By Shawn Gibson, CIO & Portfolio Manager, Liquid Strategies LLC/OVLs Overlay Shares.

Investors consistently seek out investment strategies that can help to improve the yield of their portfolios. One such strategy that has been popular for decades and is capturing the imagination of investors today is covered call writing. Covered call writing is touted as a conservative way to generate additional income from an equity portfolio while still allowing investors to participate in market appreciation and dampen downside risk and volatility. The purpose of this paper is to help investors make more informed decisions by better understanding the limitations and risks of covered call writing.

COVERED CALL WRITING EXPLAINED

When an investor writes a covered call, they agree to put a cap on the price of their stock at a specific price (“strike price”) up to a specific date in the future (“expiration date”). In return for capping the price of the stock, the investor receives an up-front premium (“call premium”). If the stock is below the strike price on the expiration date, the call option expires worthless, allowing the investor to keep the call premium (minus any costs of closing it, if applicable). If the stock is above the strike price at any time at or before the expiration date, the investor may be forced to sell the stock at the strike price, regardless of how high the stock price actually is.

Many investors focus on the call premium as a source of portfolio “income” while still participating in a limited amount of appreciation of the stock. As long as the stock stays below the strike price and the call expires worthless, the strategy can generate positive portfolio income, making it ideal for flat or down markets. However, trying to time when stocks and markets will be flat or down is extremely difficult, particularly given the long-term upward bias of the equity markets. As such, there is a hidden cost of covered call writing, which is the potentially significant opportunity cost of having the stock go above the strike price causing lost portfolio appreciation.

THE HIDDEN COST OF COVERED CALL WRITING

Marketing material for covered call writing strategies mention that investors limit equity upside potential as part of the mechanics of the strategy but understate the risk to investors for that critical part of the strategy. The focus is usually on the cash flow potential of the strategy without consideration to the economics involved with closing covered call positions. Here is a very simple case study for covered call writing in order to better see the mechanics and benefits and costs of covered call writing.

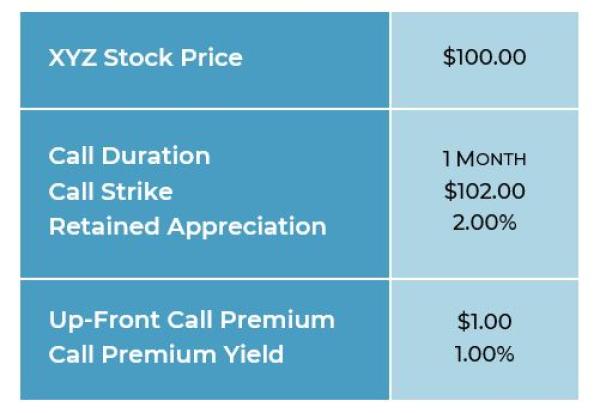

An investor owns XYZ stock and is interested in generating income for their portfolio and will do so by selling covered calls against the XYZ stock, thus hoping to generate positive cash flow to the account while allowing for upside potential in XYZ. Furthermore, the investor hopes to use cash flow received from selling the call as a buffer to offset downside losses in XYZ. As such the investor enters into the following trade:

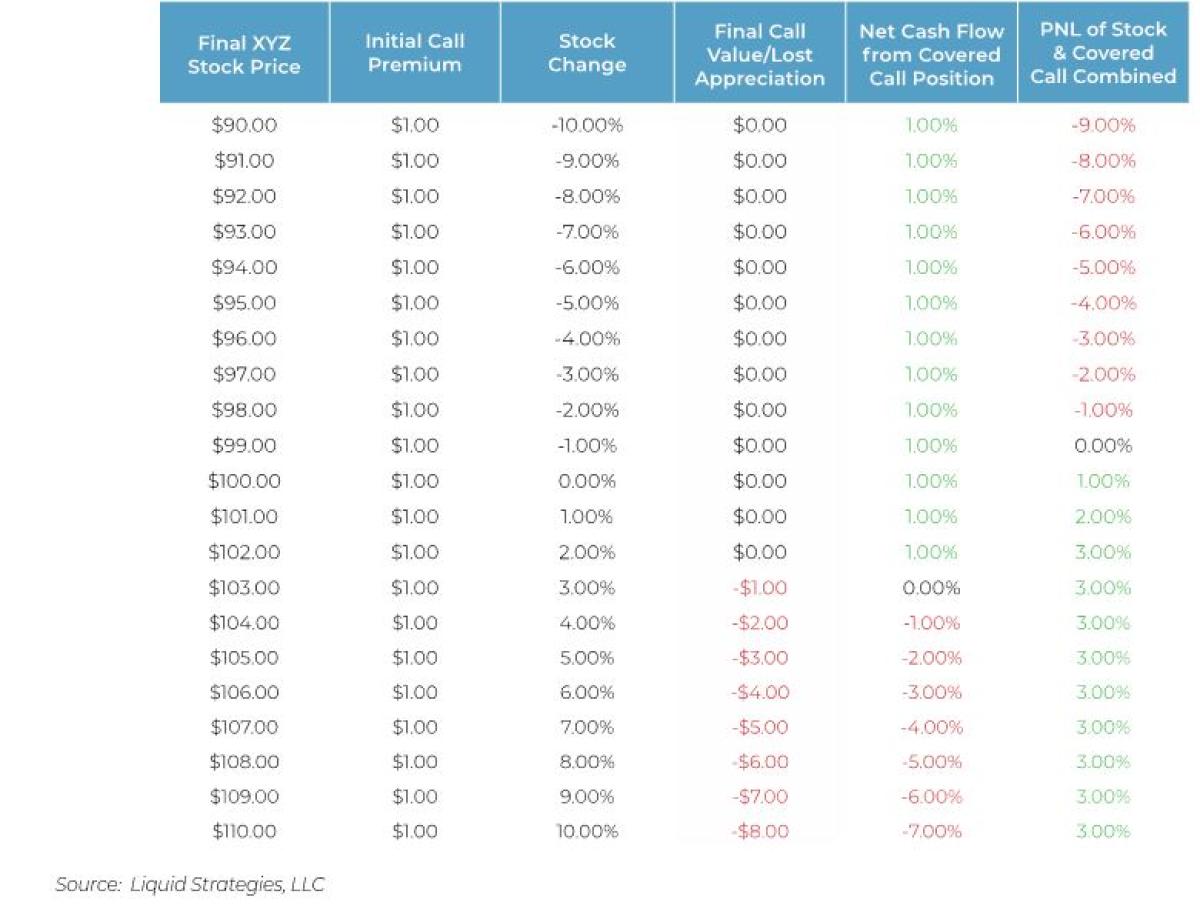

While the yield on this trade looks very attractive (1% for just 1 month), investors must factor in cost of closing the covered call at expiration in one month. If XYZ is higher than $102 at expiration, the investor will need to repay cash to close the position or allow the position to be sold at $102 regardless of how high the stock goes. The table below shows the final net profit or loss for the covered call at various final levels of XYZ stock.

