By Randy Cohen, PhD., Cofounder PEO Partners - a leader in the emerging "liquid private equity" alternatives space. PEO developed a proprietary investment model to deliver performance comparable to average LBO performance net of fees in the public markets.

It has always been the case that a handful of very large companies make up a significant percentage of the stock market. This is an example of a widespread phenomenon known as a power-law; we see power-laws occurring throughout both the natural and social sciences. For example, in almost every country we see the following pattern-the number of cities with populations greater than a given size scales with the size cutoff. In country after country, there are approximately five times more cities with populations over 200,000 than there are with populations over 1 million, and the number over 40,000 is five times greater still.

And it's not just cities. Similar results can be seen across data sets of many types including word frequencies and neural activity. Economics and finance are no exception, as seen in a series of papers by the decorated economist Xavier Gabaix. He shows that fluctuations in stock prices, trading volume, and the number of trades all follow a power-law distribution.

It should be no surprise, then, to see that the U.S. stock market has a small number of firms whose total market capitalization is enormous compared to its peers. The seven largest companies today comprise over 25% of the capitalization of all 3,000+ public corporations combined, making the average of this group more than 100 times larger than the typical listed one. As mentioned, a few giants have always captured an outsize share; for example, in 2013 the top 10 companies made up a little over 19% of the market, quite a bit less concentrated than now but at least in the general ballpark.

Today feels different and for good reason. The higher-than-normal concentration of individual stocks appears, in historical context, to be a cyclical high of a type not dissimilar to what occurred in 1999 or 2008. But the concentration by type of company appears entirely unprecedented. Let's compare a list of the top 10 firms of 2013 to a more recent list:

Some of today's tech giants are present in the 2013 list; after all, 2013 wasn't that long ago! Google, Microsoft, and Apple are among the leaders. But also represented are energy (Exxon Mobil and Chevron), communication (AT&T) as well as other sectors like industrials, health care, and consumer staples. And now? Now the power-law powers-that-be are all tech, almost all software-driven, all volatile, and thus tend to respond to similar market stimuli. A few years ago, people started to speak of FANG stocks, but this was problematic; who among us could remember whether the A stood for Apple or Amazon? So, they added a second A to capture both, and included an M for Microsoft, which briefly had the largest market cap of any company in the world. This gave us the ridiculous FANGAM stocks - couldn't they at least have gone with the more-memorable "FANMAG"? Additional confusion came as Google renamed itself Alphabet and began trading two ultra-valuable classes of stock. Plus, Facebook recently became Meta and NIVIDA became a titan. Unfortunately, if we use all these names, we'll have the MAMANANA stocks, which doesn't even qualify as a mnemonic!

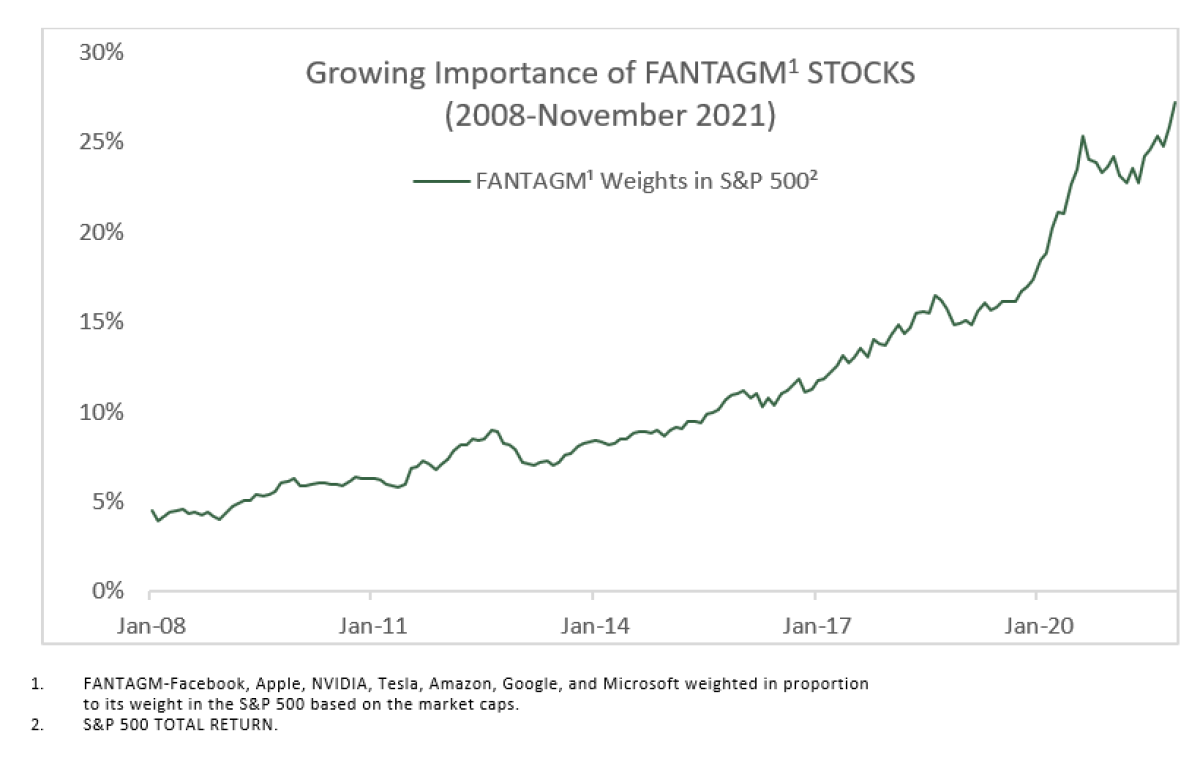

Boiling it down and sticking with names like Google and Facebook that are still in common usage despite the rebranding efforts, there are 7 companies, the seven largest by market cap in America, and as mentioned they are all enormous, all high-tech, all with a tendency to move together and more dramatically in both directions than the market. As a result, their impact goes well beyond the already huge 25+% of the market's capitalization they make up. We can even give them a cool name; let's pronounce it "phantom" though the spelling is FANTAGM: Facebook, Apple, NVIDIA, Tesla, Amazon, Google (x2), Microsoft.

Obviously, these companies are not phantoms in the sense of being spectral or nonexistent. Indeed, they affect us daily in ways far more intimate than old-school giants like TRW or Honeywell ever did. And yet the name feels fitting, as their businesses are centered in the online world that author Neal Stephenson dubbed the Metaverse. Moreover, it seems their valuations often move day-to-day based on factors outside the concrete, numbers-driven elements that govern the corporeal world of what the techies call "meatspace." Their price movements can feel, if you will, phantasmagorical.

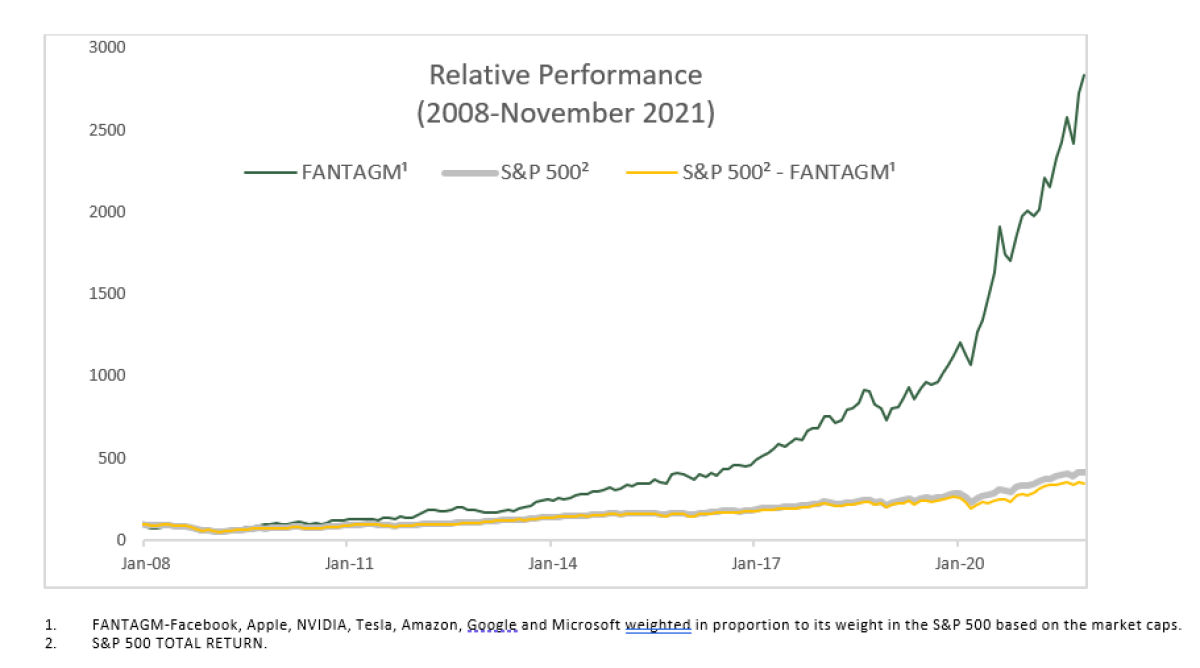

Why does this matter? Over time the concentration is not likely to be a big deal-the phantoms will have their good and bad quarters, but in the long run, will probably perform close enough to average that their inclusion won't skew decade-long returns by much. Even over the period from 2008-November 2021, which saw their spectacular rise from 5% of the market to the current five-times-larger level, they add only a little more than 1% to the average return of the S&P 500. Specifically, the S&P 500 had an average annualized return of 10.7%. The FANTAGM stocks had an average annualized return of 27.1%. This means that without those 7 FANTAGM stocks, the S&P 500 would have only had an average annualized return of 9.4%.

The extreme concentration of a quarter of the market in a set of related, software-driven companies means that any strategy that doesn't have those firms as part of its mandate will have periods where its performance relative to the value-weight market index will be determined primarily by whether the FANTAGM stocks were doing especially well or poorly. For such non-FANTAGM strategies, using the S&P 500 as a benchmark will be highly misleading at times-which are sure to be frequent-when the FANTAGMs run hot or cold.

The phantoms have performed remarkably well and, who knows, perhaps they will continue to do so; we are not here to criticize them as companies or as investments! Rather, our point is merely to say that, just as venture capital was once part of the private equity asset class but is now perceived as its own, independent class, the FANTAGM stocks can be seen as an asset class of their own, separate from the other 3,000 stocks that make up the asset class we will continue to call "U.S. Equity." Each investor needs to decide how much to invest in these high-fliers, and then choose where to invest the rest of one's capital, using appropriate benchmarks to judge the non-FANTAGM parts of their portfolio.

About the Author:

Randy Cohen is the MBA Class of 1975 Senior Lecturer of Entrepreneurial Management at Harvard Business School. Cohen teaches finance and entrepreneurship at HBS and has previously held positions as Associate Professor at HBS and Visiting Associate Professor at MIT Sloan. He currently teaches Field X/Y at HBS, a course for students who are starting businesses while obtaining their MBA. Last year he advised around 90 startup businesses in the course. He co-developed the Alternative Investments course for HBS Online which will go live in the first quarter of 2020. Mr. Cohen’s main research interests are the identification and selection of money managers who are most likely to outperform, asset allocation, risk management, and anything else related to building great investment portfolios. Cohen has studied the differential reactions of institutions and individuals to news about firms and the economy, as well as the effect of institutional trading on stock prices. Other research areas include activist investing, municipal securities, cryptocurrency, and longevity insurance. In addition to his academic work, Cohen has helped to start and grow a number of businesses, mostly, but not exclusively, in the area of investment management. He also has served as a consultant to many established money management firms. Cohen holds an AB in mathematics from Harvard College and a PhD in finance and Economics from the University of Chicago.