fund, they’re going to aggressively seek targets to buy, and those targets will invariably sometimes be in industries where PE investment is controversial for any number of reasons. So as PE gets bigger and casts it’s net wider and wider to find deals -- the likelihood of deals being blocked or voluntarily withdrawn under public pressure from politicians or grass roots/social media campaigns has increased.

Anti-Trust: New Sheriff in Town

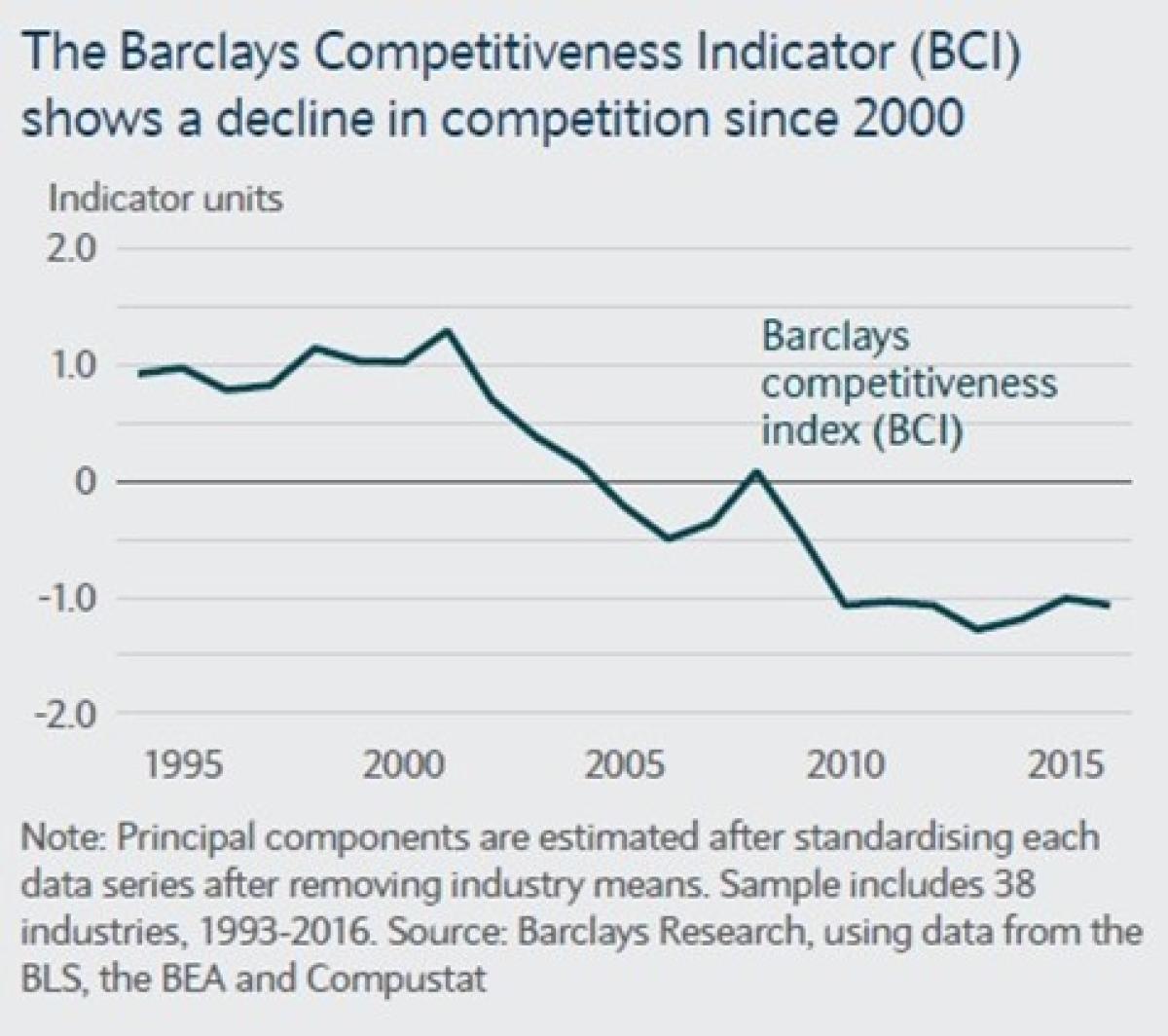

After decades of waving through corporate acquisitions with minimal review, the US economy has become increasingly concentrated by industry. Many industries are dominated by just two or three companies (see chart). Conceptually, this should be a negative for American innovation as dominant companies have less need to compete, and for wages as dominant employers effectively set wages for their industry. Joe Biden’s victory in 2020 means that for the next three years at least, a new aggressive breed of anti-trust enforcers at the FTC and Justice Department will be far more likely to block M&A deals.

