By Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director and Head of UniFi by CAIA™ at CAIA Association.

Jobu: "Every new discovery is just a reminder—"

Evelyn: "We're all small and stupid."

Everything Everywhere All at Once (2022)

As we sit on the brink of releasing our companion, A New Professionalism, to our 2022 seminal piece, The Portfolio for the Future, I’ve been traveling, speaking, and moderating panel discussions across the multiverse (see: CFA Society tour of Ohio and FutureProof by Advisor Circle). Like the way the multiverse is represented in movies, each of my discussions have been with very different people, but a similar underlying plot point underpins every discussion. The takeaway is clear – this is new for many of us, and no one has the answer just yet.

Whether you’re an institutional asset owner with billions of mission-driven assets under management, or a financial advisor stewarding the life savings of a family or individual client, you’ve likely entered a new era of portfolio construction. If anything, 2022 has been a year where many of the tailwinds that got us to this place have quickly reversed (strong and rising equities, falling and stable rates, tame inflation, and so on).

During these individual meetings and panel discussions, we’ve noticed that, while everyone has different clients and mandates, there are a few common themes that seem to resonate with investment professionals today:

- It’s all about access

- Premiums aren’t given, they’re earned

- The wrapper matters

Evelyn: "Don’t make me fight you, I’m really good!"

Jobu: “I don’t believe you.”

Better Access Leads to Better Outcomes: Leave it to me to mutter a Bill Kelly-ism (our witty CEO) in the car ride back from one of the panels in Ohio… “it’s not all about alpha, it’s all about access!” Regarding alternative investments, access to the best managers is really what drives the outcomes in the total portfolio. Mistakes are costly in this work, and the decision-making process is two-fold: the managers have to be good at investing, and you have to be good at picking the managers.

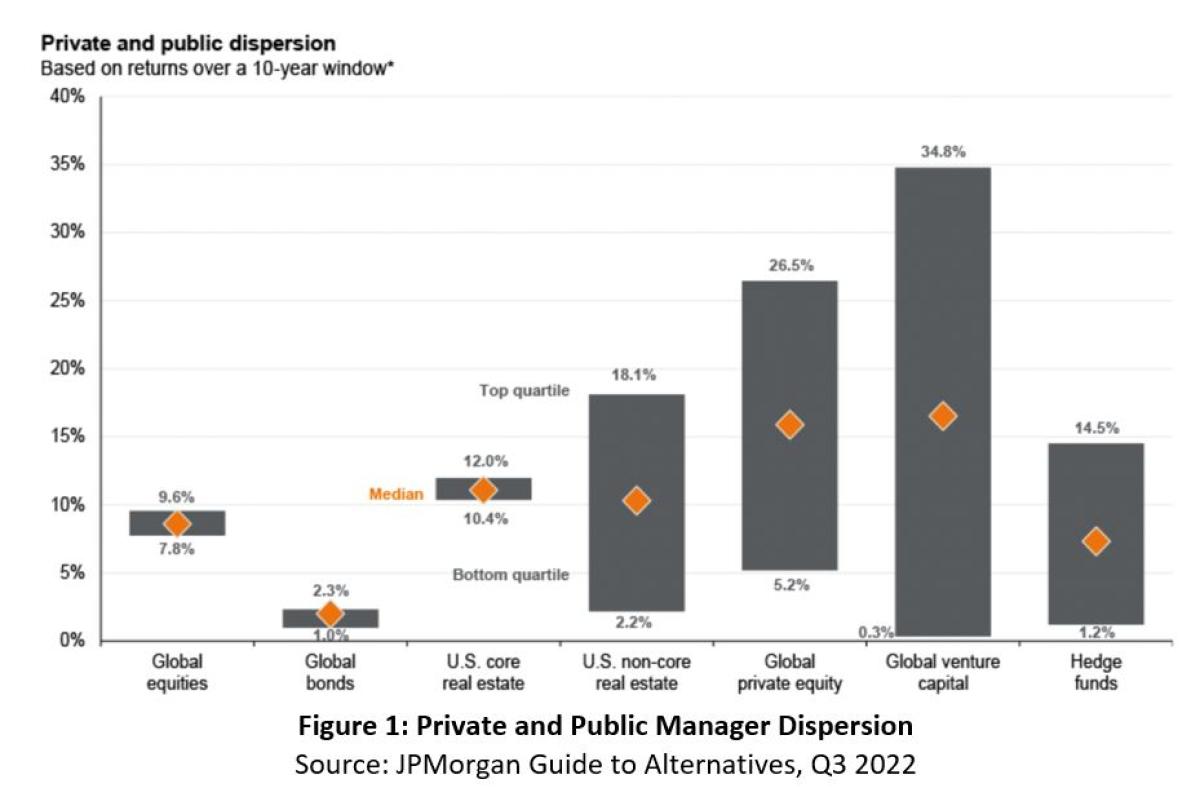

We’ve all seen different versions of return dispersion charts, and with some variation, the median return for many private capital strategies is usually close to their public market brethren. The number of funds and platforms to access funds coming to market have increased dramatically – ultimately, the choices are a good thing, but novices beware.

