By Arnim S. Holzer, Global Macro Strategist and William Visconto, Co-Founder, Portfolio Manager at Easterly/EAB Risk Solutions.

Executive Summary

This paper is an analysis of equity volatility and its impact on portfolio correlation and diversification. By examining a standard institutional asset allocation against a Hedged Equity approach, our research has found that correlation management is key to accessing the benefits of diversification. By analyzing volatility regimes and their impact on correlations to equity (S&P 500), we observed how asset allocation can improve by focusing on moments of volatility and equity vulnerability. We chose a representative institutional asset allocation portfolio, the “Institutional Portfolio (IP)” (see Appendix) for comparison against both the S&P 500 and a Hedged Equity strategy during periods characterized by extreme volatility. Through statistical analysis, we show the beneficial impact of reduced downside correlation with a Hedged Equity strategy when compared to the increased equity correlation in the Institutional Portfolio. This provides specific insight into why accepted diversification concepts may fail during times of market stress. Past bull markets may give way to more prevalent bear markets as concerns about equity valuations, inflation and less stimulative FED policy arise. In that case, traditional diversified portfolios could exhibit a higher probability of failure. As we demonstrate, there are significant advantages to allocating to equity correlation-reducing strategies, like Hedged Equity.

Background

The idea that muting volatility has value in portfolio management garnered attention after the dot.com bubble of 2000, and then became popular as an investment category after the Global Financial Crisis. Those strategies that focus exclusively on dampening volatility have the tendency to fail under the stress of the high volatility of deeper decline moves and have often found it difficult to show the benefits of volatility minimization as investors experience somewhat symmetric upside to downside capture ratios.

However, if equity volatility/correlation risk could be reduced at its simplest level, an investor could keep overall portfolio Beta reasonable and directly manage the long-term portfolio drag from deep losses. This would improve portfolio Sharpe ratios and strengthen adherence to long term asset allocation objectives, allowing for increased allocation to lower-liquidity and higher risk segments.

The two main approaches of volatility management are:

1. Derivatives-based approach - premium selling and/or buying; and

2. Underlying factor security selection-based approach

These approaches have frequently reduced downside risk but at the expense of lower upside capture. More importantly, because they focus exclusively on volatility minimization and fail to incorporate correlation management, these approaches can underperform precisely when they need to add value. Specifically, they can underperform relative to 'Hedged Equity' strategies that directly hedge portfolio downside risk by employing S&P listed (near to 6-week expiry) put and call options in a put spread collar structure.

In this article, we refer to a US Large Cap Hedged Equity composite that invests in the US stock markets going long with S&P 500 based ETFs and a total return swap on S&P 500 based ETFs and hedged with a spread collar structure that allows up to 30% leverage and 150% downside put spread coverage.

There have been three-month periods (or longer) of significant outperformance by a put spread Hedged Equity strategy versus the S&P 500 and what we refer to as the "Institutional Portfolio" on a risk adjusted basis, with significant insight to be gained from these periods. The IP portfolio is an institutionally-oriented asset allocation mix containing the following blend of asset and sector approaches.

While there is a broad range of allocation methodologies and different weightings, we think the above IP blend falls well within accepted ranges for many consultant-recommended and institutionally utilized asset allocations and reasonably approximates how many real-world committees are currently managing risk.