Why does this matter? One, because much tougher anti-trust enforcement will hamper large and mega buyout shop deals just as it will corporate purchasers. Two, because over the last decade as the competition for deals has become more and more intense, many buyout GPs have made smaller initial investments and then built up those portfolio companies to a size that was meaningful for the fund through multiple add-on acquisitions. Often, the add-on acquisitions were done explicitly to increase industry dominance. Over the years I've listened to hundreds of buyout and growth PE fund pitches and a central tactic of many GPs is for their portfolio companies to do add-on deals to achieve some degree of dominance within a relatively small industry segment, giving them pricing power. While many add-on deals may be too small to get the attention of regulators, there is now an explicit national political and regulatory focus on the issue of too much corporate concentration, too many de facto monopolies, too much rent-seeking – and this has to be a challenge for GPs with playbooks full of strategies to achieve market dominance.

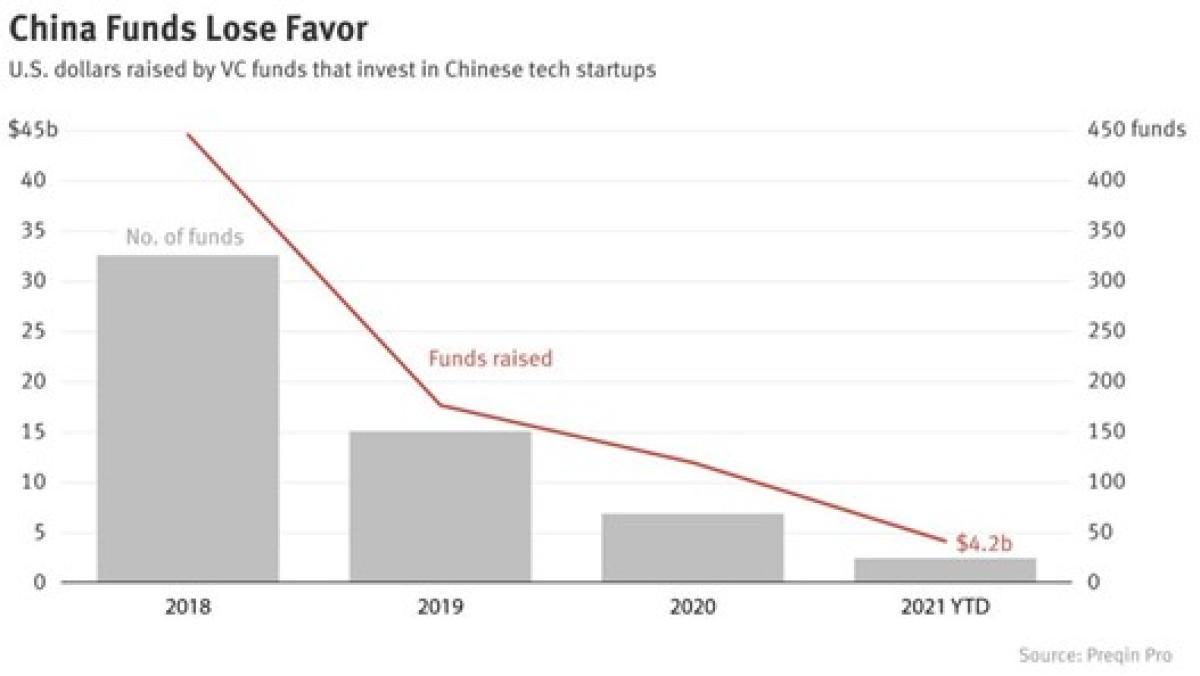

This source of returns for US investors is now questionable going forward for a long list of potential challenges. All these result from either the US/China decoupling begun under Trump (which now has bipartisan support) -- or from Xi Jinping’s crackdown on the private sector that began in late 2020. Evidently, US investors in China VC agree because funding for China VC funds based in US Dollars (which is how most US LPs invest) has declined sharply (see chart). It’s anyone’s guess how this all plays out but it’s clear that the environment which enabled strong China VC returns for foreign investors has changed dramatically.