Jobu: “I got bored one day and put everything on a bagel.”

Private Capital: Not an Everything Bagel. Earning an illiquidity premium doesn’t happen just by showing up, yet we make these assumptions that alternative investments just automatically come with pre-determined characteristics. If you’re starting the decision process by assuming a baked-in illiquidity premium, you’re probably not doing it right. Similarly, any GP, platform, or professional that leads with that value proposition is ignoring the nuance. Some recent quotes from allocators hammered this home:

- “You should assume an illiquidity premium doesn’t exist when going into private equity today. In fact, I wouldn’t be surprised if the median private equity fund return over the next ten years is the same or lower than that of a public equity index.”

- “If you lock up your money in the S&P 500 for ten years, what do you get? The same return as if you bought it in the public markets…just because you go illiquid doesn’t mean you earn a premium!”

That said, there are still some clear benefits to investing in private capital allocations:

- GPs in private capital have a structural advantage that allows them to think long-term about their portfolio companies. Owner-operators especially have that advantage.

- Private capital, through capital formation, provides exposure to alternative growth engines of the economy. The value creation in new technologies and businesses happens early, especially in venture capital.

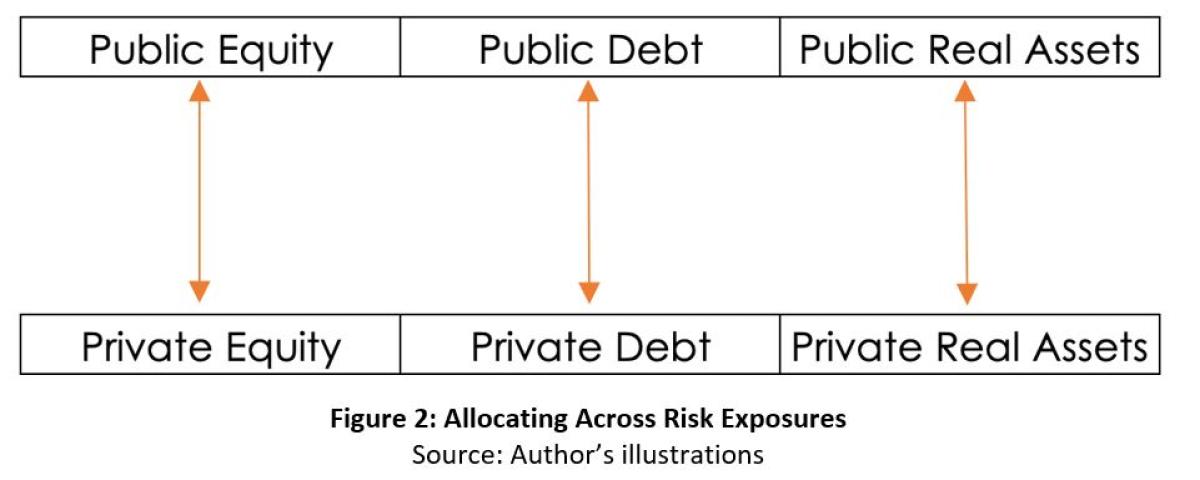

Both things can lead to a premium above public markets, but, as one panelist at FutureProof said, you’re “betting on the jockey, not the horse.” For an asset allocator, this means starting with the wanted risk exposure and selecting the most appropriate strategy across the liquidity spectrum, perhaps like the framework I’ve drawn in Figure 2. Complexity isn’t systematically rewarded, but managers that take advantage of structural advantages can prevail if implemented correctly.

