By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

The transition out of LIBOR and into SOFR1 as the reference rate for fixed income securities and derivatives is proceeding smoothly with virtually all new agreements now tied to SOFR.

Two transition changes are noteworthy. First, because SOFR is an overnight only borrowing rate while most LIBOR -based agreements use 1, 3, 6, and 12- month maturities, a “fix” was needed to secure equivalent SOFR maturities. A futures-based methodology published by CME Group has been accepted by regulators as a solution. Therefore, expect to see references to CME Term SOFR Rates.

Second, LIBOR embedded a small incremental yield attributable to bank credit risk that is not present in SOFR where Treasuries are used as collateral. The market is now addressing this potential “lost” spread by (a) adding an explicit and separate credit spread adjustment (CSA) to SOFR, or (b) implicitly including it in the credit spread charged to the borrower. Year-to-date approximately two- thirds of SOFR-based agreements have used option (a), but the trend is toward option (b).

While the LIBOR/SOFR transition has proven uneventful to date, there are certain conventions and practices that are still in flux.

Key Points –

- In late 2020, global regulators formally announced that after December 31, 2021, substantially all global LIBOR rates will either cease publication or lack “representativeness,” thus removing any uncertainty surrounding the discontinuation of LIBOR2.

- While many competing LIBOR replacements were contemplated, the industry has settled on SOFR as the accepted successor rate for U.S. dollar-based contracts. SOFR is the volume-weighted median rate for overnight cash borrowings collateralized by U.S. Treasury securities, as transacted in the repurchase agreement (i.e., repo) market.

- ARRC3 and market participants coalesced around SOFR because 1) it is derived from an active and well-defined market with sufficient depth that makes it extraordinarily difficult to manipulate or influence ($1 trillion + in daily volume), 2) it is produced in a transparent, direct manner and is based on observable transactions rather than being dependent on estimates, like LIBOR, or derived through models, and 3) it is derived from a market that is, and promises to remain, active enough to reliably produce a rate during a wide range of market conditions, including time of stress.

- Treasury rates, which meet similar criteria, are not good reference rates because they are countercyclical. When the market experiences stress, risk -off demand bids Treasury security prices up and rates fall. SOFR is instead procyclical. When the market experiences stress, lenders demand a higher rate to give up cash, and borrowers pay a higher rate to access cash. This procyclicality comports with the proper intuition in the market between lenders and borrowers broadly.

- The two main issues with SOFR as a LIBOR replacement are that it is a rate representative of overnight, secured lending between market participants while LIBOR is a rate representative of term, unsecured lending between banks.

- Because SOFR is an overnight rate and lacks a term structure, ARRC recommends the use of “CME Term SOFR Rates4,” which are published daily and are a series of forward-looking SOFR term rates derived by compounding projected overnight SOFR rates implied from futures contracts5. A term structure is important because lenders and borrowers prefer to have 1) a forward-looking rate that reflects the expectation of rates over the actual interest period, and 2) a rate that is known and can be “locked-in” at the beginning of the interest period, as opposed to in arears calculations that are unknown until the end of the interest period6.

- Because SOFR lacks a counterparty credit risk spread (LIBOR was essentially a AA bank-to-bank risk spread), some lenders and borrowers are negotiating a credit spread adjustment (“CSA”) over term SOFR. Sometimes the CSA is flat over the term SOFR curve and sometimes it steps up over the term SOFR curve (commonly referencing a 10/15/25 spread over 1-month/3-month/6-month maturities).

- It remains to be seen whether all-in lending rates include a CSA permanently (i.e., a two-part construct – term SOFR + spread + CSA), or if explicit CSAs are dropped in favor of building any compensating CSA into the overall spread (i.e., a one-part construct – term SOFR + spread).

- Note that references to CSAs are made in two different contexts: either a prospective spread (a spread that is dynamic and determined by the market of borrowers and lenders for new debt issues), or a “fallback” spread, which is a fixed spread ARCC recommends as “fallback language” for those documents that had not prior contemplated a transition away from LIBOR. The fallback rate recommended by the ARRC is based on the historical 5 -year median spread between USD LIBOR and compounded average of SOFR at the time of the recommendation7.

Early Observations

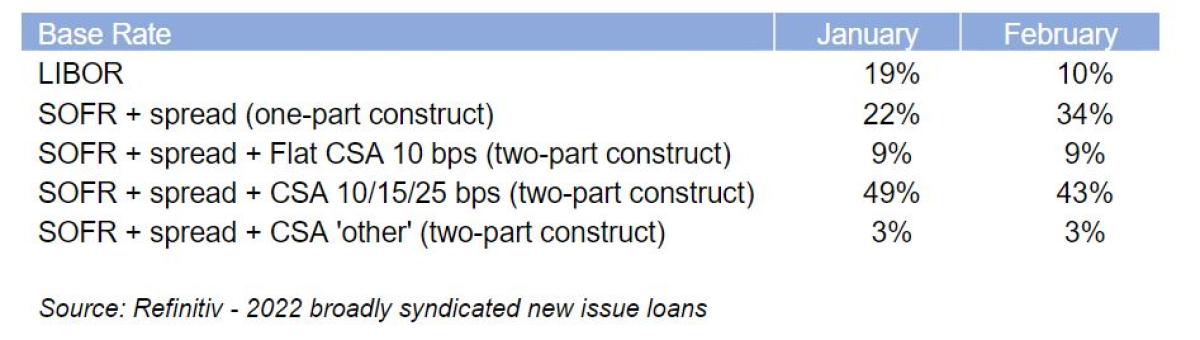

- Eighty-one percent of broadly syndicated institutional loans (BSLs) priced over SOFR instead of LIBOR, and 90% in February. This compares to only 15% during the entire fourth quarter of 2021.

- While 60% of loans priced with some form of CSA in January, 55% priced with a CSA in February. Loans pricing as a one-part construct (SOFR + spread) grew from 22% of total new issues in January to 34% of new issues in February.

- New CLO formation referencing SOFR totaled $4.9 billion during January, plus $4.0 billion of SOFR -linked deal resets and refinancings, which compares to only $0.1 billion that priced with SOFR-linked tranches in all of 2021. Almost all SOFR-linked CLOs have priced with no explicit CSA but did price with a spread 15- 20bps higher than the equivalent LIBOR spread, effectively embedding the CSA into the spread.8

Conclusion

The LIBOR /SOFR transition has proven uneventful. Adopting SOFR, as well as use of the CME Group’s term SOFR curve, has proven acceptable with broad market acceptance. Use of an explicit credit spread adjustment (CSA) in the corporate loan market has proven more mixed, however. While early still, the trend points to the market dropping a LIBOR-equivalent credit spread adjustment in favor of embedding the risk premium into a higher SOFR + spread construct.

About the Author:

Steve Nesbitt is Chief Executive Officer and oversees all investment research as the firm’s Chief Investment Officer. Prior to forming Cliffwater in 2004, Steve was a Senior Managing Director at Wilshire Associates. From 1990 to 2004, Steve led the Consulting division at Wilshire Associates and also started and built its asset management business using a 'manager of managers' investment approach, including private equity and hedge fund-of-fund portfolios. Steve started his career at Wells Fargo Investment Advisors, an early pioneer in index funds, where he developed and managed index funds and oversaw asset allocation.

He graduated summa cum laude, with a BA in Mathematics and Economics from Eisenhower College (Rochester Institute of Technology), and an MBA, with Distinction, from The Wharton School at The University of Pennsylvania.

Stephen L. Nesbitt snesbitt@cliffwater.com

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.