By Jo Murphy, Managing Director, Industry Relations, Asia Pacific, CAIA Association.

Domestic and international investors have demonstrated their confidence in India as one of the most promising growth economies of the 21st century. World Bank estimates value India’s economy at around $3 trillion today, with projections for this to increase to $5 trillion in the next 10 years.

This growth path is underpinned by the Indian Government’s dedicated efforts, along with agencies like InvestIndia, to enable a more robust and self-reliant country. The promotion of India as a knowledge-based and digital hub is a central plank of this strategy[1].

The key to India’s emergence as a credible and vibrant investment destination is undoubtedly a reform-minded and anchored government, leading to India now regularly sitting among the top 10 in the World Bank’s ‘Ease of Doing Business’ rankings.

Prime Minister Narendra Modi’s reform agenda is showcasing opportunities and gradually eradicating the structural inefficiencies that held India back for so long[2]. By doing so, the government has created a robust launchpad for accelerated economic growth.

These regulatory enhancements, especially those introduced to bolster the local financial markets, are not just underpinning the traditional public markets but, just as importantly, are extending solid and favorable support to India’s burgeoning alternative investment funds (AIF) Industry, and in particular its PEVC sector.

India’s attraction is also being soundly aided by a geopolitical tailwinds, stemming from nervousness about the impact of China’s attempts to rein-in capitalism and the economy’s debt dependence. President Xi Jinping’s crackdowns have certainly resulted in an increase in foreign institutional investors (FIIs) investigating Indian PEVC opportunities as a viable alternative.

Further, multinationals have largely been overdependent on Chinese manufacturers. In a time of political tension and supply chain pressure, they’re looking to diversify their partners. India is proving a popular choice, offering up a cost effective, reliable and English-speaking alternative. For FIIs, those actively seeking an alternative for their emerging market allocations, alongside direct investment opportunities, India ticks all the boxes.

The rapid pace of growth is further demonstrated by the sustained optimism being shown in India’s stock markets. With public market valuations sitting at lifetime highs – for example, the average price/earnings ratio across the Sensex is currently around 30x) - the market boom is drawing in new retail investors. The Sensex has more than doubled from its March 2020 low and was the best performing market in the world in 2021.

Two other factors of note and acting as further accelerants are the Central Bank of India’s liquidity high surplus levels and declining interest rates.

These factors in aggregate have drawn the attention of India’s local investor community to a wider range of investment options, leading to a marked increase in private markets activity. This greater diversification is particularly notable in the manner of its increasing momentum over the past 12-18 months.

Resilient, Raging and Raring To Go: PEVC

PEVC has been a solidly resilient sector within India’s growing private market, in spite of COVID-19’s outbreak. Deal activity is raging and 2021 was a landmark year for the industry. The sector is benefiting from sooner-than-expected business recovery, alongside solid investment inflows from both domestic sources and FIIs.

