By Randy Cohen, PhD., Cofounder PEO Partners, a leader in the emerging "liquid private equity" alternatives space.

Introduction

We believe that perhaps no innovation in the history of investing has created more wealth than the “60/40 Portfolio.” This portfolio invests its total value in two distinct market segments, with 60% of the value invested in stocks and the remaining 40% in bonds. Motivation for the original 60/40 portfolio came from a group of researchers including Harry Markowitz and William Sharpe, both of whom received Nobel Prizes for their work, when they created Modern Portfolio Theory (“MPT”). One implication of MPT was that the optimal portfolio for investors was the total market universe. Since the total market had about $1.50 stocks for every $1.00 of bonds, MPT implied that a portfolio that focused on these two primary asset classes would hold 60% in stocks and 40% in bonds.

60/40 – The Past

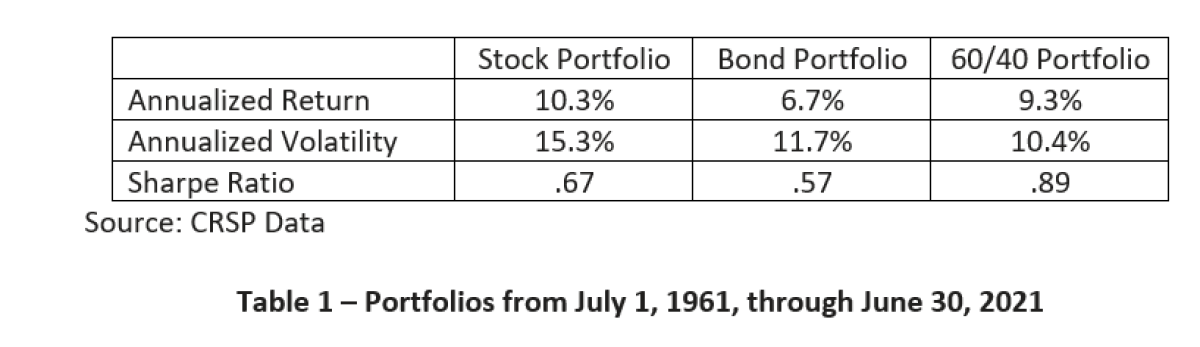

In the six decades since it was developed (the period 1961 – 2021), the performance of the 60/40 portfolio has been spectacular. The average annual return over that time has been a little over 9% (See Table 1). A return of nine percent annually over an 80-year lifespan delivers an investor approximately 1,000 times their original investment.

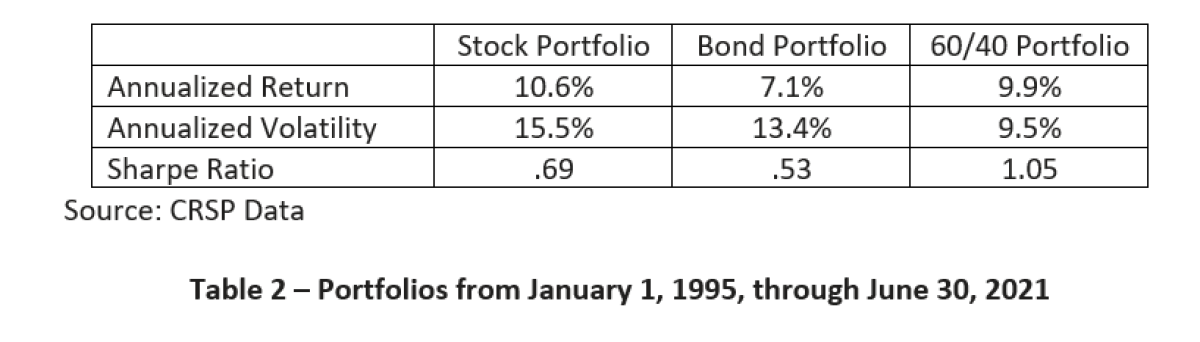

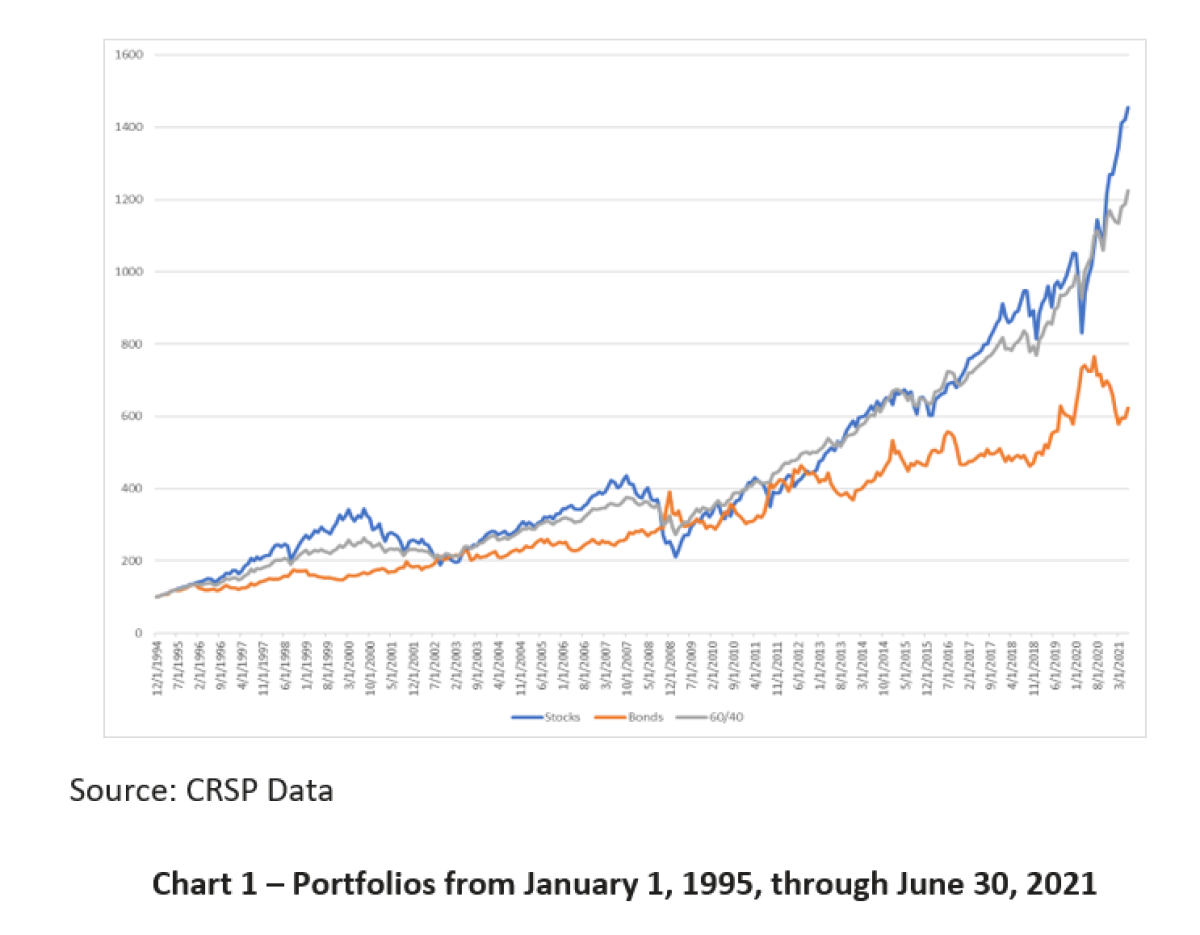

In fact, since 1995, the 60/40 portfolio has done even better with an average annual return of almost 10% (See Table 2 and Chart 1).

In addition to an attractive return, the 60/40 portfolio has delivered relatively low risk. Stocks have crashed numerous times since the creation of the 60/40 strategy. Every time stocks fell spectacularly, bonds provided ballast, so that overall, the losses of a 60/40 portfolio were mitigated. Since 1975, the 60/40 portfolio only had a single year (2008) in which it had a double-digit loss, at -12.2%. Even in 2008, 60/40 returned only about half the losses of the stock market portfolio.

Despite the extraordinary performance of the stock market over the “American Century,” investors received a higher return per unit of risk in the 60/40 portfolio as compared to a 100% stock portfolio. Investors holding a 60/40 portfolio received tremendous returns with modest risk. Performance has been so strong that the 60/40 Sharpe ratio over this period has been higher than the Sharpe ratio of stocks alone. In fact, over the period of 1995-2021, it has delivered a Sharpe ratio of 1.09 which is remarkable, and much better than stocks at 0.69 and bonds at 0.52.

The 60/40 portfolio has performed well with low risk, and it has done so for many people and a lot of investment capital. 60/40 became the baseline investment

strategy for pension funds, endowment funds, and high-net-worth individuals as well as retail investors. Wealth advising firms built the portfolios of many millions of customers around this simple rule nothing succeeds like success. The 60/40 portfolio was a success on both risk and return measures and on widespread adoption. The combination of simplicity and success made it a near-universal baseline strategy.

60/40 – The Future

Will the next generation receive rewards for investing in a 60/40 portfolio comparable to the past two generations? Unfortunately, this seems extremely unlikely. Of course, we cannot predict the future, but we do have some tools that allow us to create a forecast.

Predicting Bonds’ Returns

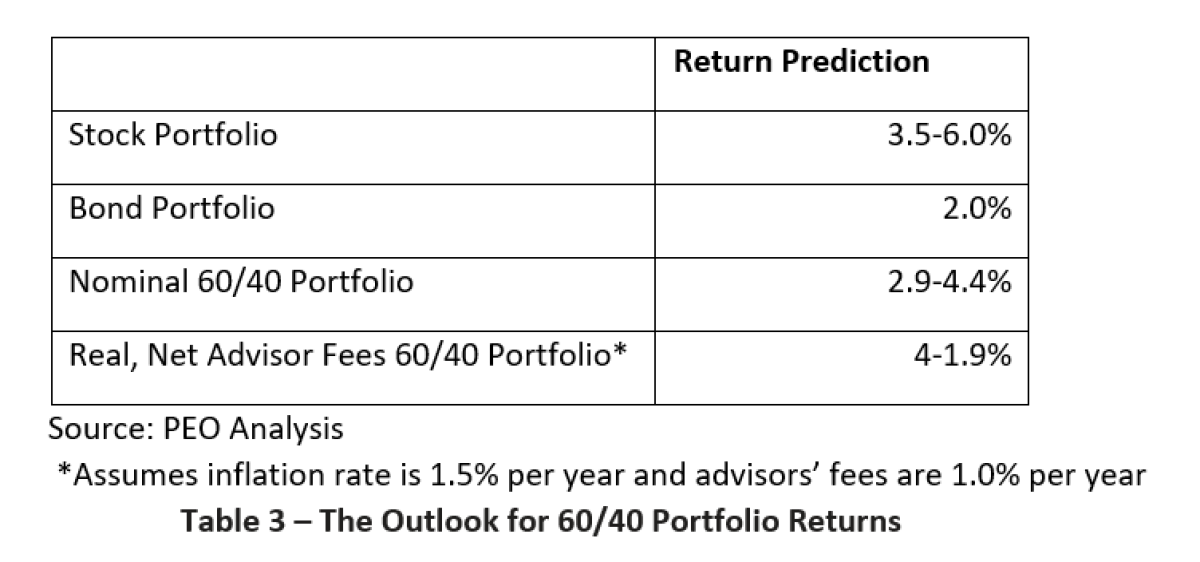

The prediction range for the stocks’ portion of the 60/40 portfolio is only 1.5% wide even using the biggest range [60% * 6 - 3.5%].

Predicting 60/40 Portfolio Returns

We can now combine our expected returns for bonds (2%) and stocks (3.5%-6%) to come up with an estimate for our 60/40 portfolio. Let’s say we think the stocks return is 5%, which gives 3.8% for the expected return for the 60/40 portfolio [5% (60%) + 2% (40%)]. We can also look at the range of expected returns given our range of predicted stock returns. At the low end, we predict a 2.9% annual return for the 60/40 portfolio and at the high end, we predict 4.4% annual return for the 60/40 portfolio. Any way you look at it, it is a very modest number compared to the historical average. It means more like making 10 times your investment over a lifetime, not 1,000 times.

Expected returns on a 60/40 portfolio are going to feel disappointing relative to the past. And, while we have been doing calculations in nominal terms, adjusting for inflation does not make the issue go away. Historically, inflation has averaged 3% per year, taking a significant bite out of the 9% historical return and leaving only 6% for the investor. Future inflation expectations are lower than what we have seen in the past, but even if we expect inflation to fall to 1.5% a year, the problem is still severe. This leaves our real expected annual return on the 60/40 portfolio to be 1.4-2.9%, nowhere near the 6% return we had.

The concern is even more severe if we start looking at returns on an after-fee basis. Registered investment advisors who help the client manage their portfolios take fees of about 1% per annum. If we now shave a percent off the expected returns, we are down to 0.4-1.9% on a real, post-fee basis. One percent annual returns are not going to create a comfortable retirement for investors. See Table 3.

Predicting the Risk

We believe that we have made a convincing argument that the returns of the 60/40 portfolio will likely disappoint in the coming years, but will 60/40 continue to offer the impressively moderate risk that it has in the past? Unfortunately, that also appears unlikely. The source of risk has changed. To put it simply, if your stocks crash, history shows that you bond portfolio will protect you. But, if your bonds crash, your stocks will absolutely not protect you!

Stocks and bonds are both long-term assets. One way to think about the risk of the stock market is to break it into three pieces. First, there is the risk that cash flows will be less than hoped, usually due to adverse economic environments. Second, people may become more risk-averse and therefore choose to discount risky cash flows at much higher rates relative to safe cash flows. Third, there is the risk that people will show a greater preference for money now rather than later. If long-term interest rates are higher than future cash flows discounted at those rates are less valuable now.

The first two of these three risks affect just stocks and have historically been the biggest drivers of returns for the market. The third affects both stocks and bonds. When stocks get bad news (or crash), people tend to want to hold more bonds and fewer stocks. This is colloquially known as the “flight to quality.” That is why stocks and bonds tend to move opposite one another, are negatively correlated, and why when stocks crash, bonds protect investors.

The current problem is that for the past several years stocks and bonds have been positively correlated instead of negatively correlated. We can interpret this as meaning that the third risk has become a more important component to investors. This is intuitive, as we can see by looking at trends in the first half of 2021. Even a cursory reading of the financial press makes it clear that investors’ number one concern is that interest rates will rise because the Fed is forced to raise rates to stave off inflation.

If the long bond goes from 2 to 3% yield, its value will fall around 30%. As we noted earlier, stocks are also likely to have a drop of 30% or greater in this scenario. Then, the 60/40 portfolio could easily fall 30%. This would far exceed any drop that has occurred in its long history.

Conclusion

Hence the conundrum of the 60/40 portfolio. If we look backward, performance is stellar: tremendous return with modest risk. It is understandable that after sixty years of great performance, any reasonable person would think it is a secure place to hold one’s wealth. However, a look ahead tells a very different story. The expected returns on the 60/40 portfolio are very modest, with long-term returns of less than 4% per year.

Yet the bed is not safe. There is enormous uncertainty in what is likely to occur. A short-term crash is not out of the question. While inflation does not explain this shift, overall interest rates do play a large role. With cash paying 0%, a 3-4% return with the 60/40 portfolio still offers a significant upside to simply putting the money in treasuries.

The internet loves an acronym. Popular discussion threads all mention “TINA” - There is No Alternative. As scary as stocks are at these prices, what is there to do? Cash pays zero! That recognition has played an important role in maintaining the popularity of stocks despite investor fears.

The adage “investors wage a battle between fear and greed” is not quite right either. The human brain tends to focus on the negative and fear is a powerful motivator. Right now, it seems that investors are torn between two types of fear – fear of crashes and fear of missing out (FOMO to the young people). They see the market climbing consistently and don’t want to lose out on that opportunity and yet they are afraid of a crash.

Wall Street has recognized this paradox and each year they innovate plenty of solutions. Some of these are legitimately attractive and some only look attractive at first glance but become less compelling when analyzed in more detail, with hidden fees, confusing vehicles, associated risks (liquidity, leverage, etc.) and other drawbacks. Finding the right alternative for a safe, secure, and attractive investment, like the 60/40 historical portfolio, is a huge challenge. Investors owe it to themselves to seek solutions that give them the kinds of high single digit returns with manageable risk levels on their portfolio that they have come to expect and not just accept the 60/40 portfolio as the only available option for the future.

About the Author:

Randy Cohen is the MBA Class of 1975 Senior Lecturer of Entrepreneurial Management at Harvard Business School. Cohen teaches finance and entrepreneurship at HBS and has previously held positions as Associate Professor at HBS and Visiting Associate Professor at MIT Sloan. He currently teaches Field X/Y at HBS, a course for students who are starting businesses while obtaining their MBA. Last year he advised around 90 startup businesses in the course. He co-developed the Alternative Investments course for HBS Online which will go live in the first quarter of 2020. Mr. Cohen’s main research interests are the identification and selection of money managers who are most likely to outperform, asset allocation, risk management, and anything else related to building great investment portfolios. Cohen has studied the differential reactions of institutions and individuals to news about firms and the economy, as well as the effect of institutional trading on stock prices. Other research areas include activist investing, municipal securities, cryptocurrency, and longevity insurance. In addition to his academic work, Cohen has helped to start and grow a number of businesses, mostly, but not exclusively, in the area of investment management. He also has served as a consultant to many established money management firms. Cohen holds an AB in mathematics from Harvard College and a PhD in finance and Economics from the University of Chicago.