By George Aliferis, CAIA, CEO of Orama a video and audio marketing agency specializing in fintech and the content creator behind InvestOrama, a content platform that explores the future of investing across alternative assets, Defi, and technology - but without the hype.

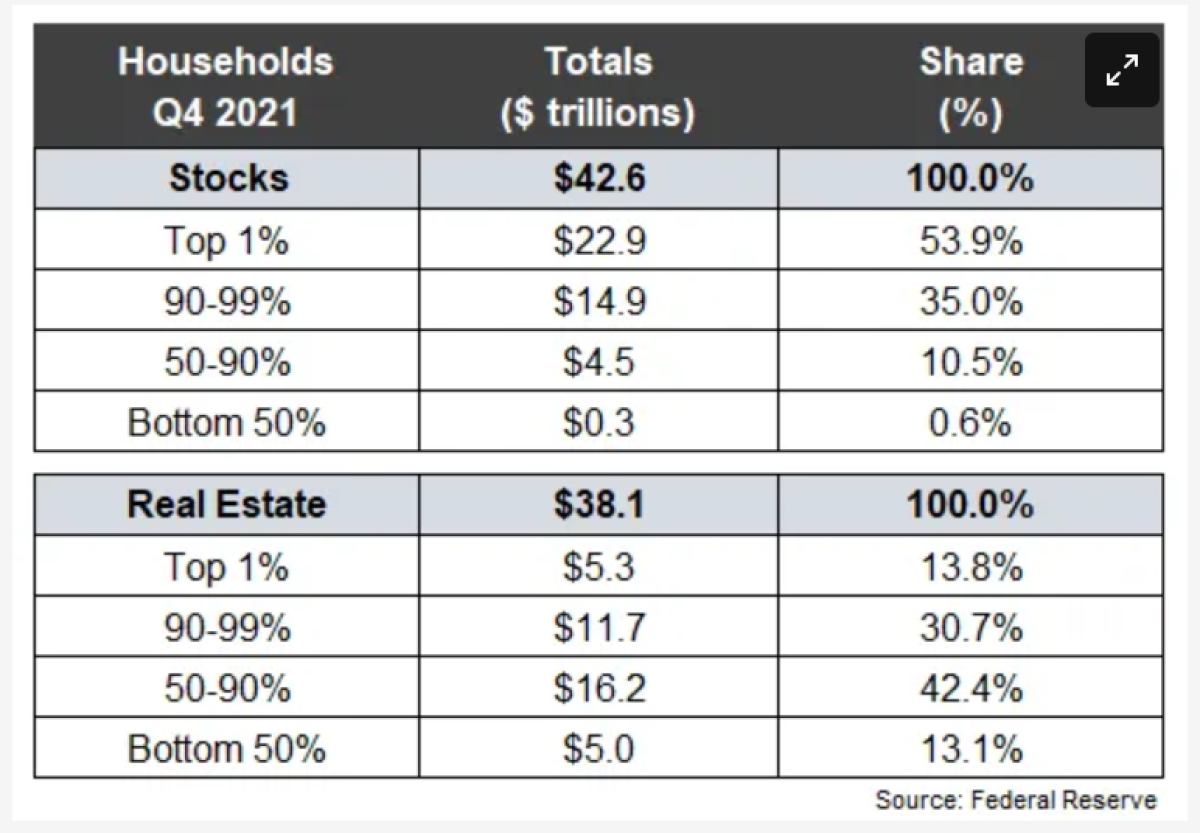

Real estate stands as the world's most crucial asset class, boasting a value exceeding $200 trillion, surpassing the combined worth of shares and bonds. For most of the Western world, the majority of our wealth is locked within this sector. In the United States, for instance, while the top 10% controls nearly 90% of the stock market, the bottom 90% owns over 55% of the housing market.

Residential real estate ownership is more widespread compared to listed stocks and bonds. However, it is still classified as an alternative asset, along with other investments outside the realm of stocks and bonds. Various avenues exist for accessing this asset class.

First and foremost, private investors have the option of direct ownership, which involves transaction fees, significant time investment, and property management responsibilities.

On the other side of the spectrum, new ways to get exposure sprout. The most recent startup I spotted offers to: “Invest in the equity of residential homes on the Blockchain”. It looks like it’s a way to securitize residential equity release. I have so many questions about that, but first: Why? (We’ll leave this for another day.)

Then there are REITs, Real Estate Investment Trusts, an established industry introduced first in the US in 1960 to avoid the shortcomings of direct ownership.

Although REITs were created for private investors, the current offerings are not designed with them in mind. It uncovers essential aspects that investors should be aware of regarding REITs.

The Origins of REITs as an Alternative to Property Ownership

REITs were first established by the US Congress in 1960 to give investors, especially small investors, access to income-producing real estate. The original purpose of REITs was:

To allow individual investors to invest in large-scale, income-producing real estate. REITs provide a way for individual investors to earn a share of the income produced through commercial real estate ownership – without actually having to go out and buy commercial real estate.

REITs quickly expanded geographically. They are now commonly available in 40 countries. Furthermore, REITs are no longer limited to commercial real estate; they encompass a broad range of properties.

Here’s a UK definition.

A real estate investment trust (REIT) is a property investment company which, very broadly, simulates (from a tax perspective) direct investment in UK property, and so avoids the additional layer of taxes that can arise when investing through a corporate structure.

While rules may vary, REITs generally distribute a high percentage of their taxable earnings (90% in the US) to shareholders, which allows them to be exempt from corporation tax on rental income and gains from investment property sales, effectively avoiding double taxation.

The idea behind a 90% distribution is that the management does not reinvest in value-creating initiatives. This presents the first paradox of REITs: although they utilize equity as a vehicle, investors aim to minimize their exposure to equity.

Currently, there are 865 listed REITs worldwide, with a combined equity market capitalization of approximately $2.5 trillion (as of December 2021).

What’s inside a REIT?

The second paradox lies in the fact that REITs do not always align with our traditional perception of property.

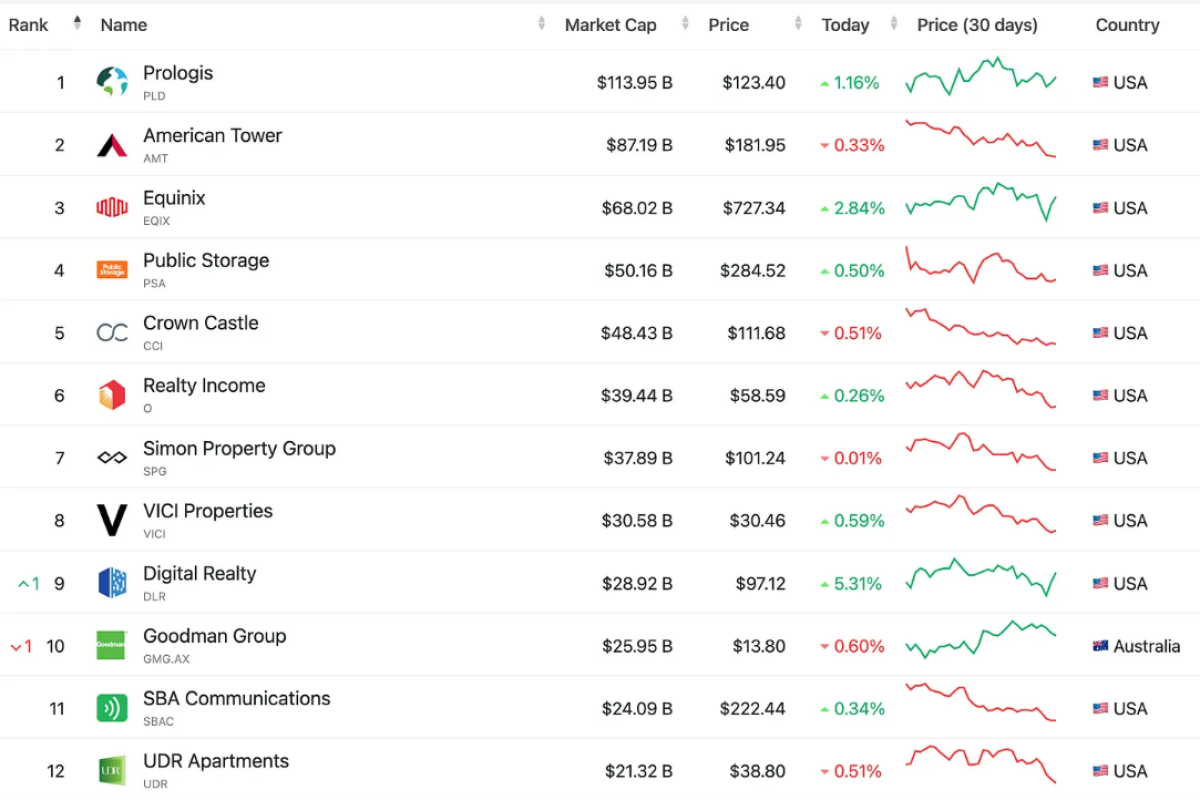

Within the realm of REITs, a wide variety of companies generally focus on specific sub-sectors. The three largest ones are American:

-

Prologis: invests in logistics facilities (Sector: Industrials)

-

American Tower: owner and operator of wireless and broadcast communications infrastructure (Sector: Cell Towers)

-

Equinix: a leader in global colocation data center market share (Sector: Data Centres)

None of those would be top of mind when it comes to property for the non-initiated. Commercial or residential properties are not in the top three, although they are the largest pool of assets. But it’s not about matching expectations. What matters is the behavior of the asset. For Phil Bak, Data Centres and Cell Towers are more correlated to tech stocks than you are to real estate.

The shift from real estate to equity means that we are looking at the asset class in terms of market capitalization, which can be problematic for allocations.

Finding residential REITs can be less obvious, but closer examination reveals UDR Apartments at #12: Luxury apartment homes offering superior comfort, amenities and premier locations from NYC to LA.

Most of those are not well-known brands, and it takes some effort to research what the company actually does, although sometimes the labeling is clear:

-

UDR Apartments does apartments

-

Public Storage does just that

However, the market's subdivisions pose an additional challenge. Taking a UK residential example, a simple search for residential REITs yields two seemingly straightforward results based on their tickers:

-

RESI

-

HOME

But if you look closer they are high-yield:

However, a closer examination reveals that both RESI and HOME belong to the high-yield or junk category.

-

RESI: invests in affordable shared ownership and retirement rentals across the UK.

-

HOME starts with a promising pitch:

Targeting inflation-protected income and capital returns by funding the acquisition and creation of a diversified portfolio of high-quality, well located accommodation assets across the UK

-

but ends with a goal

by providing accommodation to homeless people

It turns out this is a scandal-ridden company that has suspended trading and is being restructured.

This highlights the first lesson for private investors: REITs do not always match their surface appearances, and the labeling can be misleading. Furthermore, choices outside the US are relatively limited.

Accessing REITs via Funds and ETFs

Given these challenges, adopting a strategy of broad diversification appears to be a prudent approach within the industry, aligning with Warren Buffett's advice to "invest in a broadly diversified passive vehicle."

While the S&P 500 represents 80% of the total US equity market (private + public), REITs, with $2.5 trillion in assets, account for only 1% of the total real estate asset class.

REIT funds and ETFs provide avenues for investing in this asset class. Specialized funds like HAUS, which focuses on US residential real estate, are clearly labeled. However, broader funds pose greater difficulties.

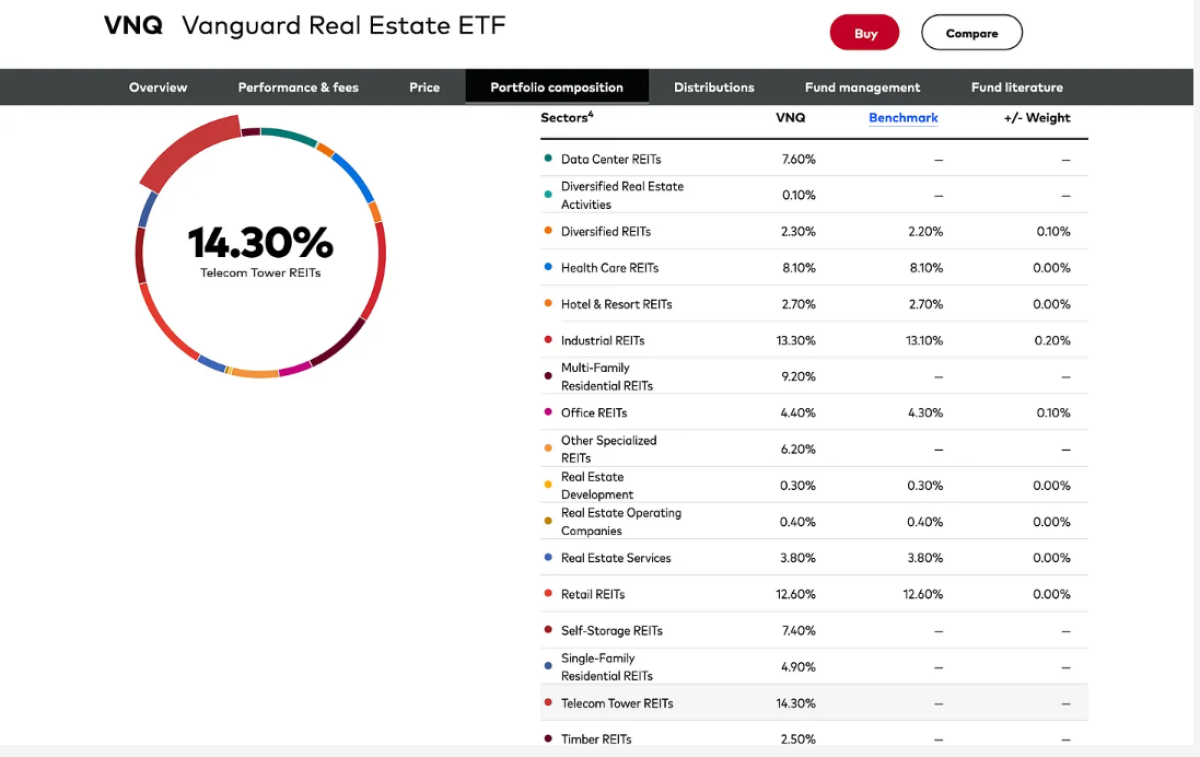

For instance, Vanguard Real Estate ETF (VNQ), the largest of its kind with over $31 billion in assets, exhibits the following sector weights:

-

Telecom Towers: 14.30%

-

Industrial: 13.30%

-

Retail: 12.60%

Considering the previous discussion on Prologis (Industrial) and American Tower (Telecom Towers), this weighting comes as no surprise. Nevertheless, it introduces a correlation that most real estate investors seek to avoid.

With a multitude of sub-sectors, classifying REITs can be straightforward in some cases. For instance, Equinix focuses on data centers, which aligns with the Data Centers sector. However, Prologis is classified as Industrial, despite its operations being centered around logistics rather than traditional industrial properties like factories.

The weighting of VNQ and other broad REIT funds encompasses both paradoxes associated with REITs:

-

The weighting is based on equity market capitalization, while the objective is to minimize equity exposure.

-

The composition introduces a counter-intuitive correlation with other sectors, particularly the technology sector.

The REIT Reality for Investors

The term Real Estate comes from

-

Realis, a Latin term that means existing and true

-

Estate, from the Latin term status, which means state or condition

REITs are a well-intentioned and successful financial innovation, but they don’t always deliver the true condition of the asset that investors desire.

While they promise exposure to real estate without the need to buy and manage the properties directly, they are complex instruments that require considerable effort to use as intended. Hence, they rightfully fall into the category of alternative assets. This underscores the crucial role that advisors need to play, aligning with the CAIA's emphasis on professionalism.

Nonetheless, it is possible to envision a future in which REITs become more mainstream and serve as suitable tools for all investors, particularly in the context of their most significant financial decision, home purchases. Achieving this would necessitate:

-

Improved labeling at the individual and sector levels.

-

Enhanced investor education.

There's a new ETF that clones BREIT for a fraction of the cost - and has liquidity.

About the Author:

George Aliferis, CAIA is the CEO of Orama a video and audio marketing agency specializing in fintech, and the content creator behind InvestOrama, a content platform that explores the future of investing across alternative assets, Defi and technology - but without the hype. Previously, George worked as a front-office professional for over a decade across derivatives, ETFs, and alternative investment products in Paris, Singapore, and London. He holds a Master's Degree from HEC Paris.