By Jeff Malec, Managing Director & Partner, RCM Alternatives.

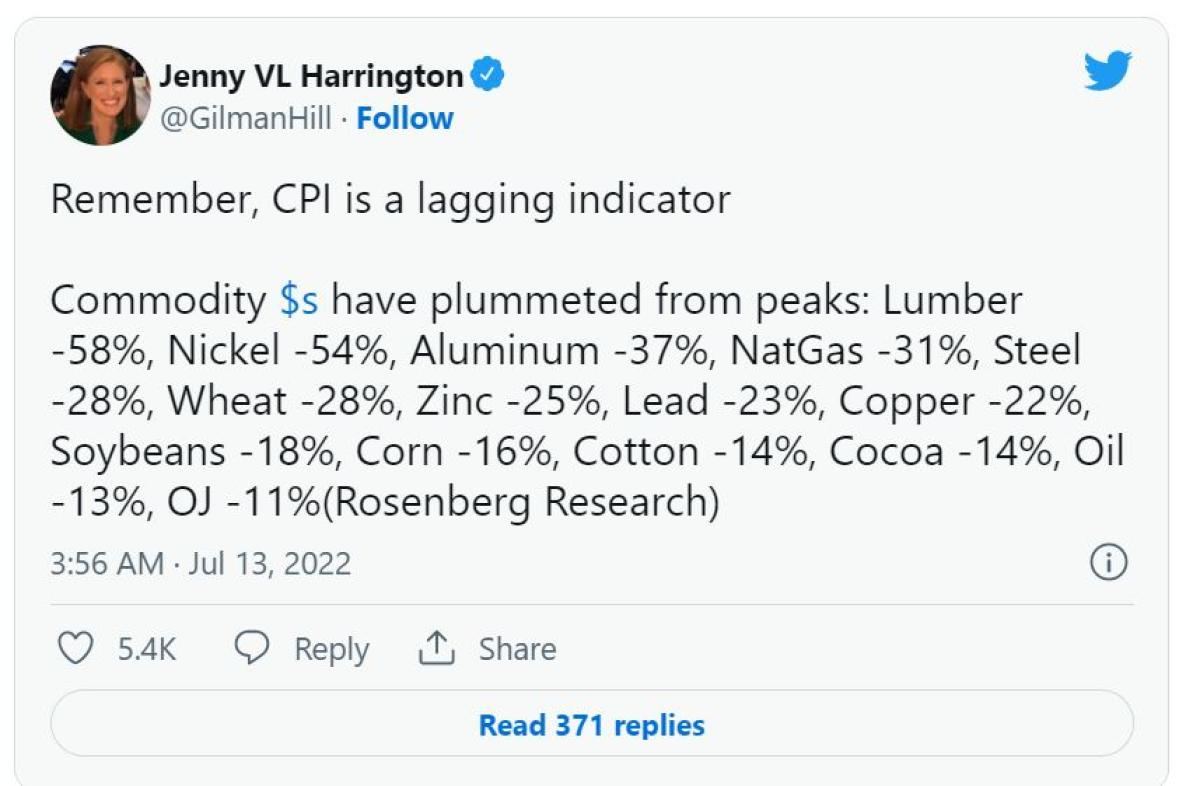

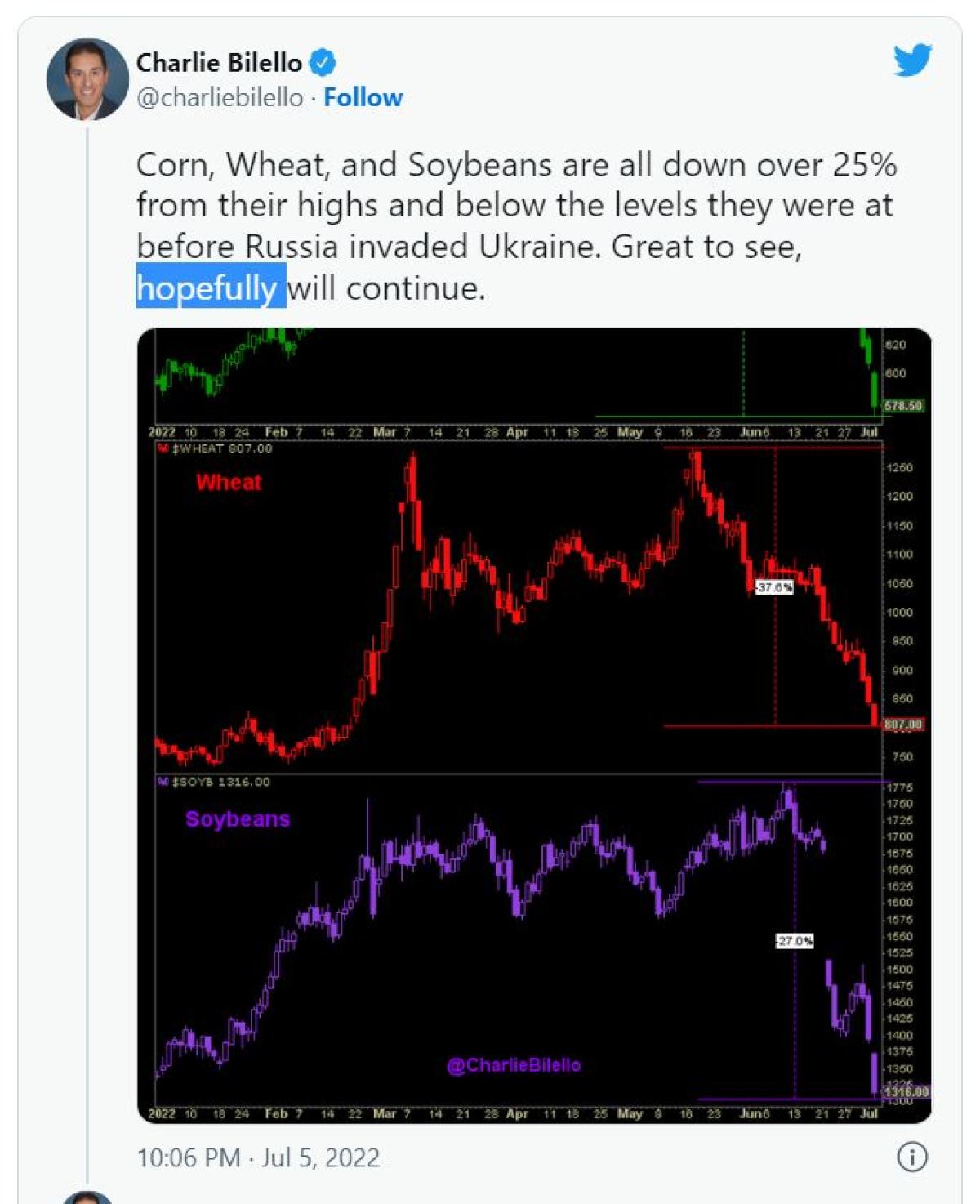

Word in the Twitter streets is of a commodity blood bath:

So are CTAs, Managed Futures, and Trend Followers also getting crushed? They were, after all, crushing it (on the good side) riding the inflationary moves higher in everything from energies to grains to metals. What goes up, must come down?