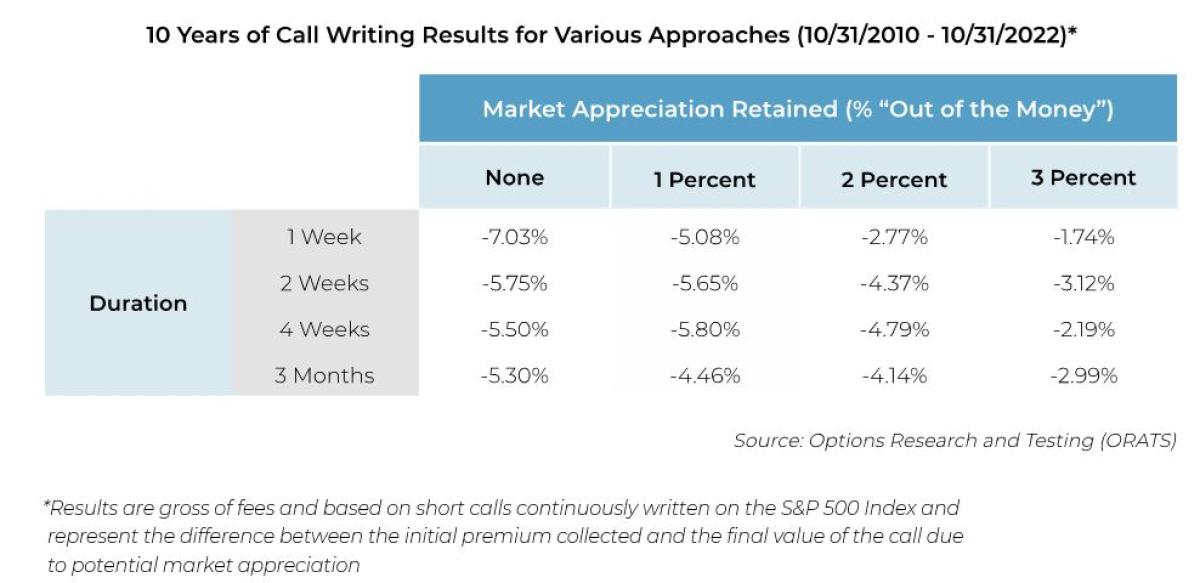

While some individual covered call positions may have positive outcomes, a series of negative impacts from covered call writing can be very detrimental to a long-term investment portfolio. While it may be tempting to add covered call writing to a diversified portfolio, over the long term, investors have not been adequately compensated for limiting appreciation potential. As the data below shows, covered call writing on the S&P 500 Index has had a dramatic negative impact on equity portfolios over the past 10 years. Over the past 10 years, these 16 covered call writing programs have all delivered significant negative annualized returns ranging from -1.74% to -7.03%, gross of fees (the negative impact would have been greater when factoring in fees paid for managing the strategy). Reducing equity returns by these amounts could dramatically hinder an investor from reaching their investment goals.

OTHER APPROACHES TO GENERATE CASH FLOW

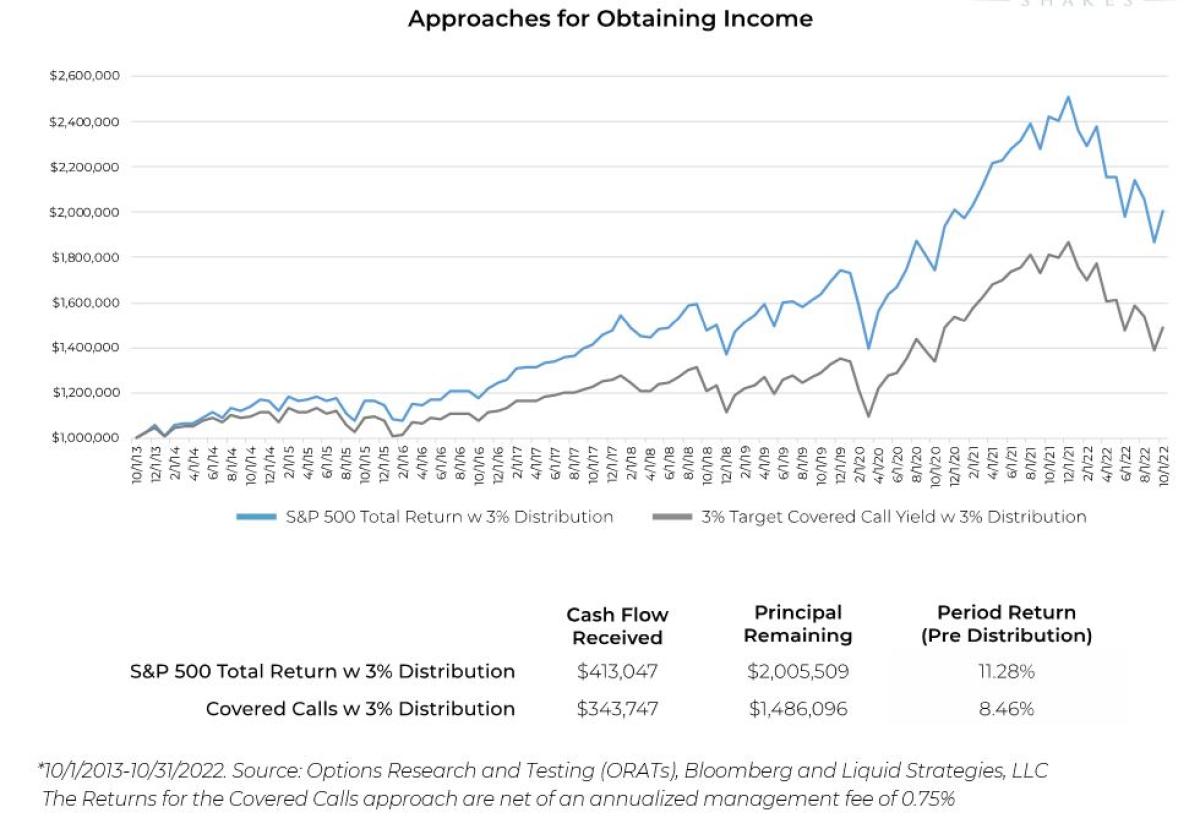

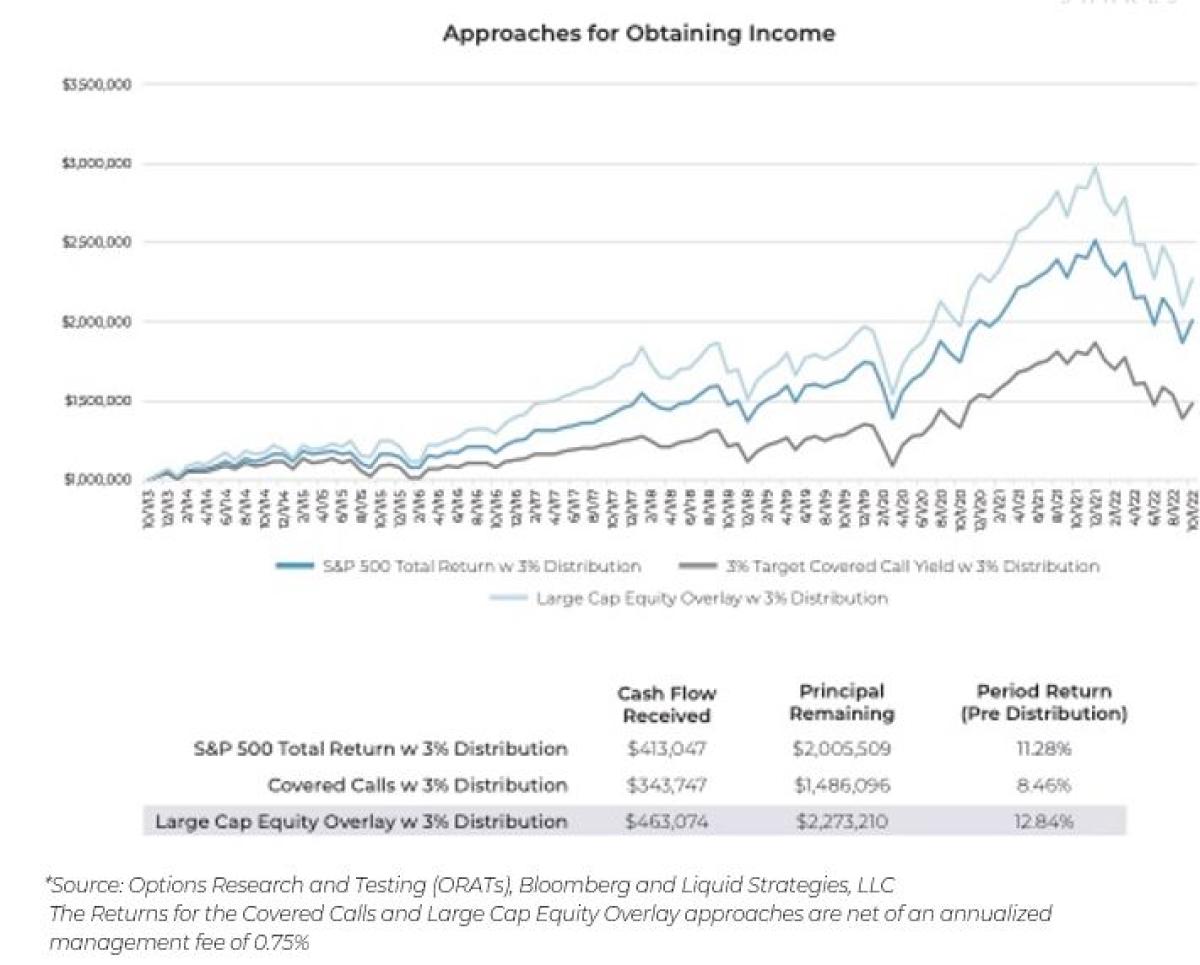

Over the long term, for investors that need cash, simply selling a portion of the principal of the equity would have created a much better investment outcome than covered call writing. Over the past 9 years, an investor seeking a strategy to generate 3% in income for their S&P 500 Index holdings could have a) simply held the S&P 500 Index and withdrew 0.75% a quarter for each year; or b) utilize a covered call writing strategy that targets 3% in annualized cash flow from each option sold, and then withdrawing 0.75% a quarter for each year. As shown below, due to the negative impact of covered call writing, an investor utilizing that approach would have finished with significantly lower final principal value as well as lower cash flow during the period (due to a limited principal base from the lost appreciation potential).

The option writing program utilized by Liquid Strategies is designed to generate positive cash over the long term, even in a rising equity market. Utilizing the same 9-year period as before, applying our income “Overlay” to the S&P 500 Index and taking a 3% annual distribution would have created a much better investor outcome.

COVERED CALL WRITING AS A RISK MITIGATOR

The call premium received by investors can help to somewhat reduce downside risk and volatility. However, given the way that most call writing strategies are implemented, the amount of premiums collected may not provide any significant downside risk reduction. A larger source of potential volatility reduction comes from the risk of lost appreciation, as previously detailed. In a rising market, covered calls may actually reduce upside portfolio volatility, which is the type of volatility that investors benefit from. As such, when evaluating covered call strategies that show lower volatility statistics than the broader market, investors should be mindful of where that volatility reduction may be coming from.

CONCLUSION

While there are certain situations where covered call writing could add value within a portfolio, investors need to consider the opportunity cost of the strategy and the impact that it can have over the long term. For investors seeking incremental portfolio income, there may be other solutions that may help them better achieve their desired outcome.

About the Author:

Shawn Gibson co-Founded Liquid Strategies in 2013 and serves as CIO and Portfolio Manager.

Shawn brings more than 25 years of investment experience primarily in the area of options trading and options portfolio management. Shawn started trading options in 1997 with the Timber Hill Group, where he was an options market maker on the floor of the Pacific Exchange and later promoted to join a small team in Greenwich, CT responsible for overseeing the firm’s multi-billion-dollar options trading portfolio. He subsequently served as Head of Options Strategy and Director of Alternative Investments at BB&T, where he worked with advisors and their clients to develop options-based hedging and yield enhancing strategies. Shawn is an active member of his community and was voted as one of the Top 40 leaders under 40 while living in Richmond after being nominated by his peers due to his professional accomplishments and community involvement. Shawn earned his B.S. in Commerce from the University of Virginia.