By Florence Angles, CAIA, FDP is managing principal within Capco in charge of Finance, Risk and Compliance (including ESG).

ABSTRACT

Growth is only sustainable if it preserves natural capital and integrates, beyond its economic implications, the environmental, social, and governance dimensions. It is a new social project advocated by the public authorities and which is applied at the corporate level through “corporate social responsibility” (CSR). Sustainability is gradually gaining ground and affecting the whole economy. As the intergenerational component of sustainable development emphasizes the objective of a long-term horizon, it is necessary to develop new instruments and mechanisms for financing the economy. Finance and sustainability come together to give rise to the so-called sustainable finance. Europe is the epicentre of sustainable finance. The lack of a clear definition has led the European Commission to work on developing a common classification or taxonomy. Environmental, social, and governance (ESG) concerns are at the heart of regulations in the financial services industry. Today, ESG is no longer just an acronym but a reality, expected to reach a third of assets under management worldwide by 2025. It is spreading across all asset classes, including the less liquid ones. ESG now defines the new frontiers of alternative investments.

1. INTRODUCTION: IS GROWTH SUSTAINABLE?

“High-income countries are responsible for 74 percent of excess resource use causing ecological breakdown”[i]. In 2012, WWF[ii] had already warned that “if we continue like this, by 2050 we will need three planets. Our pattern of consumption is unsustainable.”

Since the 1970s, we have realized that we live in a world of limited resources. This scarcity of raw materials will inexorably lead to a loss of momentum in the economy, which not only responds to a Newtonian mechanistic vision but on the contrary follows the law of entropy and more particularly the second law of thermodynamics. Thus, growth is only sustainable if it preserves natural capital and also takes account of environmental and social factors. It is about sustainable development, a new paradigm of economic development.

2. FROM SUSTAINABILITY TO ESG

2.1 How can we define sustainable development knowing that this term is very often used?

The first definition of sustainable development, often used by academics and in official texts, was provided in the Brundtland report “Our common future” of the U.N. Commission on Environment and Development in 1987. Sustainable development is “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” This definition highlights the notion of intergenerational equity, between present and future generations, and lays down the three pillars of sustainable development (SD): economic, social, and environmental.

This approach to sustainable development also applies at the microeconomic level, at the company level, with “corporate social responsibility” (CSR). CSR is not a recent concept; it came from across the Atlantic with a strong religious connotation of Protestant inspiration dating from the 1920s. The successful businessman must also give back to society a kind of implicit contract: the “trusteeship”. It was only in the 1950s that the term CSR appeared in the U.S. in the context of social movements. It gradually spread to the academic world when Howard R. Bowen, an economist of Keynesian inspiration, published his first book on the subject: “Social responsibilities of the businessman”. The maximization of profit for the shareholder is no longer the sole objective of the manager, who also aims to consider other stakeholders, perhaps as a means of fighting against the rise of communism at the time but also possibly fuel to the fire of this divisive subject. CSR is thus intimately linked to the notion of corporate governance, the separation of powers between shareholders and managers, the role of the latter, and their ethics. This gave rise to a management discipline based on the study of 2. FROM SUSTAINABILITY TO ESG

2.2 How can we define sustainable development knowing that this term is very often used?

The first definition of sustainable development, often used by academics and in official texts, was provided in the Brundtland report “Our common future” of the U.N. Commission on Environment and Development in 1987. Sustainable development is “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” This definition highlights the notion of intergenerational equity, between present and future generations, and lays down the three pillars of sustainable development (SD): economic, social, and environmental.

This approach to sustainable development also applies at the microeconomic level, at the company level, with “corporate social responsibility” (CSR). CSR is not a recent concept; it came from across the Atlantic with a strong religious connotation of Protestant inspiration dating from the 1920s.

