By Nicolas Rabener, CAIA, CEO & Founder of Finomial.

SUMMARY

- Hedging and diversifying strategies have different objectives

- Downside betas can be used to differentiate these

- Alternative strategies have overtaken bonds as the most diversifying strategies

INTRODUCTION

In investing, some terms are used interchangeably, despite these having quite different technical interpretations. For example, most investors put stocks with strong sales growth, strong performance, or expensive valuations in the same “growth stock” bucket, but these companies often have significantly different characteristics, e.g. cheap stocks outperformed and acquired momentum features in the first quarter of 2023, but these companies do not exhibit strong sales growth.

The same applies to diversification and hedging strategies, which are often considered the same but are not. Hedging refers to protecting a portfolio against a stock market crash, while diversification is about finding strategies that offer uncorrelated returns to equities.

In this article, we will contrast both strategies.

CREATING A HEDGING / DIVERSIFICATION STRATEGY

We select mutual funds and ETFs with the most promising diversification potential, which we define as the product of the downside beta to the S&P 500 and the total return over the last five years. Funds with positive downside betas are excluded. Stated differently, we are looking for funds that generate positive returns when stocks decline, but that have the ability to make money (read Downside Betas vs Downside Correlations).

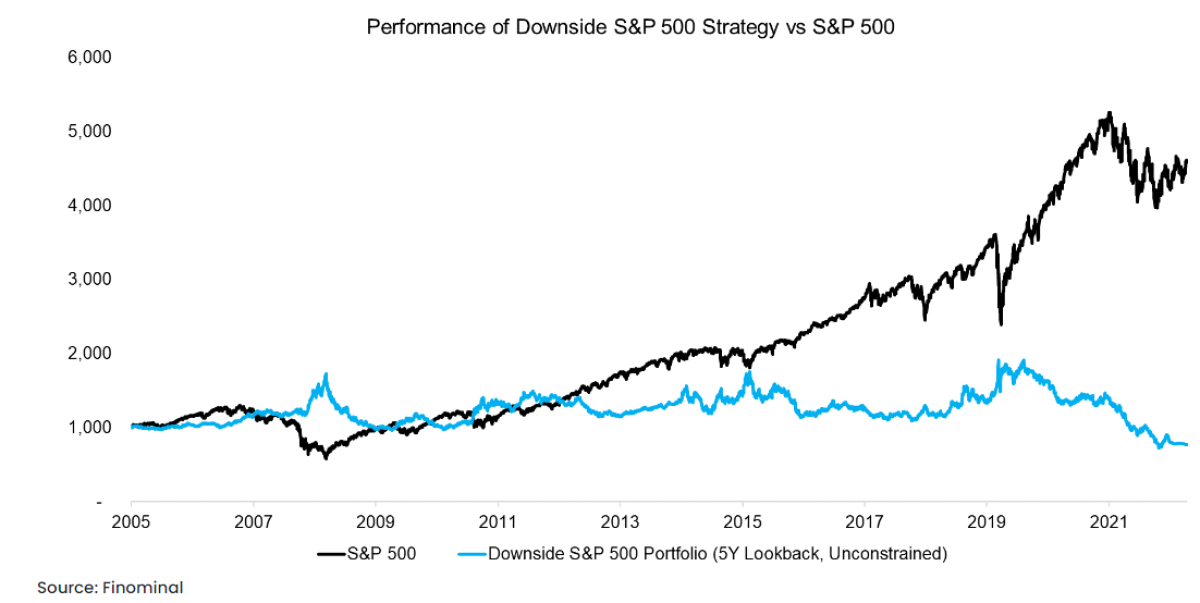

We create a portfolio of such funds by selecting the top 10 funds with the most negative scores (“Downside S&P 500 Portfolio”), which is held for a year and then rebalanced. We observe that the performance of the Downside S&P 500 Portfolio was negative over the period from 2005 to 2023, although most of the negative performance can be attributed to the last two years. More interesting is that the strategy did generate attractive diversification benefits when the stock market crashed or declined, e.g. during the GFC in 2008 or the COVID-19 crisis in 2020.

