By Joe Elmlinger, Head of Client Solutions and Alex DeFeo, Senior Portfolio Manager at Lake Hill.

The VIX Index reached recent lows this past month at 12.73 prompting some to ask if this means the stock market is in a new volatility regime. There are several quantitative and qualitative techniques to help determine if there has been a structural change in the volatility market, but as with all analytical methods, the results are never certain.

The current levels of implied volatility are below the long-term average. Will the regime persist, or is it fleeting?

The answer is YES. It can stay low. It might revert to higher levels.

The YES answer is not meant to be flippant. It is intentionally ambiguous because it does not matter to us. The current low level of implied volatility does not mean there is less opportunity or less risk. Indeed, it is this ambiguity that in large part keeps the options market active. Insurance markets - which are similar to the options markets - can provide some insight into the current implied volatility environment in equities.

What if an insurance company could perfectly predict the future? Imagine that it knows precisely how many houses will burn down or how many cars will be in fender benders next year. Even if every insurance company had this perfect information, they would still lack a key piece of information. They would not know exactly when the events will happen. It is the uncertainty in timing that drives the insurance industry and the options market – even though the basic odds are known with a high degree of certainty.

Similarly, if an investor knew with certainty that the VIX would realize 13 over the next year, that doesn’t prevent the equity market from rallying or declining 20% from here. It simply means that the price of insurance to cover that risk is cheaper now than it was a year ago.

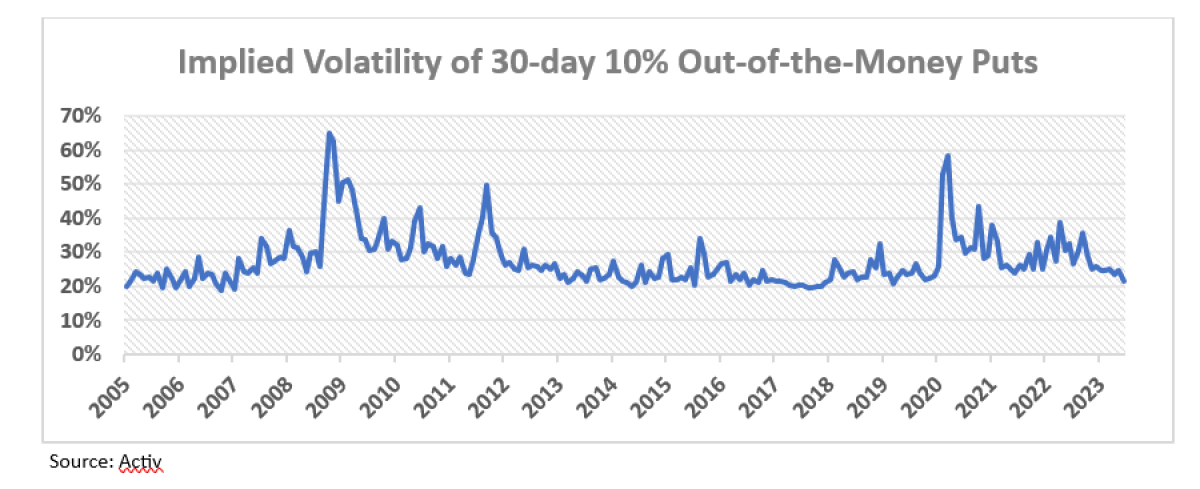

The price of stock market insurance is indeed back to levels last seen before the pandemic. The 10% out-of-the-money puts that expire in 30 days are offered at around 21% implied volatility. That is the lowest level since 2019, and it seems cheap by almost any historical measure. This level of “cheapness” was the status quo from 2012-2019 until suddenly it wasn’t, and the VIX spiked to 60.

The difficulty with simply buying out-of-the-money puts, even if they are cheap, is that they are still more likely than not to expire worthless. In fact, there is less than a 5% chance that 10% OTM 30-day puts generate a positive payoff. This reality is no different than if one was able to buy homeowners insurance for a cheap price. The chances that your house will burn to the ground are still extremely low.

Just because it is cheap or expensive doesn't necessarily change the odds of your house burning down.

The odds may not have changed.

That said, given the recent rally in equities coupled with the relative cheapness of insurance, it could seem like the obvious choice to start a simplistic put buying program. At Lake Hill, we take it a step further and use our “Engine” to determine which options are overvalued and undervalued at any given moment. Despite the graph we show above, we are currently both buying and selling OTM puts. YES, some are undervalued, and we are buying them. YES, some OTM puts are overvalued on a relative basis, and we are selling them. YES, we could make money either selling or buying the same option contract. The reason for this ambiguity is because a particular put option position may free up risk in another area of the portfolio which may be a significant return driver for the overall portfolio.

The key is to have a disciplined plan for finding the best insurance (options) to purchase while dynamically adjusting the position with other offsetting positions to have a program in place that both monetizes and adapts continuously as market conditions change.

About the Authors:

Joe Elmlinger is Head of Client Solutions at Lake Hill. For over thirty years, Joe has been a pioneer in derivatives sales and is recognized as a leader in equity derivatives, structured products, and customized financial engineering for clients. Previously Mr. Elmlinger was Head of Sales for Equities & Derivatives at Société Générale. Mr. Elmlinger spent the majority of his career at Citigroup and its predecessor, Salomon Brothers, as Global Head of Equity Derivatives. He has also held senior roles at Bankers Trust Company, Merrill Lynch, the Board of Directors of ISDA and The Options Clearing Corporation.

He has a B.A. from the University of Vermont and an M.B.A. from Stanford University.

Alex DeFeo is a Senior Portfolio Manager at Lake Hill with a finance career spanning more than two decades. Prior to joining Lake Hill, he was a Senior Portfolio Manager at Goldman Sachs where he focused on Alternative Risk Premia and Volatility Strategies. He has also held senior positions at Credit Suisse, where he served as the Head Trader and Portfolio Manager for the Alternative Beta Strategies group and at Bank of America.

Alex has been a guest lecturer at the London School of Economics and an instructor at UC Berkeley. Some of his research has been funded by the US Army, Department of Defense, and the National Science Foundation.

Alex earned an M.S. in Mechanical Engineering from the University of California, Berkeley and a B.S. in Mechanical Engineering from the Massachusetts Institute of Technology.