The successful businessman must also give back to society a kind of implicit contract: the “trusteeship”. It was only in the 1950s that the term CSR appeared in the U.S. in the context of social movements. It gradually spread to the academic world when Howard R. Bowen, an economist of Keynesian inspiration, published his first book on the subject: “Social responsibilities of the businessman”. The maximization of profit for the shareholder is no longer the sole objective of the manager, who also aims to consider other stakeholders, perhaps as a means of fighting against the rise of communism at the time but also possibly fuel to the fire of this divisive subject. CSR is thus intimately linked to the notion of corporate governance, the separation of powers between shareholders and managers, the role of the latter, and their ethics. This gave rise to a management discipline based on the study of from the Vietnam War and the Watergate scandal. It was at this time that the first SRI fund to adopt a best-in-class approach appeared, the Pax World Fund, which comprised of all sectors and favored socially responsible companies. This approach aims to combine financial performance with ESG (environmental, social and governance), or extra-financial criteria. In Europe, with the exception for Sweden, these investments only appeared late in the 1980s and 1990s under the impetus of the Brundtland report, “Our common future”, and sustainable development. This specific sector of finance is based on four pillars:

- New behaviors

- Compliance with sustainable growth

- Finance close to individuals

- Inclusive finance.

3. TRANSPARENCY WOULD BE ONE OF THE RULES OF THE GAME

Europe is the epicenter of sustainable finance, even though the market is showing signs of maturity and there is no clear definition of what is meant by the term sustainable finance. As a result, the European Commission has decided to undertake a dedicated action on a common classification or taxonomy. Environmental, social and governance (ESG) concerns are at the heart of regulation in the financial services industry. To increase the transparency on sustainable products and to avoid greenwashing, the European Union issued the Sustainable Finance Disclosure Regulation (SFDR) in 2018. It introduces various ESG disclosure-related requirements for financial market participants and financial advisors at entity, service, and product level. This phased regulation requires more transparency and disclosures about integration of sustainability into the investment process, definition of the fund as one of three classifications (Article 6: non-ESG focused financial products, Article 8: funds that promote environmental or social characteristics; or Article 9: funds that have sustainable investment as their objective), and Principle Adverse Impacts (PAIs) of investment decisions on sustainability factors. Level 1 came into force on March 10, 2021 and the Level 2 implementation, which is scheduled for January 2023, will require institutions to report on 18 PAIs alongside voluntary areas. However, SFDR follows a “comply-or-explain” principle for managers (whether traditional or alternative managers) with less than 500 [iii]employees and is applicable outside Europe for companies that market their funds in the E.U. To be compliant, fund managers face a great challenge: the availability and quality of ESG data.

SFDR is not the only E.U. regulation, it is a part of a broader package. The regulatory pressure, which many consider a challenge, is also at the root of the rise of ESG investing, which is more specific (focusing on three pillars: environmental, social, and governance) and measurable than “sustainability”.

Today, ESG is no longer just an acronym, it has become a reality, expected to reach U.S.$53 trillion by 2025, a third of global assets under management. The ESG agenda has thus become a growing priority for the financial services sector. This groundswell was reinforced during the COVID-19 pandemic, prompting institutions to prioritize their strategy, notably by integrating these three criteria into risk management and product development. Regulators have also made it their priority and we are far from the end of the regulatory wave; this is just the beginning!

4. THE NEW FRONTIER OF ESG: ALTERNATIVE INVESTMENTS

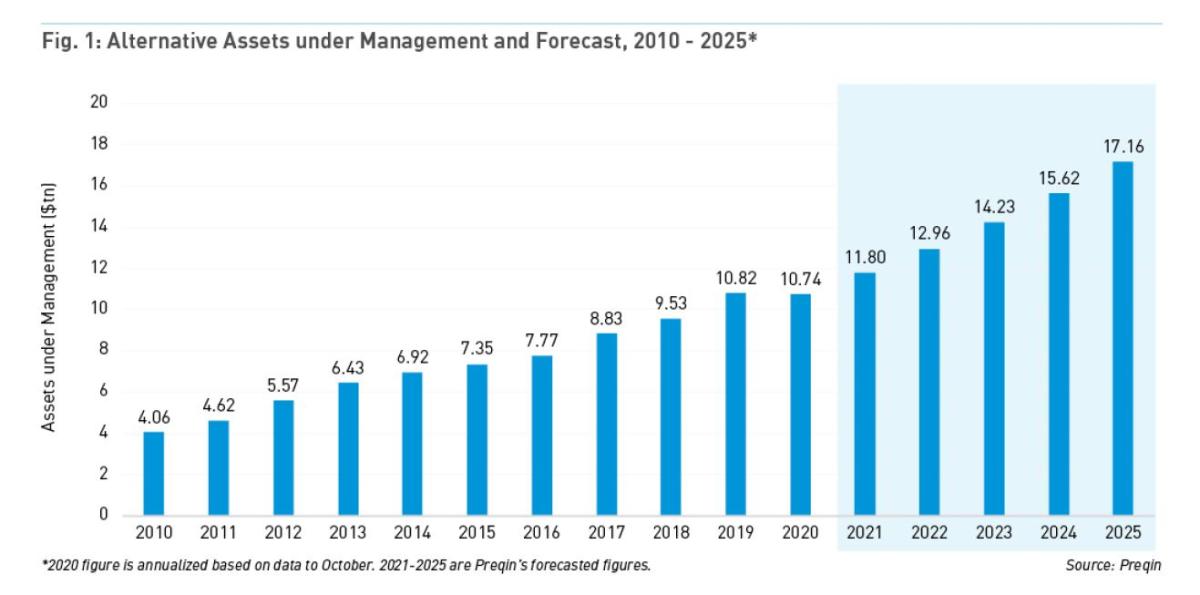

ESG concerns are spreading across the asset management industry, including alternative investments. Alternative investments are not new, and can be tracked back as far as the Industrial Revolution.4 Despite its lack of formal definition,[iv] it can be distinguished from traditional investments (stock, bond and cash related instruments). Considered initially as a very heterogeneous niche, private markets have been growing steadily over the last decade and this trend is expected to continue, reaching U.S.$23 trillion by 2026.[v]

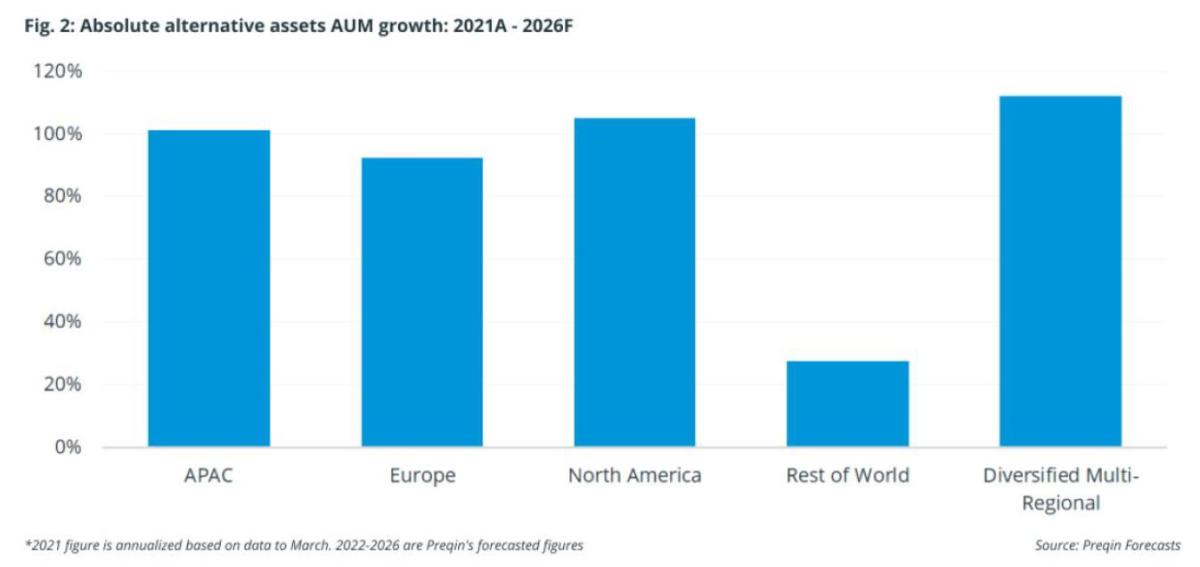

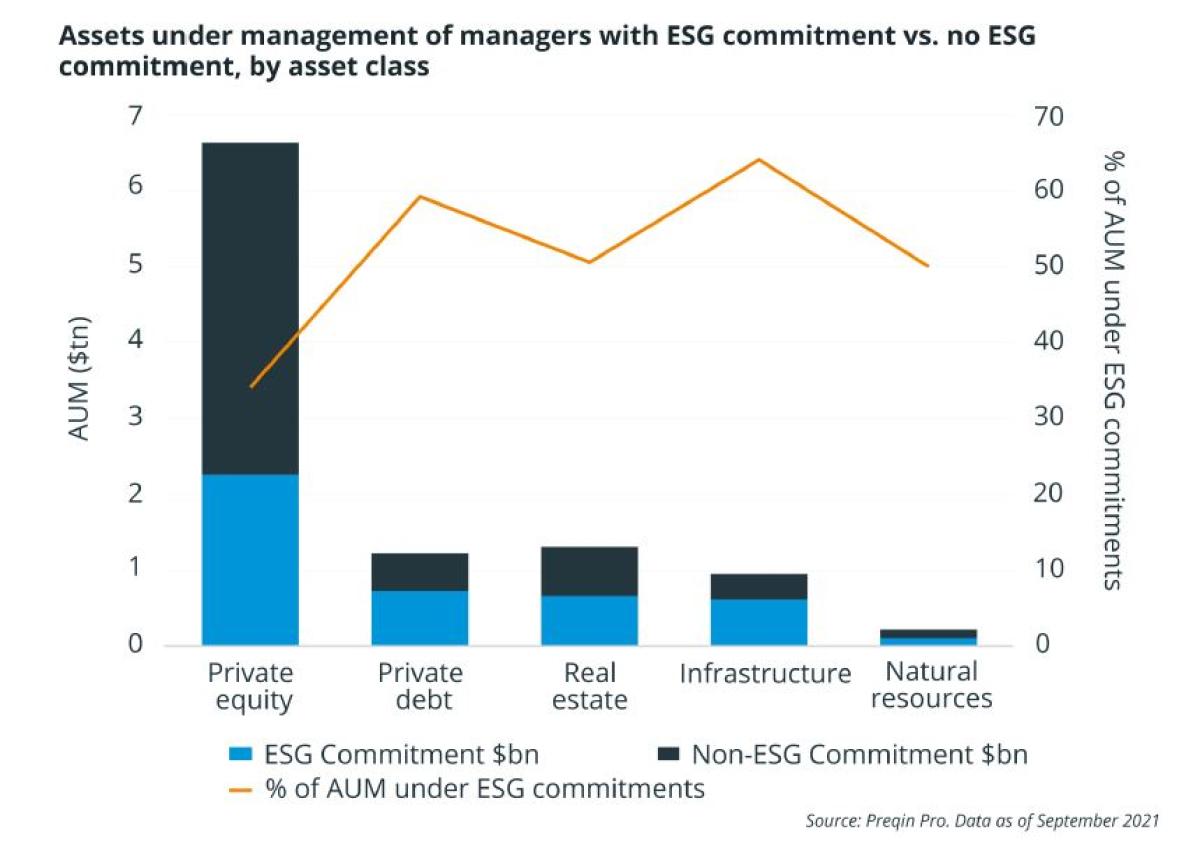

The key driver for this growth was the low interest environment in which (institutional) investors were looking for new sources of income. The ESG wave has also reached the private markets: as of October 2021, “42 percent of AUM across private capital is managed by funds that have an active ESG policy”,[vi] meaning U.S.$4.37 trillion of the U.S.$10.3 trillion market. This ESG trend is noticeable for all asset classes, with the winner being “infrastructure” (64 percent of AuM in ESG committed funds) followed closely by “private debt” (59 percent of AuM in ESG committed funds). The ESG impact on private equity is lower (only 34 percent) but has the highest overall ESG committed value of AuM, U.S.$2.3 trillion. In terms of region, APAC seems to be a less mature market than Europe and North America.

According to Preqin H1 2022 Investor Outlook, nearly threequarters (72 percent) of investors believe fund managers are adopting ESG policies because of pressures from existing and prospective limited partners (LPs). Hence, investors are the key driver for more ESG transparency in private markets. Historically, there was less pressure for private companies to disclose ESG information, but that has changed rapidly as asset owners are exercising their influence to access this information by engaging the general partners (GPs). As increasing numbers of asset owners and LPs are integrating ESG into their investment process (as of May 2022, nearly 700 asset owners globally have signed on to the PRI), they now want to better understand what GPs and alternative fund managers are doing in terms of ESG and how it is embedded in the investment statement.

to disclose ESG information, but that has changed rapidly as asset owners are exercising their influence to access this information by engaging the general partners (GPs). As increasing numbers of asset owners and LPs are integrating ESG into their investment process (as of May 2022, nearly 700 asset owners globally have signed on to the PRI), they now want to better understand what GPs and alternative fund managers are doing in terms of ESG and how it is embedded in the investment statement.

alternative fund managers may have to deal with different questions and different formats that create some difficulties for them to understand and collect all the relevant data to answer. However, some templates are available to investors to assess ESG integration such as:

- ILPA (Institutional Limited Partners Association) ESG Assessment Framework gives standards to LPs to better evaluate and compare the ESG integration of their managers.