Not so fast…

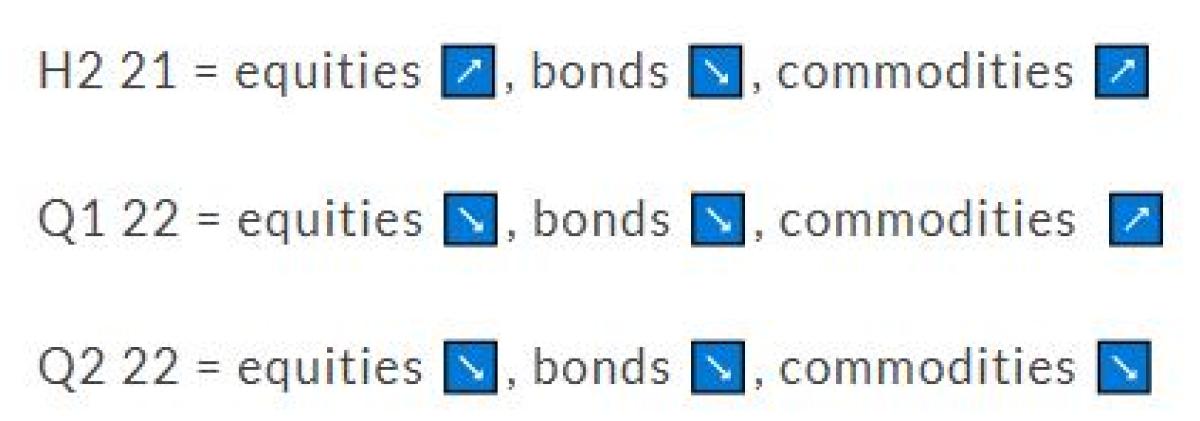

Take a look at the quarterly performance so far this year:

If you’re new here, be sure to check out these few simple definitions between trend following, CTAs, and Managed Futures on Jeff Malec’s twitter feed

So why has the SocGen Trend Index, approximating performance of trend followers held up the past month and a half despite some rather violent commodity retracements:

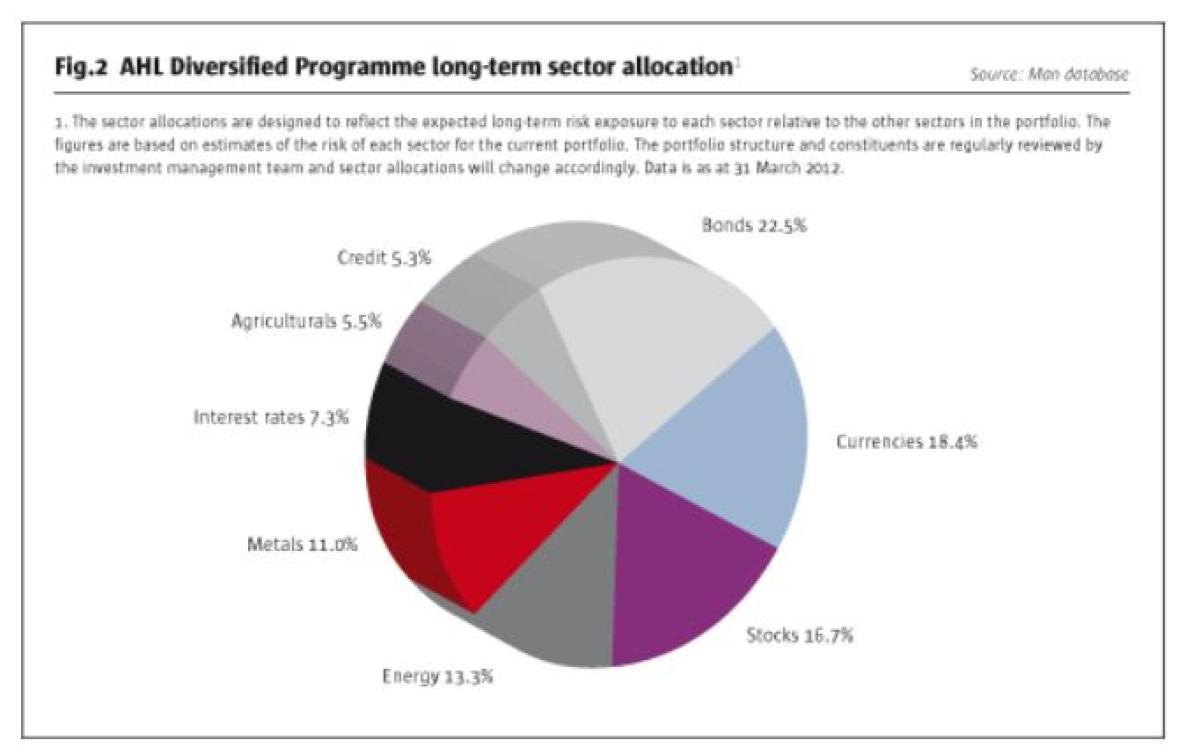

The first takeaway is that there is more going on in Trend Following than just commodities. Commodities are typically between 25% and 75% of a trend followers’ portfolio — Typically, the bigger the CTAs assets, the less Commodities.

Take a look at a look at this old chart from Man AHL showing their portfolio breakdown:

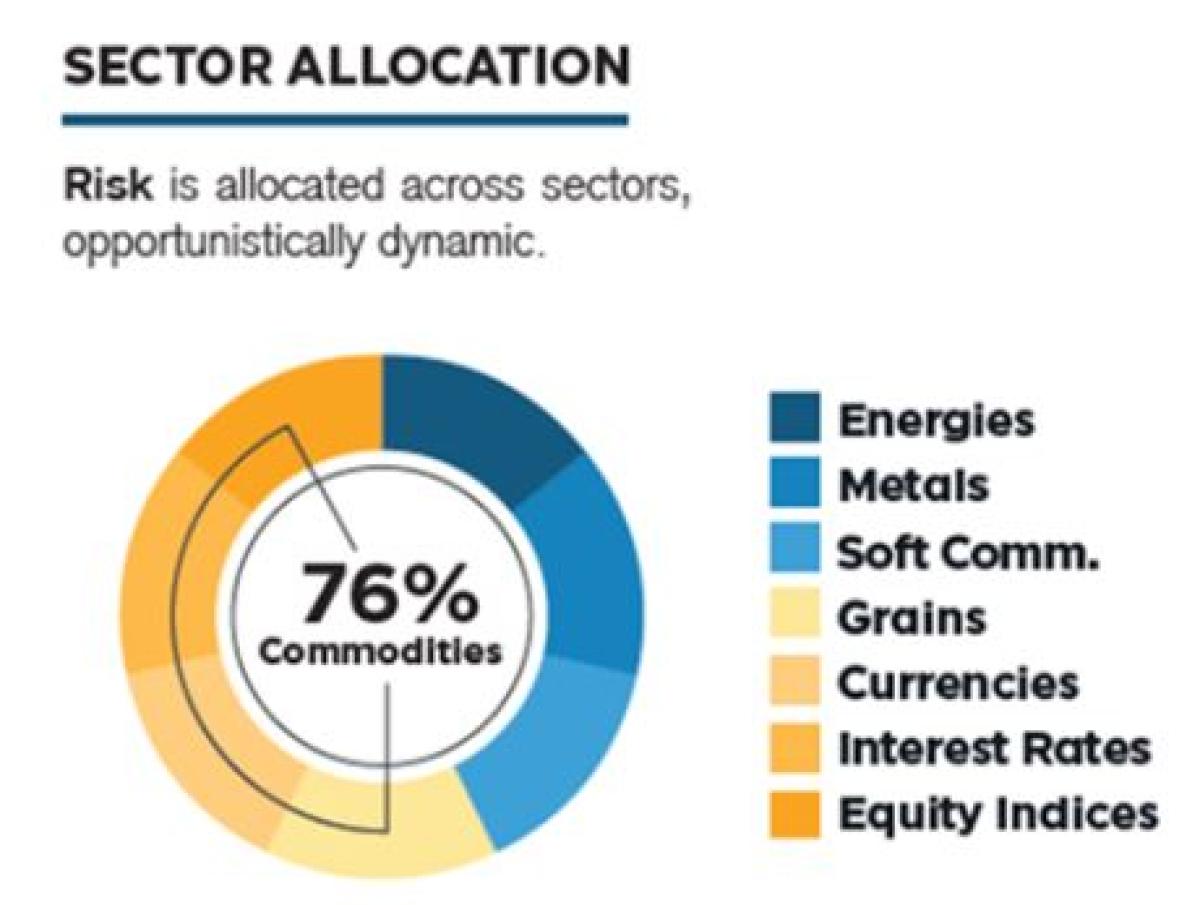

And here’s a more recent one from a more diverse commodity-focused program from Tim Pickering @AuspiceTim at Auspice Capital (Check out their program in our trend following guide here):

So if we know that commodities make up a healthy part of the portfolio, but sometimes not too much, the ability for Trend to be UP, while commodities reversed DOWN, is likely one of two things:

1. They’ve perfectly timed the reversal & are now short commodities

2. Commodities have passed the perfect baton on to other areas

Trend isn’t known for nailing reversals and if anything, their main risk is taking it in the face from sharp reversals… so it probably isn’t door #1 above. (PS – getting hit with sharp reversals was a big reason why we helped the team at Mutiny to build a hard-to-kill ensemble of lookbacks in the Trend Strategy inside their Cockroach Fund, where different trend algos/models react differently to reversals depending on whether they use a short, medium, or long-term lookback.)

We’ve seen it definitely be more of door #2 above, with a sort of ‘passing of the baton’ trend world the past 12 months, handing off the exposures as the environment shifts to keep the party going.

If we think of Trend kind of like a three-legged stool, at least two of the legs (and in Q1 and most of Q2 this year all three legs) have been working for most of the past 12 months. In short, Trend strategies have been on the right side of bonds the whole time, on the right (long) side of commodities in two f three quarters, and on right side of equities in two of three quarters.

And don’t worry, if you got lost in our stool legs analogy, here’s what that looks like graphically. We took the quarter-end positioning of each market in the SocGen Trend Indicator and calculated the percent long or short for each sector as of the end of each quarter. For example, in Crude Oil, RBOB Gasoline, and Heating Oil were all Long, but Natural Gas was short, we would show that as 75% long (3 of 4 markets long).

The surprising thing to many may be just how dynamic these exposures are, shifting quite a bit over a year period, and how each sector is rarely an all in bet (long or short) in that sector. But this is what Trend does. Trend following models are designed to shift exposures between long/short in a specific sector and even switch sectors to create as many unique bets as possible. We talked about the number of unique bets climbing higher after years of being at all-time lows on this pod here with Rodrigo Gordillo @RodGordilloP:

Back to commodities and their big sell off the past few weeks. They are often lumped into that neat word and treated as ONE thing, but they are anything but a unified asset class that moves all together. Just think about it: Cotton has different drivers than Crude Oil. Cocoa has different supply factors than Copper. Here’s what the past 12 months’ exposures have looked like just inside the commodity world:

In summary, there’s two main things going on. One, while many commodities are showing signs of retracing into a down trend – it’s nor prevalent across the dozens of markets across the energy, metals, meats, grains, and softs sectors which we collectively call commodities.

And two, there are other non-commodity markets in the Trend Portfolio which are stepping up to the plate and picking up the proverbial slack. Markets like bonds and currencies, where managed futures and CTA programs love a trending U.S. dollar.

While interpreting commodity prices can be challenging, it doesn’t have to be.

About the Author:

Jeff Malec has spent 20 years in the futures markets since his days as a clerk in the bond futures pits and serves as the managing member for multiple commodity-based hedge fund products.

Prior to RCM, Mr. Malec was the founder and CEO of Attain Capital Management, which merged with RCM after 13 years assisting clients with alternative investments. He is the great grandson of Harley Davidson founder Walter S. Davidson, and a former board member of the National Futures Association. He holds the Chartered Alternative Investment Association (CAIA) designation and has authored hundreds of white papers covering alternative investments.