By Donald A. Steinbrugge, CFA – Founder and CEO, Agecroft Partners.

The hedge fund industry’s performance has been underwhelming thus far in 2023. The HFRI Index shows year-to-date returns through May of only +1.25%, and most strategies’ returns range between -2.5% to +3.5% YTD. However, one bright spot within the industry has been ILS, or property catastrophe risk reinsurance, where the Eureka ILS Advisor Index in USD is up +5.95% through May. This marks the strongest start of a year for the ILS index since 2007. It also highlights the minimal correlation between reinsurance strategies and both equity and fixed income markets. Uncorrelated strategies reduce overall portfolio volatility which is why many of the largest pensions, endowments, and sovereign wealth funds have allocations to ILS.

What makes the strong start to the year even more compelling is that the outperformance by reinsurance, as compared to most others, only tells a part of the story. Performance is influenced by adding premiums collected, plus interest earned on collateral and subtracting claims paid and expenses. Premiums are allocated to the fund net asset value (NAV) based on when the fund assumes risk. Since the majority of risk in most ILS funds comes from US hurricanes, a substantial portion of premiums and historical returns in the industry are realized during the second half of the year, following the June/July renewal cycle. Consequently, many industry experts believe that the top reinsurance funds could potentially generate high double-digit returns for 2023, assuming an average hurricane season.

The significant increase in premiums can be attributed to both a reduction in supply and an increase in demand for reinsurance. The supply was reduced due to losses sustained by hurricane Ian and the capital markets selloff in 2022, which weakened many publicly traded reinsurers’ balance sheets. Although margins have expanded rapidly, there have been no new start-ups/entrants into the market, and only modest capital flows into reinsurance funds compared to the supply gap of $65 billion. In addition to supply being down, demand is up due to consumer inflation running at 5-8% over the past year. This has created a substantial supply/demand imbalance within the industry. The chart below draws comparisons between the decline in supply in 2022 to those that occurred in 2008 and 2001 which were years followed by material premium increases.

Additionally, reinsurance funds are required to fully reserve capital for all risks taken in their portfolios. Many reinsurance funds invest this collateral into short-term fixed income securities and have benefited from substantial yield increases. For example, in the beginning of 2022, the 6 month treasury was close to zero, whereas today it is above 5%. This excess yield acts as a significant tailwind for reinsurance performance. For funds that have performance hurdles based on short term rates, most of the excess investment returns go directly to investors.

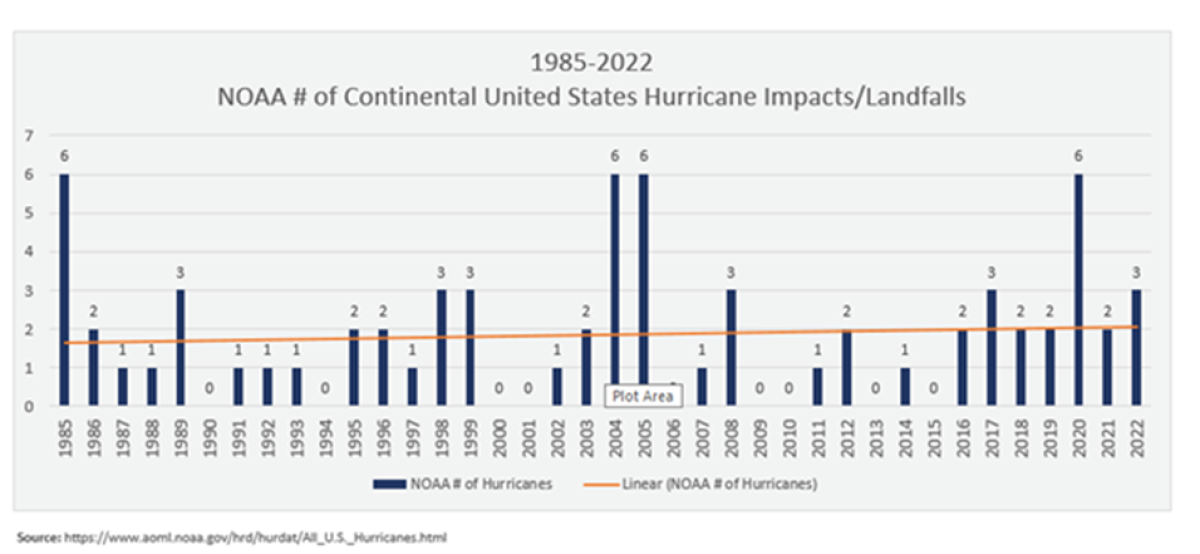

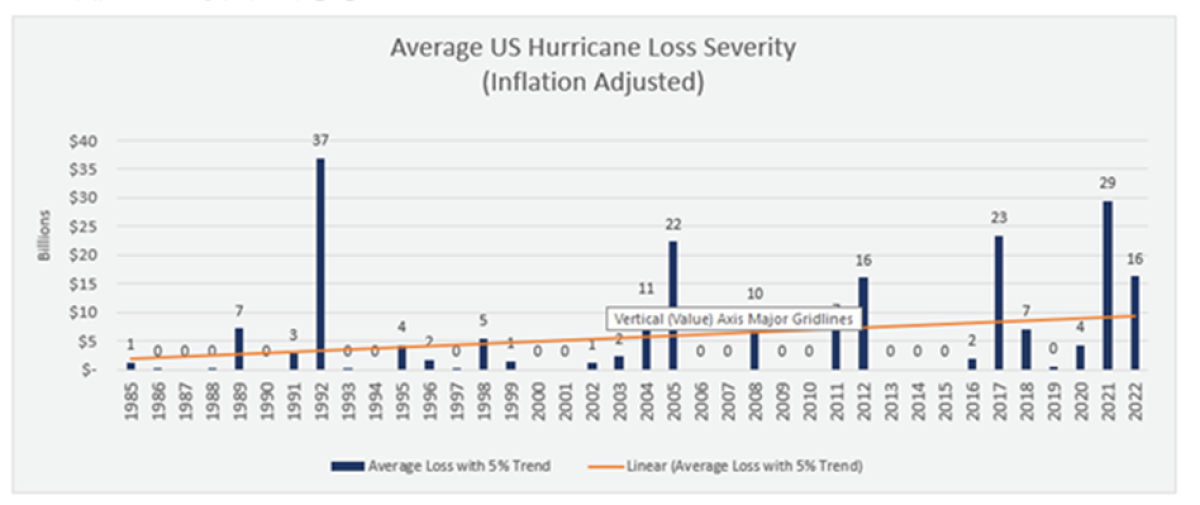

Some investors have hesitated to invest in reinsurance due to potentially unfounded concerns surrounding the impact of global warming on the industry. However, historical data indicates that the number of hurricanes and inflation-adjusted losses from hurricanes have remained relatively consistent over time.

While there has been a slight increase in dollar losses, some industry leaders attribute this to the rise in lawsuit activity. Part of these litigation costs are expected to decline as recent legislation in the state of Florida makes it more challenging for people to sue, aiming to curb the soaring cost of homeowners' insurance within the state. Furthermore, the vast majority of reinsurance deals are one-year private agreements, enabling industry participants to reassess risk annually and re-price transactions accordingly.

One factor that is likely to keep reinsurance pricing high for the foreseeable future is the strategy's underperformance over the past few years, when pricing was lower and the industry experienced higher-than-average hurricane activity. This performance history has dissuaded some investors from allocating capital. Many investors tend to avoid strategies that have not performed well in the recent past, rather than considering current valuations and future potential.

It is not easy to differentiate performance among reinsurance funds during long periods without a major event as was the case form 2013 through 2016. However, over the past few years, the industry has experienced a number of severe events which have caused relative performance among funds to widen dramatically. Performance during down years for the industry provides a good stress test to determine which reinsurance funds actually have good risk controls. How funds performed during these periods relative to expectations is important to consider when determining the potential funds to which one should allocate.

What are some other things to consider before investing in a property catastrophe reinsurance fund?

Organizations: The organization should be of institutional quality with appropriate staffing.

Investment team: Reinsurance is a relationship oriented industry. Reinsurance companies should have depth of investment team and also long tenure in the industry.

Areas of Focus: There are different ways of participating in the market whose relative risk/reward changes over time. Firms should have expertise and flexibility to maximize risk/reward across a broad spectrum of the market including Traditional Reinsurance, Retro, Industry Loss Warranties (ILW’s), Catastrophe Bonds, a hedging program, and potentially individual risk, without reliance on any one subsection.

Volume of deal flow: It is very difficult to generate a large amount of deal flow in the reinsurance space. To access the deal flow, firms must have relationships with regional insurance brokerage offices. Developing relationships across the extensive geographical landscape of the reinsurance industry takes an enormous amount of time and effort. However, the more regional relationships a firm is able to develop and, subsequently, the more deals they are able to see, the more inefficiencies in the market they can potentially identify.

Proprietary analytics: Most reinsurance firms use the same weather models and datasets that can be purchased from the scientific community. To develop an edge, reinsurance firms must develop proprietary overlays to refine and enhance the models as they pertain to specific perils and/or geographies. A large portion of alpha can be generated through improved accuracy of the risk assessment compared to the off-the-shelf models.

Risk controls: Risk control is extremely important in any reinsurance portfolio. One way to implement this control is to build a portfolio that maximizes the Omega Score. While Sharpe Ratio can be appropriately applied to instruments that have high liquidity, are easily tradeable, and have outcomes with normal or near-normal distributions, Omega Score is a more effective way to evaluate risk for the ‘fat-tail’ return distributions found in reinsurance.

About the Author:

Donald A. Steinbrugge, CFA is the Founder and CEO of Agecroft Partners, a global hedge fund consulting and marketing firm. Hedgeweek and/or HFM have selected Agecroft Partners 13 years in a row as the Hedge Fund Marketing Firm of the Year.

Don frequently writes white papers on trends he sees in the hedge fund industry. He has spoken at over 100 Alternative Investment conferences, been quoted in hundreds of articles relative to the hedge fund industry, has done over 100 interviews on business television and radio and has over 25,000 subscribers to his Hedge Fund Industry Insights Newsletter.

Don is also the Founder of Gaining the Edge LLC that runs the Hedge Fund Educational Webinar Series, which has had over 7,000 unique alternative investment industry participants, an annual Hedge Fund Leadership Conference, which sold out all 6 of its events, and the Alternative Investment Cap Intro Events. Most revenue from these events are donated to charities that benefit at risk children, which have total over $2.7 million donated since 2013.

Before Agecroft, Don was a founding principal of Andor Capital Management where he was a member of the firm’s Operating Committee. When he left Andor, the firm ranked as the 2nd largest hedge fund firm in the world. Before Andor, Don was Head of Institutional Sales for Merrill Lynch Investment Managers (now part of Blackrock). At that time, MLIM ranked as one of the largest investment managers in the world. Previously, Don was Head of Institutional Sales and on the executive committee for NationsBank Investment Management (now Bank of America).

Don is a member of the Board of Directors of Help for Children (Hedge Funds Care) and the Virginia Home for Boys and Girls Foundation. In addition, he is a former Board of Directors member of the University of Richmond’s Robins School of Business, The Science Museum of Virginia Endowment Fund, The Richmond Ballet (The State Ballet of Virginia), Lewis Ginter Botanical Gardens, Child Savers Foundation, The Hedge Fund Association and the Richmond Sports Backers. He also served over a decade on the Investment Committee for The City of Richmond Retirement System.