- The PRI’s “Limited Partners’ Responsible Investment Due Diligence Questionnaire” is intended to help LPs “understand and evaluate a General Partner’s (GP) processes for integrating material environmental, social, and governance (ESG) factors into their investment practices and to understand where responsibility for doing so lies.”

Investors now demand additional transparency into their holdings and consistent asset-level data across their portfolios, including private investments. This additional transparency leads to a huge growth in data needs and consumption and creates new challenges for GPs and alternative fund managers, who are not always equipped to provide, analyze, and report accurate data at the level of granularity required. They are facing an important data challenge, as this information is not publicly available and there is also no clear and consistent approach across asset types. Furthermore, the data may sometimes be in different systems and need to be retreated manually, increasing the risk of operational errors and decreasing at the same time data quality. This manual retreatment approach to data processing from fund managers and GPs leads to long delays in delivering the information to their investors. There is room for improvement in terms of innovation, agility, and risk management but this may require the modernization of IT tools and the use of new technologies.

Beyond the data challenge, the alternative investment industry is also facing a lack of standardization. For instance, for private equity and venture capital it is difficult to compare data between portfolio companies as they do not have the same data collection process, the same data quality, and disclosures. But the various stakeholders are fully aware of this standardization gap, and they carry out concerted actions. A concrete example is the ESG Data Convergence initiative launched in September 2021, gathering LPs and GPs from the private equity industry. This project seeks to standardize ESG metrics and provide a mechanism for comparative reporting for the private market industry representing U.S.$8.7 trillion in AUM and over 1400 underlying portfolio companies. There is certainly more that can be done in this space with these companies being just the tip of the iceberg but the economic motivation is there and the will appears to be following. Whether this can move across multiple geographies and jurisdiction as well as investment sizes and asset classes are yet to be seen.

5. CONCLUSION

Historically, Europe has led the way on ESG assets as well as serving as a global barometer, but the U.S. is catching up with 40 percent market growth over the past few years and now accounts for U.S.$17 trillion, or nearly half, of the global ESG assets under management. As the ESG agenda continues to gain prominence, with global ESG assets expected to grow to U.S.$53 trillion by 2025,[vii] there is an increasing demand from institutional investors not only in traditional investments but also in alternatives.

They expect more granular reporting to better understand where alternative fund managers and GPs are standing in terms of ESG journey. Transparency is now the rule of the game.

ESG is a great opportunity for the industry but also an important challenge due to the lack of standardized data and reporting framework. This data gap makes it harder for investors to assess funds’ performance and compare them to their peers from an ESG perspective – comparing on a so-called apples-for-apples basis.

However, the alternative investment industry is adapting to the ESG era and innovating through the development of common standards thanks to the collaboration of the different stakeholders. Hence, ESG data is on the way to becoming one of the main drivers of innovation and, combined with new technologies, it will become the solution instead of the problem to the challenge of a lack of standardization.

[iii] , first investment in infrastructure with the Transcontinental Railroad

[iv] CAIA Association

[vi] ibid

About the Author:

Florence Angles, CAIA, FDP is managing principal within Capco in charge of Finance, Risk and Compliance (including ESG).

During the last 3 years, Florence leads the ESG practice for Capco Switzerland including ESG mandates. Florence has 22 years of experience in banking and asset management, more particularly in the risk management field in Europe for Tier 1 banks, private banks and asset managers and was leading the Risk Management Practice of a big 4 in Switzerland. She has a strong knowledge of Swiss, EU and UK regulations including supervisory audit. she followed an engineering degree in France supplemented by a MBA in finance and a DBA in partnership with Georgetown University on the topics of ESG. Florence is also a certified ESG analyst from EFFAS.