The days of light touch regulation of the private sector from Beijing is over. Private Chinese companies with US investment will no longer be able to list in New York without multiple regulatory approvals, if then. Beijing is steering VCs to invest less in consumer and software (where they made a fortune) and more in enterprise and tech hardware. While it is perfectly understandable why China wants more investment in real innovation and less on making computer games, investing in tech hardware, particularly semiconductors, has historically been a great way to lose money.

Related Posts on American Carnage:

- Enough Already! Archegos Shows Wall Street Needs Radical Reform

- China’s Economy: Still Unbalanced After All These Years – And Now Close To Recession

Return Dispersion: Your Returns May Differ...

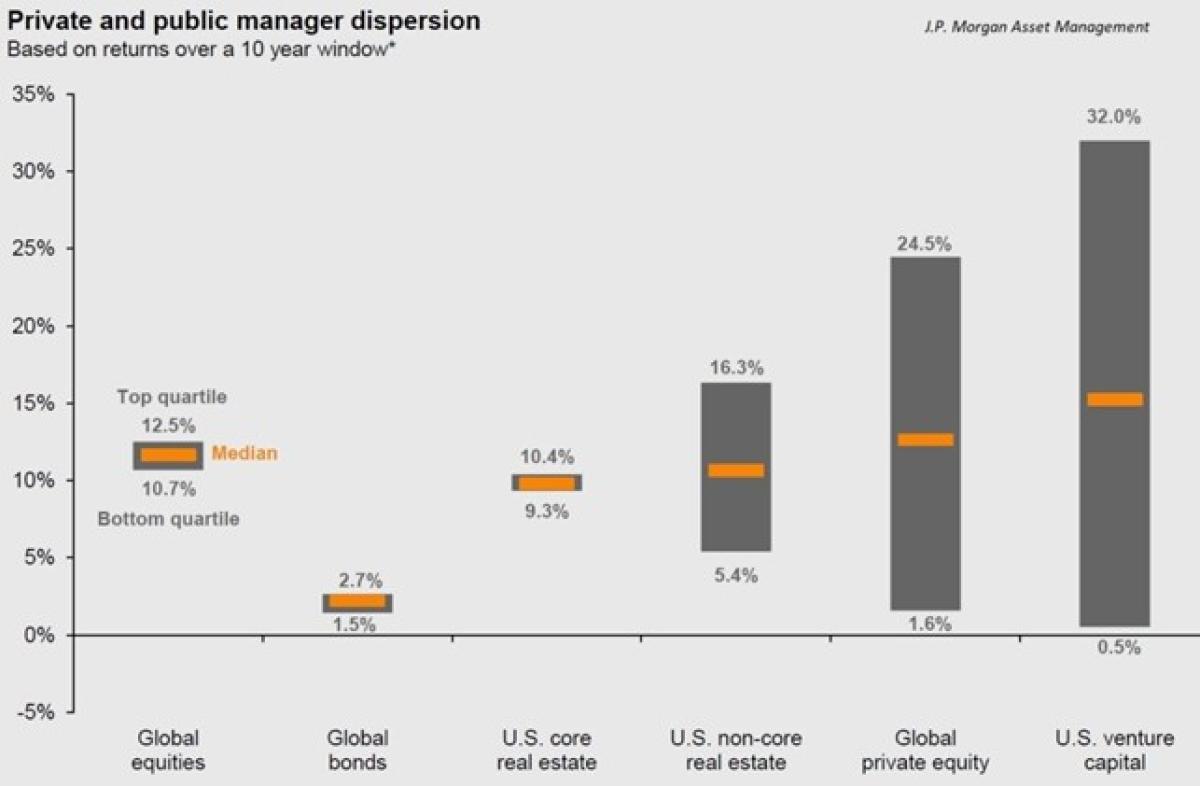

So far, I've focused on average industry returns but one feature of PE makes it especially rewarding for those who can pick the best funds and especially perilous for those who pick the worst funds: huge return dispersion. Historically, return dispersion for buyout managers has been more than 10x that of public equity managers while dispersion for VC funds is even greater (see chart). While industry average returns are likely to be single digits over the next 5-10 years, many investors (as noted above) can still do very well by picking 1st and 2nd quartile funds. But remember: this is not Lake Wobegon. Half of GPs will do better than the median but -- stating the blindingly obvious -- half of all GPs will do worse.

Illiquidity: Cash Poor?

It ought to go without saying but when institutions increase their allocations to private investments (of all types -- PE, real estate, debt, and infrastructure) to 40% or more of the total, ensuring there is adequate liquidity to fund annual cash payouts, other capital calls, fund new investments, and other cash needs will become more challenging and more complicated. In 2008, a number of endowments were forced to sell bonds in order to meet capital calls and other cash needs. When there’s a sharp drawdown in public equities, private assets, because they’re only valued quarterly, will appear to be a far larger portion of the portfolio (until those assets are eventually marked down) – further increasing complexity and the burden on small investment teams. PE investors will all tell you that by investing in PE, they are harvesting an “illiquidity premium”. My guess is that many investors will get the illiquidity but not the premium.

Public Equities: Superbubble?

Many of the same arguments against continued high PE returns are relevant of course for stocks too. Valuations are near-2000 levels, profit margins are also near record peaks, rising rates, anti-trust, rising costs -- all are challenges for stock prices. Jeremy Grantham, founder of GMO and "bubble scholar", says the US equity market is in a superbubble, a three sigma move away from trend. Perhaps it goes without saying but the correlation between public and private equity is approximately 1. So, if there's a bear market in stocks, there will be a bear market in PE, just with a one or two quarters lag.

New Paradigm, Same Ending

In my three decades of institutional portfolio management, I’ve seen a number of institutional asset management manias. Periods where it became universally accepted that a particular asset would show phenomenal long-term returns, only to end in tears when hope collided with reality. I’m old enough to remember the growing popularity of Portfolio Insurance in the mid-1980s which disappeared without a trace after the 1987 crash. In the early 1990s, it was the Asian Miracle and Barton Biggs was “maximum bullish” but in 1997 it became the Asian Crisis as currencies pegs broke causing a deep recession across the region. In 1998, I had a portfolio manager explain to me how the old valuation parameters were no longer relevant and that we had to embrace the “new paradigm” and buy large cap TMT stocks. Two years later, TMT blew up and growth underperformed value for the next ten years.

For seemingly the last twenty years or more, I’ve been told Emerging Markets are the place to be because, “that’s where the growth is”. The EM mania remains firmly in place, stubbornly resistant to the sad fact that EM has underperformed DM over almost any time period you choose to look at (though institutions which have the resources to identify, diligence, and gain access to the very best local EM managers may achieve great absolute returns regardless of what the local indices do).

In the early 2000s, Hedge funds were de rigueur for every self-respecting endowment CIO – right up until 2008 when the industry utterly failed to preserve capital during a 50% market crash with only a few exceptions. Since then, hedge funds have mostly been poor performers in good markets and in bad, weighed down by total assets still 10x greater than the amount they were when HFs last performed well (and of course the still ridiculous fee levels). Most recently, in the early 2010s, I was told that America is entering an energy renaissance driven by shale oil and horizontal drilling. Almost every large US endowment had 5-10% of their portfolios invested in private oil and gas partnerships focused on shale. This was such a successful mania that so much new domestic oil and gas production was funded that it eventually caused global oil prices to collapse in 2014. Today the net return of all dollars invested into US shale in aggregate is still negative.

All of these were the “accepted wisdom” at the time. People talked about them as though they were almost obvious, something “everyone knows” and those who disagreed were treated as, well, not very bright. Today's “can’t miss forever” asset class is private equity. But the combination of high valuations, much larger size, a tougher regulatory and political environment, and, most importantly, rising interest rates -- is likely to lead to disappointment, just as it has so often in the past when investors fell hopelessly in love with an asset class.

About the Author:

Joseph S. Bohrer was a professional money manager for the last 30 years before retiring from asset management in 2020. He managed “institutional money”, e.g., multi-billion-dollar pension fund, endowment, and sovereign wealth fund assets. He spent 18 years as a portfolio manager and business manager at J.P. Morgan Asset Management, ten years of which was posted overseas in London, Singapore, and Tokyo.

Joe worked for almost ten years as an investment director at the Alfred P. Sloan Foundation in New York City, part of a small team tasked with managing their ~ $1.5 billion endowment. Most recently, he was the Chief Investment Officer, based in New York, of the Lafayette College endowment (~ $1 billion in assets) for the six years through 2020 where he established the College’s Investment Office.