By Lucie Delzant, Enrica Bruna, and Rémy Estran-Fraioli, PhD of EthiFinance.

Introduction

In a context of inflation, geopolitical instability, and economic uncertainties, private debt remains an asset class demonstrating stability and retaining investors’ confidence. This is partially due to the less volatile dimension of this market, as compared to public markets. Indeed, in a report, McKinsey[i] highlighted the “cyclical resilience” of this asset class, which has known continued growth over the past decade, supported by the expansion of direct lending. Lenders are thus confident regarding the outlook for the market’s evolution.

The interest for the private debt market is associated with growing demand and popularity of ESG integration across all asset classes, including Private Debt. This ESG momentum arises from several factors, such as regulatory pressure, the acknowledgment that ESG factors can be a driver of risk and opportunities, as well as Limited Partners’ (LP) demand for ESG integration.

Sustainable finance is now an unavoidable dimension of investment strategies. Yet, ESG integration remains complex for private debt investors due to several factors, such as the lack of standardization of market practices and the financial innovations, such as impact or ESG-linked credit. However, the multiple levers for actions as well as the large field for innovation available to asset managers render ESG integration very relevant for Private Debt.

The following article aims to provide insights on the drivers pushing for ESG integration in Private Debt and the levers for action of investors with a description of each approach to be leveraged by the investors. It also aims to understand the challenges associated with this practice.

1. Drivers of ESG Integration in Private Debt

The growth of sustainable finance and its deployment across all asset classes, including private debt, is pushed by several factors. The trend for ESG in financial markets which is moving away from its niche position to become mainstream can lead asset managers with no ESG strategy to be considered laggards compared to peers. Basic ESG strategies are no longer a market differentiator but are considered a prerequisite.

Also, market expectations with regards to asset managers’ ESG practices tend to be higher, pushing to strive for differentiating, innovative, or leading ESG approaches, including articles 8 and 9 classifications based on the Sustainable Finance Disclosure Regulation’s (SFDR) nomenclature. As a reminder, article 9 classification refers to funds with one or several clear sustainable objectives, article 8 classification refers to funds that take ESG factors into consideration while article 6 funds are those that do not take ESG factors into account.

Regulation both at the national and European levels has contributed to push strongly for ESG integration, making ESG disclosure mandatory for most actors of the financial market, as SFDR requires investors to disclose ESG metrics, understand the negative impacts generated by their investments and communicate on these aspects.

This is particularly the case for Private Equity and Private Debt: while reporting frameworks and regulations at the national level already existed for equity/bond funds, this was not the case for funds of non-listed assets. Moreover, ESG analyses by non-financial rating agencies have always focused primarily on listed assets.

SFDR has been a real driver of change for Private Debt as it has established for the first-time common indicators for this asset class, the principal adverse impacts (PAI).

Alongside the PAI, the EU Taxonomy has also accelerated the debate on the impact of Private Debt: the classification of European economic activities according to their degree of environmental sustainability has made it possible to develop initial analytical frameworks for an asset class that was previously far from being involved in discussions on the positive or negative effects of credits on climate change.

Beyond external factors and regulatory considerations, the analysis of potential borrowers’ ESG performance provides an extra level of risk and opportunity analysis, assuming that ESG factors may affect financial performances and can be a driver of risk. The awareness of ESG risks and opportunities demonstrates maturity and readiness for future challenges and thereby contributes to reducing ESG risks, such as those associated with a transition to a low-carbon economy.

Lastly, borrowers tend to be more demanding with regard to the support that investors, whether equity or debt investors, can provide them on ESG matters. Indeed, there seems to be a growing demand for lenders’ sensitivity to ESG, which can turn into a market differentiator and driver of competitivity, in a context of competition among lenders. As such, ESG can be a differentiator and contribute to a borrower’s decision.

