By Adam Guy Orlebar Garrett, MEng (Oxon), MBA (IUJ), CQF, CAIA, Chief Investment Officer at Hong Kong based New Asia Ferrell Asset Management Limited where he is leading the firm's alternatives business including in the media investment space.

Introduction

In this article, we talk about specific examples of how investors can gain exposure to the media industry. But before we do that, let's first touch on why investors might want to gain exposure to media assets in the first place.

Diversification Benefits

One of the chief reasons that an investor considers alternative investments is because of the expected low correlation between an alternative investment asset class and those traditional asset classes that probably make up a significant portion of the investor's existing portfolio.

Why does an investor want something with low correlation? Because the key benefit of adding an investment that has a low correlation to the constituents in an existing portfolio is, as any student of finance knows, an expected improvement (i.e., reduction) in the overall volatility of the combined portfolio (thus improving risk-adjusted returns) as well as potentially improving expected absolute returns too.

We can easily do quick, indicative, back-of-the-envelope tests to see if, broadly speaking, such portfolio improvements seem to be the case for media investments too, by using various proxies both for our media asset class and for our traditional (e.g., equity and fixed income) investment asset classes. The following subsections show two such indicative tests, the first assuming we invest in movies, and the second assuming we invest in streaming content such as TV shows. We use both box office and home entertainment data from the annual THEME (Theatrical and Home/mobile Entertainment Market Environment) reports published by the Motion Picture Association of America.

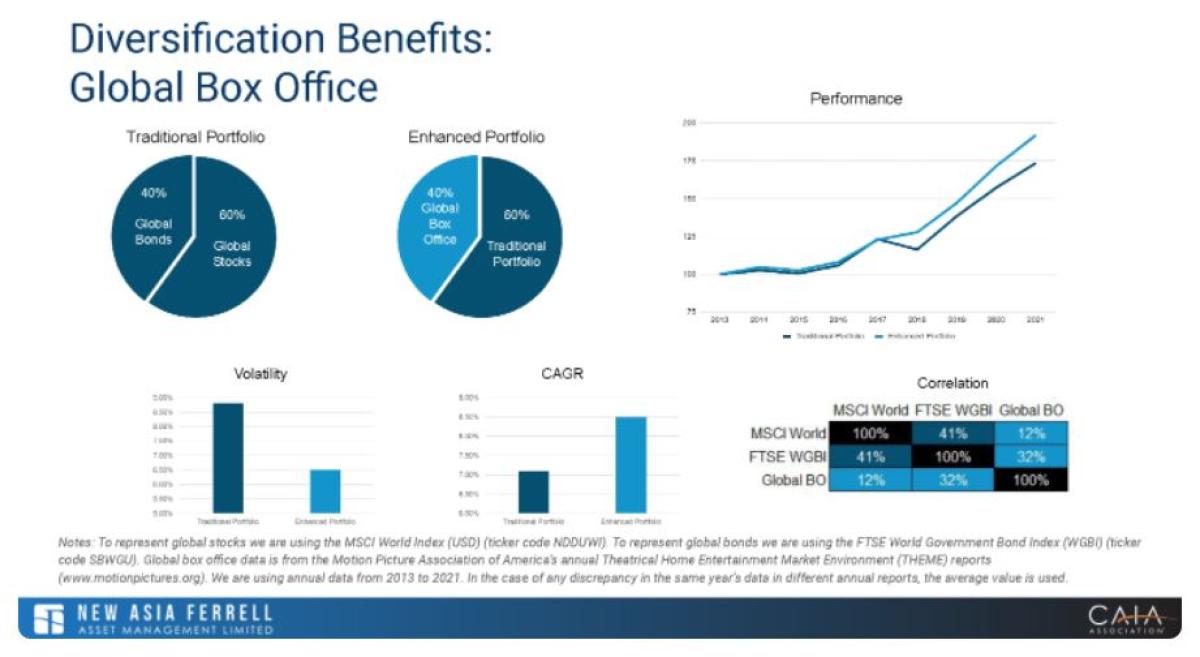

Diversification with Movies

In the following charts and correlation table we are using the MSCI World Index (USD) to represent global stocks, FTSE World Government Bond Index to represent global bonds, and global box office data to represent exposure to movie investments. We are assuming a traditional investor portfolio is 40% bonds and 60% global stocks, and we are comparing this traditional portfolio with an enhanced portfolio consisting of 60% of the original traditional portfolio with 40% performance from the global box office. In all calculations we are using annual data.

Note that, as expected we see improvements in both a lower volatility (8.8% to 6.5%) and a higher CAGR/annualized return (7.1% to 8.5%). This is because the global box office very lowly correlated to global stocks and global bonds (12% and 32% respectively).

