By Bo Trant, Director, and Tim Wolak, Senior Associate, of Barings’ Structured Credit Investment Group.

Despite generating attractive returns with low default rates for more than a quarter century, CLOs are still a commonly misunderstood asset class.

Collateralized loan obligations (CLOs) have existed since the 1990s, but misconceptions surrounding the asset class persist. We present the following to help better understand this intriguing market segment and to separate fact from fiction.

Fiction:

CLOs are the same as CDOs and caused the financial crisis.

Fact:

Collateralized debt obligations (CDOs) is the broad term that describes a type of structured finance security that can be backed by a portfolio of various forms of debt including corporate loans and bonds. However, most people are aware of the CDOs that are backed by subprime residential mortgage-backed securities (RMBS). In the buildup to the Global Financial Crisis (GFC), subprime residential mortgages often had little or no documentation and were poorly underwritten. When housing prices crashed during 2007–2009, these highly correlated subprime mortgages experienced massive losses, which resulted in substantial defaults in RMBS CDO portfolios. Those defaults are what bled into the broader macro environment. But RMBS CDOs are not CLOs.

CLOs are a specific type of CDO that are primarily backed by highly diverse pools of senior secured loans. These loans have historically strong recovery rates averaging over 70% for the years spanning 1987–2022, and are typically made to large well-known corporate borrowers such as United Airlines, Virgin Media, and Burger King, who provide extensive annual reporting.1 In an issuing company’s capital structure, these loans are usually senior to other outstanding debt, including high-yield bonds. These loans are also secured by some or all of a borrower’s assets, which offers additional credit risk protection.

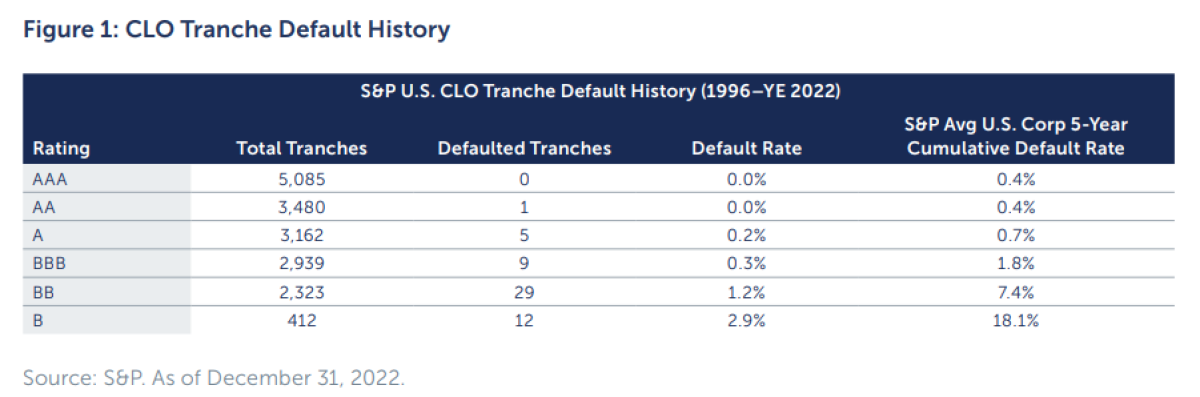

The underlying pool of loans in a CLO is actively managed by a collateral manager and the CLO vehicle contains structural enhancements that support the debt in times of distress. While CLOs experienced some volatility during the GFC, the overall default rate was incredibly low (Figure 1). In fact, out of more than 17,000 U.S. CLO tranches rated by S&P as of year-end 2022, only 56 (0.3%) have ever defaulted. Furthermore, no AAA-rated tranche has ever defaulted.

Fiction

All CLO tranches are overly complicated and incredibly risky

Fact:

Although a CLO is a more complex vehicle than a typical debt or equity investment, the nuances in the structure have historically provided investors with additional protections, which has resulted in more robust performance.2 In addition to the active management of an underlying collateral pool made up of 150–200 senior secured loans in 15–20 diversified industries, the CLO structure is sliced into a series of tranches that redistribute the risk of the underlying pool of loans. Investors seeking additional credit enhancement can invest in senior tranches, which get paid first and receive losses last in a CLO payment waterfall. At the same time, more risk-on investors seeking extra returns may look at the equity tranche, also known as the first loss piece of a CLO. The CLO equity tranche is last in line to receive proceeds. Due to this added risk, however, it has the greatest potential upside as it gets any residual proceeds generated by the assets.

Investors seeking additional credit enhancement can invest in senior tranches, which get paid first and receive losses last in a CLO payment waterfall. At the same time, more risk-on investors seeking extra returns may look at the equity tranche, also known as the first loss piece of a CLO. The CLO equity tranche is last in line to receive proceeds. Due to this added risk, however, it has the greatest potential upside as it gets any residual proceeds generated by the assets.

CLOs also benefit from coverage tests that serve as early warning triggers to divert proceeds to senior tranches in times of distress. Two typical types of coverage tests present in CLOs are the over-collateralization (OC) test and the interest coverage (IC) test. The OC test requires a specific ratio of assets to be maintained compared to the outstanding CLO debt tranches. Meanwhile, the IC test ensures that sufficient interest proceeds are generated by the underlying loans to cover the interest due to CLO debt tranches.

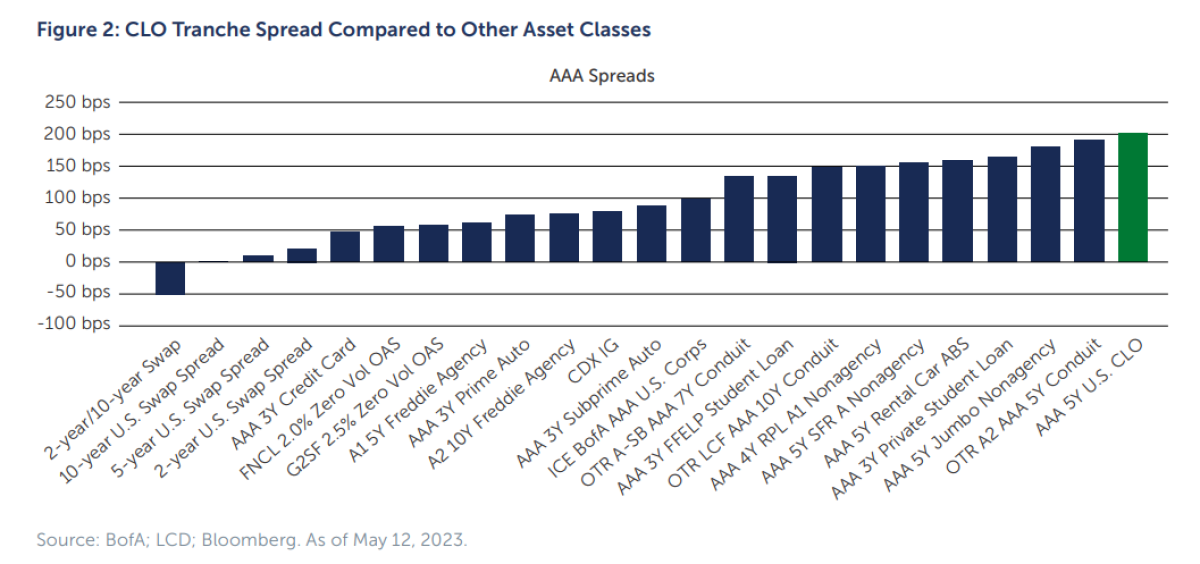

The “information premium” associated with understanding the CLO structure has helped contribute to a strong return profile compared to other similarly rated asset types.3 The AAA tranche is the safest investment in the CLO structure and currently offers a spread of around 2% plus the reference rate (typically SOFR) above 5%, resulting in an all-in coupon of about 7% (Figure 2).

Fiction:

The market for CLOs is small and illiquid.

Fact:

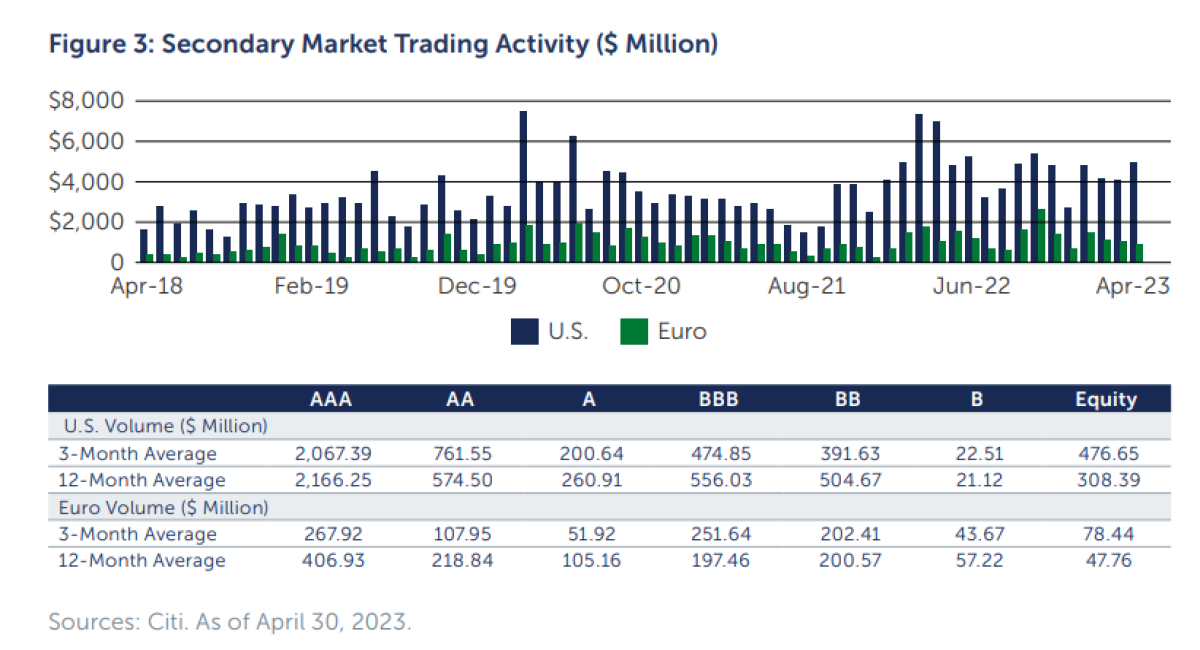

CLOs first appeared in the late 1990s, and over the subsequent quarter century, more and more market participants began to understand the benefits and subtleties of the vehicle. The CLO structure continued to evolve in the 2010s with structures that increased subordination for debt tranches, attracting even more investors. The CLO market has grown to more than $1.2 trillion globally, with a diversified base of investors comprising national and regional banks, overseas banks, insurance companies, pension funds, asset managers, hedge funds, private equity funds, and family offices.4 With an increasing number of buyers in the market for a higher yielding, diversified product that boasts structural protections, liquidity in all CLO tranches also has increased.

For the most part, CLOs are traded over the counter via a bid wanted in competition (BWIC) process. Since 2020, more than $46 billion in U.S. CLO tranches have traded annually via BWIC in the secondary market.5 This active trading has provided pricing transparency and allows investors to enter and exit the market efficiently.

To meet investor demand, more than 120 managers have issued a CLO over the past two years.6 The number of issuers provides investors with a variety of choices among CLOs. At the same time, the breadth of choice requires that investors have a comprehensive understanding of each collateral manager’s investment style, track record, and commitment to the high-yield loan market when selecting with whom best to invest.

Fiction:

CLOs issued during times of market distress have performed poorly.

Fact:

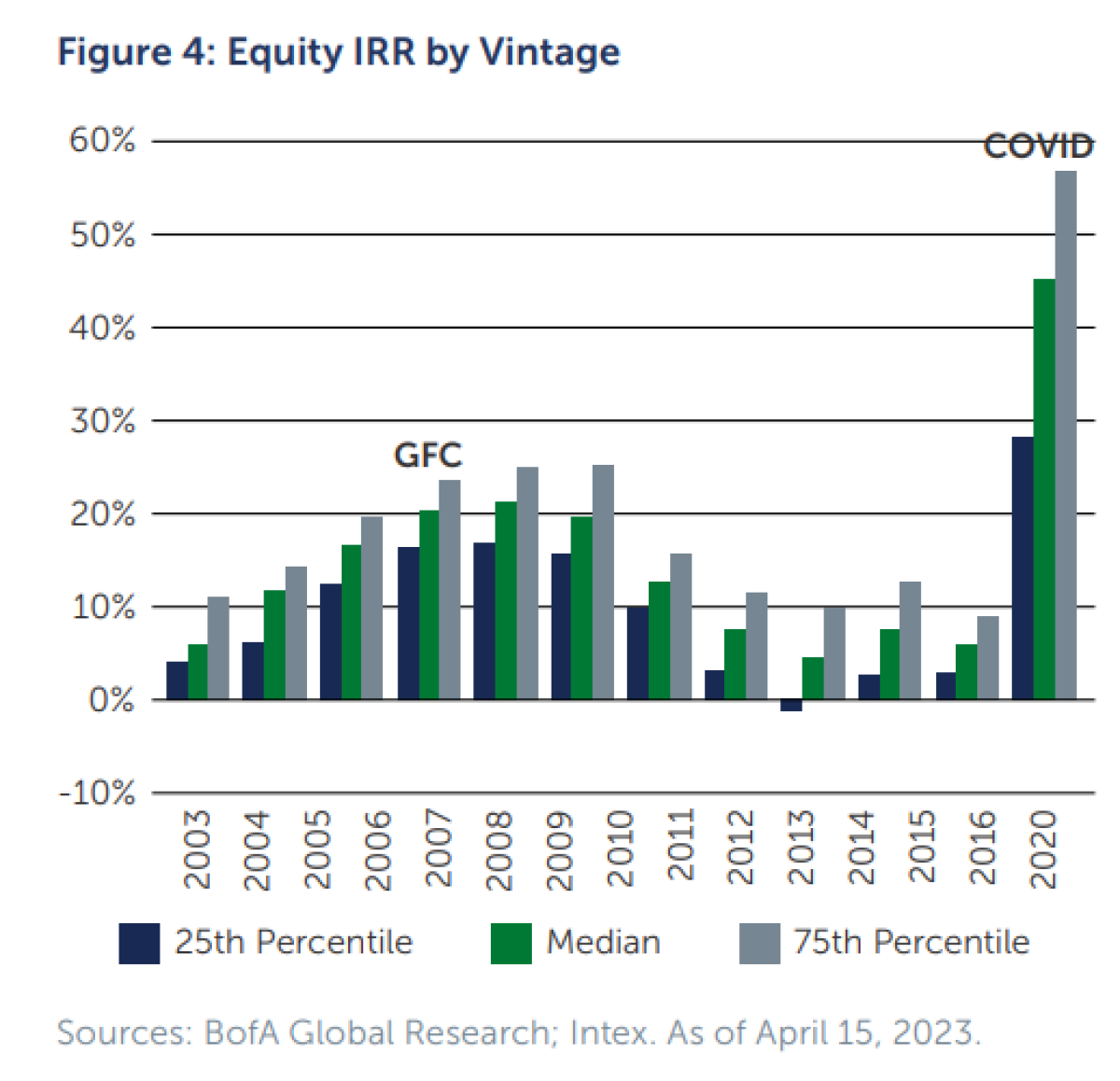

Periods of distress, such as the GFC and the Covid-19 pandemic, are associated with rising default rates and negative market sentiment. This logically results in lower prices across many asset classes, including loans. That said, CLOs issued during such times have recorded some of the most substantial equity internal rate of returns (IRRs) in history (Figure 4). Although this may seem counterintuitive at first, the logic surfaces when analyzing the CLO structure and recognizing the role of active management. The ability of collateral managers to purchase loans at discounted values in down markets has ultimately proved accretive to CLOs as they are not forced sellers or mark-to-market vehicles. Their structure allows buy-and-hold investors to benefit from the “pull to par” effect of securities bought at depressed prices that ultimately rebound.

To keep overly aggressive CLO managers from purchasing only poor performing highly discounted priced assets, the CLO governing document, called the indenture, limits how many “discount obligations” a CLO manager can hold in its portfolio. Further, it defines a “discount obligation” as anything priced below 80 cents on the dollar. This distinction requires assets purchased below 80% of par to be held at market value in the OC test, which can cause the test to trip sooner to protect senior debt investors with additional proceeds that would have otherwise gone to equity investors. Knowing how to navigate these constraints successfully during volatile periods requires an experienced manager to potentially maximize returns for debt and equity investors alike.

Takeaway

CLOs are often maligned in the media by people who have not taken the time to understand them. However, a deep dive into their history reveals that CLOs have performed strongly during the heights and depths of market cycles while offering investors robust credit enhancements, consistent liquidity, and attractive return profiles.

Barings, as a pioneer in the CLO industry, a manager of more than $25 billion in CLO tranche assets, and an issuer of 100 CLOs, is an advocate for demystifying the investment vehicle itself and the process of CLO investing.7 Our team vigorously investigates the CLO universe through a thorough qualitative and quantitative examination of a CLO manager’s investment style, a complete bottom-up analysis of the underlying loans, and an in-depth review of each CLO structure.

CLOs have offered investors a diversified product with the potential for compelling returns and protections throughout their existence. With market volatility likely on the horizon, educated investors may unearth attractive opportunities in this growing market segment.

Footnotes:

1. Source: Moody’s. As of March 13, 2023.

2. Source: S&P. As of December 31, 2022.

3. Sources: BofA; LCD; Bloomberg. As of May 12, 2023

4. Source: Citi. As of April 19, 2023.

5. Source: Citi. As of December 31, 2022.

6. Source: LCD. As of December 31, 2022

7. Source: Barings. As of June 12, 2023

About the Authors:

Bo Trant is a member of Barings’ Structured Credit Investment Team. Bo is a Client Portfolio Manager who serves as a CLO specialist and is responsible for the business development and ongoing relationship management for the Structured Credit Investment Team. Bo has worked in the industry since 2006. Prior to joining the firm in 2022, he was a Structured Credit Business and Relationship Manager at Fitch Ratings. Prior to that, he was a senior CLO and CDO analyst at S&P Global Ratings. Bo holds a B.S. in Quantitative Finance from James Madison University and an M.B.A. from Columbia Business School.

Tim Wolak is a member of Barings’ Structured Credit Investment Group. Tim is an investment specialist, responsible for new product development, marketing and servicing existing strategies. He has worked in the industry since 2019 with experience in investment management. Prior to joining the firm in 2022, Tim was an investment analyst at AJ Wealth, a wealth management firm in Manhattan, NY. He holds a B.S. in Finance from Lehigh University.

Barings is a $362+ billion* global investment manager sourcing differentiated opportunities and building long-term portfolios across public and private fixed income, real estate and specialist equity markets. With investment professionals based in North America, Europe and Asia Pacific, the firm, a subsidiary of MassMutual, aims to serve its clients, communities and employees, and is committed to sustainable practices and responsible investment.