2. Embedding ESG in the investment process

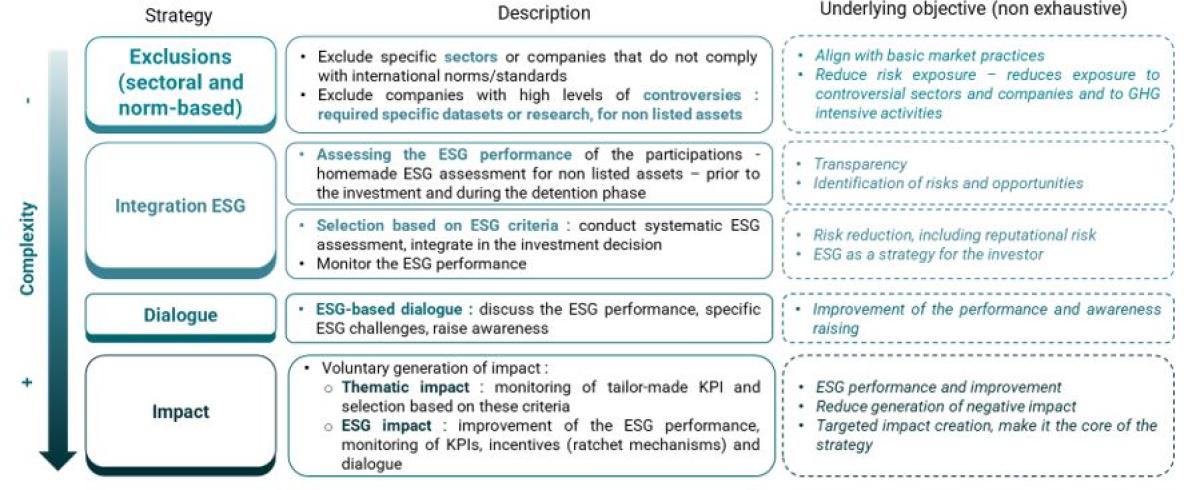

The traditional approaches of Responsible Investment can also apply to the debt market. ESG can reflect different visions from investors as regards to their role, ranging from more basic and less complex practices to advanced and complex practices which correspond to the ESG strategy and objectives set at the investor level. Investors can combine and create tailor-made strategies.

Below, the various approaches of Sustainable Finance applied to Private Debt are described.

Negative screening

Prior to the deal, asset managers can apply a negative screening, which corresponds to the exclusion of potential borrowers on ESG criteria, such as:

- Exposure to controversial activities and sectors (weapons, tobacco …).

- Norm-based or controversy exclusions: companies that do not respect international standards and principles, such as Human Rights, or that face controversies. As a reminder, a controversy is defined as an event that has negative impacts on sustainability factors, such as societal, social or environmental factors.

Should the asset manager have an exclusion policy, the negative screening applied shall match the policy’s exclusions to the least but can also be extended. Negative screening is a standard market practice that contributes to reducing exposure to sectors considered as risky: it can also be a means of addressing sustainability risks identified by the investors, as required by SFDR.

ESG Screening: assessing the ESG performance and/or apply positive screening

ESG screening corresponds to the systematic collection of ESG data, for various purposes. It can then be used by the asset manager to apply an additional layer of selection, based on the achievement of ESG targets or minimum ESG requirements. The data collected during this initial ESG assessment can also be used by the asset manager as the basis for dialogue or to identify areas for improvement.

It requires developing an ESG assessment methodology, to conduct ESG due diligence with pre-determined thresholds. When developing an in-house methodology, the investor can tailor the assessment conducted, deployed with tools such as an ESG questionnaire and dialogue.

A major benefit of developing an in-house methodology lies in the opportunity for the investor to focus on issues and topics which are the most material and relevant to them. However, it reduces the market homogeneity regarding ESG assessment as each investor develops its own analytical framework. The same company can thus have a different level of ESG performance according to the investor’s interests, concerns, and main focuses. Positive screening can be challenging for this asset class as a result of the lack of publicly available and homogenous information, the lack of data collected by potential borrowers, and a lesser level of maturity as regards to ESG and sustainability compared to listed peers.

During the holding period, a similar ESG assessment process can be applied. The investor’s approach then consists of accompanying borrowers to improve their ESG performance.