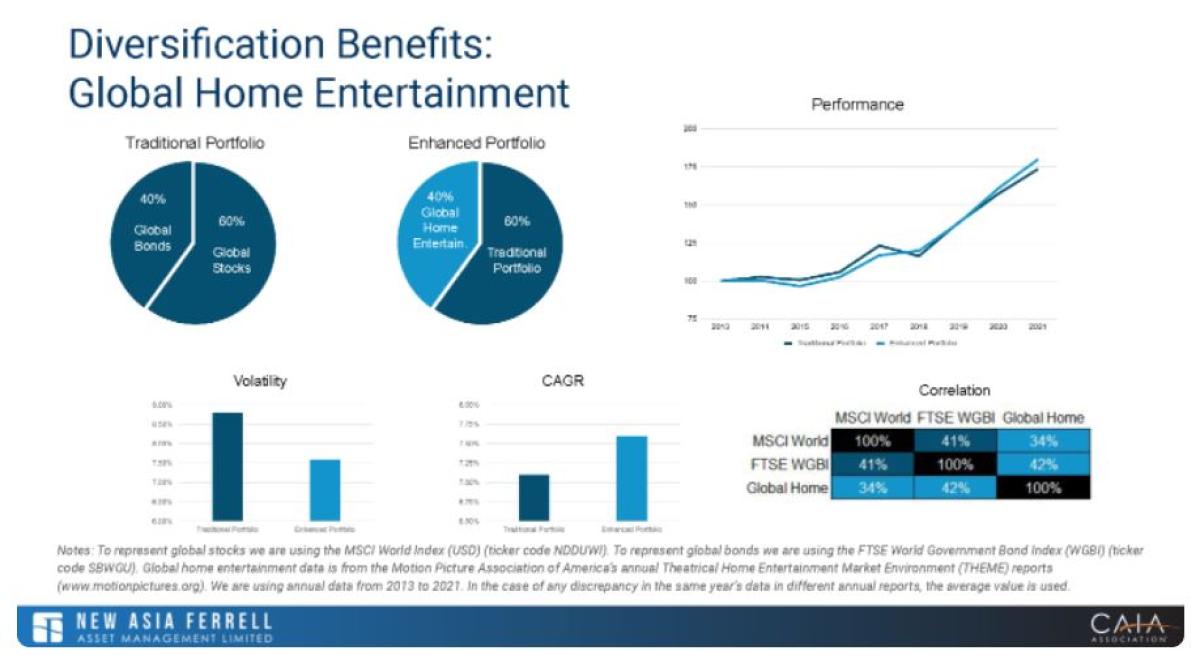

Diversification with Home Entertainment (i.e., Streaming Content)

In the following charts and correlation table we are using, once again the MSCI World Index (USD) to represent global stocks, and the FTSE World Government Bond Index to represent global bonds. We are now using global home entertainment data - defined as entertainment content viewed on all devices (both TVs and mobile devices) and includes both digital (i.e., streaming) and physical delivery (i.e., blu-ray and DVD sales and rentals) - to represent exposure to media investments to be consumed at home (typically via streaming). As before, we are assuming a traditional investor portfolio is 40% bonds and 60% global stocks, and we are now comparing this traditional portfolio with an enhanced portfolio consisting of 60% of the original traditional portfolio with 40% performance from the global home entertainment market. Again, in all calculations we are using annual data.

Once again, and as expected, we see improvements in both a lower volatility (8.8% to 7.6%) and a higher CAGR/annualized return (7.1% to 7.6%). The diversification benefits aren't quite as good as when we used the global box office data earlier, because correlation for the global home entertainment data, whilst still respectfully low, is slightly higher to global stocks and global bonds (34% and 42% respectively) than the correlation for global box office data was.

Nevertheless, the purpose of these quick, indicative, back-of-the-envelope tests is to provide a general indication of the ability for media assets to provide diversification to one's portfolio, which we have successfully done.

Common Investment Methods

For media investments specifically, CAIA Book II, Section 21.2.3 gives a comprehensive overview of the types of investments available. In summary, these are:

Equity:

- slate (to diversify risk)

- corporate (e.g., invest in production companies, VFX companies, startups, etc.)

- coproduction (to share the risk of a single project)

Debt:

- senior secured (using negative pickup, presales, tax credits/grants as collateral)

- gap financing (e.g., collateralized with unsold territories)

- super gap financing/junior debt (usually syndicated lending on any remaining budget gap)

Other:

There are also several options not mentioned explicitly in the CAIA book, including:

- investing in real estate (e.g., studio space)

- crowdfunding & NFTs for retail investors

However, like an over-the-counter option in the financial markets, every movie, and how it is financed, is typically uniqe. This is wonderfully exemplified by the title of the book "43 Ways to Finance Your Feature Film" by John W. Cones. In practice any movie will likely use a mixture of any number of these 43 different ways, resulting in many, many possible combinations to actually finance a movie.

Media Investment Landscape in US

Buyside firms in the US such as Blackstone have already recently noticed the profitable opportunities in content creation because of the current state of today's streaming content war-driven media industry. Journalist Jennifer Saba in a recent Reuters article entitled "Private equity will be potent Hollywood antihero" correctly describes the opportunities ripe for Blackstone and other such buyside firms:

“Blackstone steps into a battlefield… but a private-equity newcomer would have an advantage: rivals all have their own broadcast channels and streaming services to feed, whereas a standalone content-producer could sell each show to the highest bidder, becoming what some industry executives liken to an ‘arms dealer’.”

To reiterate this, Ms. Saba encapsulates in a nutshell what the media investment opportunity currently available for investors exactly is, namely where: "a standalone content-producer [sells] each show to the highest bidder".

Alongside Blackstone, according to Business Insider other major private equity investors currently active in Hollywood include:

- Apollo Global Management

- Atwater Capital

- Crestview Partners

- Guggenheim Partners

- KKR

- Providence Equity

- RedBird Capital Partners

- Shamrock Capital

- Silver Lake Partners

- TPG

- Yucaipa Companies

- Zelnick Media Capital

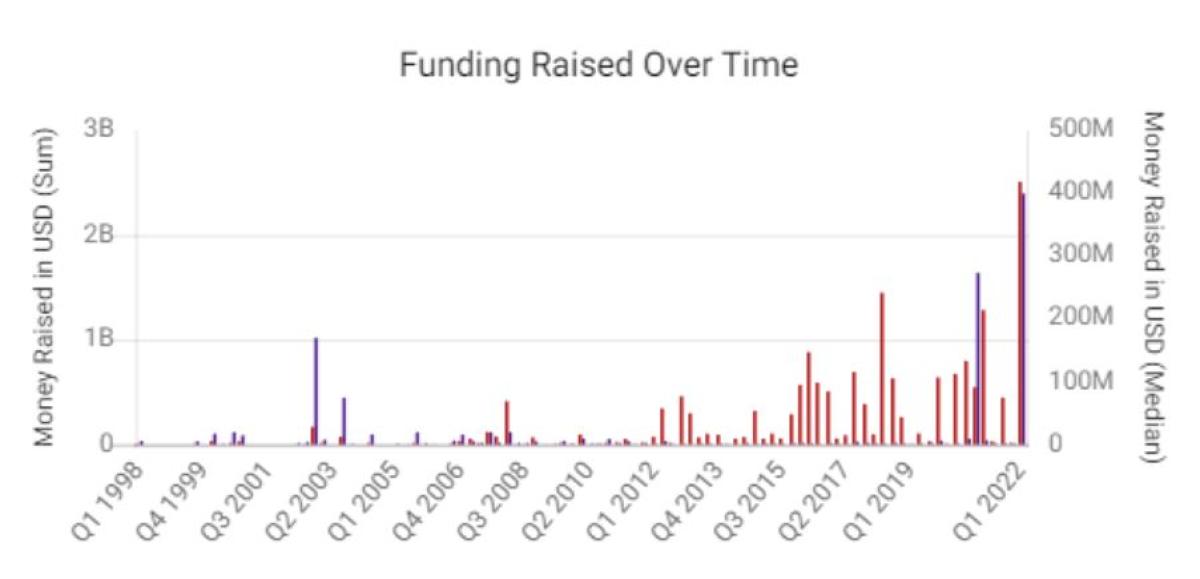

In the below chart we see how investment in film companies has continued to grow and reach new highs since 2016 according to Crunchbase:

Media Investment Landscape in Asia

Unlike in more mature markets like the US, Canada, and the UK, there currently aren't many investment opportunities in general for professional (let alone retail) investors in Asia.

However, we do expect that to change over time. Note that:

- Singapore is the main Asia hub for Hollywood companies to set up regional headquarters, and these companies are increasingly ensuring they have representative offices in Japan, Korea, and other countries too.

- Taiwan is fast becoming the key hub for Mandarin-language shows since the streaming platforms now recognize there is a large diaspora of Mandarin-speaking viewers outside China across Asia and around the world.

- As mentioned in the first article in this three-part series, Netflix and the other major streaming platforms recognize that carrying Asia content is important for international audiences including their domestic audience in the US, and there is an ongoing strong increase in content spend occurring in the Asia region.

Although there aren't many investment opportunities in Asia. There are a few. Besides New Asia Ferrell, other media investment companies keen to find investors in Asia include Singapore's Causeway Media Productions Pte Ltd, and from Los Angeles Lynmar Entertainment LLC and Media Capital Technologies.

Key Investor Questions

Lastly, here are some typical FAQs that professional investors exploring the feasibility of investing in media may have.

What are the expected returns and cashflow timings?

Whilst every media project is unique and the purpose of this series of articles is to provide general information to professional investors only, just by way of general indication our financial models at New Asia Ferrell show typical returns for movie projects as 50%~100% (meaning an investment of $100 would return including the original $100 investment as well as an additional $50~$100) and for scripted TV series as 25%~50% within 2 to 3 years.

Examples of investable Asia projects include:

What are typical benchmarks and comparables?

In terms of publicly available data, box office numbers (for example from BoxOfficeMojo) and budget number (e.g. from IMDBPro or online news articles) are the best means to see how other movies in a similar genre, or similar budget, or with similar cast etc have fared. (Incidentally, both BoxOfficeMoji and IMDB/IMDBPro are now owned by Amazon.)

Before the rise of streaming, box office performance was also a strong indication of how successful a movie would be on DVD/Bluray too; therefore, it is almost certain that streaming platforms consider a movie's box office performance as an appropriate measure to gauge the expected level of interest from streaming subscribers also.

For benchmarks and comparables for streaming TV shows, obtaining data for viewer numbers for a particular show is much harder, as explained in this excellent post by entertainment journalist Stephen Silver. For example, only Nielsen seems to provide viewer numbers for TV shows... but even there this is for some streaming platforms only (such as Amazon, Disney and Netflix) , but not for other important ones (like Apple, HBO Max (Warner Bros. Discovery), Paramount, or Peacock (NBCUniversal)).

How should we do meaningful valuations?

Armed with the movie budget and box office returns for similar (in terms of genre, or particular leading actors involved, etc.) movie projects and/or (if you can get it) viewer numbers for similar TV shows, then the best way to do a valuation is to construct and calibrate a linear regression model and use that.

An alternative approach is to use the box office returns versus budgets of similar projects to deduce a likely range of expected returns (best case, expected case, worst case) along with the likely probability of each to give you a rough probability distribution for the range and likelihood of returns you can expect.

What criteria should we look at to pick promising movie and TV projects?

To maximize the chance of picking projects which will prove successful, he key things to keep in mind are (i) who are the key producers/director/showrunners and how is their track record in terms of success and keeping within budget, and (ii) is there current market demand for this type of project (in terms of the genre, cast, what similar has been popular recently)? Ultimately, do you have faith and trust in the people involved to successfully sell and deliver a quality movie or show?

Are there any additional perks unique to investing in media?

Investors in media projects typically are able to receive invitations to premiere/red carpet events, to be able to visit sets, and even take non-speaking single-scene extra roles if they have such a burning desire.

Final Words

In summary:

- Media is a viable alternative investment asset class to diversify a portfolio and improve risk-adjusted returns and can come with a wide variety of risk-reward profiles and investment ticket sizes.

- Demand for global content continues to have double-digit growth year-on-year (with the Financial Times reporting 35-40% for Disney+, 25% for Netflix, etc.), with a significant increase (e.g., double for Netflix) in content spend in Asia.

- Theatrical markets are also beginning their recovery as the pandemic eases.

- The biggest challenge for investors in Asia is securing consistent investment opportunities of suitable investment size into quality media projects from a team of experienced professionals that they can trust.

Here's the podcast:

About the Author:

Adam Garrett is Chief Investment Officer at Hong Kong based New Asia Ferrell Asset Management Limited, an Asia-focused financial services group which has been serving family offices and private individuals globally since 2016 with innovative investment solutions including in the alternatives media investment space. Previously, Adam was Chief Investment Officer at PINS Asset Management (Asia) Ltd for 5 years, specializing in alternative investments in real estate, quant trading, food & beverage, and TMT private equity. In addition to his buyside experience, Adam also has a financial sell side background in volatility trading at Mizuho Securities and quant trading & equity derivative structuring at Lehman Brothers in both Hong Kong and Tokyo. Through his film production company Agog Film Productions Ltd which he established in 2007, he is also an award-winning independent filmmaker, winning the 2009 Gold Kahuna Award for Excellence in Filmmaking for his directorial debut that starred Hong Kong's Gordon Liu, and announcing in early 2022 Agog Films' involvement in a global genre slate of projects to be shot in the Philippines.