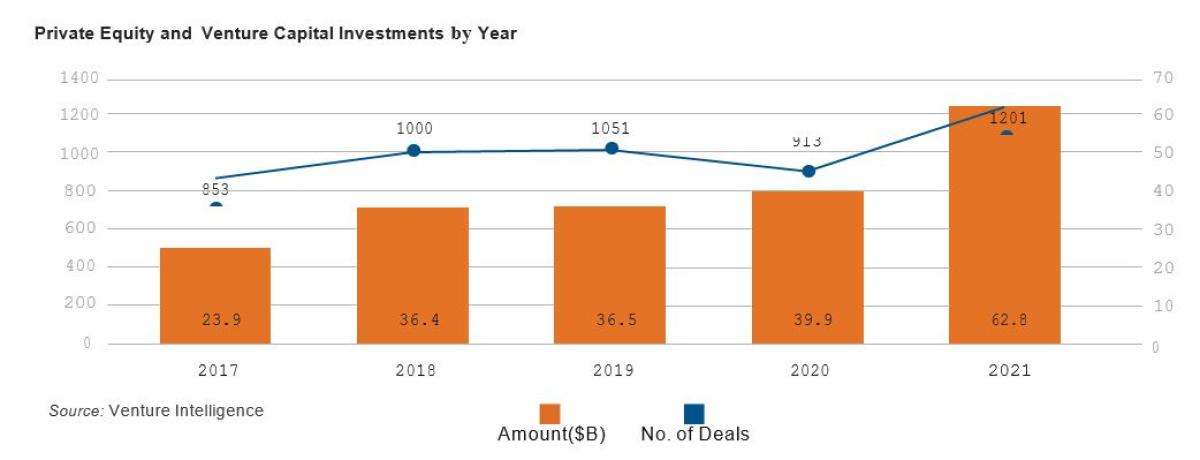

One of the most encouraging aspects for India is that new investments are larger. During the first half of 2021, investments grew 33% year-on-year, with investment flows of $27.1 billion across 442 deals, compared to $20.4 billion, across 433 deals during the same period in 2020 (Venture Intelligence Data).

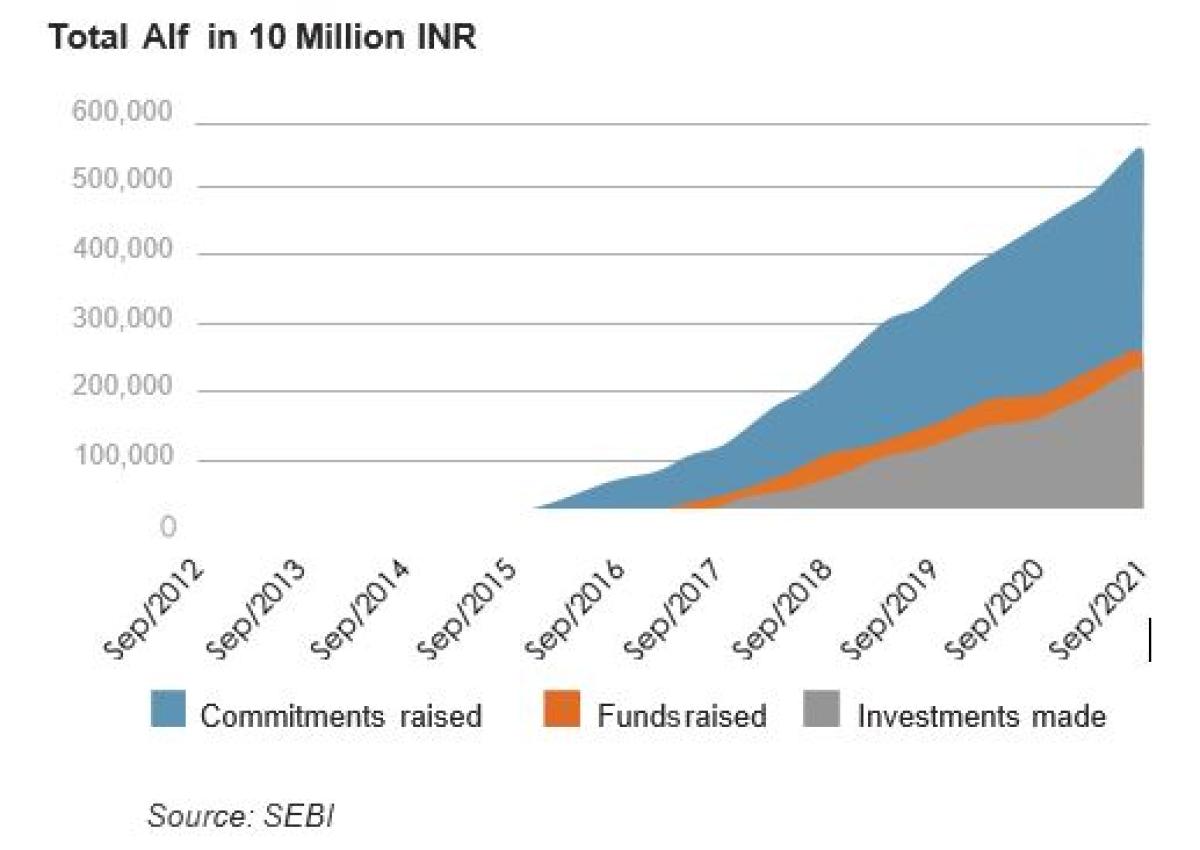

The past decade has certainly seen a coming of age for India’s PEVC sector. We’ve seen the number of fund managers swell from XX in 2010 to YY in 2021. Capital flows have been equally buoyant with a pool of $XX back in YY rising to $YY in 2021. Noteworthy is the mix of both interest from FIIs - finding India’s allure too good to miss – alongside home-grown investors diversifying their portfolios.

