By Nicolas Rabener, CAIA, CEO & Founder of Finomial.

SUMMARY

- Ideally diversifying funds are uncorrelated and generate positive returns

- However, identifying such funds is more challenging than expected

- Creating a diversified portfolio requires thoughtful fund and asset class selection

INTRODUCTION

In our last research note (read Diversification versus Hedging), we explored creating a diversification strategy by selecting funds that exhibit negative downside betas to the S&P 500. We learned that downside betas are useful metrics for evaluating funds, but need to be viewed carefully. If too negative, then these funds essentially represent tail risk hedges, which are less attractive as investors can simply reduce their equity exposure to achieve the same effect.

In contrast, funds with only moderately negative downside betas are more useful for portfolio construction as they make money when stocks lose, but can also produce positive returns when stocks rise, at least theoretically. Bonds exhibited these unique characteristics for the better part of the last four decades until central banks started rising interest rates to combat inflation in 2022, which resulted in poor performance of the traditional 60-40 equity-bond portfolio.

In this research note, we will continue to explore creating a diversification strategy by selecting funds primarily based on their downside betas.

CREATING A DIVERSIFICATION STRATEGY

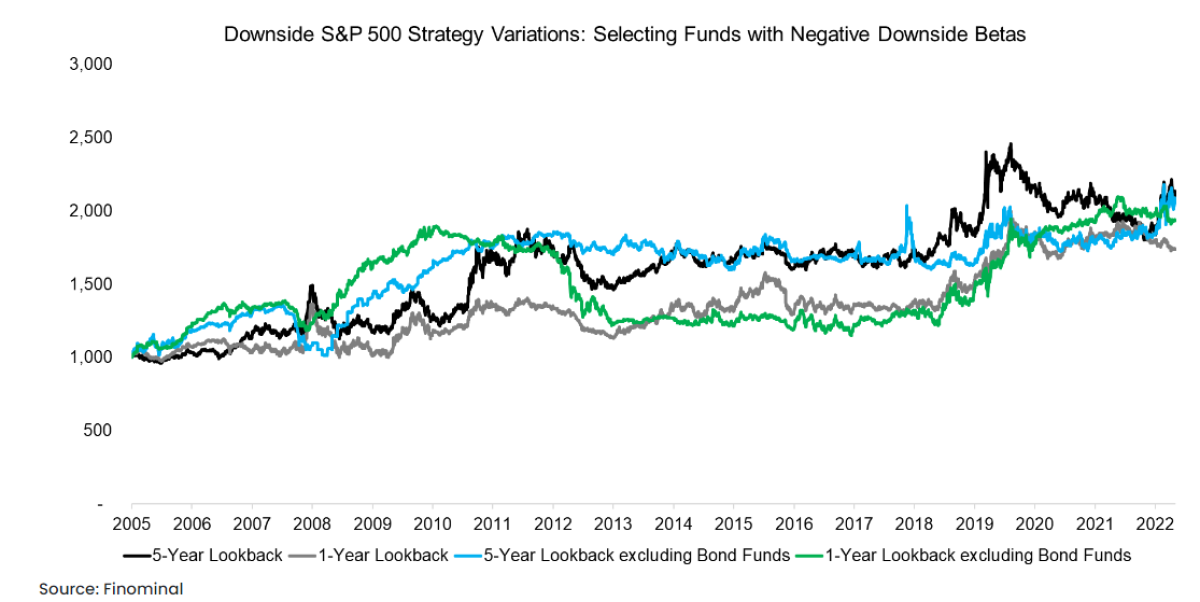

We rank all funds trading in the U.S. stock market, which includes mutual funds and ETFs, by their downside betas to the S&P 500, but exclude any with betas below -0.5 in order to avoid including tail risk products (try Finominal’s Diversification Booster).

We create four portfolios by selecting the top 10 funds with the lowest downside betas where we vary the lookback for calculating the downside betas between one and five years, and versions where we exclude bond funds. The reason for excluding bond funds is that most investors already have exposure to fixed income, i.e. these should not be considered diversifying products, and the low-interest rate environment has made them less attractive given low to negative expected returns. Portfolios are held for a year and then rebalanced.

Evaluating the performance of these four portfolios in the period between 2005 and 2022 highlights that all generated positive returns. However, we observe that the portfolios excluding bond funds lost money during the global financial crisis in 2008, while the two portfolios including bond funds lost money in 2022 when interest rates increased.

BREAKDOWN BY FUND TYPES

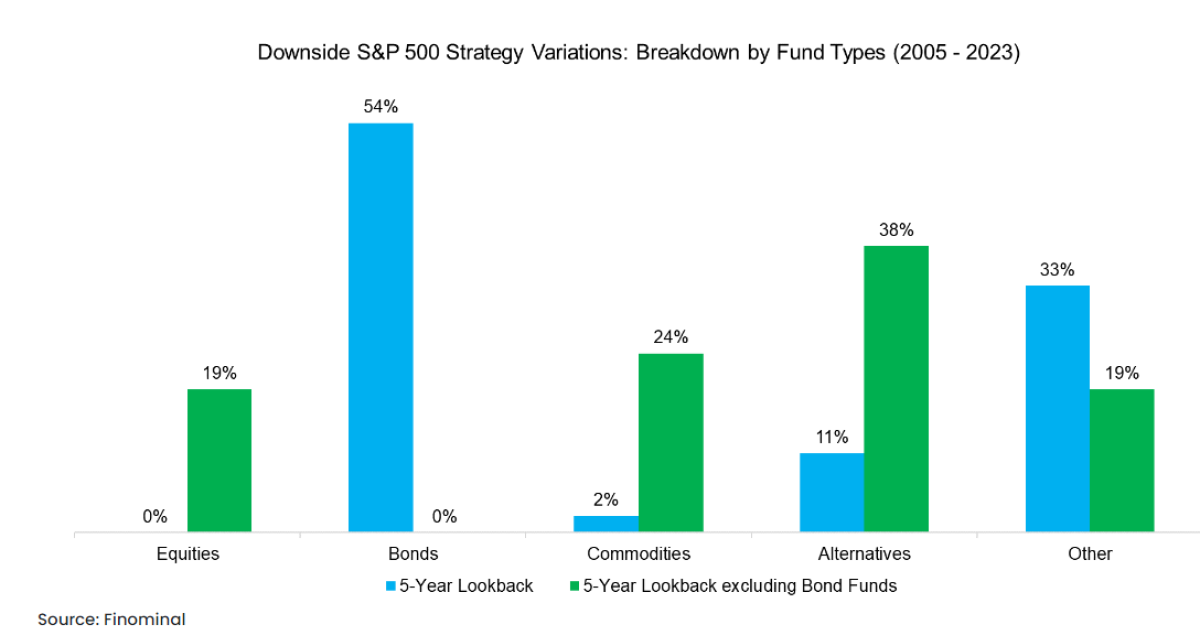

Reviewing the breakdown by fund types of the two portfolios highlights that the unconstrained portfolio was more than 50% comprised of bond funds in the period between 2005 to 2023. The portfolio excluding bond funds was more diversified with alternative funds representing the largest fund type. However, it also included equity funds, which are typically not considered when creating a diversification portfolio, although most of these offered differentiated exposure such as gold miners, special opportunities, Chinese stocks, and real estate.

DOWNSIDE PROTECTION + POSITIVE RETURNS

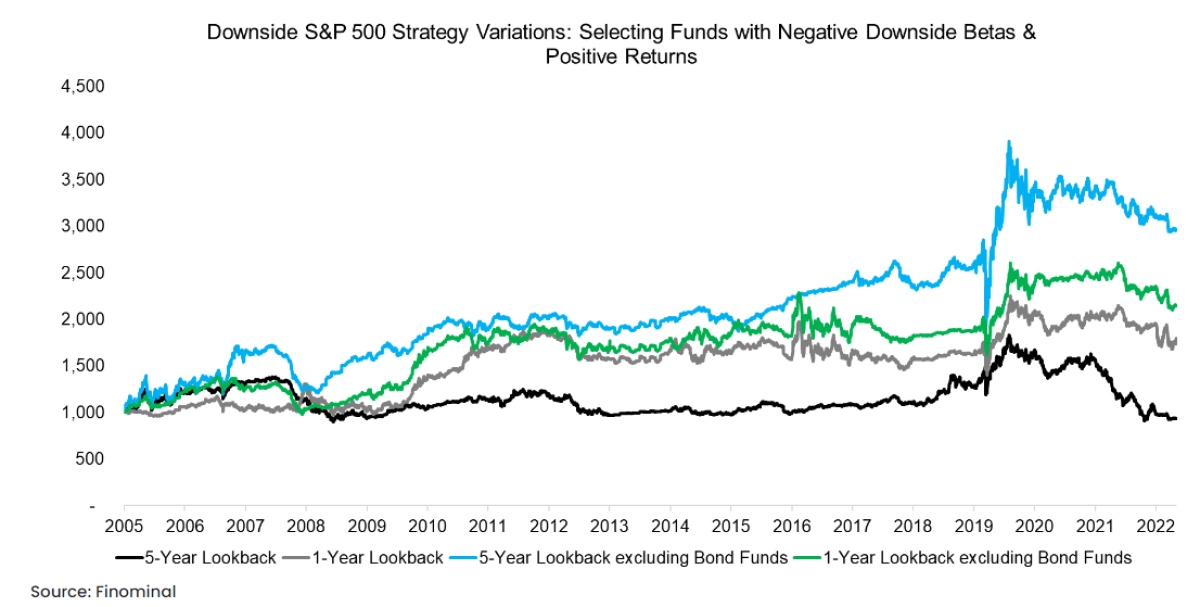

Our approach to selecting diversifying funds can be challenged as it focuses exclusively on downside betas. It could be argued that ideally diversifying funds should offer negative downside betas to stocks as well as positive returns (read Finding Funds with Diversification Potential).

We test this hypothesis and create four additional portfolios that rank funds by their downside betas and total returns, which are calculated separately and then combined via the geometric average into one metric. We observe that three of these portfolios would have generated a positive performance over the last 18 years. However, they seem to have been less effective at offering diversification benefits as they lost money both during the global financial crisis in 2008 and the COVID-19 crisis in 2020.

Devising a methodology for combining downside betas and total returns is more challenging than perhaps expected. Some funds generate outsized returns for idiosyncratic reasons and exhibit slightly negative downside betas, thus ranking them highly, but not structurally representing diversifying strategies. Other funds feature more negative downside betas, but also negative returns, e.g. managed futures / CTAs did not perform well during the last decade, thus ranking them lowly.

CORRELATION ANALYSIS

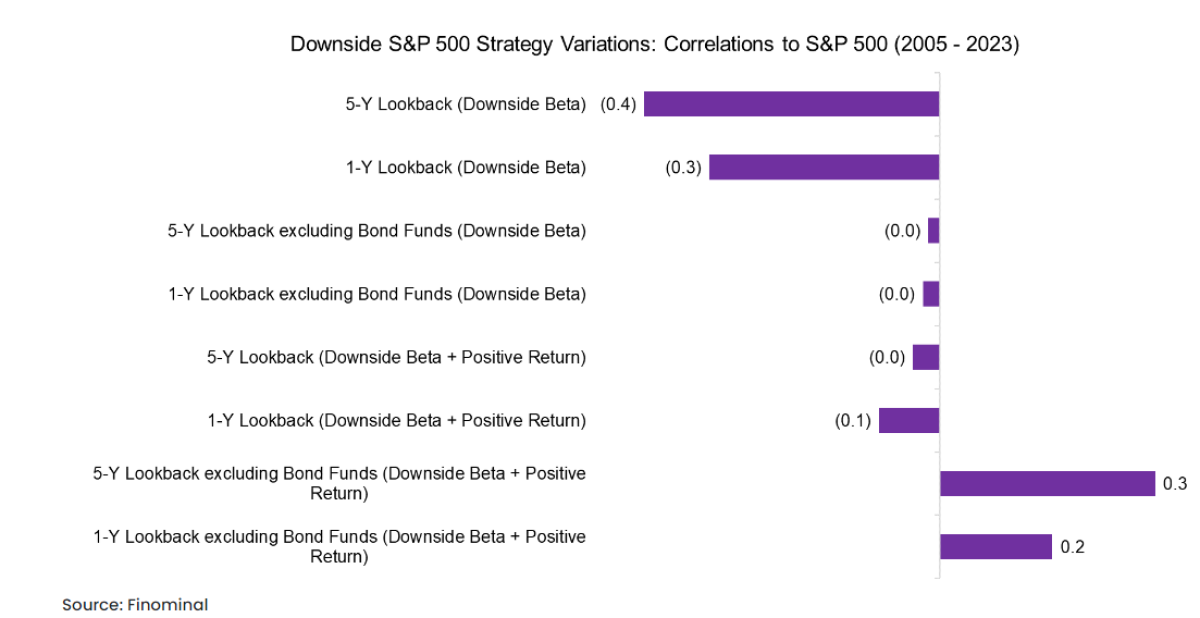

In order to quantify the diversification benefits, we calculate the correlations of these eight portfolios to the stock market in the period between 2005 and 2023. We observe that the two portfolios using only downside betas for fund selection exhibited the most negative correlations. In contrast, including the positive return requirement and excluding bonds resulted in a positive correlation to stocks.

Given this, we would prefer to focus on downside betas rather than trying to combine downside betas and positive returns.

DIVERSIFICATION BENEFITS

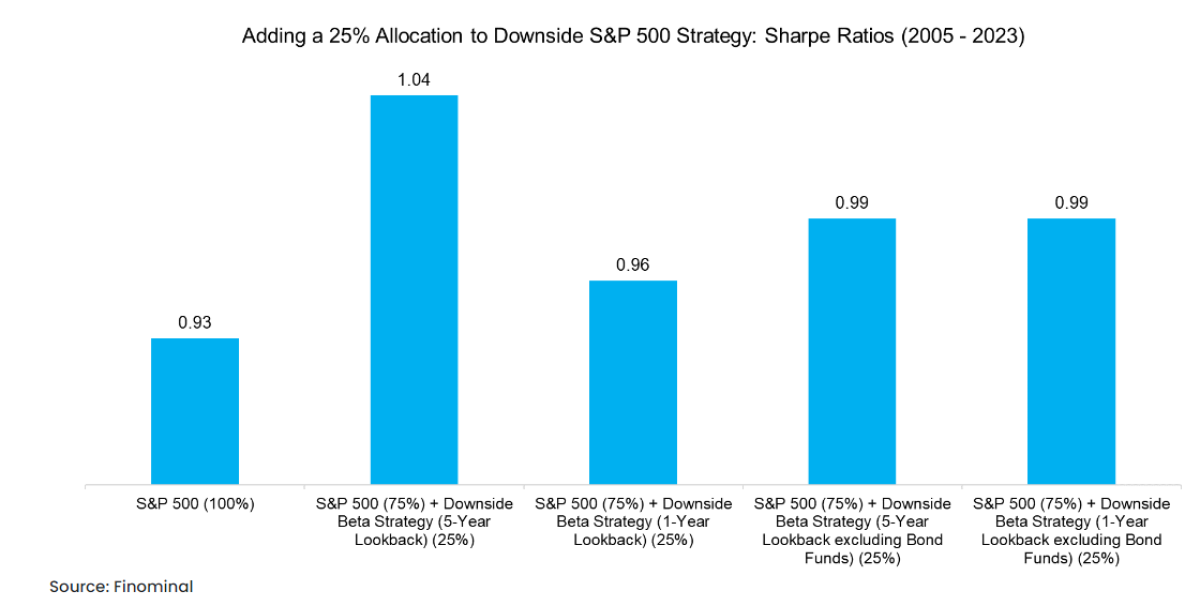

Finally, we backtest adding a 25% allocation of either of these four strategies using exclusively the downside betas to a portfolio comprised solely of the S&P 500. We observe that the Sharpe ratio would have increased marginally in the period between 2005 and 2023. Given that the S&P 500 was mostly represented a bull market, the total returns of the combination portfolios were lower, but so were volatility and maximum drawdowns.

