By Jason Kirchhoff, CAIA, CFA, CFP, Director with the land investment team at The Summit Agricultural Group.

A high-level comparison of farmland to traditional real estate sectors

Real estate continues to be a basic building block for investors as they create portfolios designed to generate strong real returns. The recent spike in inflation has heightened the interest in real assets as financial assets are priced near historic highs on several different metrics. Investors seeking inefficiencies and diversification have been drawn to some of the smaller niche real estate investments such as self-storage, marinas, or cell towers.

However, there is one large real estate sub-sector that many investors continue to overlook but has provided strong real returns for decades and diversifies a portfolio. That asset is U.S. Farmland. It provides investors with several differentiating characteristics, which set it apart from other asset classes even within real estate. The following sections highlight some of these differences.

Size of Asset Class

The value of U.S. Farmland is approximately $2.7 trillion according to a recent report from the USDA. [i] In 2018, NAREIT estimated the total value of commercial office space in the U.S to be about $2.5 trillion and multifamily housing to be roughly $2.9 trillion. [ii] These numbers come from different sources and require high level assumptions and estimates. However, the fact that US Farmland values are roughly equal to office space or multifamily is probably surprising to most investors

Competition/Supply

The supply of farmland is shrinking often because the other real estate sectors are growing. [iii] The demand for industrial space and housing continues to grow in the outer-ring suburbs of city centers. The supply is rising to meet that demand and often removes more and more arable farmland. For example, according to an October 2021 census report, the number of multi-family housing units under construction is close to a fifty-year high. [iv] Unlike other real estate sectors that will see additional supply during periods of high demand, the supply of farmland is relatively inelastic.

Tenants/Vacancy

One of the risks with traditional real estate sectors is making sure income is consistent and maximized by keeping the rent rolls near capacity with credit-worthy tenants. Farmland is almost always 100% occupied as there are usually local farmers looking to expand their operations by leasing additional ground. In addition, the famers typically pay a cash rent in advance.

Capital Expenditures

Traditional real estate buildings depreciate over time and need periodic renovations and upkeep to remain competitive with new supply. Farmland typically does not depreciate and requires minimal ongoing investment, especially annual row crop farmland.

Pricing Transparency/Efficiency

Commercial real estate is typically listed on a local service as well as a national database and it is relatively easy to track previous sales and comparables. Farmland transactions often occur on a privately negotiated basis or at a locally advertised auction and there is no comprehensive database of transactions.

Diversification Benefits

Most real estate sectors are sensitive to business cycle or macro-economic factors and thus have a high positive correlation to stocks. Farmland has historically not had any correlation to other commercial real estate and stocks as evidenced by the NCREIF Farmland Index.

Historic Returns

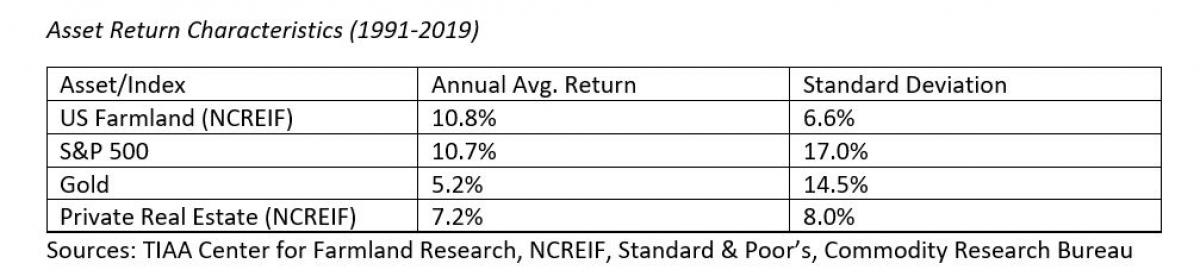

Over the past thirty years US Farmland has generated a strong return with much lower volatility which has compared favorably to both the US Stock market and a US private real estate index.

Summary

U.S. Farmland is a unique asset class that provides investors with an attractive risk/return profile and will add diversification benefits to a portfolio.

Refrences:

[i] USDA ERS - Assets, Debt, and Wealth

[ii] Estimating the Size of the Commercial Real Estate Market in the U.S. | Nareit

[iii] U.S. Farmland is Rapidly Decreasing · Giving Compass

[iv] Most Housing Units Under Construction Since 1974 (substack.com)

About the Author:

Jason Kirchhoff, CAIA, CFA, CFP is a Director with the land investment team at The Summit Agricultural Group where he is responsible for their managed accounts platform. He can be followed on Twitter @jason_kirchhoff where he regularly shares macro information on farmland investing.