With many sectors flagged for growth, PEVC LPs and GPs are increasingly eager to assess opportunities early, seek solid partnership actively, and allocate investment quickly.

Change of Approach

Fuelling this activity is a significant change in the approach target companies are taking during the formation stages of partnerships, and their engagement with PEVC partners. There’s now an increasing willingness to provide control to PEVC firms, sturdily assisting with the acceleration and growth within the sector. This approach was previously absent, leading to often thwarted and stalled transaction negotiations, muddled engagement and, ultimately, compromised returns. The old guard wanted to hold on too tightly to the reins.

The large pool of young Indian entrepreneurs is spearheading this change. Globally exposed as well as professionally trained, they are unencumbered by the conservatism of the previous generations. This cohort of entrepreneurs are eager to embrace the opportunity to partner. Indeed they are actively seeking out potential opportunities, whether via domestic or international channel sources. This certainly bodes well for the sector; for engagement, for opportunities and for returns ahead.

Sectors of Note

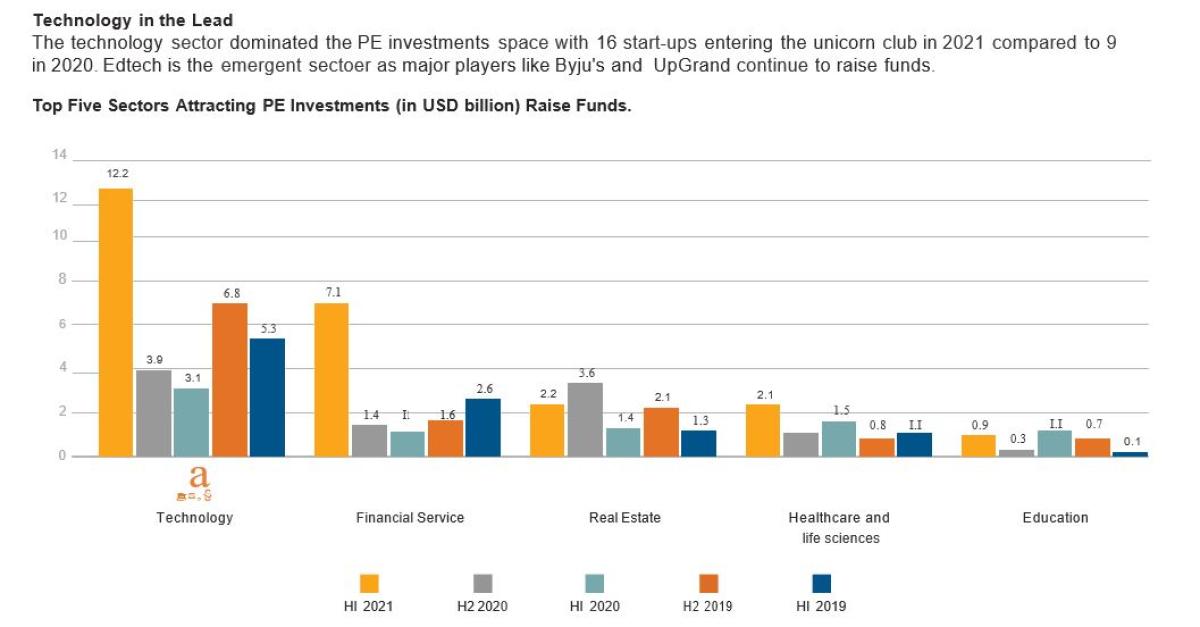

The Information Technology (IT), Information Technology Enabled Services (ITeS), Software as a Service (SaaS), Healthcare and Pharmaceutical sectors, each saw a significant portion of new investment flow in 2021. IT, ITeS and SaaS have benefitted strongly from the growth of digital adoption, as well as a greater need for digitization on the back of strong consumer shifts during COVID-19. In the wake of the pandemic, India has emerged as the fastest-growing and third-largest fintech ecosystem in the world. This led to a spike in deal volume, where the number of transactions was greater than $100 million, to 73 in the first half of 2021 compared to 28 during the same period of 2020.

The Banking, Financial Services and Insurance (BFSI) sector has seen a contraction of interest in non-banking financial companies to an increased focus towards insurance – focused on the insurer and insurtech segments. This focus has been enhanced by the Insurance Regulator and Development Authority of India (IRDAI) permitting insurance companies to invest in Fund of Funds, in April 2021, providing a further and significant boost.

For at-home services – consisting of consumer technology, vertical e-commerce, edtech, fintech and foodtech – each attracted significant interest during 2021. With the rise of disposable incomes, focus is increasing on businesses who serve the Indian consumer, both offline and online. As a result, the logistics sector is anticipating exponential growth, with many new investment targets emerging.

Global institutional investors are increasing their real estate allocations and are looking at opportunistic real estate investment strategies in India. PE real estate in India has significant momentum, led by the aggressive investments of Blackstone and Brookfield. According to Jones Lang LaSalle, more than $14 billion was invested by private equity in Indian property since 2006. Approximately 10 new PERE funds are being launched annually.

"This cohort of entrepreneurs are eager to embrace the opportunity to partner. Indeed they are actively seeking out potential opportunities, whether via domestic or international channel sources."

India’s collapsing and aged infrastructure offers endless creative development opportunity between public and private interests, particularly in roadways, electrical grids, renewable energy and telecommunications.

Tech in Focus: (R)Evolution

As noted, the appetite for tech-related investment is substantial, which is probably not surprising given India’s domestic demographics and such a large pool of the ‘online first’ digital generation. With almost 30% of India’s citizens under the age of 14, there is undoubtedly a demographic dividend that works to the advantage of the technology sector.

India has a strong heritage in IT services stemming back to the 1980s when India provided agile and robust SaaS solutions to global markets. India’s strong links with its colonial past mean English is widely spoken. Officially there are over 130 million English speakers across the country, the second highest in the world after the US. There are over 1.5 million new engineering graduates entering India’s job market each year, making it the second highest talent hub in the world, after mainland China.

With this backdrop, India’s burgeoning technological evolution - indeed, revolution – has become a reality and, given it was a core pillar of PM Modi’s move to a more robust and self-reliant India, the country is well on the way to achieving that goal.

India’s digital generation are early adopters, enjoying the warm embrace of the world’s largest 4G network, low-cost data accessibility and widespread smartphone use - India has more than 1.1 billion smartphone users. Naturally, eCommerce and digital banking services have accelerated at a speed that reflects this classic technology leap, experienced by all emerging markets.

It is also instructive to factor in India’s sizeable pool of increasingly affluent workers, consumers and investors – expected to comprise of 1 billion people by 2030 (World Economic Forum) - around 70% of the population. Digitization has transformed life in India’s vast expanse, creating a mass of consumers from city to hinterland and promising a tremendous pool of opportunity now and in the future.

A recent paper ‘Digital India : The $1 trillion Opportunity’ positions India as the world’s fastest growing digital economy. It notes that India is well on the way to unlocking $1 trillion in value (from ~$250 billion in 2020) and will account for over 25% of India’s overall GDP by 2025. The PEVC sector is eager to participate in this opportunity, so India’s digital economy is definitely one to watch.

Access for all? …. Caveat Emptor

In common with any new investment growth market, as confidence rises and demand grows for access to India’s PEVC story, it is important to note the attendant risks. There are liquidity, valuation and exit terms to be considered, each providing a long list of due diligence to complete and monitor. The particularly porous nature of PEVC target firms also need close attention. Deep research, checks and balances within any investment, operation or monitoring procedure is absolutely key.

Given that PEVC target firms are often working with third parties, this does also require caution. Fraudulent activities – and not just from within – but by and on portfolio companies invested in and third parties being dealt with are certainly more possible. In particularly challenging moments, when economic survival is threatened, a blurring between what’s acceptable and unacceptable behaviour can occur. Fraud does occur, in all markets, like in the cases of TAL Education Group and Luckin Coffee (Source: KPMG).

"The checks and balances call for careful, robust monitoring and clear preventative protocols to be firmly in place."

The checks and balances call for careful, robust monitoring and clear preventative protocols to be firmly in place. With distressed deals in particular, manager selection, KYC and deep (even forensic) levels of pre-investment due diligence are required.

Experienced PEVC investors know this, but window dressing is a real risk too. Operations may present healthy profits but upon further investigation, accompanying financial reports do not tally up. WeWork’s infamous ‘Community Adjusted EBIDTA’ is an example of how a company can manipulate and misrepresent financials. As with any PEVC investment, caution is encouraged.

With engagement, review and investment in target firms happening at an increasingly speedy pace, cybercrime also needs solid consideration, as do data breach and IP theft. India’s regulatory landscape – whilst certainly having been adapted and refined of late – remains complex in many parts. This is particularly so when the threads of central, state and local municipal authorities each need to be understood and stitched into a transaction. Wishing to transact speedily within such a framework certainly calls for caution.

Additionally, both governance and sustainability factors are being more deeply reviewed. For many PEVC funds - particularly the global heavyweight firms who are already in or are entering the market - investing in certain portfolio targets will require substantive change so that their own internal protocols and investment-ready permits are met.

Where target companies do not exhibit the same robustness around their governance and ethics framework that foreign investors in particular are used to, there will be pressure for change in the sector. Funds are now addressing these areas actively with target portfolio companies; imposing change requirements on each company and closely monitoring for implementation.

Some of these differences in business culture will likely cause tension and perhaps a delay in engagement but, most importantly, we will ultimately best practice across the board and a stronger and more robust Indian PEVC sector.

Conclusion

Being or investing in a unicorn is a rather tantalising proposition. India’s PEVC sector has laid the foundations for local and global investors to fully engage. With India’s strong economy, an evolving and progressive regulatory framework, combined with a highly entrepreneurial landscape, there will undoubtedly be great opportunities ahead.

If you enjoyed this article, be sure to read CAIA Association’s new report, The Rise of India’s Private Equity Market.

Footnotes:

About the Author:

Jo Murphy has been in Asia for over 20 years, predominantly based in Hong Kong but with two valuable years spent in Singapore. She has held several senior Asia Pacific wide management positions, successfully leading sales, business development, marketing and client relationship management divisions for major institutions; and has both built and managed large and effective regionally located teams.

Jo was expatriated to Hong Kong, with Morgan Stanley, in early 1997 and has worked for several global institutions; covering intermediary, buy and sell side, entrepreneurial and now in a professional education business environment - throughout the Alternative Investment industry.

In 2000, Jo joined HSBC Securities Services (previously Bank of Bermuda) as Head of Sales, Asia Pacific (based in Hong Kong) and in 2005 moved on to Head of Sales Asia (ex-Japan) and Product Specialist for all alternative investment products at Deutsche Asset Management (in Singapore). In 2008 Jo joined Triple A Partners, a privately held group. In early 2012 Jo joined the Chartered Alternative Investment Analyst (CAIA) Association, the international leader in alternative investment education and provider of the CAIA designation, as Managing Director, Asia Pacific.

Jo enjoys the reputation of being hard-working, capable, committed and commercial; was voted “Asia’s most influential woman in the alternative sector” and also one of “The 25 most influential people in Asian hedge funds” by the industry’s leading AsianInvestor magazine. Jo also was a founding member of the Hong Kong AIMA Chapter, previously held an Executive Committee Member position and now sits on its Education Committee. Further, she also holds a number of corporate advisory positions, is a Fellow of SUSS (Singapore) as well as an advisory council member of UPACA Gurukul (India).