DOWNSIDE BETAS TO STOCKS & BONDS

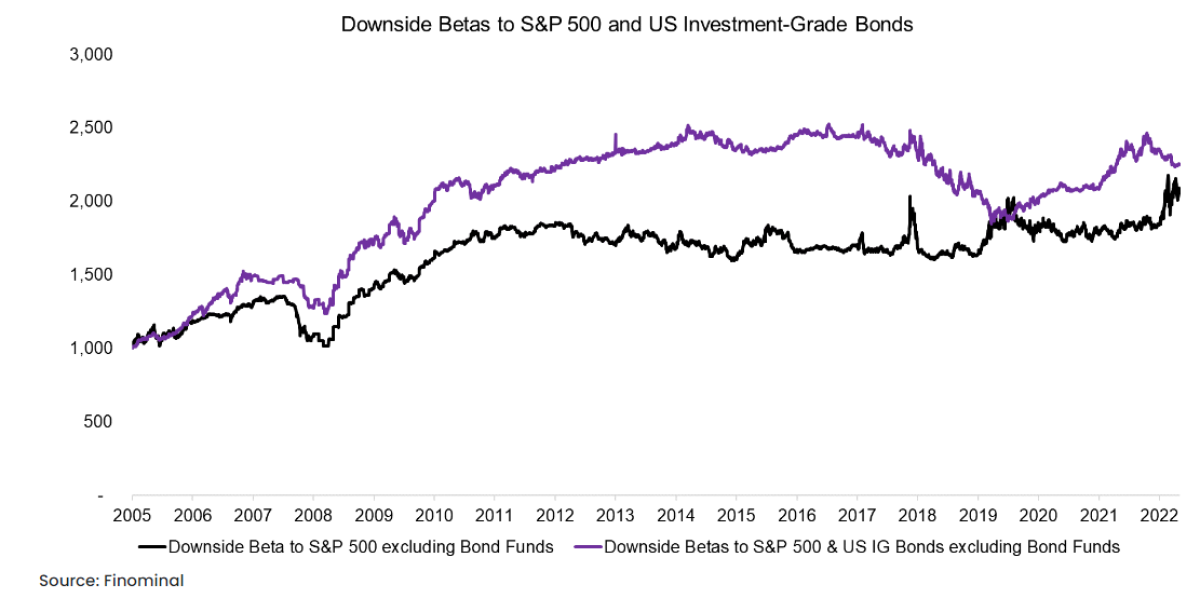

Theoretically, it would make sense to measure downside betas to stocks and bonds given that most investors have exposure to both asset classes.

We run this additional scenario by selecting the top 10 funds with the most negative downside betas to the S&P 500 and US investment-grade bonds, which are combined using the geometric average. We use again a maximum downside beta of -0,5, a five-year lookback, rebalance annually, and exclude any fixed-income funds.

The performance of this scenario is somewhat comparable to the strategy of simply using the downside beta to the S&P 500 and excluding bond funds, at least from 2005 to 2018. Thereafter the performance was markedly different.

FURTHER THOUGHTS

The base requirements for any diversifying strategy should be uncorrelated returns to stocks, specifically when stock markets crash or decline, and positive returns. However, it is remarkably difficult to identify products that fulfill these two criteria.

Bonds offered this historically, but have become riskier given lower yields. Almost all other asset classes, eg like private equity or real estate, or complex trading strategies, like carry or variance risk premium harvesting, are just bets on economic growth again, ie provide the same exposure as equities.

Downside betas can help to reduce the universe of strategies, but building a diversified portfolio requires thoughtful fund and asset class selection.

RELATED RESEARCH

Diversification versus Hedging

Finding Funds with Diversification Potential

Downside Betas vs Downside Correlations

Upside versus Downside Stocks

Myth Busting: Alts’ Uncorrelated Returns Diversify Portfolios

Are Alternative ETFs Good Diversifiers?

Market Neutral Funds: Powered by Beta?

Merger Arbitrage: Arbitraged Away?

Hedge Fund ETFs

A Horse Race of Liquid Alternatives

Liquid Alternatives: Alternative Enough?

About the Author:

Nicolas Rabener is the founder & CEO of Finomial (formerly FactorResearch) and previously founded Jackdaw Capital, an award-winning quantitative hedge fund. Before that Nicolas worked at GIC and Citigroup. Nicolas holds an MSc from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon).