By Doug Dundas, Chief Marketing Officer of Essentia Analytics.

Active managers are still very much at play in today’s market, and recent findings show that skilled ones can outperform their indexes.

Essentia’s recent announcement of a skills-based manager assessment methodology — the Essentia Behavioral Alpha® Benchmark — contains findings that illuminate and advance the discussion about whether active portfolio managers can justify their approach (and their fees) versus no/low-fee passive index strategies.

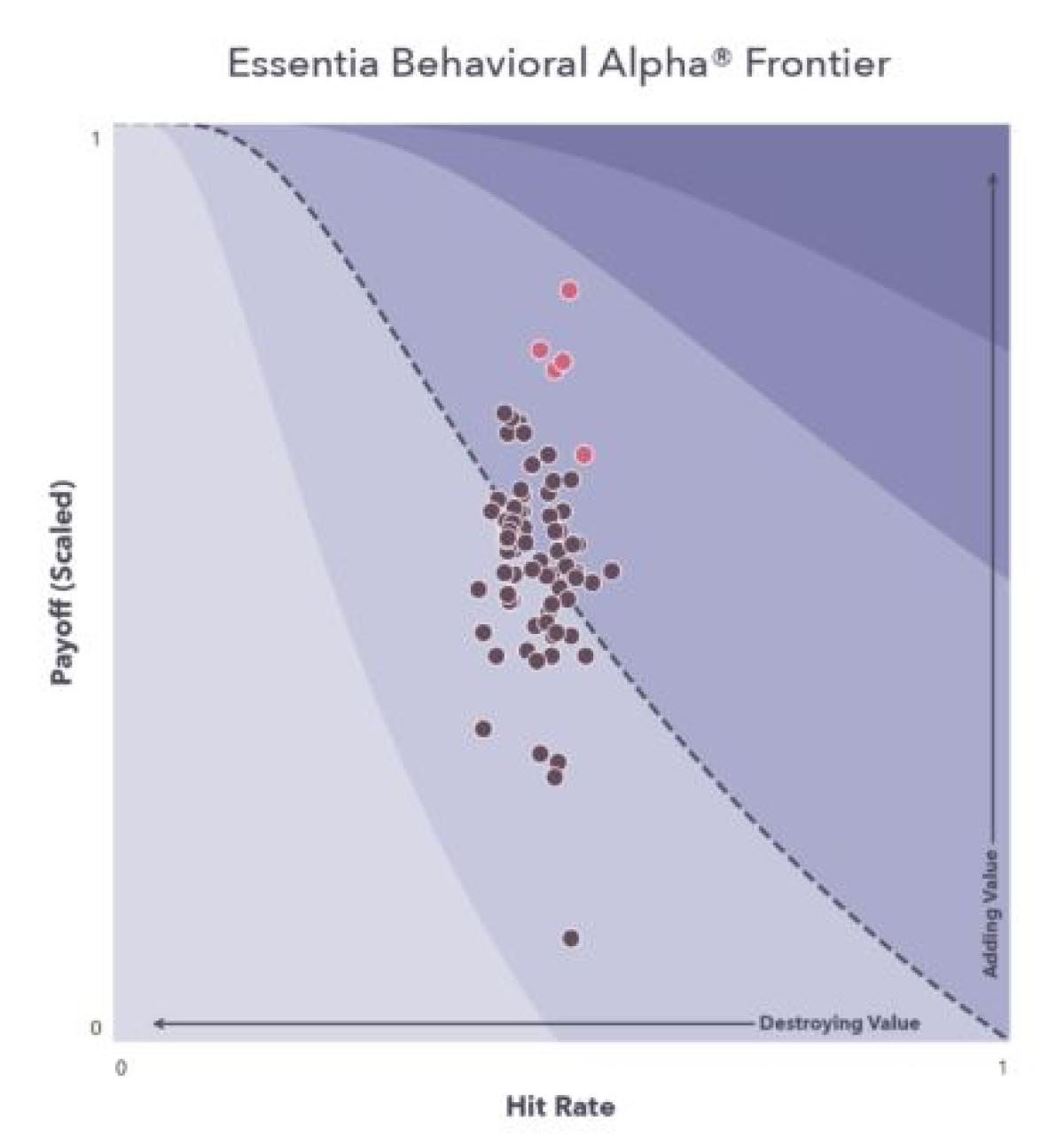

The Benchmark enables us to do the same analysis we’ve been doing for years at the individual portfolio manager level on groups of PMs — so we can, for the first time, compare/rank PMs based on their demonstrated skill across a number of key decision types, and aggregate the analysis. The diagram below plots 76 active equity managers we analyzed with the Benchmark over a three-year period — the top five managers are indicated by the magenta dots.

It will probably come as no surprise that we found some stark deficiencies in the active managers’ demonstrated decision-making skill when compared to index funds (which, as passively-managed vehicles, entail no active-management decision-making and thus reflect no “skill effect” one way or another). The most drastic takeaway: only 18% of fund managers made the right decision most of the time (the full paper with detailed results is available for download here).

That’s a sobering figure, and our findings contain other formerly undiscovered dimensions of active managers’ relative underperformance. But given the exhaustive coverage of active managers’ shortcomings in the media and academia, it’s no surprise.

What is at least illuminating — if not surprising, at least not to us at Essentia — is the fact that a lot of active managers do exhibit evidence of skill beyond the neutral effect of the index. That’s clearly evident in the diagram above: the dashed line is the “value threshold,” and is the boundary between evidence of being skilled or unskilled relative to the fund’s index. Every dot to the right of that line is an active manager who’s adding value.

And on some specific metrics, active managers in aggregate clearly demonstrate value-additive skill over and above their index — in some cases, like stock picking, by a healthy margin (58% of the managers in our study added value through their stock picking decisions).

We can deduce a couple of key points here:

-

- Human portfolio managers are quite good at some things (like buying stocks), but bad at others (like getting out of a position — which we already knew from our Alpha Lifecycle research that showed the propensity of managers to fall in love with a stock and ride it off the proverbial cliff). So the question is: can human PMs get better at the things they’re bad at? Yes, they can, by mitigating bias and improving their decision-making — we’ve demonstrated it. As we have reported in the past, we see a strong correlation between engaging in nudges — one of our key decision-making tools — and significantly improved alpha generation (see the study here).

- Less than half, but still a significant percentage (low 40%), of human managers do show evidence of value-added skill. And some add a lot of value. Telling investors not to pick active funds because 60% of them look unskilled assumes investors are completely mindless in their selection of managers. That’s not true — everyone makes an effort to pick good managers; the problem is the assessment tools are largely based on past performance, which is highly subject to the effects of luck. What if we factor in a thoughtful manager selection process with tools that help them assess managers based on demonstrated skill, rather than their most-recent historical return? Surely that will yield a higher likelihood of adding value than the 40% you’d get by random selection. Today, there really are tools and processes that affect this ratio — one can significantly discount the effectiveness of these tools and still easily get over the 10% or so improvement required to get into value-additive territory.

Given all the buzz portending the collapse of active investing at the hands of passive index-based strategies, it’s no surprise that there’s a popular anti-active manager sentiment in the market. And it’s true that active strategies have, on average, underperformed, and also that passive strategies are a great fit for many investors — particularly at the retail level.

But active managers are still very much at play in the market, the good ones do have the potential to outperform their indexes, and the technology is increasingly able to effectively assess — and assist — them.

About the Author:

Doug Dundas is Chief Marketing Officer of Essentia Analytics.

Before joining Essentia, Doug served as CMO at Octagon Asset Management and Marsh Inc., the global insurance brokerage firm. Prior to that, he held leadership roles at Citi, Goldman Sachs, McGraw-Hill, Time Inc., and ABC News.