By the Thinking Ahead Institute.

Performance Confidence

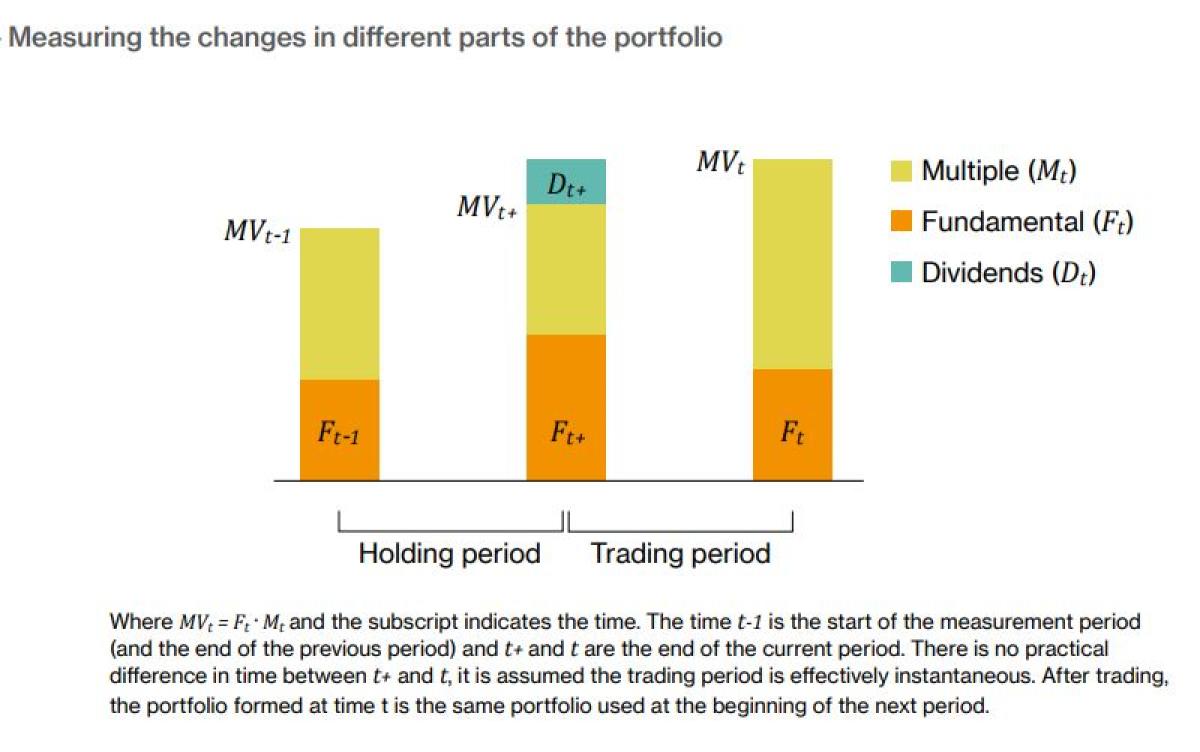

Retaining sufficient confidence in an under-performing, but high-quality, asset manager has long been a challenge for asset owners, not least for those who are minded to be long term. The investment industry has always struggled under this form of short-term pressure, exacerbated by traditional performance reporting, and many mandates have been terminated for the wrong reasons and at the wrong time. This short-term behavior prevents our benefitting from the long-term return premium (LTRP). While looking closely at this problem, when searching for and quantifying the LTRP, we started research into an alternative approach: Fundamental Return Attribution (FRA). This new attribution and monitoring framework – which had input from Baillie Gifford, MFS, S&P Dow Jones Indices and WTW - separates a portfolio’s returns into three main components:

- The growth of the portfolio’s fundamental characteristics (growth return)

- The change in these fundamental characteristics due to changes in the portfolio’s holdings (activity return)

- Returns arising from changes in market sentiment (multiple return).

In our view, decomposing returns into these three components enables a deeper understanding and assessment of how an investment strategy generates returns. Compared to more traditional attribution methods (that focus on explaining returns by reference to the performance of different groupings of securities), this approach considers how the decisions of the asset manager within their investment process generate the portfolio’s returns. The FRA approach separates out returns arising from changes in short-term market sentiment (essentially noise and, arguably, mean-reverting around zero impact over the long term), enabling a longer-term outlook by asset owners and asset managers when evaluating recent performance or setting future return expectations.

The FRA framework can be applied to all asset classes but, as with any single measurement methodology, it may be more applicable to some mandates than others. Currently, it has been applied to portfolios using company fundamentals, but there is potential to apply it to other characteristics that investors increasingly wish to monitor or manage in their portfolio.

While the FRA methodology is already being used by some members to assess equity managers, in future we think it will have broader applications. For example, it may be able to support investors who seek to align their portfolios to ESG objectives but are struggling to identify if a portfolio’s decarbonization is, for instance, due to underlying companies reducing emissions or the divestment of high-emission companies. We believe this framework could provide much needed clarity into how ESG objectives are being managed and achieved. But it will require an enhanced version of the tool.

And this is one of the main reasons we opted to open-sourced the underlying computer code (on Github.com) – to access cognitive diversity on a grand scale and stimulate real innovation. If the industry responds positively, it could kick start a real change in the way investors think and act around investment performance and how it is reported. And in turn it should improve the quality of conversations between asset managers and asset owners about the long-term return drivers of an investment strategy, particularly during periods of underperformance. This may prove quite helpful in the predicted period of significant turbulence.

Conclusion:

The proposed framework is a broadly applicable approach to separating a strategy’s returns into returns due to growth in the intrinsic value of the portfolio and returns due to changes in market sentiment. An asset manager can control (either through direct action or previous asset selection) the change in a portfolio’s intrinsic value, but market sentiment is generally outside an asset manager’s control.

By using this framework to decompose returns an asset owner and asset manager can engage on the investment decisions taken by the asset manager, and the resulting outcomes, to build a meaningful dialogue about the investment strategy and whether it is profiting from return sources that are likely to persist in the future. This framework is able to allocate returns between the current decisions of the asset manager (trading activity), consequences of past decisions (underlying growth) and the impact of broader market sentiment (multiple returns) over time with reference to a suitable proxy of the portfolio’s intrinsic value or other attribute of interest.

“We believe this framework provides a relatively new and comprehensive approach to evaluating the returns of an investment strategy. Contrary to established approaches this framework captures the influence of different aspects of asset manager decision making over time...”

Our grateful thanks go to members: Baillie Gifford, MFS and S&P Dow Jones Indices, for their time, insights and expertise in assisting the production of this research and for supporting the vision to turn this research into innovative: Access the open-source code

Read the original article here: Original Article

Interesting videos: Fundamental return attribution framework and open-source code - Thinking Ahead Institute

References

Philip U. Straehl and Roger G. Ibbotson. The long-run drivers of stock returns: Total payouts and the real economy. Financial Analysts Journal, 73(3):32–52, August 2017.

Jesse Livermore, Chris Meredith, and Patrick O’Shaughnessy. Factors from Scratch: A look back, and forward, at how, when, and why factors work. O’Shaughnessy Asset Management, May 2018.

Arnott, R.D., Harvey, C.R., Kalesnik, V., Linnainmaa, J.T., 2019. Reports of Value’s Death May Be Greatly Exaggerated. SSRN Journal. https://doi.org/10.2139/ssrn.3488748

About the Thinking Ahead Institute: The Thinking Ahead Institute seeks to bring together the world’s major investment organizations to mobilize capital for a sustainable future. Arising out of Willis Towers Watson’s Thinking Ahead Group, formed in 2002 by Tim Hodgson and Roger Urwin, the Institute was established in January 2015 as a global not-for-profit research and innovation group comprising asset owners, investment managers and service providers. Currently it has over 50 members with combined responsibility for over US$12trn.

Limitations of Reliance: This document has been written by members of the Thinking Ahead Group 2.0. Their role is to identify and develop new investment thinking and opportunities not naturally covered under mainstream research. They seek to encourage new ways of seeing the investment environment in ways that add value to our clients. The contents of individual documents are therefore more likely to be the opinions of the respective authors rather than representing the formal view of the firm.