Monitoring the ESG performance

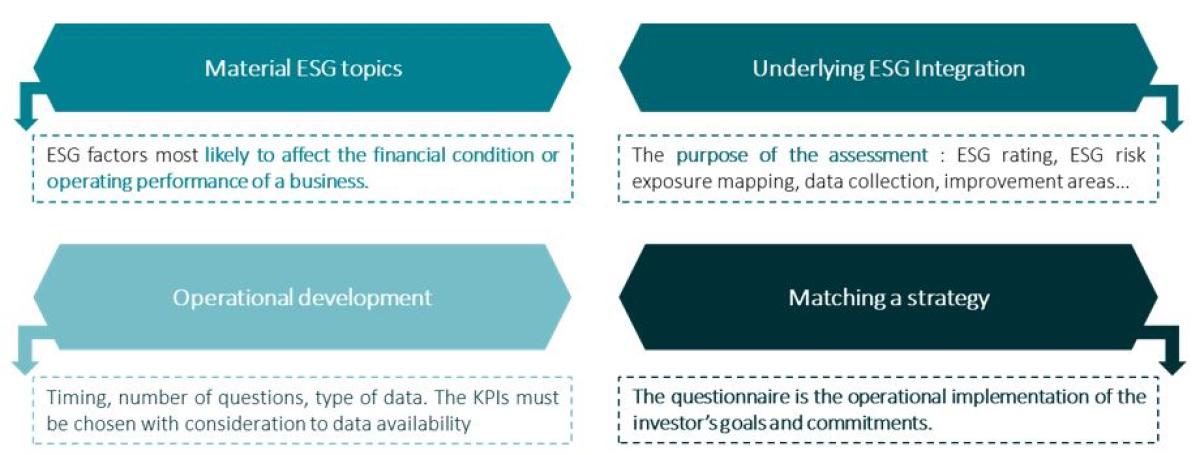

ESG Integration can also involve the monitoring of ESG performance through the deployment of an ESG questionnaire, which can be a similar or the same as the one used to conduct the ESG Due Diligence or the initial ESG assessment

Conducting ESG assessments requires the investor to develop an in-house assessment methodology or to externalize it with experts, tailored to its needs and topics of interest, as well as to the type of actors that is being assessed. Below, a non-exhaustive list of elements to be kept in mind in order to design an ESG questionnaire:

By asking borrowers to measure their performance and report it through a questionnaire, lenders contribute to enhancing the borrower’s awareness of ESG-related issues. Furthermore, the ESG assessment is also the tool that will enable investors to collect the data for reporting or compliance requirements. Indeed, funds classified as article 9 or funds managed by asset managers above the size threshold defined by SFDR are compelled to report on the Principal Adverse Impacts of their underlying investments. The PAI indicators can thus be integrated into the ESG questionnaire.

ESG-terms integration in loan documents

Investors can integrate ESG-related clauses in the lending terms and documents. An ESG clause can be a major leverage of ESG integration as it offers an opportunity to engage the parties on ESG from the inception of the transaction. The clause should enhance the ESG commitment of the borrower and can integrate various elements, such as the discussion of ESG topics at Board meetings, mandatory reporting on specific KPIs, and monitoring, and improvement of pre-determined criteria, designed and agreed upon during the deal settlement.

Integrating an ESG clause into a contract can also consist of requiring the borrower to respond to an ESG questionnaire at a predetermined frequency. The clause incentivizes borrowers to communicate and assess results while raising their awareness on these issues.

Dialogue

Dialogue is the equivalent of active ownership applied to debt and is key to building trust with borrowers. Dialogue can promote ESG topics in order to raise awareness and improve the ESG performance of borrowers. This lever for action is relevant for direct lending only and not for syndicated loans.

Dialogue can offer qualitative insights into management’s sensitivity to and awareness of ESG-related risks and issues, which cannot be grasped through quantitative ESG due diligence. It provides additional information for the investment decision, in the pre-deal phase. It also demonstrates interest in ESG topics to the potential borrower, in a context of competition among lenders.

During the holding period, ongoing dialogue can be conducted on ESG-related topics. Should ESG assessments be conducted, the results can be used as a basis for dialogue in order to analyze the potential improvements that can be achieved as well as the ESG risks identified. Dialogue can also be leveraged to discuss events, such as controversies, that might occur and which could be of significant ESG relevance with financial or ESG impacts.

Measure outcome and report

Beyond the analyses conducted for ESG integration purposes, there should be strong emphasis put on ESG outcome measurement and reporting. The growing pressure for disclosure is the result of the demand for accountability and transparency, arising from civil society, institutional investors, and regulators. Reporting needs to provide information on the ESG strategy adopted, the objectives and resources dedicated to achieving the objectives, and the sustainability outcomes and results.

3. ESG integration in Private Debt offers opportunities for financial innovation

Private Debt appears to be an asset class for which there is plenty of possibilities for financial innovation, within financial products themselves but also to disrupt traditional collaboration and business practices between stakeholders. Below, two examples of innovations are described, the prior being the impact-debt mechanism, also referred to as ESG-linked loan, the latter being the potential of coordination with Private Equity Sponsors, an innovative market dynamic.

Impact-debt mechanism or ESG-linked-loan

Among the impact debt mechanisms, a growing market practice consists of incentivizing borrowers to improve their ESG practices through the implementation of ESG-related reductions in the cost of debt through a margin ratchet mechanism.

The potential lender conducts an ESG assessment prior to the investment and identifies Key Performance Indicators (KPI) that are material to the borrower and that need to be improved – the number of KPIs can vary according to the lender’s expectations or the borrower’s maturity.

For each KPI, the lender and the borrower agree on a target to achieve within a determined time horizon. The targets have to be ambitious yet achievable, material, and consistent with the investor’s ESG goals.

The achievement of the ESG target(s) is associated with a capital cost reduction. The more criteria the company meets, the larger the cost reduction. The KPIs are monitored and reviewed annually. The lender can also apply a penalty if a target is not achieved.

Benefits of these mechanisms

- In a market with fierce competition between investors, impact debt can give a competitive advantage to the lender, who demonstrates interest in extra-financial issues.

- Determining the KPIs and monitoring them fosters dialogue and incentivizes the borrower to collect ESG data.

- The incentive is strong for companies, which creates a favorable context for them to achieve their goals.

- The cost reduction corresponds to a lower exposure to ESG risk: the risk/return ratio is close to stable.

Risks associated with this mechanism

- As the market is highly competitive and prices low, a margin ratchet mechanism might lower already low prices.

- The difficulty lies in defining targets that are ambitious and require efforts from the borrower to achieve them but have to be reachable and consistent. Too easy targets to achieve expose the exercise to “impact-washing” criticisms.

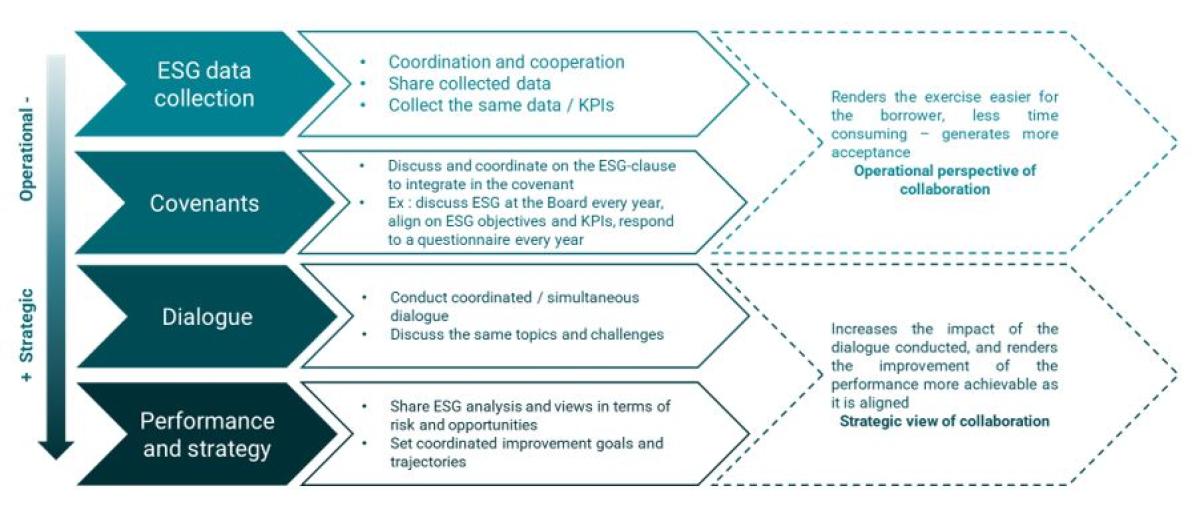

Coordination with Private Equity Sponsors – creating new market dynamics

Lenders can coordinate with Private Equity Sponsors when it comes to ESG-related topics. This coordination can apply at several levels and take different forms, ranging from a more operational collaboration to a more strategic one, as illustrated in the figure below.

Outlooks for ESG Integration in Private Debt

The greatest challenge for Private Debt is access to data. Indeed, despite the resources available for ESG research purposes (desk research, third-party providers, technical experts, legal due diligence documents, co-investors, ESG questionnaires, and dialogue with management), there is a great difficulty to collect relevant ESG data, which can be explained by several factors:

- Borrowers do not systematically track their ESG impacts and therefore do not have information – this is likely to become less of an obstacle with regulation introducing more requirements and extending the scope of application of mandatory non-financial reporting. The Corporate Sustainability Reporting Directive (CSRD) indeed broadens the scope of mandatory reporting as opposed to the Non-Financial Reporting Directive (NFRD) due to the lower size thresholds.

- Companies are solicited by several investors to respond to their ESG questionnaires. As ESG questionnaires vary from one investor to another, filling them in becomes a burden for companies, leading to them not responding.

- There can be a mismatch between the data collected by the borrower and the data required by the lender. This is likely to become less of an issue with the introduction of the CSRD and entry into force of the European Single Access Point.

There is a lack of public reporting obligations for non-listed and small companies and therefore a lack of available data. This challenge can be partially overcome with the development of internal capacity to gather ESG data, such as ESG questionnaires which comprise quantitative and qualitative questions, or through market initiatives that foster homogeneity in ESG data collection.

The forthcoming regulation and the entry into force of CSRD are likely to ease the access for investors to ESG data, as companies will be compelled to disclose standardized ESG metrics and data. The growing regulatory constraints on disclosure as well as the fund classification introduced by SFDR also contribute to enhancing market transparency, especially with regard to ESG.

Overall, the Private Debt market has a fast-paced evolution, especially for ESG-related concerns. The constant financial innovation, the growing demand from borrowers for support in the implementation of CSR strategies and non-financial support as well as the market’s scrutiny and expectations on ESG integration contributes to rendering this asset class a perfectly well-suited one for ESG integration, in spite of the data constraints it faces and the regulatory uncertainties.

Conclusion

To conclude, despite the complexity and variety of tools at the disposal of Private Debt investors, this asset class seems to be very well suited to foster a higher level of ESG integration. Indeed, it offers a new area for innovative practices which will be supported by an always more demanding regulation.

Data-related constraints are likely to become less challenging with the entry into force of CSRD and the increasing capabilities of financial actors, who tend to be often equipped with modeling tools or accompanied by independent experts. Also, borrowers are likely to become more familiar with ESG data monitoring and collection, which will contribute to smoothening the exercise.

Footnotes:

[i] Private markets rally to new heights (2022), McKinsey Global Private Markets Review 2022, https://www.mckinsey.com/~/media/mckinsey/industries/private%20equity%20and%20principal%20investors/our%20insights/mckinseys%20private%20markets%20annual%20review/2022/mckinseys-private-markets-annual-review-private-markets-rally-to-new-heights-vf.pdf

About the Authors:

Lucie Delzant, Sustainable Finance Consultant

Lucie accompanies investors in the design and implementation of their ESG strategies, which encompasses operational, strategic but also regulatory aspects. Lucie has developed expertise on climate-related topics, including carbon, climate-related risks and more recently on biodiversity. Indeed, Lucie has coordinated the climate-related work (carbon and biodiversity) at EthiFinance and has contributed to the development of an in-house methodology to assess biodiversity-related risks at the portfolio level. Lucie holds a Magistère in International Relations from the University of Paris 1 Panthéon-Sorbonne and a Master of Science in International Sustainability Management from ESCP Europe.

Enrica Bruna, Sustainable Finance Consultant

Enrica supports investors in designing their ESG approaches as well as in understanding regulatory issues in sustainable finance at the European and national levels. She is also part of a working group of the EFRAG Secretariat from 2021 that supports the Project Task Force on European Sustainability Reporting Standards (PTF-ESRS) in defining European sustainability reporting standards for companies subject to CSRD. Enrica holds a degree in Risk Management in Developing Countries from Sciences Po Bordeaux and in International Relations from the University of Turin.

Rémy Estran-Fraioli, PhD, FRM, CAIA, Modeling & Analytics Director

Rémy is the director of the « Modeling & Analytics » department at EthiFinance, an innovative European rating, research, and advisory group serving sustainable finance. He heads EthiFinance’s team of quantitative consultants and advises the largest European banking institutions on their financial and non-financial risk models. Graduating from Paris 1 Panthéon-Sorbonne University with a PhD in finance, Rémy has conducted research in risk modeling and has authored several articles in both professional and academic journals and books. He is also a former lecturer in finance at Paris Dauphine University and at ESCP Business School.