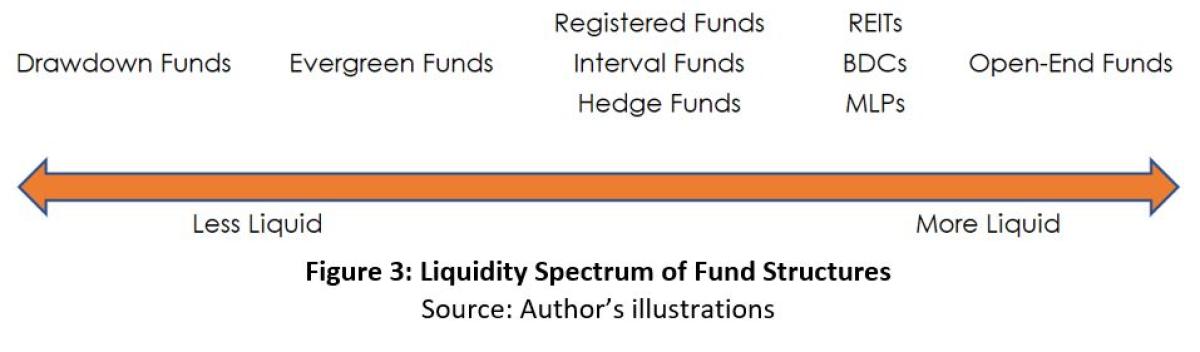

Democratized vehicles: Buyer Beware? While the traditional GP/LP drawdown structure has been the norm for institutional asset owners, the number and variety of vehicles to access illiquid markets have proliferated to the point where knowing the wrapper is half the battle. Having a framework of asset class vs. liquidity spectrum might be helpful given the options, as shown in Figure 3.

Are these structures appropriate for broadening access to illiquid markets? In the words of a true economist: “it depends” on the following factors:

- What’s the liquidity profile of the asset class?: Interval funds have grown in popularity over the past several years, but the underlying assets tend to generate cash flow or have a shallower/shorter J-curve, such as secured lending or core/core-plus real estate. For a wrapper that requires 5% liquidity per quarter, that may just work. For longer-dated assets, such as venture or buyout private equity, a vehicle may prove more problematic unless the funds are well diversified and take advantage of more liquid assets in the public or secondary markets.

- What’s the valuation policy of the fund?: One panelist noted that, in a drawdown structure, price matters but mostly at purchase and at the exit. These funds are valued once-per quarter, but new investors aren’t really entering the door outside of capital calls in the beginning. In more evergreen structures, where dollars may be invested monthly, and redemptions made quarterly, the NAV valuation becomes very important, both for buyers and sellers. In many ways, these NAVs are merely estimates and it’s important they reflect a close estimate of the value before exit.

- What’s your time horizon? More liquid structures may be attractive for newcomers because it allows them to test the illiquid waters. However, if your timeline is perpetual (for an institution) or multiple decades (for an individual or family), liquidity may not matter as much as achieving a long-term outcome.

Becky: "I Always Learn Something When I Hang Out With The Elderly.

Old People Are Very Wise."

The most valuable takeaway from these sessions was that it’s important for any institutional or wealth management professional to answer this ultimate question first:

“What am I trying to solve for?”

Democratization of alternatives started ten years ago with hedge funds and the liquid alternatives craze that led to disappointing results and, at the worst, a few fund blow-ups. While some of the stronger funds may remain, we have an obligation as an industry to do it right as the 2.0 effort takes over.

In A Renewed Professionalism, pay particular attention to the evolution of the alternative investments industry and the resulting roadmap we provide to make sure we do right by the client. Lead with a fiduciary mindset, diagnose your client’s needs and, most importantly, participate fully informed.

About the Author:

Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP is Managing Director and Head of UniFi by CAIA™ at CAIA Association. You can follow him on LinkedIn and Twitter. Learn more about UniFi by CAIA™. Prior to this, Aaron was responsible for the strategic direction of CAIA Association's content agenda, thought leadership, and member education initiatives, and supported content development for the CAIA Charter Program. His work has been published by Oxford University Press and The Journal of Investing, and covers topics such as ESG/sustainable investing, liquid alternatives, commodities, and asset pricing/factor investing. He is a frequent writer and speaker on these topics. Aaron’s practitioner experience lies in private wealth management, where he served as portfolio manager, overseeing asset allocation, portfolio construction, and manager research efforts for high-net-worth individuals and institutional retirement plans.

He earned a B.S. with distinction in Finance and a Master of Finance from Penn State University. He holds the Chartered Alternative Investment Analyst (CAIA), Chartered Financial Analyst (CFA), Certificate in Investment Performance Measurement (CIPM), Financial Data Professional (FDP) designations, as well as CFA Institute's Certificate in ESG Investing. He is a Past President of CFA Society Columbus and serves on the CFA Society Philadelphia Programs Committee. Aaron is an adjunct professor and serves on multiple advisory boards for Penn State University.