By Colin Hatton, Senior Consultant, Endowment and Foundations Team.

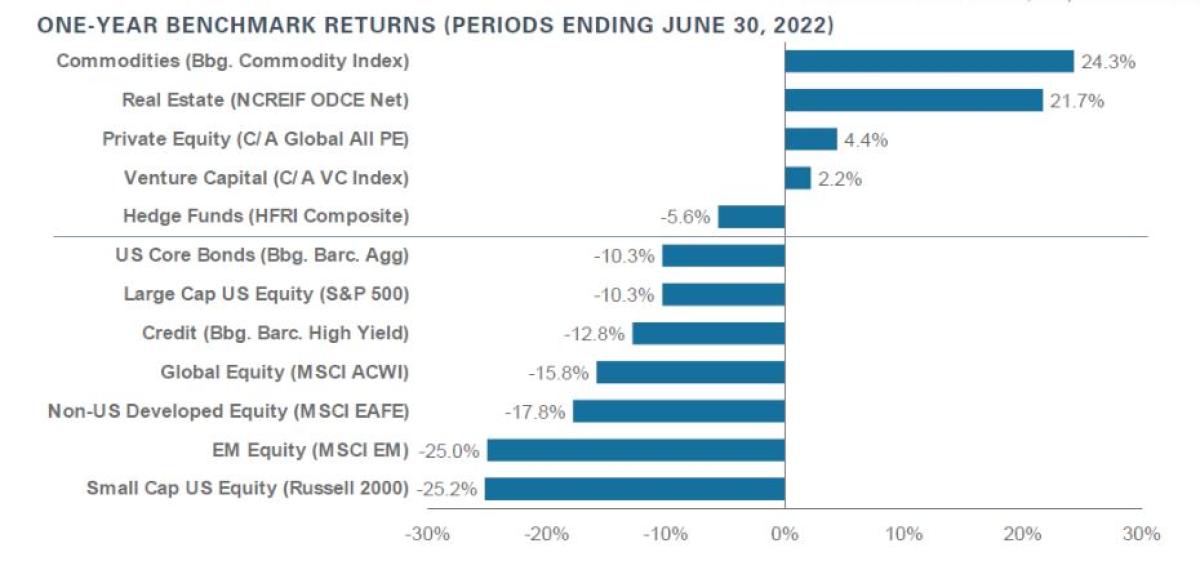

Buoyed by fiscal year 2021’s record endowment returns, many higher education institutions were starting to recover from the costs of managing through COVID-19 restrictions. But then the dark forces of inflation increased operating costs and budget pressures for many institutions. To rein in inflation the Federal Reserve began to tighten its policies and markets responded in brutal fashion. Both equity and fixed-income markets were in the red, with the MSCI ACWI Index down 15.8% and the Bloomberg Barclays U.S. Aggregate Bond declining 10.3% for the one-year period ending June 30, 2022.

In these challenging times, mega endowments continued to outpace their smaller peers. As in years past, private equity outperformed on a relative basis. In the fiscal year 2022, mega endowments also benefitted from greater allocations to other diversifying asset classes such as real estate, real assets and hedge funds. Investments in these asset classes helped soften the impact associated with drawdowns in the public market.

Strong performances in public equity and fixed-income markets in the post-global financial crisis world led many to question the value of various diversifying asset classes, such as real assets and hedge funds. Public equities and fixed-income securities were among the strongest performing classes in the protracted zero-interest-rate environment, challenging the merits of diversification.

To exacerbate matters, these diversifiers provided little to no protection during the rout fueled by the COVID-19 pandemic in 2020. While all higher education endowments have generally reduced their exposure to these diversifying asset classes in recent years, industry reports show that the biggest endowments maintained the largest allocations to real assets, private equity and hedge funds.

Benefitting from their scale, mega endowments tend to produce stronger returns than smaller institutions. Over the trailing one-year period ending June 30, 2022, the median mega endowment lost 4.1% (net of fees) versus the E/F Universe’s loss of 12% (net of fees).

Kansas State University Foundation (KSUF) topped the list for FY 2022 with a 5.7% return. In the Fund’s annual report, CIO Lois Cox credits investments in private capital and diversifying strategies for the strong returns. Diversifiers collectively returned 42.7% for the fiscal year with investments in short-term trading strategies like global macro and statistical arbitrage benefiting from increased market volatility, and private real estate, real asset and commodity investments responding to rising inflation.

We can surmise that alpha decisions added 5.8 percentage points to overall returns based on the Foundation’s Policy Index of -0.1% for the fiscal year. By itself, the Policy Index would have ranked in the top 10 of all reporting institutions. Paul Chai, Senior Director of Investments at KSUF, highlighted that, based on forward-looking views, they are increasing their target allocation to diversifying strategies such as hedge funds, private real assets and private credit1. Ms. Cox notes that while they are pleased with returns for the fiscal year, their focus remains on longer-term outcomes and meeting the ultimate objective of intergenerational equity.

In recent years, we theorized large endowments were generally outperforming their smaller peers due to higher allocations to private markets. In FY 2022 this remained a driving factor but extended to nearly all alternative asset classes. Interestingly, among broad asset classes, alternatives outperformed traditional investments for all asset classes over the past year, accounting for the large differential in returns between mega endowments and their smaller peers. At the start of 2022, the average endowment had 69% of their portfolio invested in public equity and fixed-income managers. Conversely, endowments with more than $1 billion in assets under management had only 38%2. The largest share of this difference came from private equity and venture capital (34.7% vs 17.7%), but the mega endowments also had greater allocations to real assets (10.5% vs. 6.6%) and hedge funds (18.1% vs 10.1%). In 2022, we experienced a challenging market environment with higher interest rates and inflation. In such an investment landscape, we expect real assets and active hedge fund strategies to outperform. However, we expect the difference between public and private market performance to narrow over the coming quarters. READ MORE: Taking Stock: Private Markets (Part One): Today’s Market Dynamics

During the past fiscal year, when public markets were down significantly, investors that maintained discipline and remained committed to holding a diversified, all-weather portfolio were rewarded. As we enter a new year, we recommend clients remain disciplined in their asset-allocation process and assess the role of all investments within their portfolio, particularly as we enter a higher interest-rate environment. While many have benefitted from investments in diversifying asset classes over the past year, chasing allocations in the hottest asset classes rarely produces long-term success.

References:

1 Kansas State University Foundation 2022 Endowment Report, https://ksufoundation.org/wp-content/uploads/2022/10/Endowment-Report-2022.pdf

2 2021 NACUBO-TIAA Study of Endowments. Difference between dollar weighted average allocation of >$1B Endowments and Equal Weighted average allocation of all institutions. https://www.nacubo.org/research/2021/nacubo-tiaa-study-of-endowments

3 As of October 1, 2022

About the Author:

Colin Hatton, CFA, CAIA, Sr. Consultant - Colin joined NEPC in 2015 and has 14 years of experience in investment consulting and financial services. He is a senior member of our Endowment & Foundation consulting practice. Colin serves as a trusted advisor to an array of Endowment and Foundation clients and has meaningful expertise both in technical analysis (asset allocation studies, manager searches, investment policy) but also in working with investment committees and staff on their investments goals and governance challenges. In addition to his client responsibilities, Colin is a senior member of NEPC’s Asset Allocation and Private Investment Committees.

Prior to joining NEPC, Colin worked at A. Gary Shilling & Co., Inc. where he was responsible for developing macroeconomic analysis and market insights for various Fortune 500 companies, Investment Management Firms and Institutional Investors.

Colin earned his B.A. in Economics from The University of the South. He also holds the Chartered Financial Analyst (CFA) and the Chartered Alternative Investment Analyst (CAIA) designations.