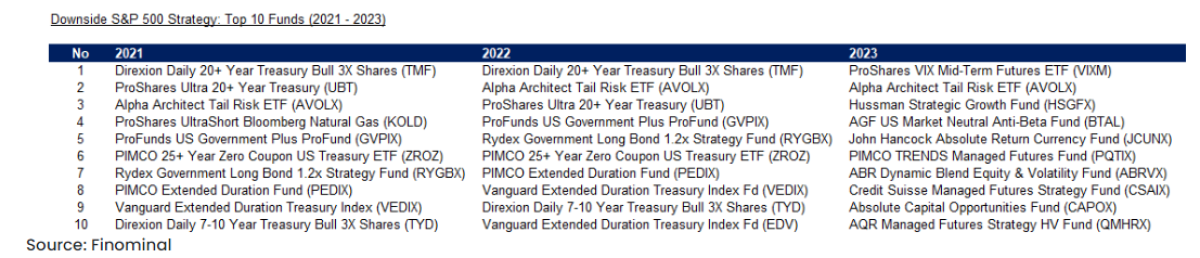

Reviewing the funds selected at the beginning of the last three years shows that in 2020 and 2021 these were primarily leveraged long-duration bond funds, which then changed in 2023 as not a single fixed-income product was chosen. The fund selection became much more diverse and included VIX, tail risk, and managed futures strategies (read Finding Funds with Diversification Potential).

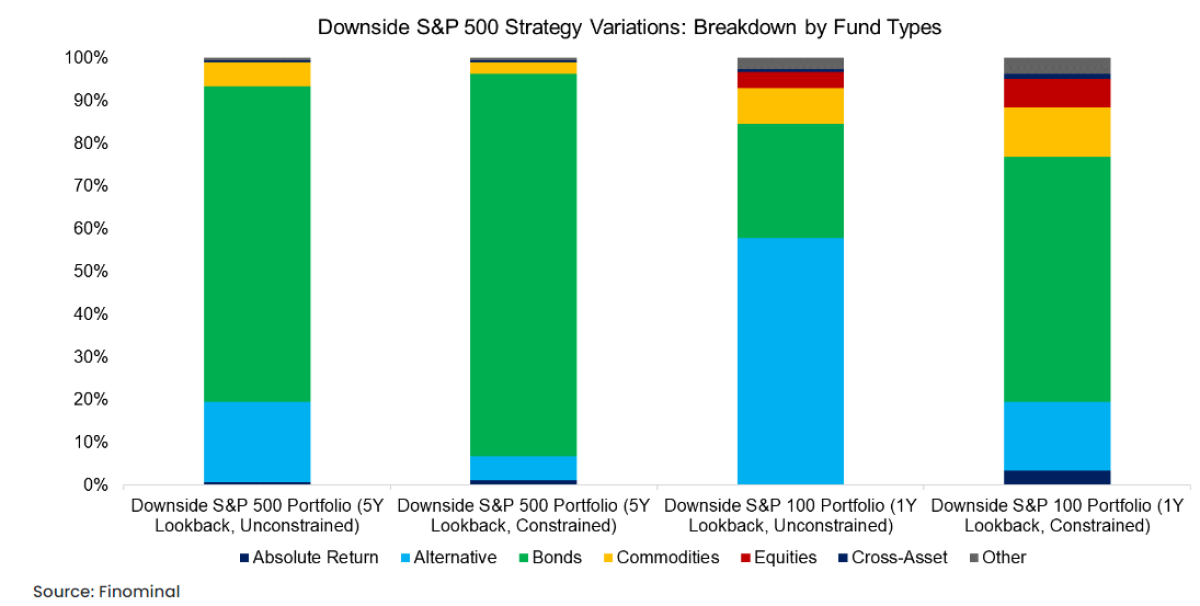

BREAKDOWN BY FUND TYPES

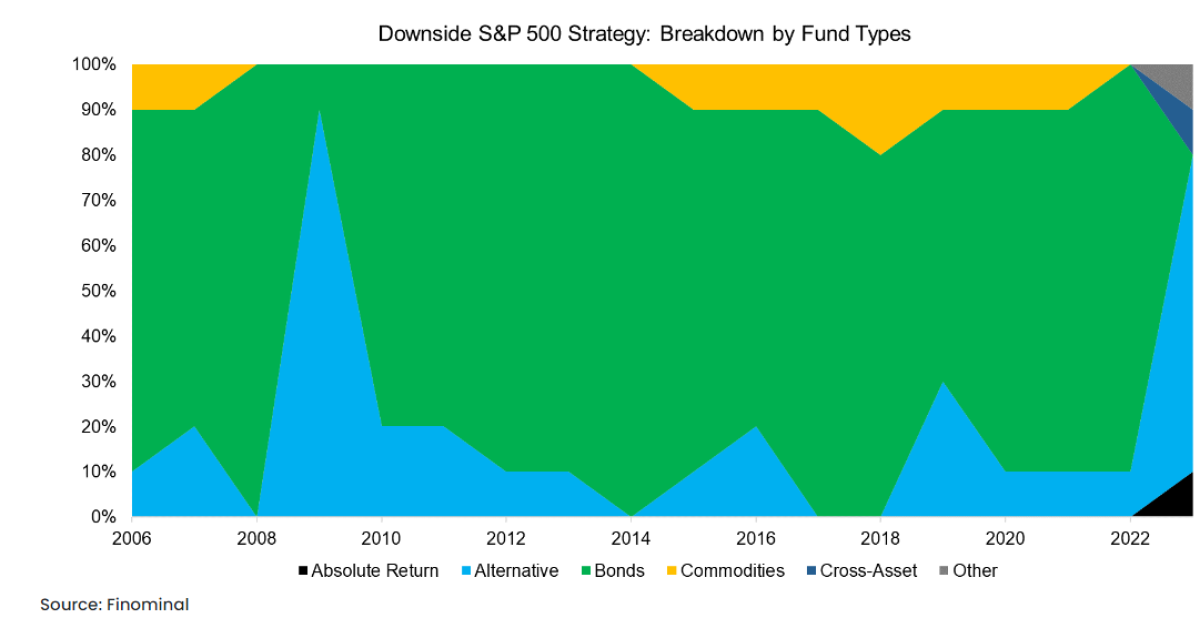

Reviewing the fund selection over the entire 15-year look-back shows that the portfolio was primarily comprised of bond funds, except during 2008 and 2023. Naturally, this makes sense as bonds were negatively correlated to equities throughout most of that period, and generated positive returns given the bull market in bonds that has been going on since the 1980s. They were the perfect diversifiers.

However, as we pointed out many times in previous research articles, bonds become less attractive when their yields are close to zero as their expected returns also approximate zero, and they can lose substantially in value when yields rise, which is exactly what happened over the last two years given rising inflation rates and corresponding central bank policies (read How Much Can You Lose with Bonds?).

S&P 500 DOWNSIDE STRATEGY VARIATIONS

We used a five-year lookback when selecting diversifying strategies, but this can be challenged as not being particularly dynamic and responsive to rapidly changing capital markets. We simulate reducing the lookback to one year, and also implement a constraint that we only select funds with a downside beta of larger than -0.5 as we want to avoid strategies that are hedging rather than diversifying.

We observe that decreasing the lookback from five to one year reduces the number of bond funds in the portfolios significantly, however, primarily when not constraining the downside beta.

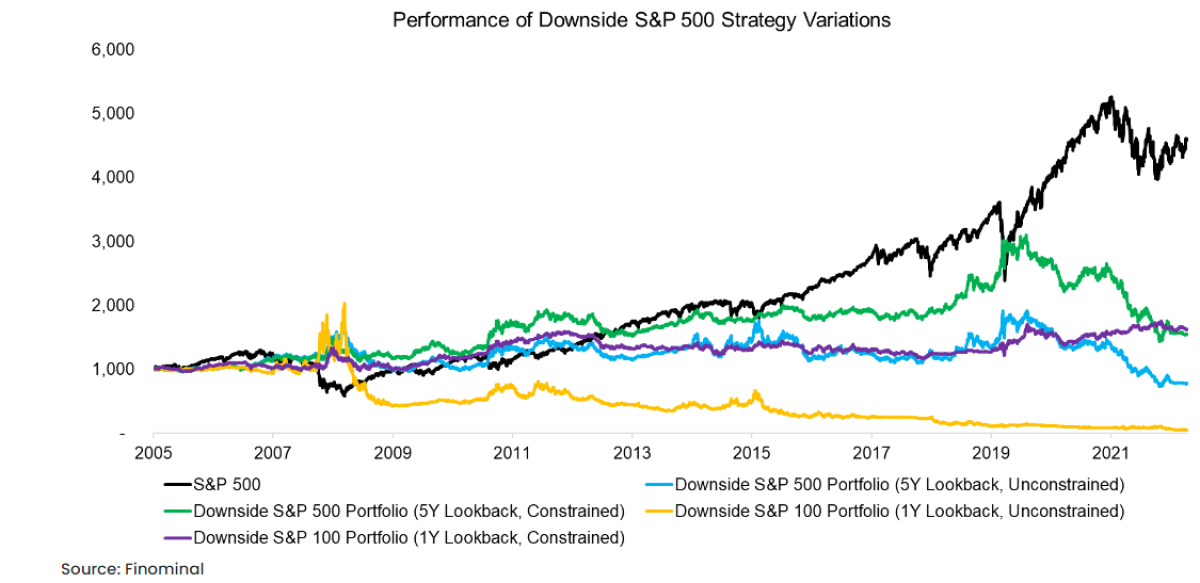

We backtest the performance of these Downside S&P 500 Portfolio variations and observe that the two strategies with a five-year lookback exhibited identical trends in performance. Both offered diversification benefits during stock market declines but lost substantially when bonds fell as their portfolios adjusted slowly to the regime change.

The unconstrained strategy with a one-year lookback performed like a classic tail risk hedge, i.e. strong returns during stock market crashes, but consistent losses otherwise, which makes this strategy difficult to hold for investors. Constraining the downside beta reduced the bleed as it removed products like VIX ETFs that are essentially short positions on the stock market.

MEASURING DIVERSIFICATION BENEFITS

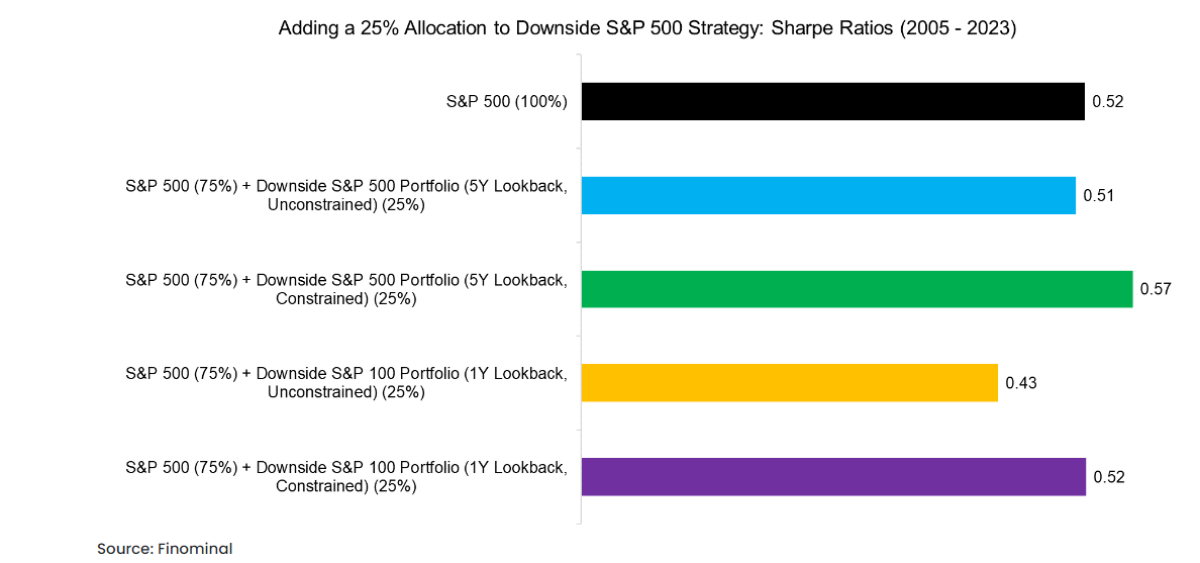

Finally, we evaluate the diversification benefits of these four portfolios by simulating adding a 25% allocation of either to a portfolio comprised exclusively of the S&P 500.

We observe that the Sharpe ratios of the combination portfolios did not increase significantly to the S&P 500 on a standalone basis. The maximum drawdown reduces from -55% to a range between -35% to -42%, but the return decreased proportionally, therefore only marginally improving the risk-adjusted returns.

FURTHER THOUGHTS

Given that adding these portfolios did not generate significant diversification benefits, do we conclude that using downside betas for identifying diversifying strategies is a poor methodology?

Not necessarily, as it was almost impossible to detect the regime shift in bonds with such a systematic approach. Essentially, constructing a diversified portfolio requires thoughtful portfolio construction that should include various types of diversifying strategies (try Finominal’s Diversification Booster), rather than just allocating to bonds.

RELATED RESEARCH

Finding Funds with Diversification Potential

Downside Betas vs Downside Correlations

Upside versus Downside Stocks

Myth Busting: Alts’ Uncorrelated Returns Diversify Portfolios

Are Alternative ETFs Good Diversifiers?

Market Neutral Funds: Powered by Beta?

Merger Arbitrage: Arbitraged Away?

Hedge Fund ETFs

A Horse Race of Liquid Alternatives

Liquid Alternatives: Alternative Enough?

Original Article from Finomial

About the Author:

Nicolas Rabener is the founder & CEO of Finomial (formerly FactorResearch) and previously founded Jackdaw Capital, an award-winning quantitative hedge fund. Before that Nicolas worked at GIC and Citigroup. Nicolas holds an MSc from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon).