By Todd Trubey, senior manager research analyst for Morningstar Research Services LLC, a wholly owned subsidiary of Morningstar, Inc. He covers multi-asset and alternative fund strategies.

Multi-Asset Income Funds: Is the Extra Income Worth the Extra Risk?

While all the major asset classes have collectively taken a beating this year, multi-asset income, or MAI, funds have held up comparatively well. In the first five months of 2022, the three most crucial markets for U.S. investors—domestic stocks, international stocks, and U.S. bonds—have tumbled nearly in lockstep. Specifically, through May 31, the Morningstar US Market Index dove 14.1%, the Morningstar Global ex-US Index fell 10.3%, and the Morningstar US Core Bond Index dropped 9.0%. Meanwhile, the 68 mutual funds we identify as multi-asset income slid an average of just 7.4%. In other words, they have recently been more buoyant than the broad markets—despite devoting an average of 45% of assets to equities.

Those results might make you think these funds are solid capital-preservation tools. But portfolios that offer sustainable, repeatable downside protection generally do so because their design includes some combination of cash, short-term fixed-income, and holdings with low intercorrelation. Multi-asset income funds, on the other hand, exist specifically to distribute attractive levels of income, so most of them eschew low-yielding bonds and hold different assets based on income potential more than for diversifying characteristics. In other words, the multi-asset income fund group may occasionally do well in a downturn, but that’s by chance—not by plan.

While these funds have done well in this downturn, they don’t always play strong defense: Just two years ago in the pandemic panic, most of them plummeted. Their heavy emphasis on income has meant that, inside most of these multi-asset packages, two subasset classes usually take up a lot of space. And these two sub-asset classes, high-yield bonds, and large-value stocks can move together in a downturn—sometimes for better and sometimes for worse.

The Origins of Multi-Asset Income

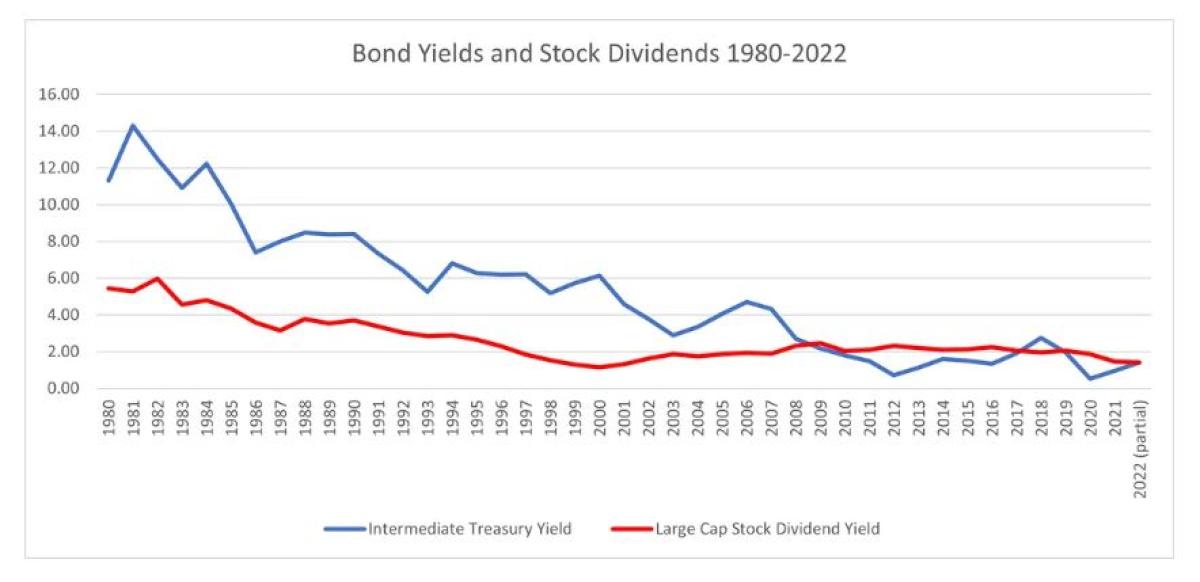

It’s obvious why investors would want an investment to produce income and almost as clear why they’d want it to come from more than one asset class. Most people invest primarily to secure comfortable retirements—specifically to generate dependable, stable, long-lasting levels of income, ideally without quickly or sharply cutting into principal. And most investors would rather not put all their eggs in one basket, as the proverb goes. Traditionally, mixing stocks and bonds has seemed prudent. But over the past four-plus decades, using a straightforward mix for income in retirement has become far more challenging as bond yields and aggregate stock dividend yields have steadily, significantly declined.

Four decades ago, in 1980, intermediate-term Treasuries yielded 11.3% and large-cap stocks yielded 5.5%. By April 30, 2022, both intermediate government bond yields and stock dividends had cratered to 1.4%. An even mix of bonds and stocks produced a roughly 8.4% portfolio yield in 1980; at the end of April 2022, the same blend only generated a 1.4% yield.

- source: Morningstar Direct; IA SBBI Indexes. The IA SBBI US IT Government Yld Index tracks Intermediate Treasury Yields The IA SBBI US Large Stock IR Index tracks the monthly income return of the S&P 500.

For retirees looking to replace paychecks with income, a once-simple determination has become a baffling challenge. Many investors hope that multi-asset income funds are part of the solution.

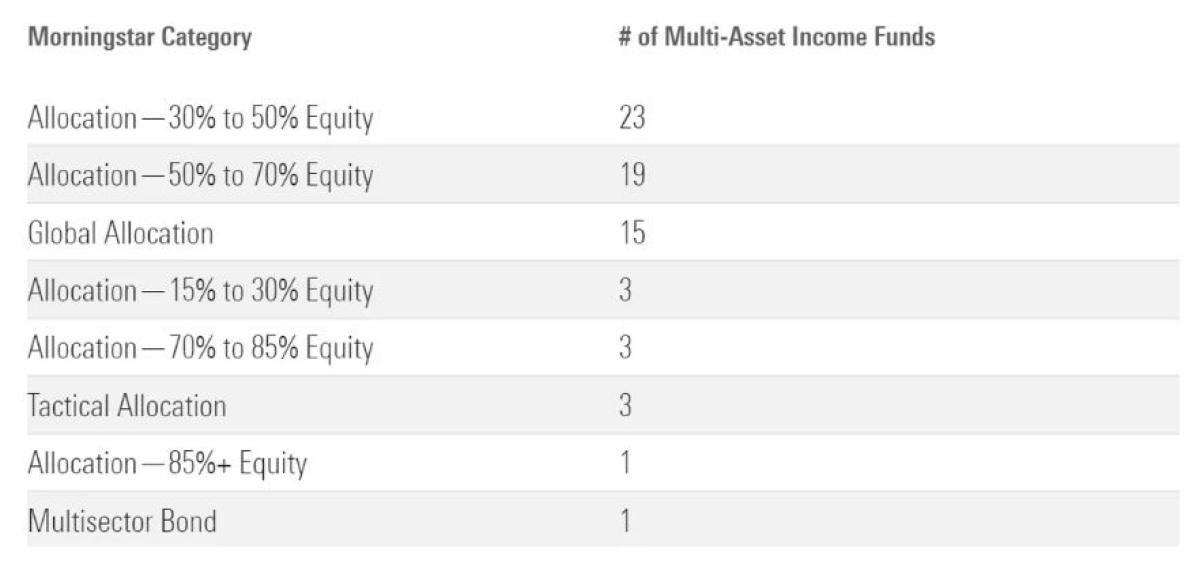

The core idea behind multi-asset income funds is straightforward: a portfolio that aims to provide income from a variety of assets. To be clear, Morningstar doesn’t group multi-asset income funds into one Morningstar Category because the funds collect income from a wide array of asset-allocation schemes, and holdings exposures drive our category system. We do have a separate multi-asset income institutional category that tracks 68 funds with two key things in common: All actively focus on income, and they have more than one asset class in their portfolio. All but one (Delaware Wealth Builder (DDIAX)) have “income” in their name: 13 contain the phrase “multi-asset income” and another 14 use “income builder.” The 68 funds spread across eight conventional Morningstar Categories, mainly congregating in three:

- source: Morningstar Analysts

These funds have consistently provided yields well above their own category peers that don’t intentionally focus on income. As the saying goes, however, you can’t get blood from a turnip. In an investment world where yields (especially in fixed-income) remain below their historical averages—even after the sharp rise in bond yields in 2022—few assets provide the kind of truly attractive yields that were once commonplace. Moreover, those investments producing higher income generally carry some type of added risk.

So, while most portfolios that mix multiple asset classes aim to offset the characteristics of one asset with counterbalancing traits from another, multi-asset income funds tend to lean heavily on subasset classes whose behavior has some key similarities. Specifically, the large-value equities these funds overweight tend in some ways to be a rather bondlike group of stocks given their attractive dividend yields and sedate profile (relative to other stocks). And in the fixed-income sleeves of multi-asset income funds, there’s heavy emphasis on high-yield bonds, whose sensitivity to companies’ creditworthiness makes them more volatile than other types of bonds (although they’re generally only about half as volatile as equities). Plus, high-yield bonds often slide when stocks do—just when higher-quality bonds tend to serve as ballast. Overall, multi-asset income funds have succeeded in generating plump yields, but that’s because they have heavy concentration risks in areas such as high-yield bonds and large-value equities, meaning the multi-asset income funds can fall much more than one would expect when risk becomes reality.

A Popular Potential Solution

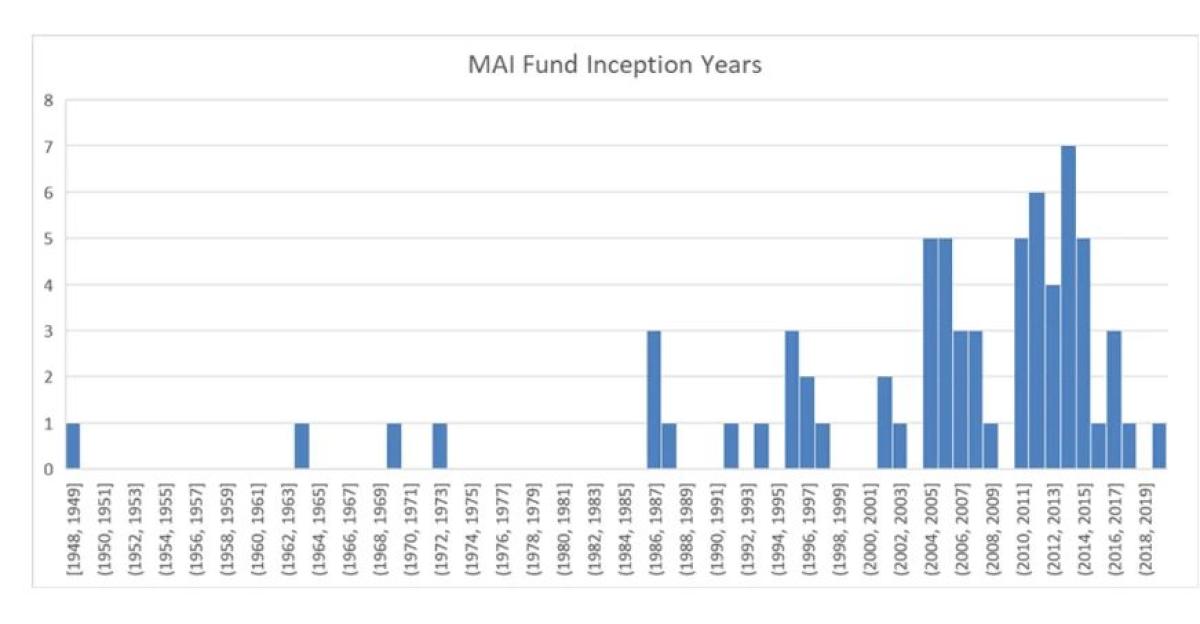

While they’ve proliferated since the global financial crisis from 2007-09, multi-asset income funds aren’t an exclusively recent phenomenon. About half of those existing today were launched in the last decade, a quarter in the previous decade, and the remainder before 2000. (Not all of them—especially the older ones—have always been multi-asset income funds. For instance, Goldman Sachs Income Builder (GKIRX) was originally Goldman Sachs Balanced and changed name and strategy in 2012.)

- source: Morningstar Direct

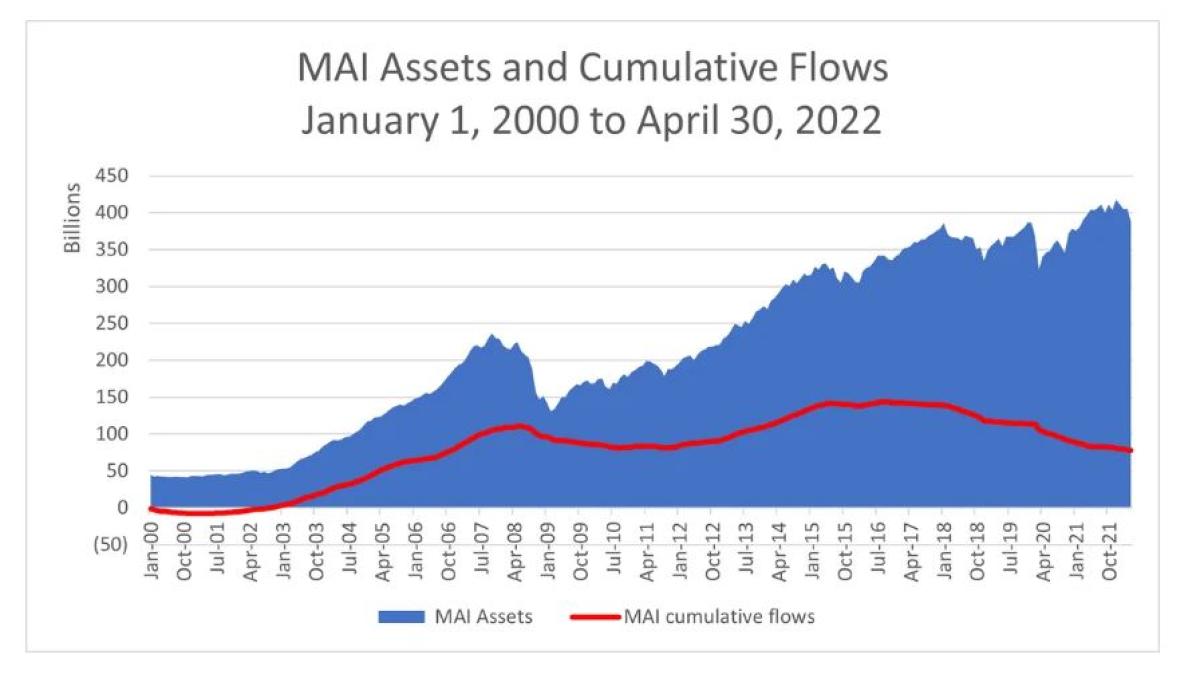

Over the past two-plus decades, multi-asset income funds have quietly accumulated a large asset base. At the turn of the century, they held $48 billion but as of April 30, 2022, held roughly 8 times that amount at $388 billion. That asset base is a bit smaller than that of the diversified emerging-markets category and a bit more than the collective assets of the funds in the small-blend category. (It’s worth noting that about 40% of the assets in multi-asset income offerings are invested in two American Funds—American Funds Capital Income Builder (CAIBX) and American Funds Income Fund of America (AMECX).) Most of this asset growth has been asset appreciation, though: Inflows have only totaled $78 billion over those two-plus decades.

- source: Morningstar Direct

A Few Fundamental Risks

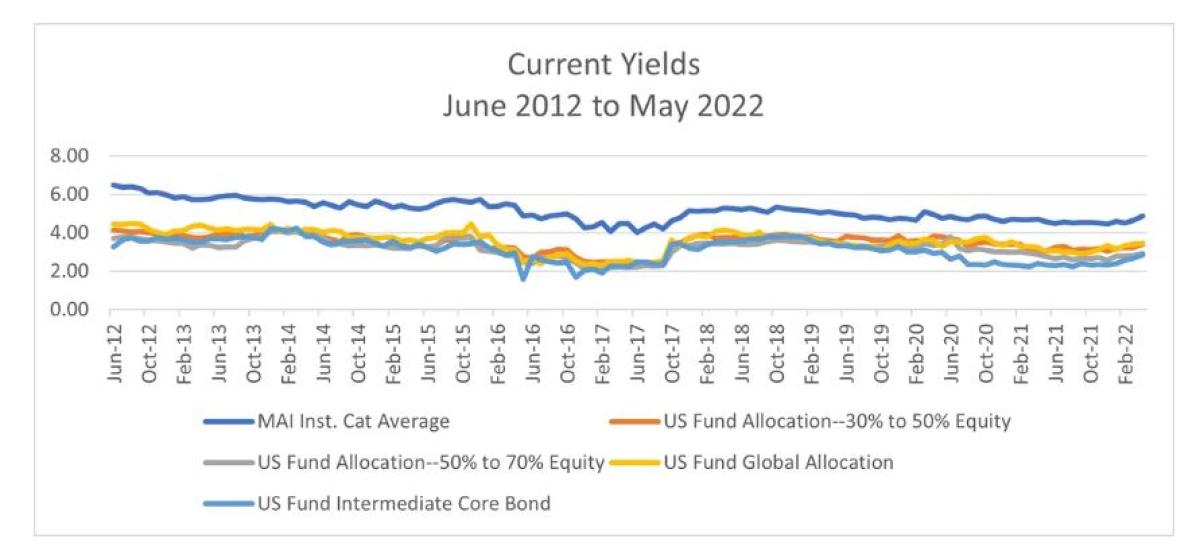

Compared with some broadly comparable Morningstar Categories, including those that call them home, multi-asset income funds as a group have certainly provided lofty income. While their average yields declined to 4.9% from 6.5% over the past decade, they’ve consistently boasted much higher yields than those of the allocation categories and especially the intermediate core bond Morningstar Category that covers the same ground as the broad-market Morningstar Core Bond Index or the Bloomberg U.S. Aggregate Index.

- source: Morningstar Direct

Indeed, versus the intermediate core bond category, which carries considerable interest-rate risk but only modest credit risk, the multi-asset income institutional category has had a roughly 200-basis-point yield advantage over time. Put another way, the average yield among multi-asset income funds is currently about 72% higher than that of the average core bond fund. That yield premium is a dependable signal of one type of elevated risk or another.

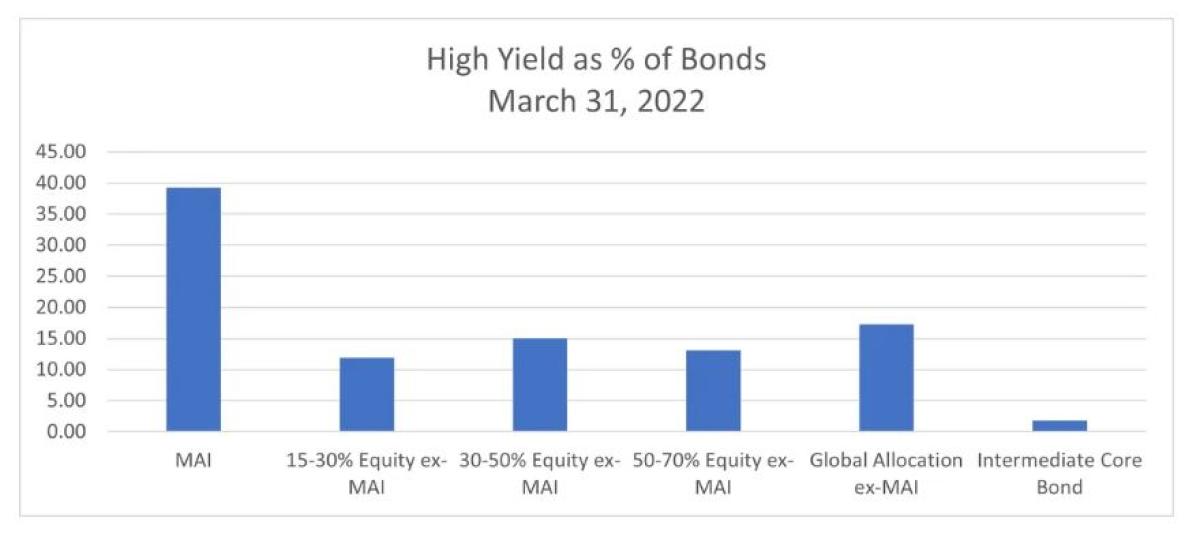

While these funds are far from uniform, the most common hunting grounds for their income, as above, are in high-yield bonds and large-value stocks. Across the 68 funds in the institutional category, on average, 39% of fixed-income assets went to high-yield bonds as of March 31, 2022. For comparison, in the intermediate core bond category, the average was 2%; for funds outside the multi-asset income group in the allocation—30% to 50% equity Morningstar Category, the average was 15% of assets in high-yield bonds.

- source: Morningstar Direct

Turning to large value, as of March 31, 2022, multi-asset income funds invested, on average, 28% of equity assets in large-value stocks. For comparison’s sake, within the allocation—30% to 50% equity and global allocation categories (aside from multi-asset income funds) the typical fund devoted an average of 18% and 20% of equity assets to large-value stocks.

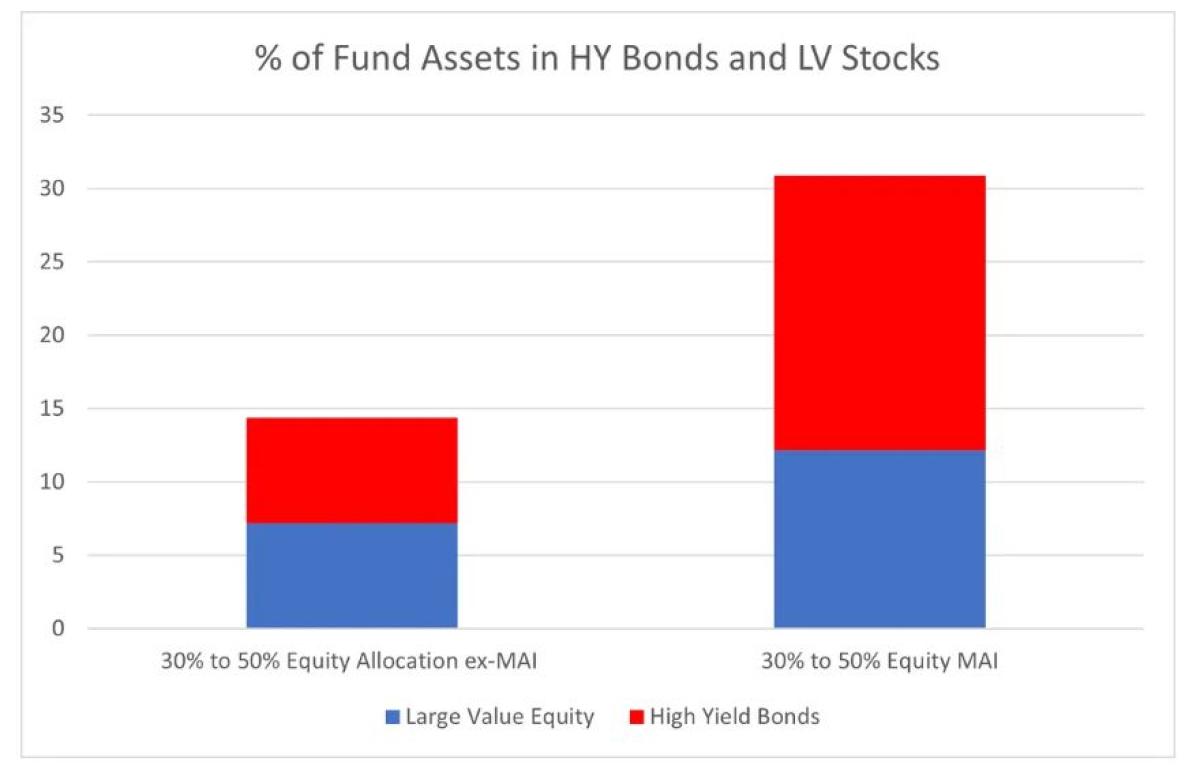

To get a sense of what these concentrations mean in combination, here’s a quick look at the allocation—30% to 50% equity category as of March 31, 2022. Excluding the subgroup of multi-asset income offerings, funds in that category averaged 14% of fund assets combined in high-yield bonds and large-value stocks. By contrast, multi-asset income funds in the category carried 31% of their assets in high-yield bonds and large-value equities. Note that these are averages; some funds lean extra hard on these areas: Transamerica Multi-Asset Income (TASHX) recently devoted 60% of assets to high-yield bonds and large-value stocks. Such a level of concentration in two asset classes that share risk factors, such as credit sensitivity, makes them precarious.

- source: Morningstar Direct

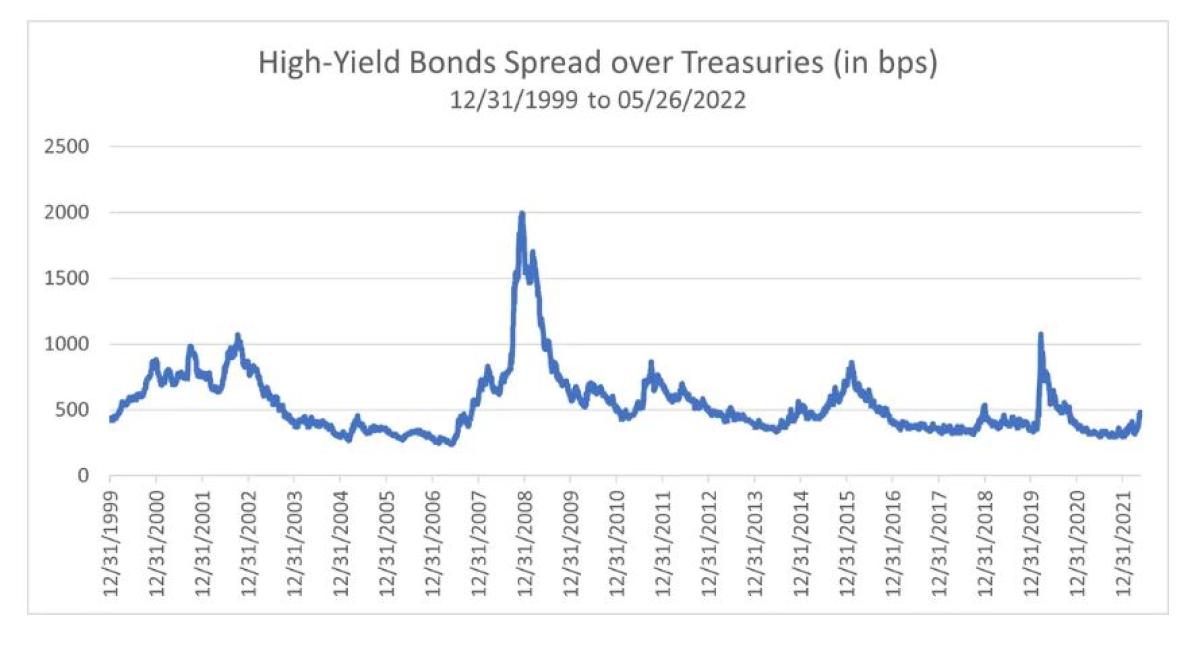

In addition to this concentration risk, there is also high-yield bonds’ credit risk. As interest rates have risen in 2022, credit spreads have widened. That said, they’ve only recently reached the normal range—not a generous one. Since Dec. 31, 1999, high-yield investors have received an average premium of 5.4% percentage points over 10-year Treasuries, with the median level at 4.6%. The average spread was just 3.3% on March 31, 2022, before it rose swiftly to 4.6% as of May 26, 2022.

- source: Morningstar US High-Yield Bond OAS Index

This fairly standard level of compensation comes when many believe the Federal Reserve’s overnight lending rate hikes may cause a recession. Receiving only average yields on debt from companies with risky financial footing in a precarious environment doesn’t argue strongly for a comfortable margin of safety. If the economic risks become reality, considerable drawdowns in high-yield bonds remain possible.

Return-Based Risk Measurements Miss the Mark

The fundamental risks that we see in multi-asset income funds, moreover, can hide in plain view for extended periods. That is, when looking at metrics based on trailing returns, funds can look sedate until a crisis. On this front, multi-asset income funds faced a comeuppance in early 2020 during the pandemic panic from Feb. 19 through March 3.

The classical volatility measure is historical standard deviation, which didn’t signal an impending problem heading into the 2020 crisis. From 2012 up through early 2020, it would have been fair to call multi-asset income funds sedate based on it. Over this nine-year period, they had an average three-year standard deviation of 6.6%, roughly two thirds that of the S&P 500 index’s 10.5% mark. At the end of 2019, multi-asset income funds’ average three-year standard deviation was just below that level, at 6.4%. As the pandemic panic took hold, however, their average standard deviation jumped to 10.3% in just three months, a 60% increase.

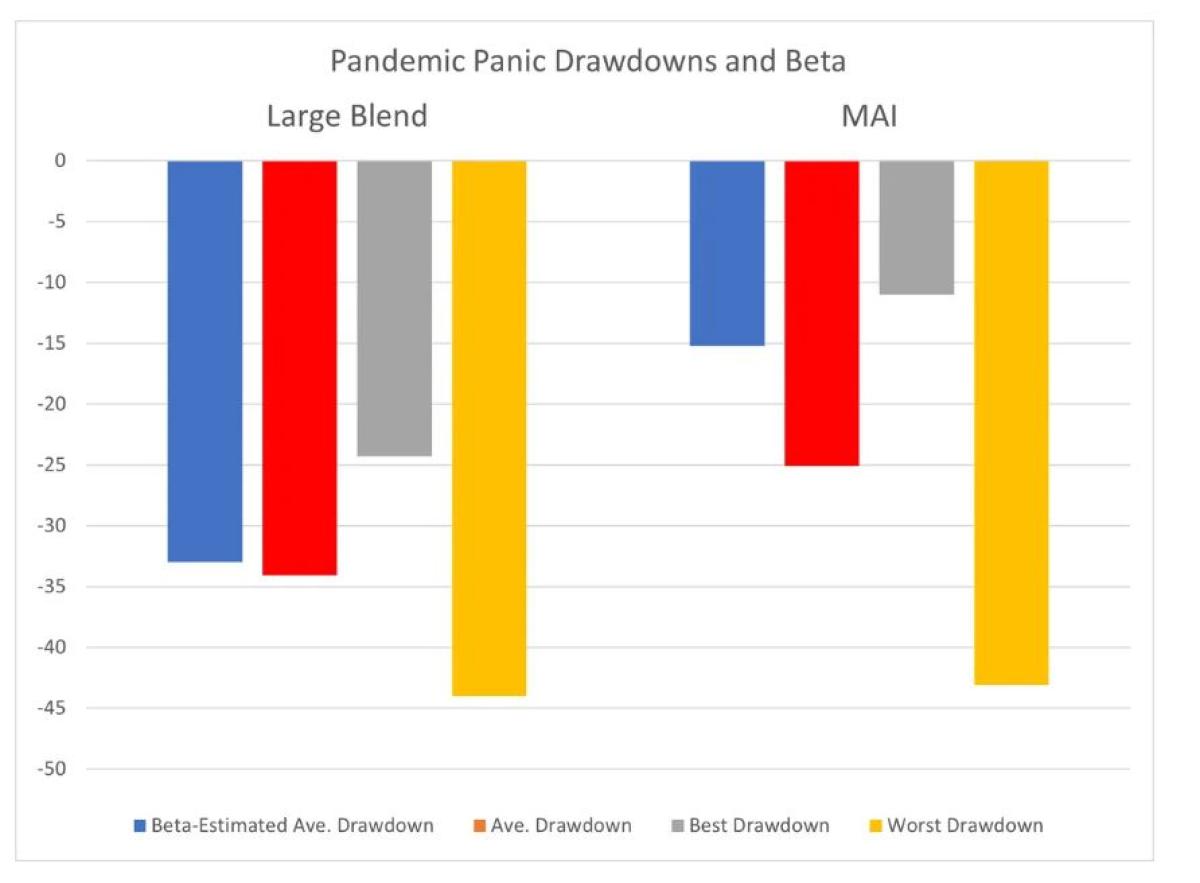

Another metric that would have projected a relatively low-risk image was beta, which approximates market sensitivity. Ideally, this metric should indicate how much an asset will fall (or rise) compared with a broad market benchmark—typically the S&P 500 index. It can be helpful in making rough estimates. For instance, in late 2019, the nearly 300-fund large-blend category had an average beta of 0.99 to the S&P 500. So, when that index fell 33.5% from Feb. 19 through March 23, 2020, you would have expected the average large-blend fund to drop about the same amount. The actual figure was 34.1%, for a single percentage point of additional damage.

On the other hand, the admittedly heterogenous multi-asset income group had an average beta of 0.45 to the S&P 500 at the end of 2019. Using that number, you’d estimate a typical pandemic-panic loss of 15.2%. The actual losses, however, were an average of 25.1%, or roughly 1,000 basis points more than a beta measurement would have suggested. Of course, that’s just the average loss: Individual fund showings ranged from a best return of negative 11.0% to a worst return of negative 43.1%.

- source: Morningstar Direct

The calculation behind beta rests on past returns, and as the warning goes: Past performance does not necessarily predict future results.

To understand why multi-asset income funds slid so badly, you’d need to go back to fundamentals risks: multi-asset income funds’ concentration in their favored subasset classes. First, there’s large value. While that corner of the market didn’t implode, it did underperform: The large-value Morningstar Category fell 37% in the pandemic panic. Second, high-yield bonds crashed when compared with other fixed-income assets. The average high-yield bond fund plummeted 20.0% in the pandemic panic—or 1,700 basis points worse than the typical intermediate core bond fund. When investors anticipated the ravages of recession and default, highly compressed credit spreads gapped widely, driving a selloff that coincided with and echoed the stock market’s plunge.

A sharp capital loss can easily create a difficult situation for income investors. After all, total returns are composed of capital returns and income. But those investors who are spending the income—and there’s no good reason to own a strongly income-focused fund if you’re not spending the income—are not reinvesting to build their asset bases back up. That can be fine in a mild pullback but creates more difficulty in a crisis. Because of the pandemic panic, 26 out of 68 mulit-asset income funds (nearly 40% of the total group) had negative returns in 2020—and didn’t fully recover from the sharp losses early in the year. Problematically, 21 out of those 26 also had lower income levels in 2020 than in 2019. And these funds’ income levels dropped a lot, averaging 22% less income from 2019 to 2020. Keep in mind, those income returns were not mere paper losses: Owners of those funds living on the income either had to reduce spending, find funds elsewhere, or sell down something in their overall portfolios to make up the difference. (While investors may seek the high income levels that multi-asset income funds provide, it’s not a good idea to use them as one-fund holdings in retirement.) Those who sold down their MAI funds, of course, were lowering their income levels going forward because they were, in effect, locking in losses in their asset bases.

As noted, every downturn is different, and multi-asset income funds won’t always deliver bad surprises when the stock market falls. As above, in 2022 through May 31, 2022, the Morningstar US Market Index has fallen 14.1%. The multi-asset income funds had an average three-year beta of 0.59 to this broad index as of year-end, so an investor might have expected a loss of 8.5%. The actual average for the funds has been a decline of 7.4%—nearly a percentage point better than one might have anticipated.

The rising interest rates that are largely driving the current downdraft in both equity and bond markets may also help create a new era for multi-asset income funds. First, with higher absolute yields now more widely available, the funds themselves may diversify more and tamp down risks. Second, now that core bond holdings have improved yields, investors may find the income streams of more conservative vehicles more attractive.

Multi-Asset Income Funds That Stand Out in the Crowd

In the meantime, while it’s clear that many multi-asset income funds now carry significant risks hiding in plain view, worthy mutual funds in the group do exist. Indeed, several carry high Morningstar Analyst Ratings, and they’ve often fared better than the pack.

The only Gold-rated fund in the multi-asset income group is Vanguard Wellesley Income (VWINX), which resides in the allocation—30% to 50% equity category. It should be no surprise that its profile is more conservative than those of its multi-asset income peers. The fund stands apart by emphasizing dividend growth over dividend level and, strikingly, by swearing off high-yield bonds. Its yield was recently a conservative and maintainable 2.9%; given its relative caution, the Vanguard fund fell just 17.2% in the pandemic panic—outperforming the average multi-asset income fund in the allocation—30% to 50% equity category by 700 basis points.

American Funds has three Silver-rated funds in its lineup that demonstrate how multi-asset income funds can manage risk effectively in different ways. American Funds Income Fund of America (AMECX) is one of the few multi-asset income residents of the allocation—70% to 85% equity category. It mixes a 71% stake in dividend-paying equities (with a combined target of 2.5% yield) with high-yield bonds that consume 5% to 10% of total assets. Given an equity weight that’s fairly high-octane in the multi-asset income group, the fund fell a comparatively light 25.7% in the pandemic panic—in line with the typical multi-asset income fund overall. American Funds Capital Income Builder (CAIBX) is a similar global allocation fund that tilts more toward foreign stocks. Recently, it devoted 79% of assets to equities, including 34% from abroad. It doesn’t lean hard on high yield, however, with just 6% of its bond assets in that sector. Much like its sibling, it slid 25.0% in the pandemic panic, about the same as average multi-asset income funds with much higher equity weightings. Finally, American Funds Conservative Growth & Income (RINFX) has demonstrated that even with high exposures to the favored MAI areas, a fund can perform well in choppy markets. Its 39% combined weight in large value and high yield is even higher than the 31% figure typical of multi-asset income funds in the allocation—30% to 50% equity category. Yet, given the portfolio managers’ security-selection skill, the fund outperformed those multi-asset income allocation—30% to 50% equity peers by 300 basis points in the 2020 pandemic panic.

Finally, showing that a multi-asset income fund can do well despite a truly heavy stake in high-yield bonds, there is Silver-rated BlackRock Multi-Asset Income (BIICX). The fund loaded up on high-yield fare to the tune of 54% of bond assets recently. So, the managers do hold a larger slug of riskier bonds but focus tightly on keeping the fund’s volatility below that of a 50% equity and 50% bond benchmark. Using that framework, the fund lost just 19.5% in the pandemic panic, nearly 500 basis points better than the typical allocation—30% to 50% equity multi-asset income offering’s loss despite the large high-yield stake.

About the Author:

Todd Trubey is a senior manager research analyst for Morningstar Research Services LLC, a wholly-owned subsidiary of Morningstar, Inc. He covers multi-asset and alternative fund strategies. Before re-joining Morningstar in 2021, Trubey served as Vice President of Marketing & Analytics for Advisory Research, Inc. and as Vice President, Portfolio Strategies for Ariel Investments. In his previous stint with Morningstar, he worked in training and education and was a senior mutual fund analyst. Trubey holds a bachelor’s degree in English from Sewanee: The University of the South and both a master’s degree and a PhD in English from Northwestern University.