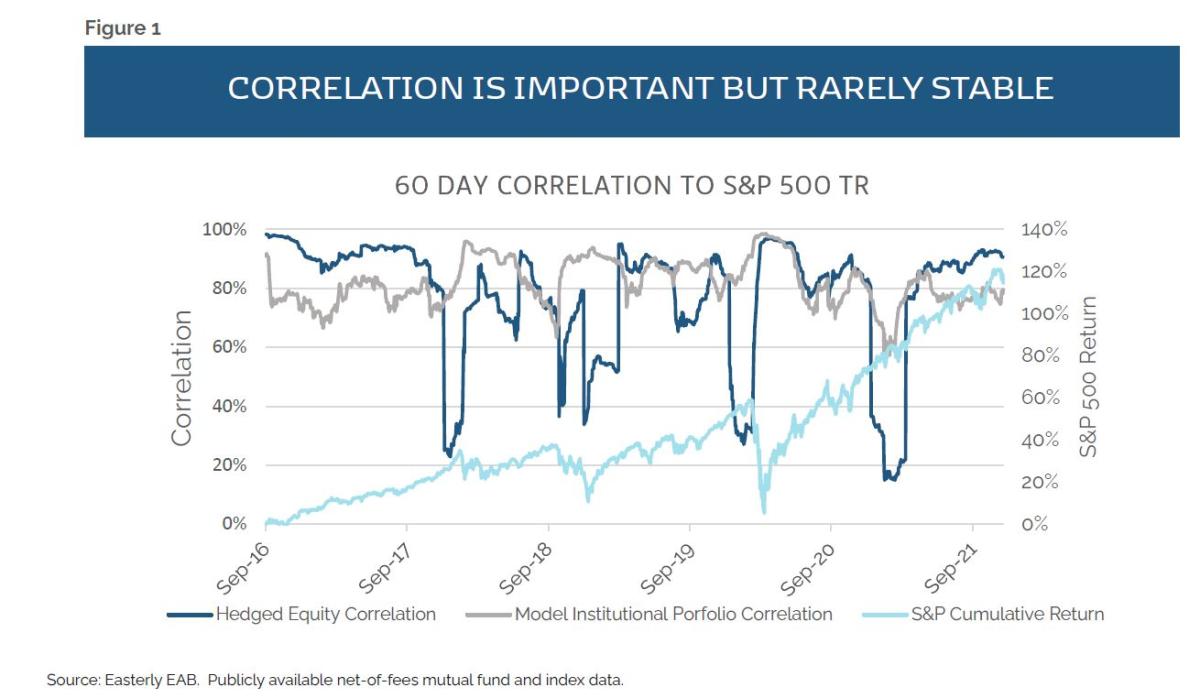

As seen in Figure 1, the correlation of diversified portfolios, such as the Institutional Portfolio (IP) to the S&P 500, often have greater correlation than their allocation to equity would infer and exhibit increased correlation when the S&P 500 declines. Hedged Equity’s realized correlation performs quite differently in these environments where the value of variable correlation (i.e., lower decline and a quicker to recovery characteristic), becomes apparent.

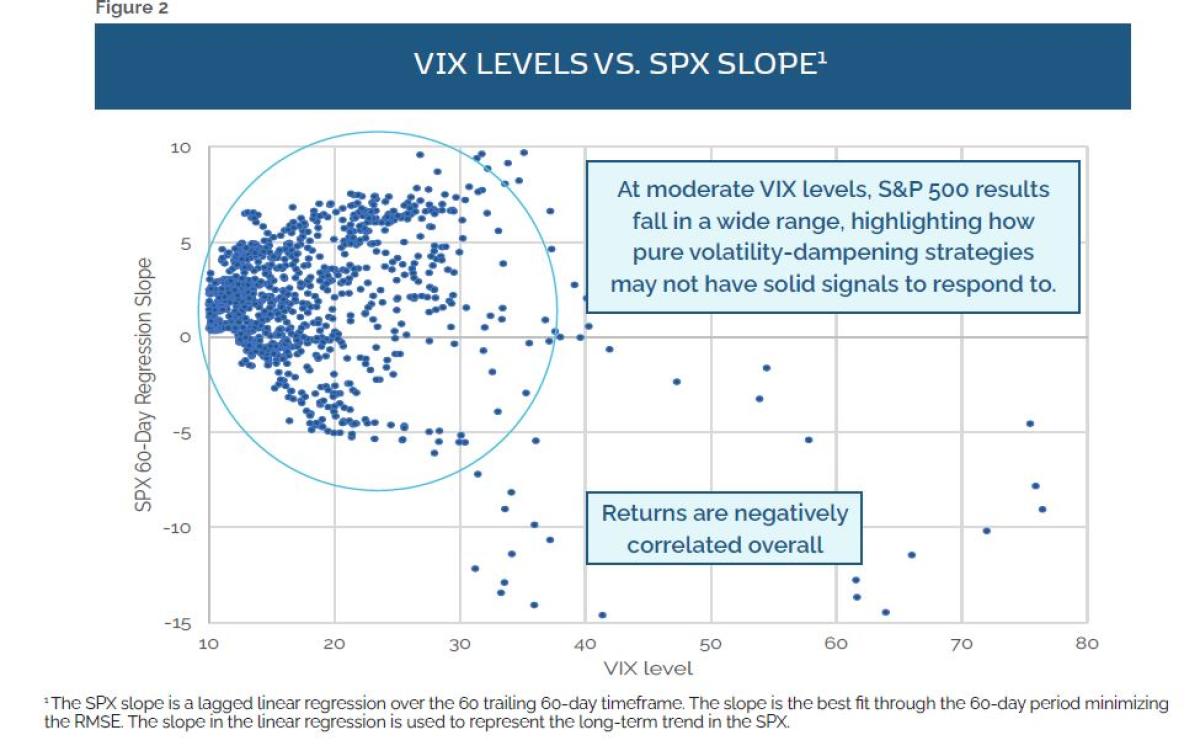

It’s also important to recognize that most asset allocation construction is based on long term average returns, volatility, and correlation forecasts. Because of the impact of extreme volatility on correlations, the actual performance of asset allocation/diversification can significantly differ from the expected performance. As a result, the optimization of diversification using historical averages falls short of its goal. Therefore, we have identified the characteristics in moments of extreme volatility that need to be addressed to optimize diversification. We performed a regression analysis of the VIX against the S&P 500 to better understand the relationship of volatility to S&P 500 price levels. (Figure 2).

Interestingly, our results show that the VIX itself did not provide any meaningful signal for S&P 500 values or direction, meaning that with the VIX between 15 and 30 the S&P 500 could be positive or negative on a daily basis. This is very important as it challenges the idea that traditional volatility minimization has a repeatable information ratio. Volatility management is important, but to find the real story and see through the noise in the relationship between the VIX and S&P 500 a regime analysis must be done. Because much of the volatility and equity correlation data is noise within normal ranges of volatility, they can mask the value of the more extreme periods.

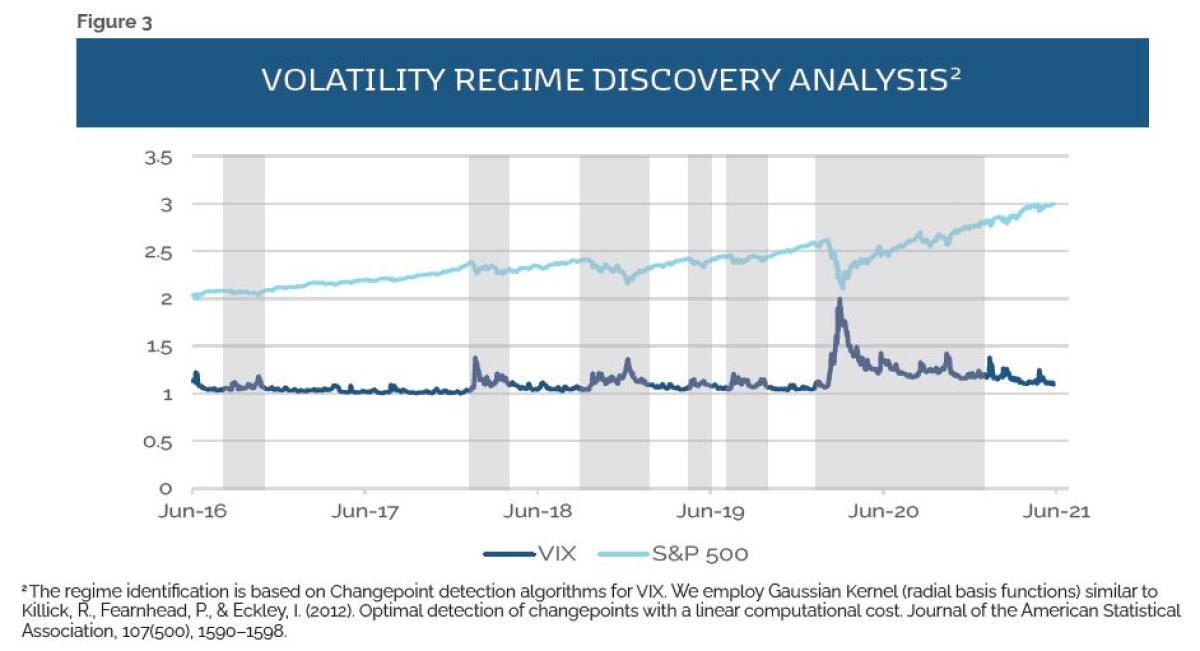

While one may think these extreme periods are only tail events, they are not. We show that over the last five-plus years there have been six such events (see shaded areas in Figure 3). When volatility moves outside of normal ranges, there is a tendency for the impact on security, sector, and asset class correlations to create unpredictable performance. In analyzing efficient portfolio diversifying approaches, we examine the periods most likely to create disruptive performance. We believe any approach not considering that tendency will lead to poor diversification performance. Post-mortem analysis of significant events and diversification failures often attribute this asset allocation and/or manager failures to unpredictable and idiosyncratic results. Furthermore, we believe it is possible that diversification and manager failures in these moments may be due to an inability to manage Beta expansion of extraordinary correlation moves that take place in extreme volatility regimes.

As Figure 3 highlights, with spiking levels of volatility, equity returns often turn negative. Due to the tendency of high volatility environments to increase Beta, these are the moments of diversification risk that must be addressed to preserve portfolio value. As a result, decreasing correlation to equity in those moments is a vital component of effective asset allocation. In essence, a broad reduction of Beta can prove to be inefficient relative to a managed reduction during stress events.

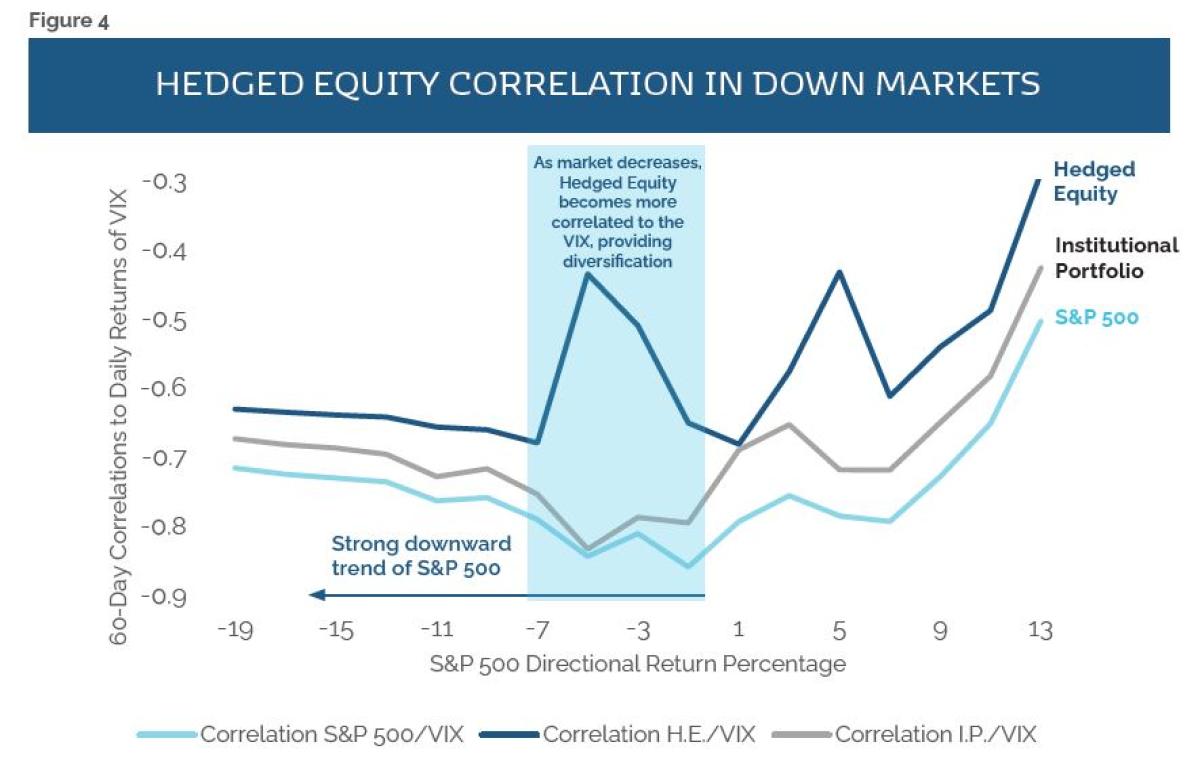

As correlations between Hedged Equity and S&P 500 decrease, there is a clear increase in correlations between the IP and S&P 500, revealing a consistent pattern of return degradation for the IP portfolio (see Figure 4). The data shows that during periods of extreme volatility, the diversification provided by the IP does not meaningfully reduce correlation to S&P 500. The Hedged Equity correlation, in contrast, begins to drop at lower levels of decline (between -2% and -7%) and provides a different return profile than the S&P 500 or the IP.

Another important feature of these drawdowns has been the potential of a change in risk premia post-event because market participants demand higher returns for the new information in the market. As the Hedged Equity approach uses volatility as one of its inputs, it responds well to moments of stress and residually high post-event volatility and correlation. It collects higher volatility premiums from its call sales, but also maintains its managed correlation versus the S&P 500. That contrasts with the IP, which suffers higher-return premiums and remains highly correlated. From the chart above (Figure 4) one can see that as the S&P 500 moves into negative territory, Hedged Equity starts to correlate to the VIX, benefitting from the rise in volatility, whereas the S&P 500 and the IP decline. This highlights how the diversification value of the IP is reduced.

In the most prevalent zone of S&P 500 declines, in the -2 to -7% range, the Hedged Equity correlation increases to the VIX, which is distinguished from that of the IP and S&P 500, which do not benefit from volatility correlation. Even in deeper declines the hedged equity correlation to the VIX remains above that of the IP and S&P 500. The upward status of the hedged equity line through the range of down markets represents a greater sensitivity to extreme volatility moves and, therefore, functional diversification against the more poorly performing IP and S&P 500. If these negative S&P 500 moments represent risk-adjusted return drag for equities and the IP, the aggregate effect explains why the Sortino ratio of hedged equity exceeds that of the Sharpe ratio and why there has been such dissatisfaction with asset allocation during stress events.

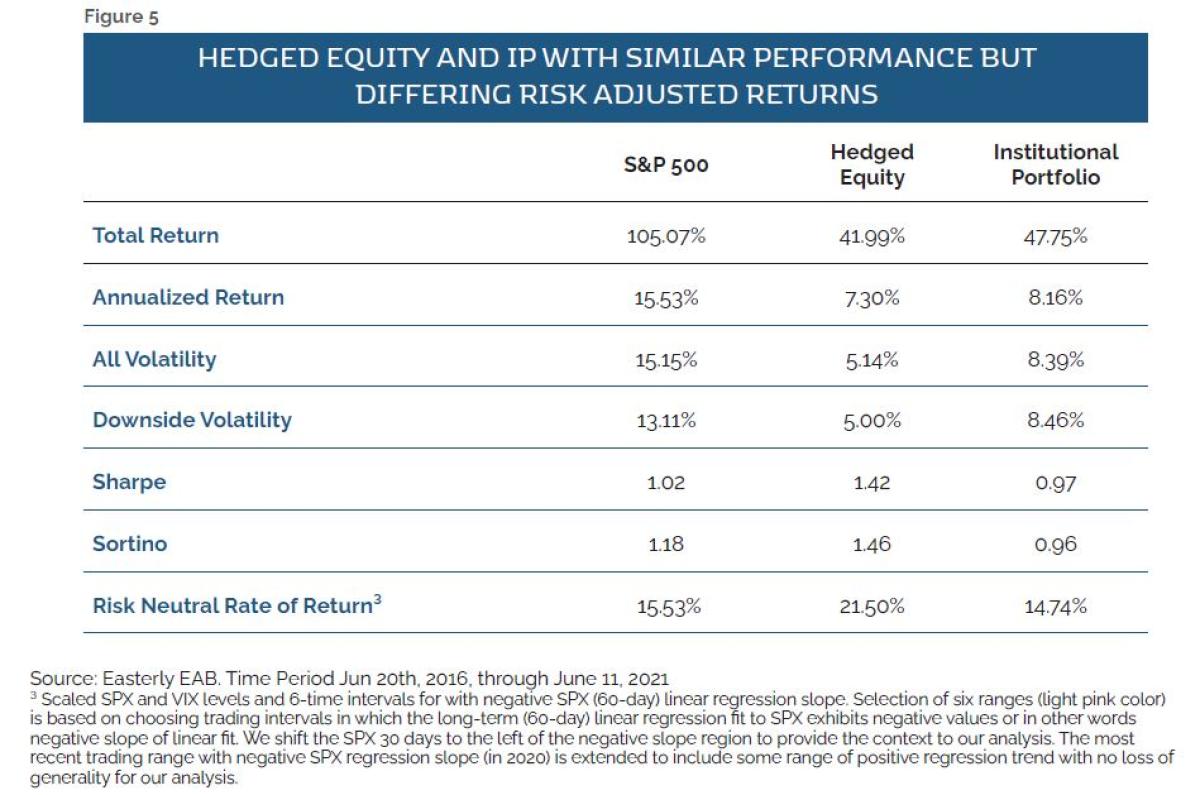

While the raw performance of the IP and Hedged Equity are similar, this analysis (see Figure 5) explains why Hedged Equity is a powerful diversifier, especially during periods of market stress. Despite the IP’s greater correlation to equities, its risk neutral rate (see appendix) of return underperforms Hedged Equity significantly⁴. This is evident when one sees the Sharpe and Sortino benefits of Hedged Equity despite a strong equity environment. If this occurs during a strong period for equities, it would only be logical to believe the noted risk adjusted return improvement of Hedged Equity in a bear market would be much more significant. The idea that the use of a managed correlation approach can offset greater Beta exposures elsewhere and still outperform an institutional asset allocation looks to have important implications for portfolios going forward. It is clear from the analysis that diversification is not a panacea, but utilizing managed correlation approaches, like Hedged Equity, that possess the specific characteristics that investors are targeting when they choose to diversify, can be strongly beneficial.

The Outperformance of Hedged Equity’s Sortino and Sharpe Ratios Matter

For most of the volatility minimization approaches that linearly or inconsistently manage their correlation to the S&P 500, we would argue that Sortino and Sharpe ratios prove difficult to use or compare as the ratios may be the result of timeframes analyzed or other active bets. As the managed volatility class targets diversification and risk management, we believe solid Sharpe and Sortino ratio analysis must be confirmed with predictably exhibited correlation patterns. We would extend that concept for the IP and its components. While the IP is allocated ~41% to equities, the portfolio correlations typically run above 80% (see figure 1). However, when evaluating the absolute and risk adjusted returns of the IP, it clearly underperforms. The Sortino ratio for the IP (see figure 5) shows there is little drawdown benefit, underperforming both the S&P 500 and Hedged Equity.

Conclusion

Correlation management provides a powerful diversifier to equity correlation risk that plagues portfolios. As many studies have focused on long term return periods that can be characterized as bull markets, there is a disconnect with the basic premise of diversification - the smoothing out of equity deep decline risk. If an investor is targeting maximum return, one would not diversify away from equity and equity-like assets. Therefore, we theorize that maximizing the defensive utility of a diversified portfolio is the only viable reason for diversification. In that case, the data shows that the Hedged Equity addition to the Institutional Portfolio is of significant value at overcoming the tendency for asset allocation portfolios to increase equity correlation risk under stress.

Key Findings:

- Standard diversification takes a static view of betas and correlations as being true to their long-term averages. We know that this assumption is false, and is a major reason why standard asset allocation, full long/short and other forms of risk-managed approaches often fail under stress.

- While Hedged Equity looks like a return dampener, in a blended portfolio looking for resiliency, it is not. This is because it allows portfolios to allocate more greatly to higher Beta and higher-return allocations, such as those in various private markets vehicles and concentrated strategies. We also find that once the initial equity declines occur, the Hedged Equity optionality and put position monetization allows for outperformance even as the equity market starts recovering.

- Conceptually, in the same way that Hedged Equity manages correlation in market stress events, there are opportunities to harvest correlation, or Beta expansion, that would likely also add to the robustness of portfolios. It is clear from the results of this analysis that any approach that can provide dependable correlation patterns to equities and standard diversified allocations, but can also respond positively to VIX increases, would provide similar benefits as a component of those portfolios. This is more important than optimizing to long term average volatility and correlation forecasts.

- Finally, it also should be noted that the Hedged Equity performance was defensive in each of the studied

six regimes even if the level of responsiveness was not exactly the same. The combination of risk increase (VIX spike) versus equity decline, clearly impacts the dimension of return improvement. Interestingly, the defensive characteristics however remained in place providing a lower degree of correlation as declines ensued. We believe that makes the case for systematic hedge positioning versus discretionary hedging. One cannot know when events will occur, so being consistently and systematically positioned is a key component to diversification.

Appendix:

The Institutional Portfolio: The IP was rebalanced annually in the data set to allow customary drift but at the same time reasonably approximates how a real-world committee would reset allocations to manage risk. Institutional Portfolio components use recognized indices or ETFs as publicly available.

Easterly EAB Hedged Equity Approach: The US Large Cap Hedged Equity composite invests in the US stock markets going long with S&P 500 based ETFs and a total return swap on S&P 500 based ETFs and hedged using S&P listed (near to 6-week expiry) put and call options in a put spread collar structure to manage risk.

Optimization of the Institutional Portfolio and Hedged Equity - Standard Optimization and Monte Carlo Probability Distributions.

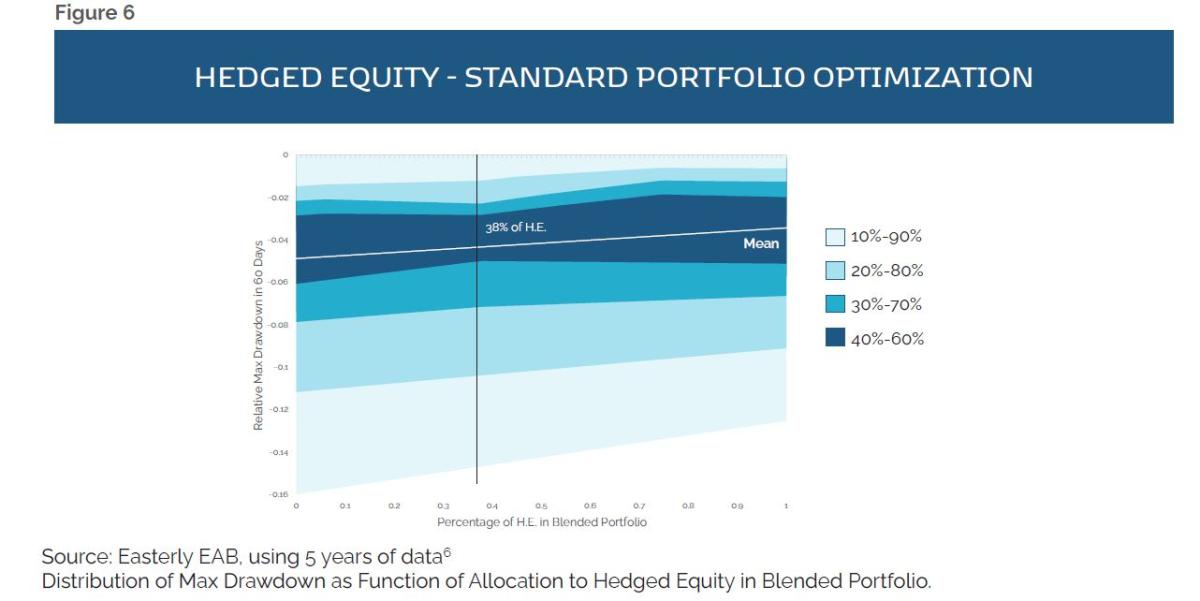

To test the hypothesis of whether Hedged Equity improves the diversification benefit of the Institutional Portfolio in declining markets, we performed an optimization using high volatility regime periods. The optimization focused on finding the percentage of Hedged Equity, when added to the Institutional Portfolio, most reduced the risk of drawdowns (see Figure 6). As one can see, adding Hedged Equity provides better results across a range of allocations, but there is a visible tightening in the 30-40% allocation range. This reflects the importance of correlation dampening strategies when many of the underlying assets in the Standard Portfolio experience correlation expansion. To understand the implications of this optimization, we have performed a Monte Carlo analysis to arrive at return probability distributions for the Institutional Portfolio and the portfolio including Hedged Equity for a hypothetical one-year volatility regime-oriented period⁵.

.

To highlight the benefits of correlation management, an optimization was performed to demonstrate the power of downside beta management. While we are well aware that a 38% allocation to a single strategy presents practical challenges, the optimization nonetheless shows the benefit of Hedge Equity characteristics. A 38% Hedged Equity allocation to the IP tightened the range of approximately one standard deviation results (the 40%-60% range of max drawdowns) seen over rolling 60-day periods. As the range is visually crimped at about 38%, this is viewed as the optimal allocation to minimize max drawdowns. It is also clearly visible that as the allocation to Hedged Equity increases, the range of max drawdown tightens, and the mean decreases, as shown by the solid black line.

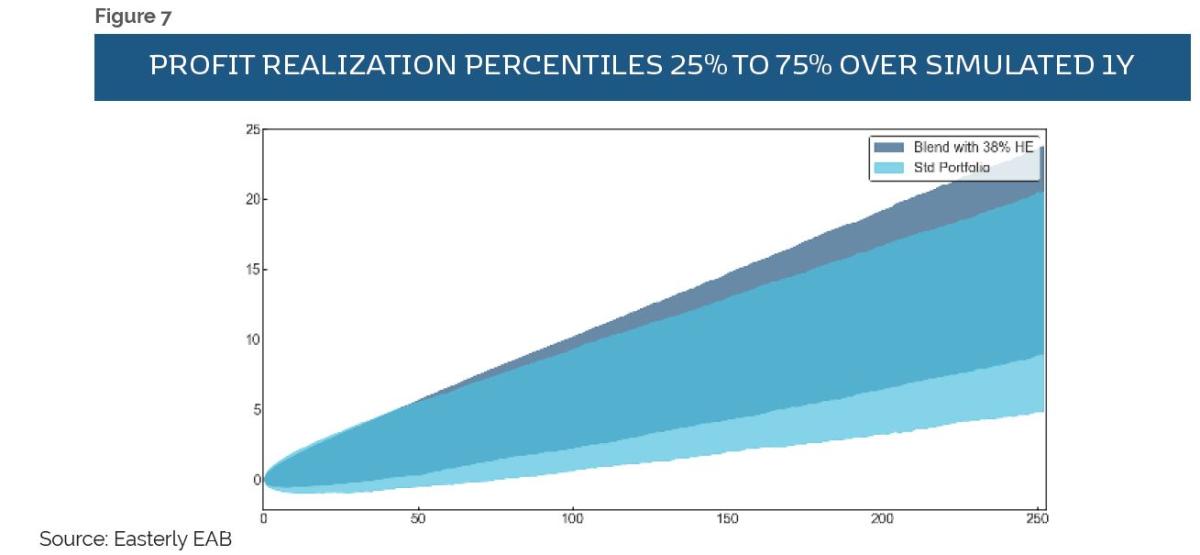

Monte Carlo analysis and probability distributions show the benefits of adding Hedged Equity to the IP in terms of overall performance, drawdowns, and tightening of expected return ranges.

Monte Carlo analysis and probability distributions show the benefits of adding Hedged Equity to the IP in terms of overall performance, drawdowns, and tightening of expected return ranges.

The one-year bear market simulation shows that the blended portfolio (see Figure 7) starts to improve the range of return within months, particularly relative to the IP.

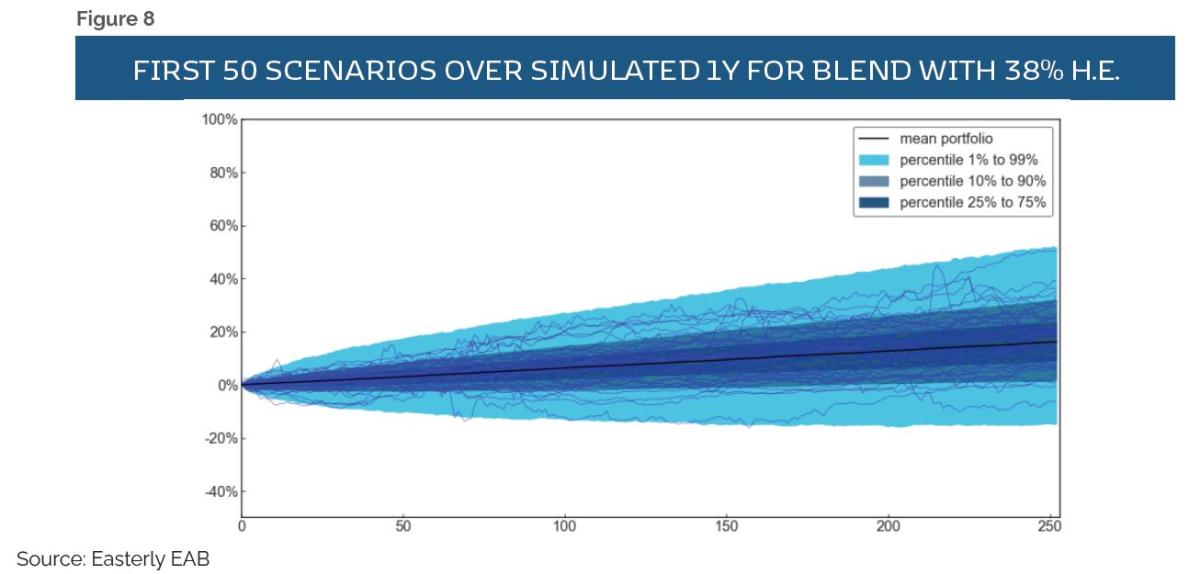

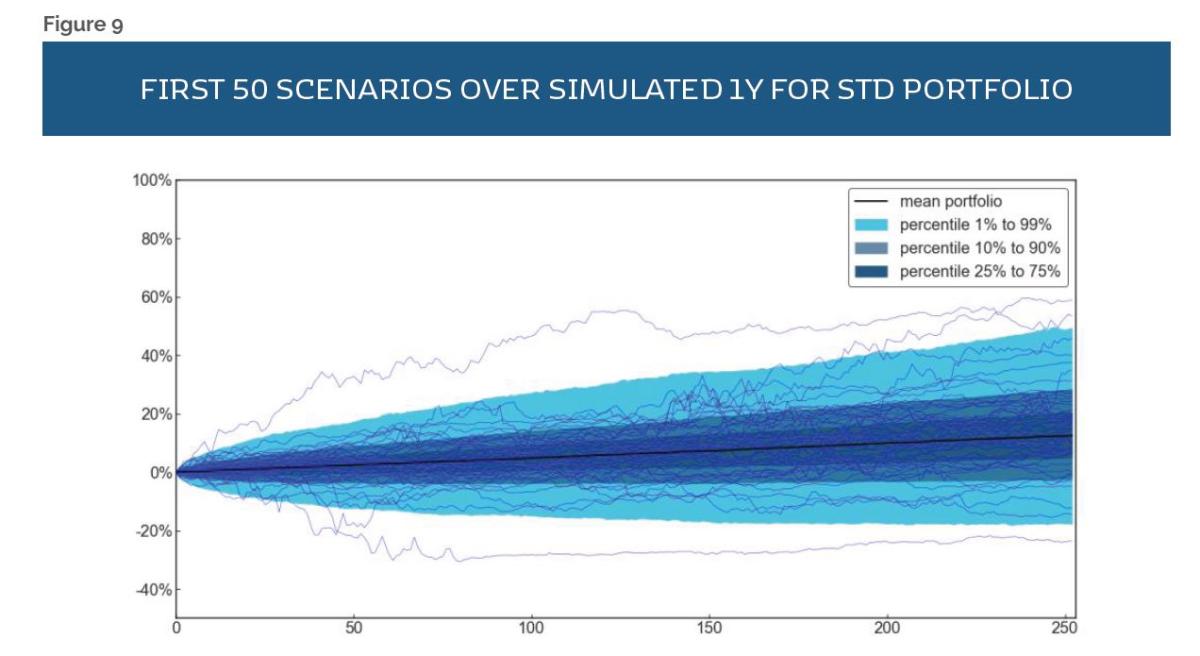

Another way to look at the simulation is to examine the first 50 scenarios (figure 8) to get an idea what possible performance paths could look like. As one examines these paths for the IP along with the blended portfolio one sees a tighter distribution for the blended portfolio relative to the IP which possesses the potential for “rogue” tail-oriented paths not present with the blended portfolio.

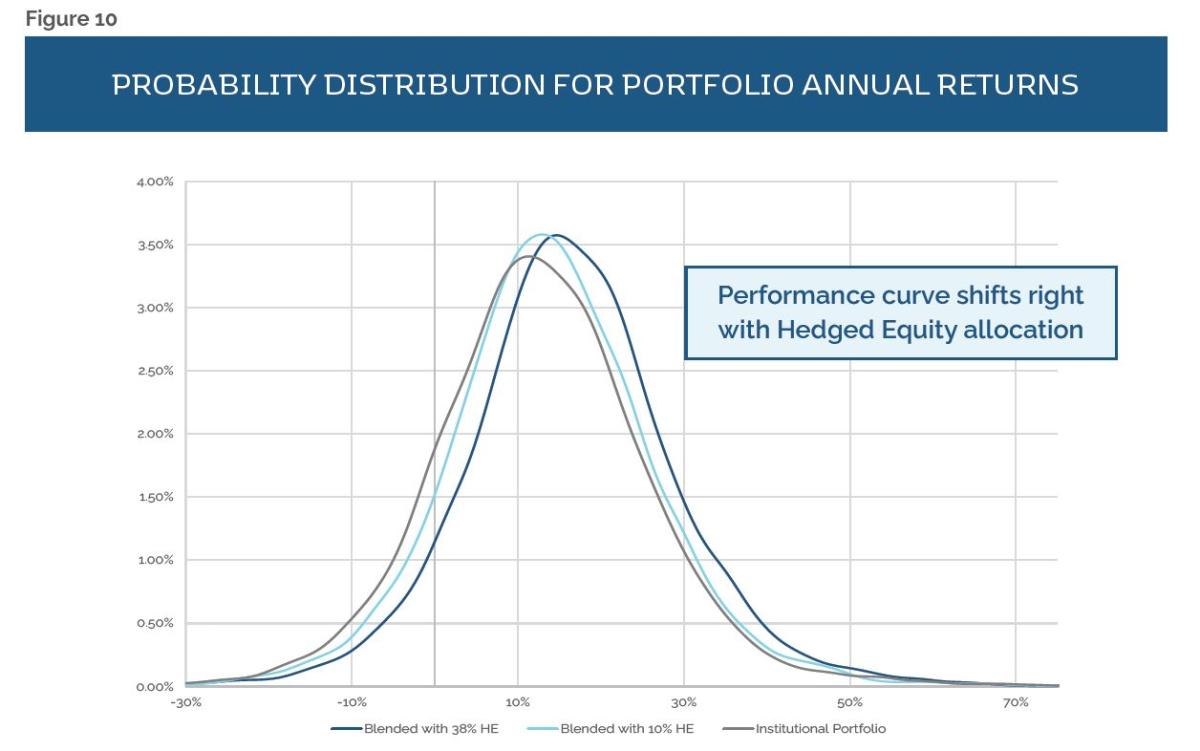

Using a robust 10,000 sample scenario run, the benefits of allocating to Hedged Equity are clear, on average, with a reduction in the depth and number of drawdown occurrences. This leads to the performance curve shifting to the right, connoting better returns and lower drawdowns (see Figure 10) with the Institutional Portfolio having the tendency to produce extreme and unstable downside occurrences not seen in the blended portfolio. The fact that the simulation shows higher upside under stress scenarios counters the common belief that using Hedged Equity reduces return and alpha while muting volatility compared to a standard asset allocation.

About the Authors:

Arnim Holzer is the Global Macro Strategist and Client Portfolio Manager at Easterly EAB Risk Solutions.

He has over 40 years of global macro and multi asset experience. Arnim has served as Chief Investment Officer, Strategist, Portfolio Manager, and Client Service and Marketing executive at several firms over the past 30 years. His investment philosophy is a unique blend of fundamental, technical and, quantitative disciplines honed over the years of working with many of the top firms and investors in each of these disciplines. His particular macro skill is understanding the relationships of correlation and volatility in the optimization of portfolio construction and return generation. Prior to EAB, Arnim founded a tail risk consulting firm, ASH Strategy, LLC, where he developed a novel multi asset hedging approach for institutional, high net worth, and family office investors. For 6 years he managed or served as senior strategist on multi asset funds or strategies at Deutsche Asset management and Scudder. While at Deutsche he was the portfolio manager on approximately $3 billion of assets in domestic and offshore multi-asset funds. He also founded and managed a multi asset offshore hedge fund at Israel Discount Bank of New York. Arnim received his undergraduate Economics degree from Princeton University and his MBA-Finance from Fordham University. He holds a Series 7 and 65 Registered Representative securities registration.

Bill Visconto is the Chief Operating Officer and Portfolio Manager at Easterly EAB Risk Solutions. Prior to EAB, Bill was a head volatility trader at McGowan Investors LLC.

His responsibilities were to implement the firm’s strategy in the volatility arbitrage space and deploy the firm’s capital to maximize returns. Before joining McGowan, he was Co- Founder of Volare Capital, a hedge fund that pursued statistical/volatility arbitrage strategies in index and single stock options. Bill was the Head of Portfolio Management and Trading Floor Operations for PFTC Advisors and PFTC Trading. At PFTC, he was responsible for managing a team of 4 portfolio managers and 17 floor traders. PFTC Trading was one of the largest liquidity providers in the United States. Bill received his B.S. in Marketing from the University of Scranton. He holds his FINRA Series 7, 63, 65 licenses and is a CFA Level 3 Candidate.