By Alan Dunne, CEO | Founder of Archive Capital.

-

The US and global economies continue to confound expectations of recession, even after significant monetary tightening

-

A number of factors appear to be blunting the typical transmission mechanism of monetary policy in this cycle, many related to COVID-19

-

Meanwhile, equity investors appear to be extrapolating the recent goldilocks performance of the economy with expectations of accelerating earnings in H2 2023

-

From an asset allocation perspective, although the 60-40 portfolio has recovered in the last three quarters, longer-term real return expectations are muted

-

Alternatives and diversifying strategies continue to look compelling given valuations of traditional assets and macroeconomic headwinds

Where’s the recession?

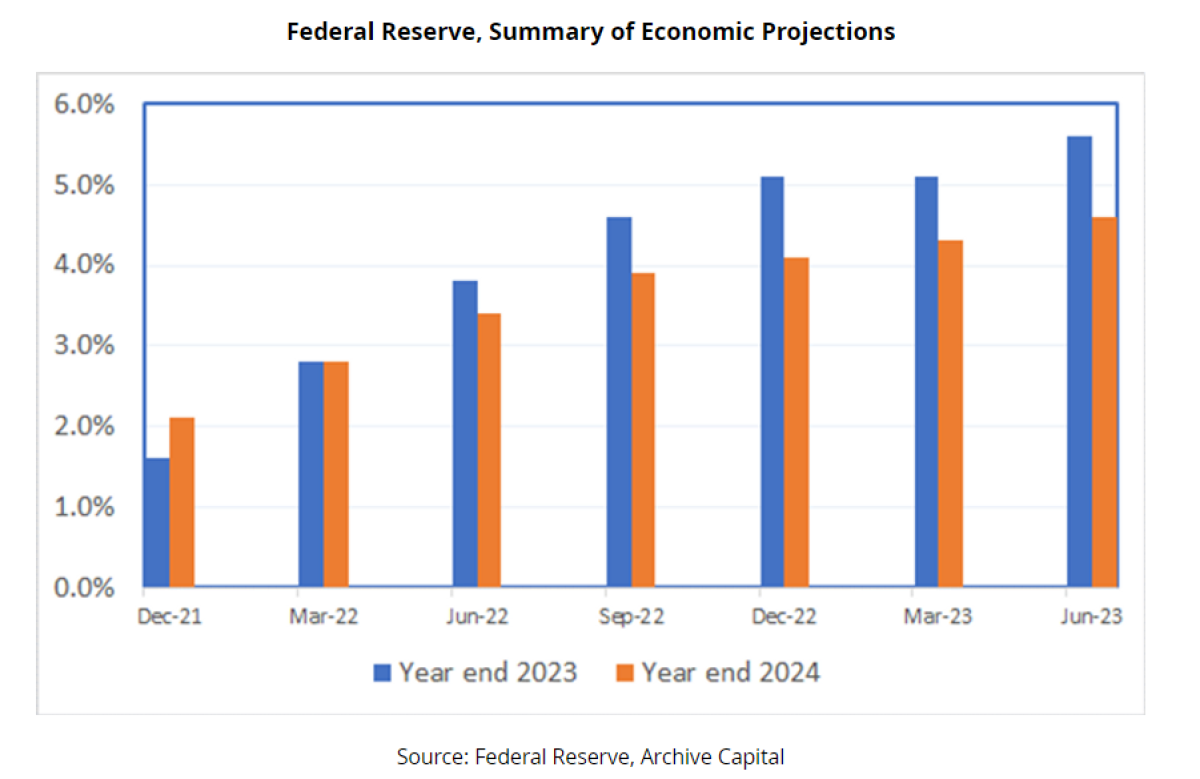

In its latest Summary of Economic Projections (SEP), the Federal Reserve upgraded its forecast for growth, lowered its projection for unemployment, and raised its forecast for core PCE inflation for 2023. The dot plots also pointed to an expectation of higher rates with the median forecast for Fed Funds for December 2023 rising to 5.6%. Sixteen months into the tightening cycle and 500bps of rate hikes later and the economy shows no clear sign of slowing down despite the Fed having forcefully slammed on the brakes.

The resilience of the US economy in the face of higher interest rates has been remarkable. For context, when the Fed started raising rates in March 2022, the dot plots pointed to the Fed funds being at 2.8% at the of 2023 and 2024. As of December 2022, those rates were 5.1% and 4.1% respectively. In fact, apart from March 2023 when the Fed was assessing the impact of the banking strains on the economy, the Fed has raised its forecast for rates at end-2023 and end-2024 in each set of SEPs since the start of the tightening cycle.

The Fed has not been alone in its misdiagnosis of the economy. At the start of the cycle a pervasive view in markets was that due to high debt levels, the economy would not be able to withstand rates going above the 2018 peak of 2.375%. Even in December 2022, talk of recession was everywhere. When we wrote our last investment update in December 2022, we noted “Given the almost universal expectation of recession next year and the fact that recessions are typically a surprise it is tempting to take the contrarian position of growth surprising to the upside.”

The resilience of the economy has been reflected in equity markets with the S&P TR index up 14% this year and the Nasdaq 100 up 36%. Meanwhile, bonds have also posted positive returns as headline inflation levels have declined significantly although core inflation has been somewhat more stubborn.

Why has the economy not yet cracked?

There are three likely explanations for the resilience of the economy and the apparent inefficacy of monetary policy in slowing the economy.

Long and variable lags

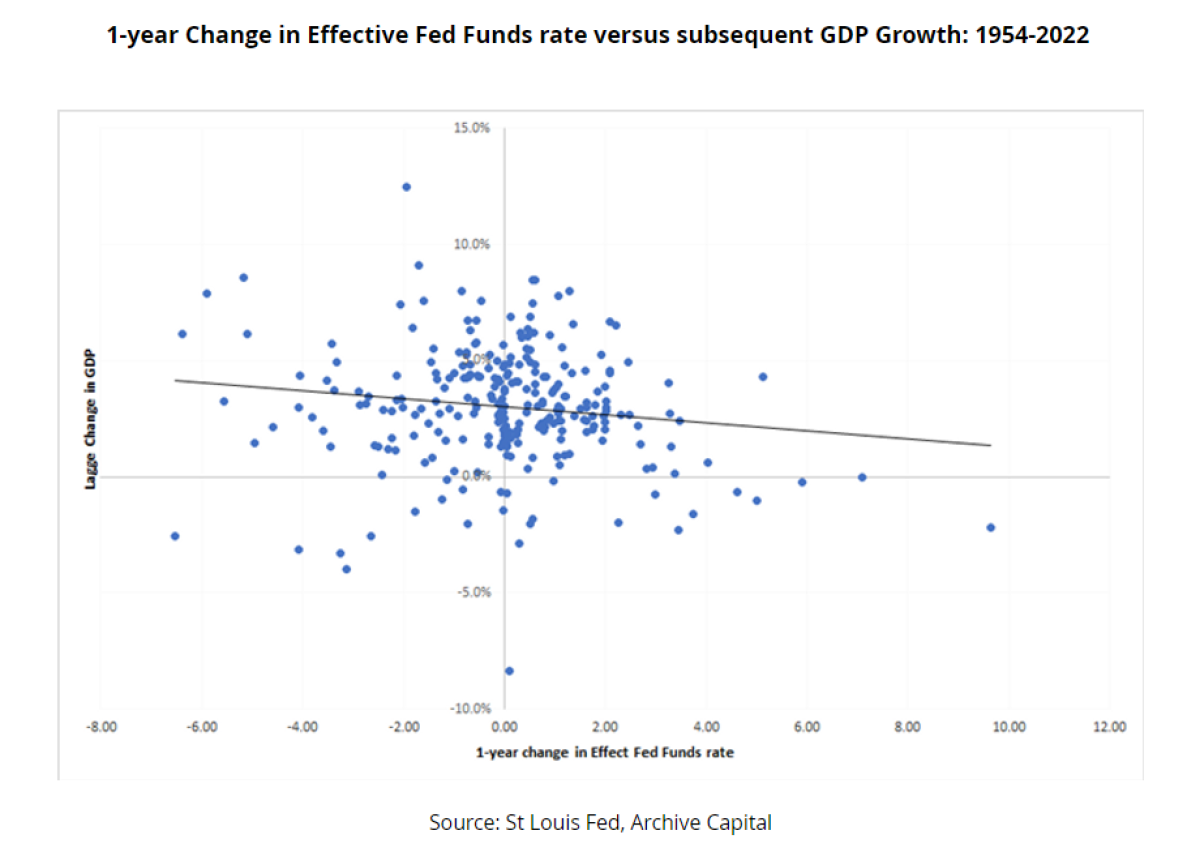

As we wrote in December, the lags with which monetary policy impact the economy are long and variable but also highly uncertain. The Fed started raising rates in March 2022 but much of the tightening has been in the last 6-9 months. If the lags are 12-18 months we may not see the impact of that policy tightening until later this year or next year.

Of course, economists don’t know precisely how long the lags are and as we can see in the chart below the impact of an X% increase in interest rates on the economy is variable over time. A range of factors like demographics, shifting levels of inequality, changing debt levels and the distribution of debt amongst other factors.

We have seen signs that the economy may be starting to crack (notably in banking, commercial real estate and leverage loans) but to date any slowdown in the real economy has been at the margin.

The transmission mechanism of monetary may have been blunted

A key reason why the lag of monetary policy may be longer this time centres on what economists call the transmission mechanism of monetary policy; the chain of events by which higher rates result in slower growth.

In standard economic models higher interest rates slow demand by reducing growth in consumer spending and investment demand. Higher interest rates make savings more attractive, increase the cost of borrowing for current expenditures and increase mortgage rates (which tend to be a big part of monthly expenditure for homeowners).

Higher interest rates also raise the required return for investment. In a typical investment, you spend money now (e.g. to build a factory) on the expectation of a benefit in the futures (future cashflows). Higher interest rates mean that future cashflows are discounted at a higher rate, reducing the net present value of the investment and in theory making fewer projects look attractive, all else being equal.

There are also second and third-order effects from higher rates which are even more uncertain and tend to be nonlinear and harder to model. Higher interest rates can reduce asset values (like equities and housing) and induce a negative wealth effect (potentially triggering asset sales, further price falls and negative feedback loops). Whereas rising asset values can encourage people to borrow against the equity in their homes, declining asset values may prompt deleveraging.

However, the sensitivity of each of these factors to interest rates is not constant over time. Consumer spending is influenced by the state of the labour market, wage growth and “consumer confidence”. Although jobless claims have started to rise recently, US unemployment remains low by historical standards. Wage growth is solid and household balance sheets are still in aggregate strong. Researchers from the San Francisco Federal Reserve estimate that as of May 2023, households in the US may still have $500bn which they built up during COVID. Higher rates can be a positive for people who have high cash balances.

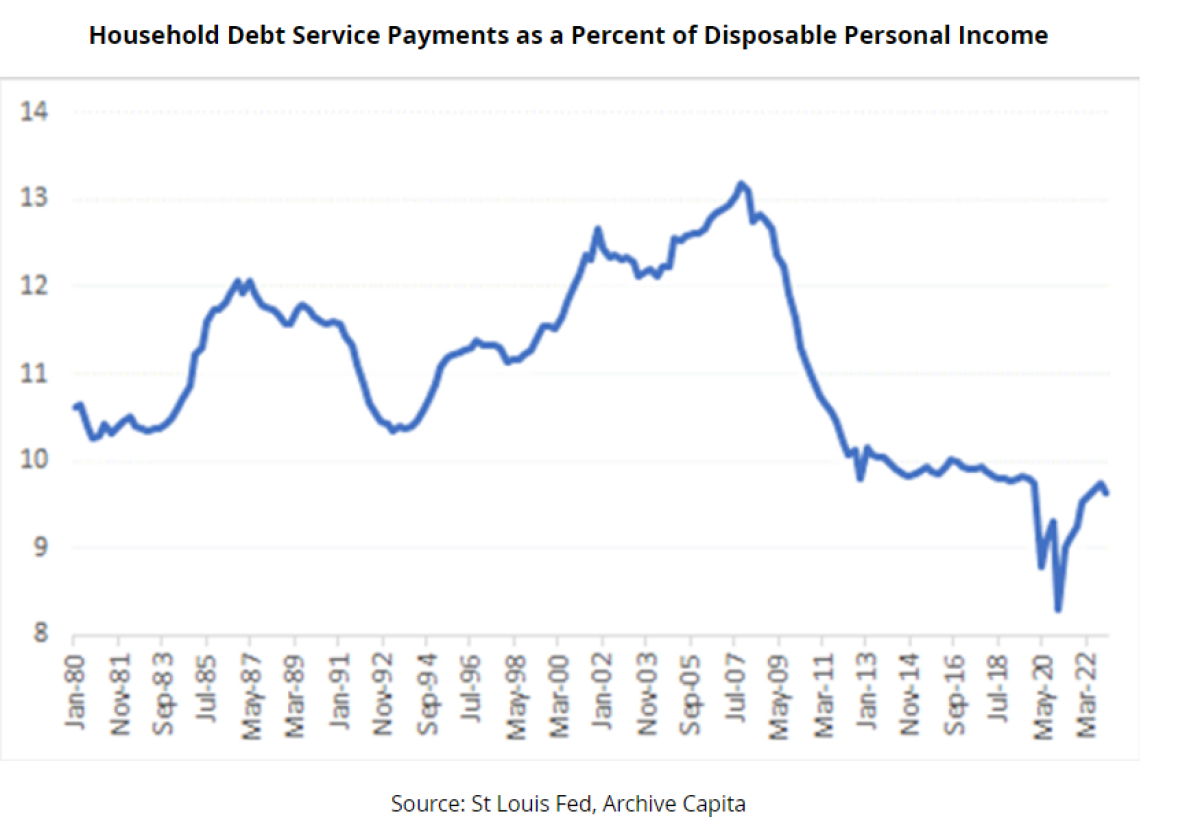

Although interest rates have risen, household debt service payments as a percentage of disposable income are much lower than in previous cycles (because house owners locked in really low mortgage rates when yields fell at the onset of COVID).

On the investment side, as Keynes pointed out, investment decisions are heavily influenced by “animal spirits” and other factors rather than just interest rates. In recent months we have seen a surge in factory construction in the US on the back of a structural trend of nearshoring and incentives around the Inflation Reduction Act.

Total Construction Spending: Manufacturing ($,bn)

Investment in residential housing did slow as house prices fell as mortgage rates rose. However, recent data on housing starts has shown renewed strength as the lack of supply of existing homes has encouraged home builders to bring on a supply of new homes.

Fiscal policy has also continued to provide support. In the US, the government continues to run a budget deficit of 5% of GDP, very high by historical standards for an economy at full employment. In Europe, governments are providing fiscal support to offset the cost of living crisis. In its recent annual report, the BIS suggested that governments should tighten fiscal policy to aid in the fight against inflation. Loose fiscal policy means monetary policy may have more to do to weaken demand to constrain inflation.

Interest rates and financial conditions

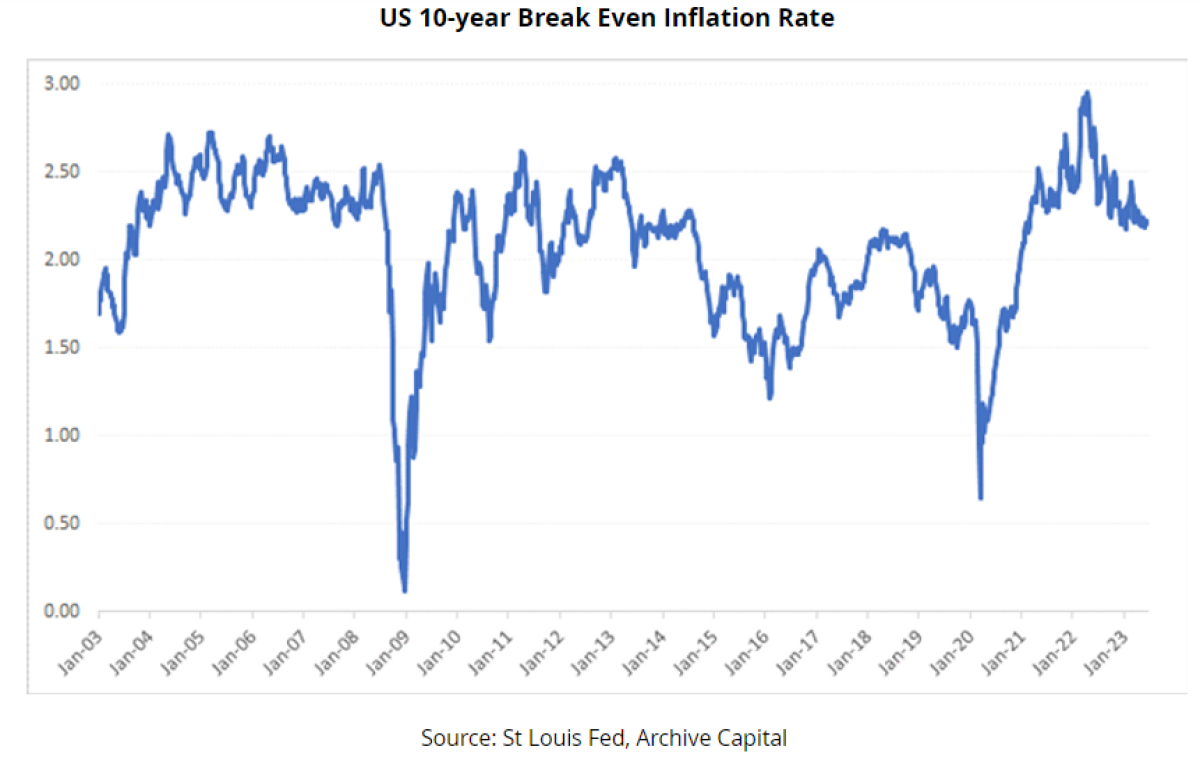

Another contributory factor may be long-term interest rates. Although the Fed has raised the Fed funds rate 500bps, US 10-year yields have been risen by about 3% (from what were unusually low levels during COVID). The failure of long-term bond yields to match the rise in short rates echoes Alan Greenspan’s bond market conundrum of the 2000s. At that time strong demand for US assets from countries recycling current account surpluses (Ben Bernanke’s global savings glut) kept long-term rates in check even as short-term rates rose.

For sure, QE has also distorted long-term rates but other factors have been at play. For one, the Fed has been a victim of its own success as long-term inflation expectations, as reflected in TIPS breakeven rates have remained well anchored. Second, although the Fed has commenced QT this year, subdued issuance at the long end may be supporting long-term bonds. Furthermore, the pervasive expectation of recession continues to fuel expectations of lower future policy rates, keeping longer-term yields in check.

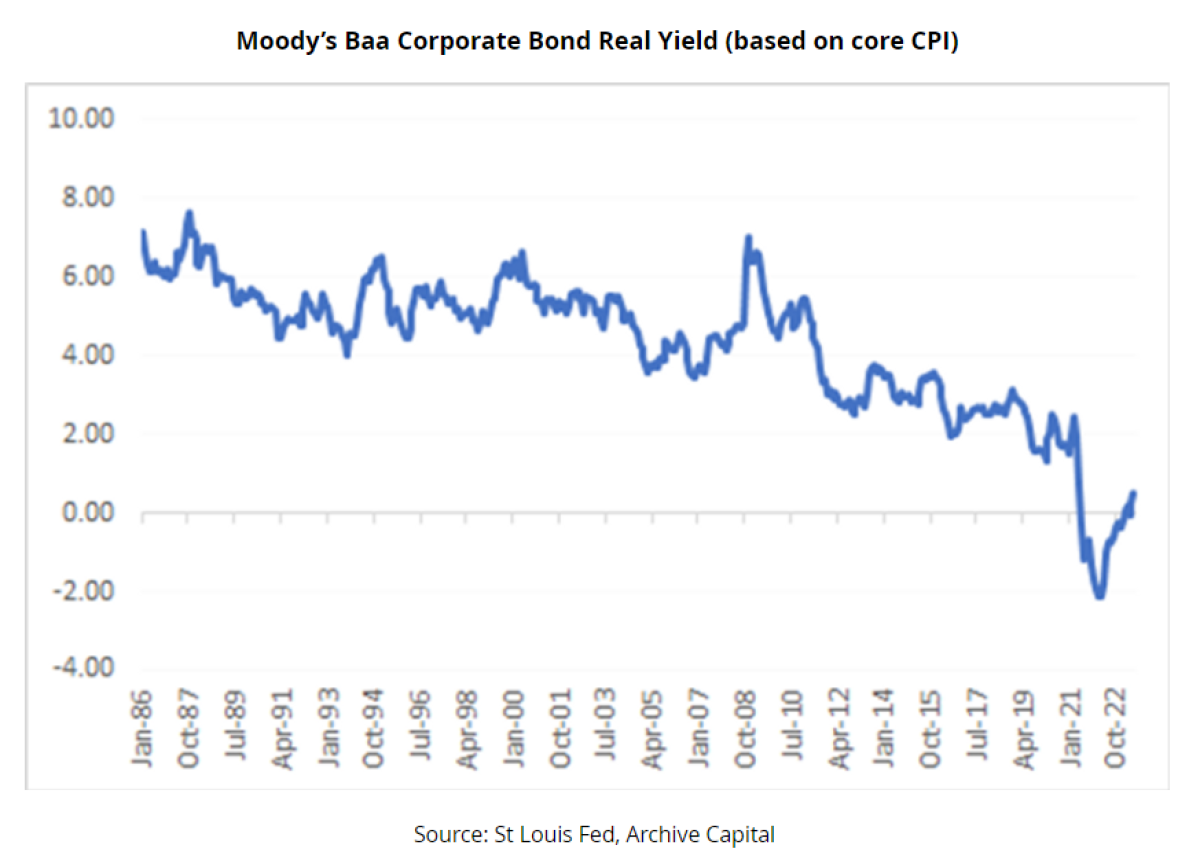

Although declining inflation means real short-term interest rates are now positive, real 10-year yields are still negative (based on either CPI or core CPI). Real 10-year corporate bond yields are also well below levels associated with previous recessions. With equities up about 20% from the lows and nominal bond yields down, financial conditions in the US in aggregate may have eased in recent months.

It may be that we need to see higher yields before we see a meaningful reaction in the economy to higher policy rates.

Market implications

As is often the case there appears to be a disconnect between the bond market and the stock market. Bond markets are factoring in future rate cuts, presumably reflecting an economic downturn, while stocks are rising on hopes that earnings will re-accelerate in H2.

Of course, it is possible that the “immaculate disinflation” could continue allowing the Fed to move rates back to more neutral levels. Although there has been progress on headline inflation and the Fed’s current key focus (services inflation ex housing) from a credibility perspective, it would be difficult for the Fed to risk lowering rates with core rates still well above target.

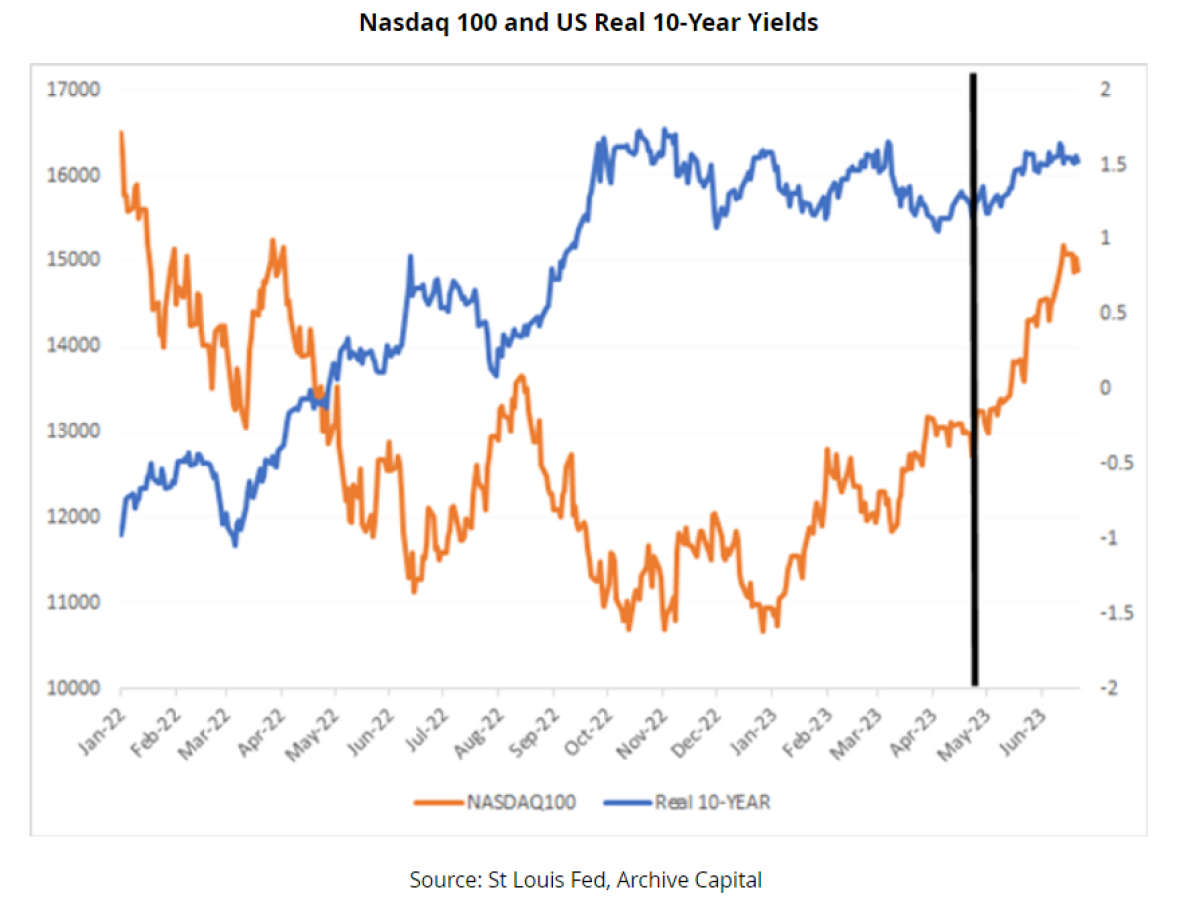

Optimism around growth and earnings appears to be the key driver in equities at the moment. The Nasdaq 100 rallied 30% from early March to its recent high. Initially declining yields and liquidity injections from the Fed after the banking strains of March were seen as a support for stocks, particularly long-duration assets like technology stocks. However, since late-April tech stocks have disconnected from interest rates, continuing to post strong gains even as real yields rose.

Data from FactSet indicates that although analysts expect earnings to decline in Q2 2023 they expect a reacceleration to growth of 8% yoy in earnings by Q4. The optimism is largely focused on Communication Services and Information technology sectors and particularly Amazon, Meta, Alphabet and Nvidia. If these companies were excluded, the estimated earnings growth rate for the S&P 500 for Q4 2023 would fall to 4.2% from 8.2%.

A key support for these stocks and technology more broadly in recent weeks has been optimism around Artificial Intelligence. A recent report from McKinsey highlighted how transformational AI may be for the global economy, potentially delivering $4trn in value on an annual basis and a boost to productivity of 0.1% to 0.6% per annum.

From an economic perspective, greater adoption of AI would result in an outward shift in the aggregate supply curve, resulting in higher output and lower inflation over time as the same amount of labour resources can produce a higher level of output. If true that would be a welcome disinflationary force given the long list of potentially inflationary factors (deglobalization, spending on green energy and demographics etc).

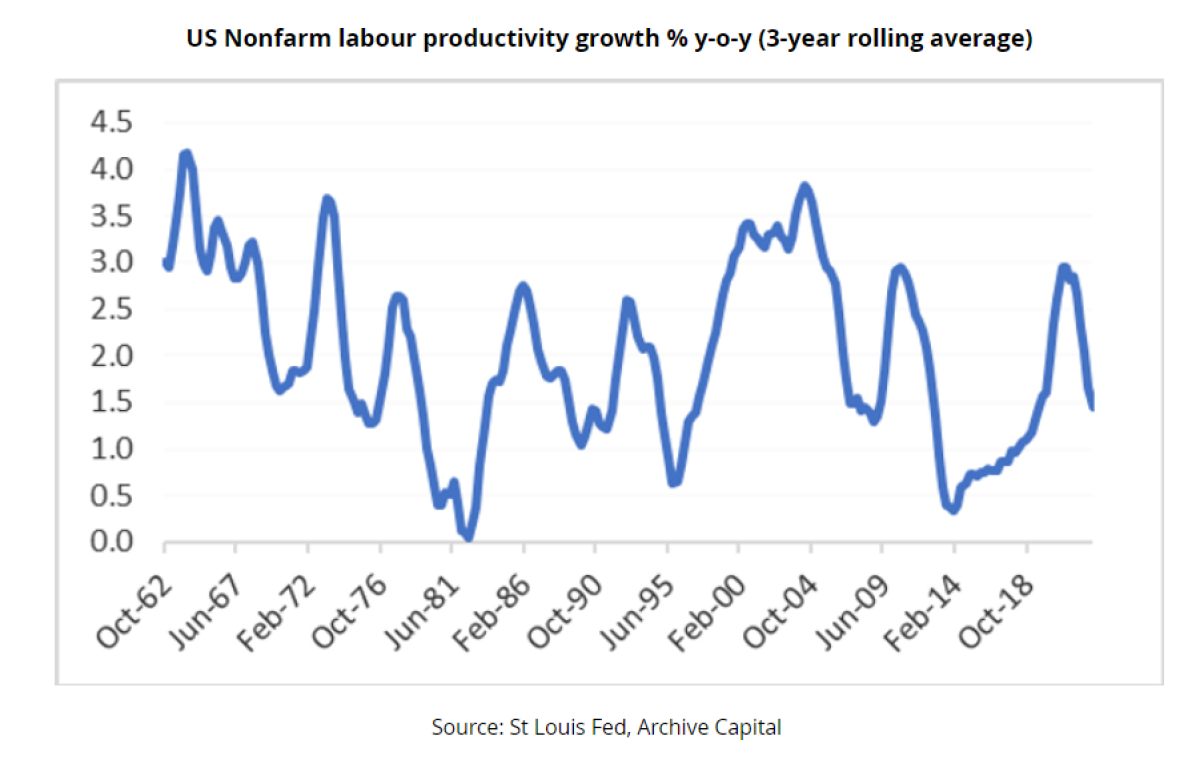

While the case for AI being transformational is compelling it is equally uncertain in its timing and magnitude. Labour productivity rose strongly in the late 1990s (during Greenspan’s new paradigm) but then slowed for the next decade even after the development of the internet. It took ten to fifteen years before there appeared to be a sustained pickup in productivity. According to McKinsey the gains from AI will be significant but will likely play out in in the next number of decades between 2030 and 2050.

In the near term, the key is whether the potential around AI will translate into higher IT spending and stronger earnings. It is notable that the recent run-up in the Nasdaq 100 accelerated after the positive Nvidia earnings and guidance.

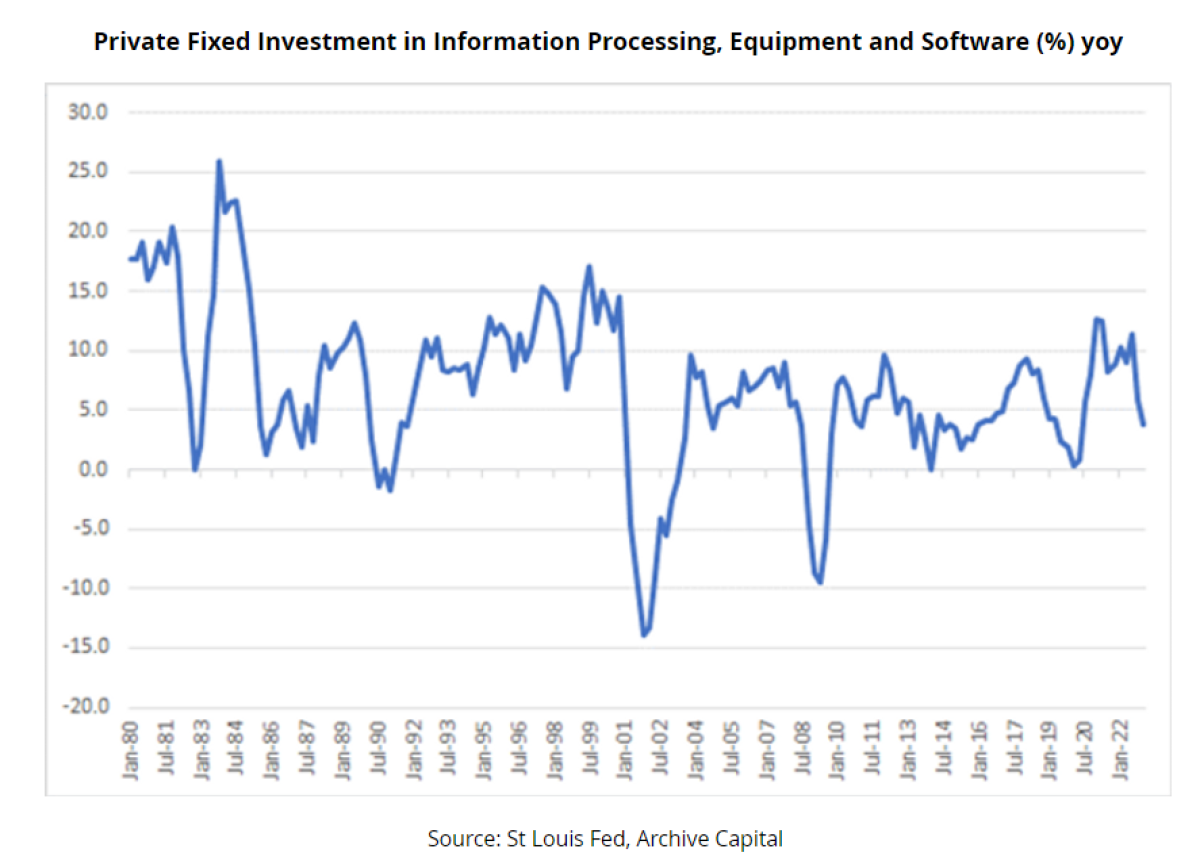

However, that brings us back to the economic outlook. Should the economy slow later this year and into next year, one would expect investment in investment processing equipment and software to take a hit, as has been the case in each recession in the last four decades, which would be a significant headwind for technology earnings.

Asset allocation

After the annus horribilis of 2022 for the 60-40 portfolio, the goldilocks' performance of the economy in 2023 has seen a recovery for both stocks and bonds. In the year to 23rd June, the US 60-40 portfolio is +9.3%. However, even after a 15% recovery since October of last year, the 60-40 is still down -8% from the start of 2021.

Although bonds are positive this year, anybody who invested in the US aggregated at the start of the decade would be in a drawdown of about -5.7% and far more in real terms.

Three factors made 2022 particularly painful for 60-40 investors:

First, coming into 2022 bond yields were unusually low proving an unusually high downside risk for bond prices (bond duration is higher at lower yields). Second, in 2022, the correlation between bonds and equities turned positive as inflation fears dominated; bonds and equities experienced significant drawdowns concurrently. And third, the volatility of bonds and equities rose as prices declined.

Fast forward to 2022, and things look different on each of these measures. Bond yields have risen and real yields are no longer negative. US 10-year investors can expect annualised nominal returns of about 3.6% p.a. from 10-year bonds over the next decade based on the current yield. That marks a significant change from Q1 2020.

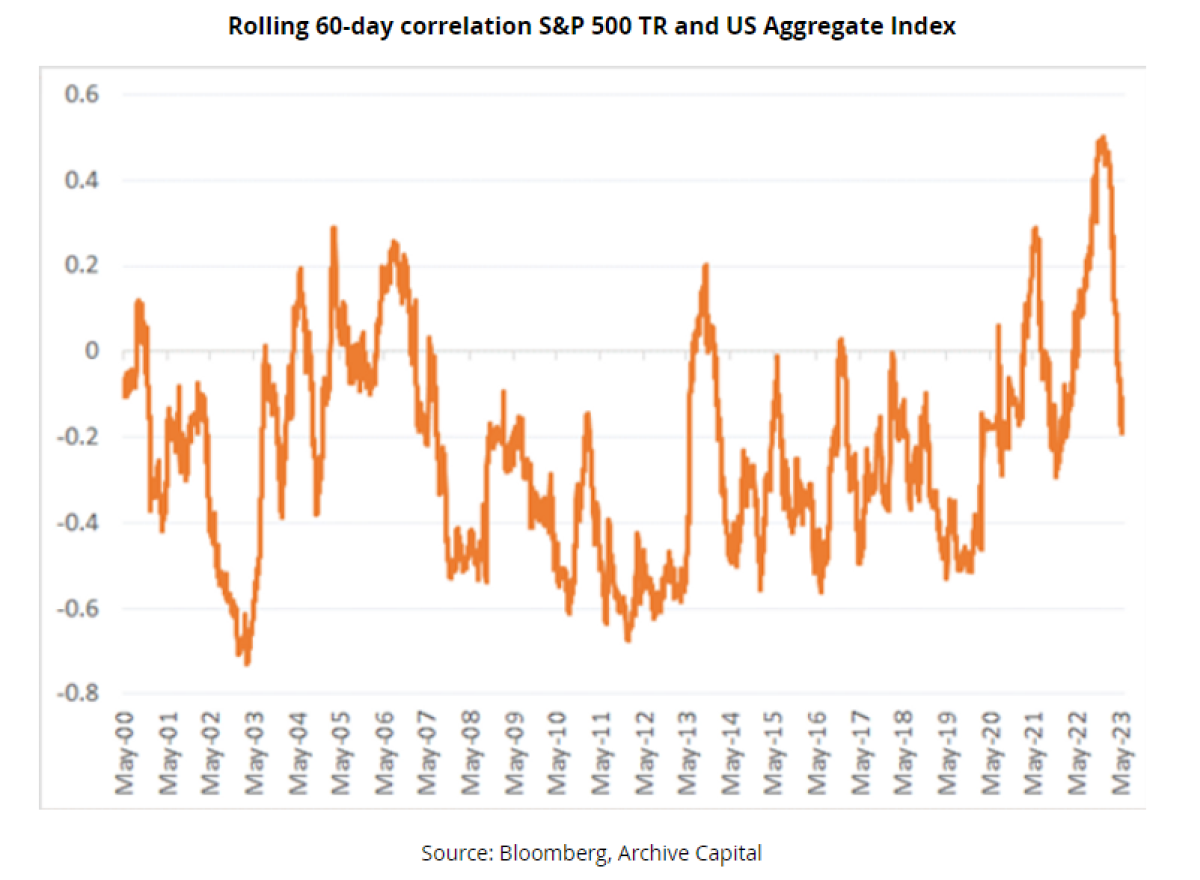

Second, the correlation between bonds and equities has turned negative, suggesting growth rather than inflation is a bigger driver of markets at the moment. Looking back in history equities and bonds were positively correlated for long periods prior to the 1990s as inflation was the primary concern in markets. When inflation fell in the 2000s and growth become more of a concern bonds and equities became negatively correlated. That suggests should the economy go into recession there is a better chance that bonds might provide diversification to equities.

Third the realised volatility in equities and bonds has also been trending down in recent months providing an even smoother ride for 60-40 investors. The VIX and MOVE indices of implied vol also suggest investors are less concerned about major dislocations looking ahead.

At the same, the diversifying strategies like managed futures and global macro are generally close to flat on the year. Investors are prone to myopia and may already be forgetting the enormous diversification value such strategies brought to traditional portfolios last year.

There is often a tendency to extrapolate recent positive news (of declining inflation, solid growth and rising equities) and assume it can continue indefinitely However, there remain many reasons for caution and in turn for maintaining meaningful allocations to diversifying strategies.

Only last August when global central bankers met at Jackson Hole all of the talk was of long-term structural challenges of de-globalization, resource constraints, constrained aggregate supply and even of a more volatile environment.

Stacked up against the potential positive of AI there remain a long list of risk factors for the global economy such as:

-

Spending on green technology risks keeping aggregate demand elevated and inflation above target over time

-

Deglobalization/nearshoring raising costs and keeping inflation elevated

-

Geopolitical risk in relation to the current trend of disengagement between the US and China

-

Financial stability risks from exposure to commercial real estate

-

Disruptions to crops and food prices as we move into El Nino

Meanwhile, valuations still look challenging for the 60-40 portfolio. Although the fall in equities last year has taken the froth off equity valuations in absolute terms relative to bonds (and particularly relative to cash) equities still look expensive.

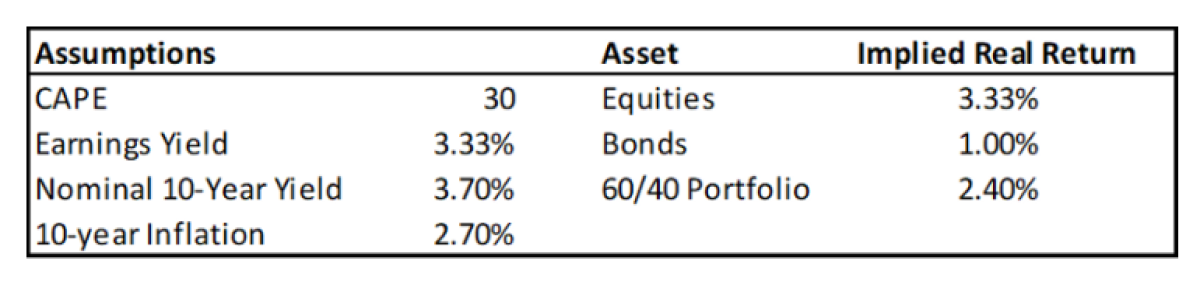

Based on 2023 earnings estimates the price-earnings ratio for the S&P 500 is close to 20. However, Robert Shiller’s longer-term Cyclically Adjusted Price Earnings (CAPE) measure, which smooths out fluctuations in earnings, is just under 30 or a 3.4% earnings yield. That is a real yield as earnings will grow with inflation but it is still at the lower end of the longer-term historical range.

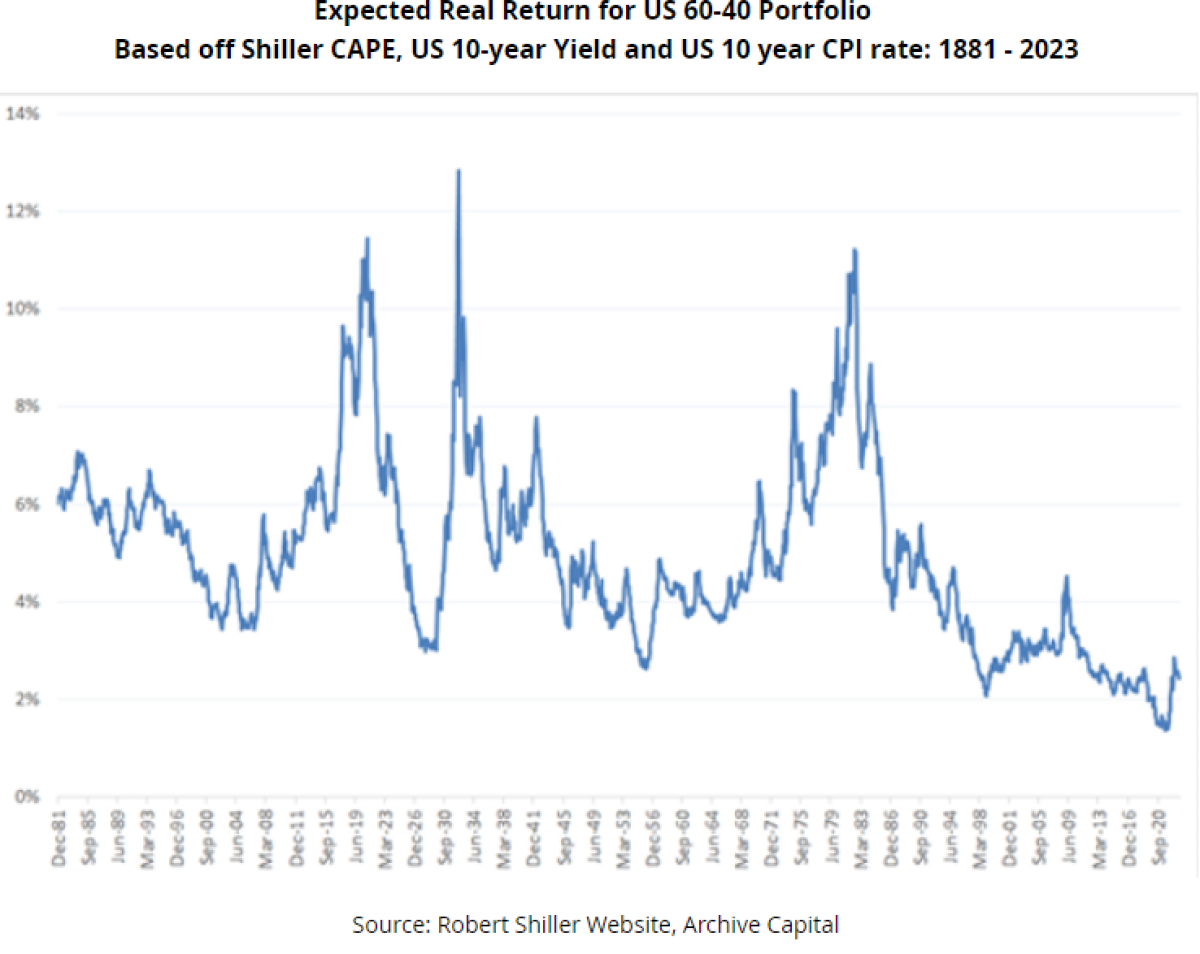

Combining, the equities CAPE of 30 with current 10-year yields of 3.7% and 2% inflation gives a 10-year expected real return of 2.7% for the US 60-40 portfolio. It seems reasonable to expect that inflation might be higher than 2.0% over the next decade. Even if CPI averages the same as the last decade (2.7%), that would push the real expected return on the US 60-40 portfolio down to 2.4%, not as low as prospective returns in 2021 but at the very low end of the range of the last 140 years.

How that scenario might play out could be something like the 1966 to 1982 period when equities were broadly flat but experienced a number of bear market episodes (1966, 1969/70, 1973/74, 1977, 1981) and a number of significant rallies, similar to what technology stocks are currently experiencing. No doubt at each peak in the rally there was optimism that equities were resuming the longer-term bull market.

Given that fundamental backdrop, the case for alternatives and diversifying strategies remains strong notwithstanding more muted performance in 2023. A number of hedge fund strategies such as managed futures and global macro benefit directly from higher interest rates as they trade on margin.

Whereas in early 2022 the case for allocating to diversifying strategies largely reflected the very low bond yields and large downside risk in bonds, the case now reflects still elevated valuations in equities, and the risk of more challenging trade-offs for policymakers trying to steer the global economy towards a soft landing.

Conclusion

The global economy has confounded the pessimists this year and may continue to do so in the near term as the transmission mechanism of monetary policy remains blunted by repercussions of COVID on balance sheets and investment behaviour.

Interest rates may indeed have to go higher and be kept there longer to reduce demand and bring inflation back to target.

That raises the risk further out of a nonlinear response to higher rates at some point, particularly once the excess savings in the system have diminished.

From a longer-term asset allocation perspective, although the last three quarters have seen the 60-40 portfolio bounce back, both valuation and macroeconomic factors point to a strong value in maintaining meaningful allocations to alternatives and diversifying strategies.

About the Author:

Alan Dunne is the Founder and CEO of Archive Capital. Prior to founding Archive Capital, he was Managing Director and a member of the investment committee at Abbey Capital. In total, he has worked in the financial markets for over 25 years at hedge funds and investment banks as a CIO, hedge fund allocator, macro strategist, and technical analyst.

About Archive Capital

Archive Capital is a boutique alternative investments and investment research firm focused on the use of global macro and managed futures strategies in asset allocation. We work with investors looking to source, evaluate and allocate to liquid alternative diversifying strategies.

This information and commentary is of a general nature for information and education purposes. It is not to be used or considered as a recommendation to buy, hold or sell any securities or other financial instruments; and does not constitute an investment recommendation or investment advice. Any investment decision should be based on appropriate professional advice specific to your needs.