By Alex Botte, CFA, CAIA, Head of Client and Portfolio Solutions at Runa Digital Assets, an investment firm specializing in digital asset portfolios.

Key Points

- The evidence points to an imperfect relationship between blockchain fundamentals and future token returns. Most of the time there is no evidence that fundamentals impact future returns (and vice versa).

- This loose, complicated relationship with fundamentals might mean that we as an industry are not yet ready for fundamentals-based asset pricing models, risk models, and factor-based portfolios.

- Fundamentals can be a way to understand blockchain adoption, but they should be only one part of a broader set of metrics and considerations to take into account before investing in a blockchain’s native token.

- We expect this relationship between fundamentals and future token returns to change over time.

Introduction

“It’s always sunny in San Diego… It pretty much never rains.” This is what I’ve been told, and aligns with what I mostly remember of the weather when I grew up in the southern California city. But this certainly hasn’t held true for 2023 so far. Through mid-March San Diego measured 9.11 inches of rainfall, which is notably more than was measured for all of 2022 (5.90 inches).

Recently my friends and I were discussing what this meant for the wildfire season. My expectation was that more rainfall would dampen the impact of fires later in the year. The thought process was that the ground would still be wet from all the rain and therefore hard for fires to catch. My friend told me it was the opposite - fires would likely be more pervasive since all the rain meant plentiful brush and vegetation growth - thick and tall and flammable.

This unexpected result had me wondering about another cause and effect relationship I had been pondering: do fundamentals drive returns in digital asset markets? Fundamentals are absolutely key to understanding valuations of traditional assets like stocks and bonds. But given the virality, narratives, sentiment shifts, and speculation in crypto markets, how important were fundamentals to token prices? Was it possible the relationship was in fact reversed? Crypto markets can be reflexive in that way - when a token pumps, more people start to pay attention to it, and perhaps that leads to more on-chain activity in that token’s blockchain.

I gathered the data and set off to answer these questions.

Do Stronger Blockchain Fundamentals Lead to Higher Future Returns for Tokens?

Yes, blockchains have fundamentals. In this analysis we’ll focus on four of them, which were all sourced from Artemis:

- Fees: Fees paid by the blockchain’s users

- Total Value Locked (or TVL): Crypto native measure of the value of funds locked into the blockchain's smart contracts

- Daily Transactions: The number of transactions registered on-chain in a 24 hour period

- Daily Active Addresses: The number of unique wallet addresses sending an on-chain transaction in a 24 hour period

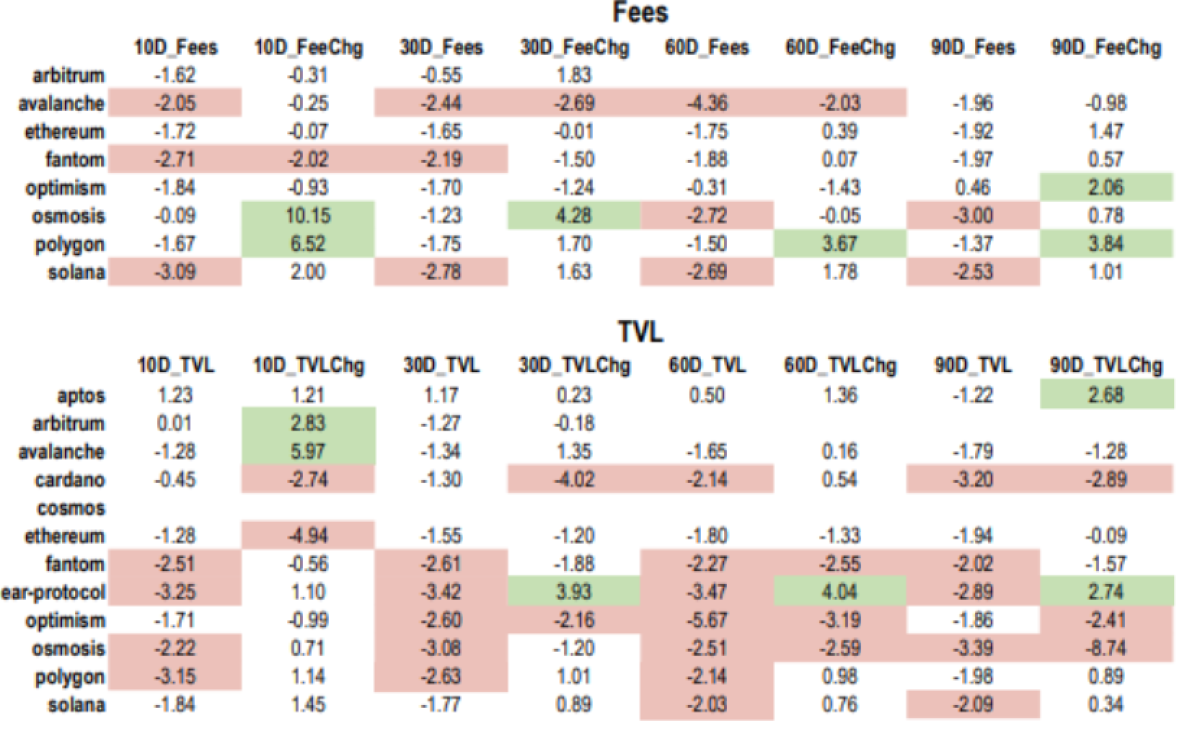

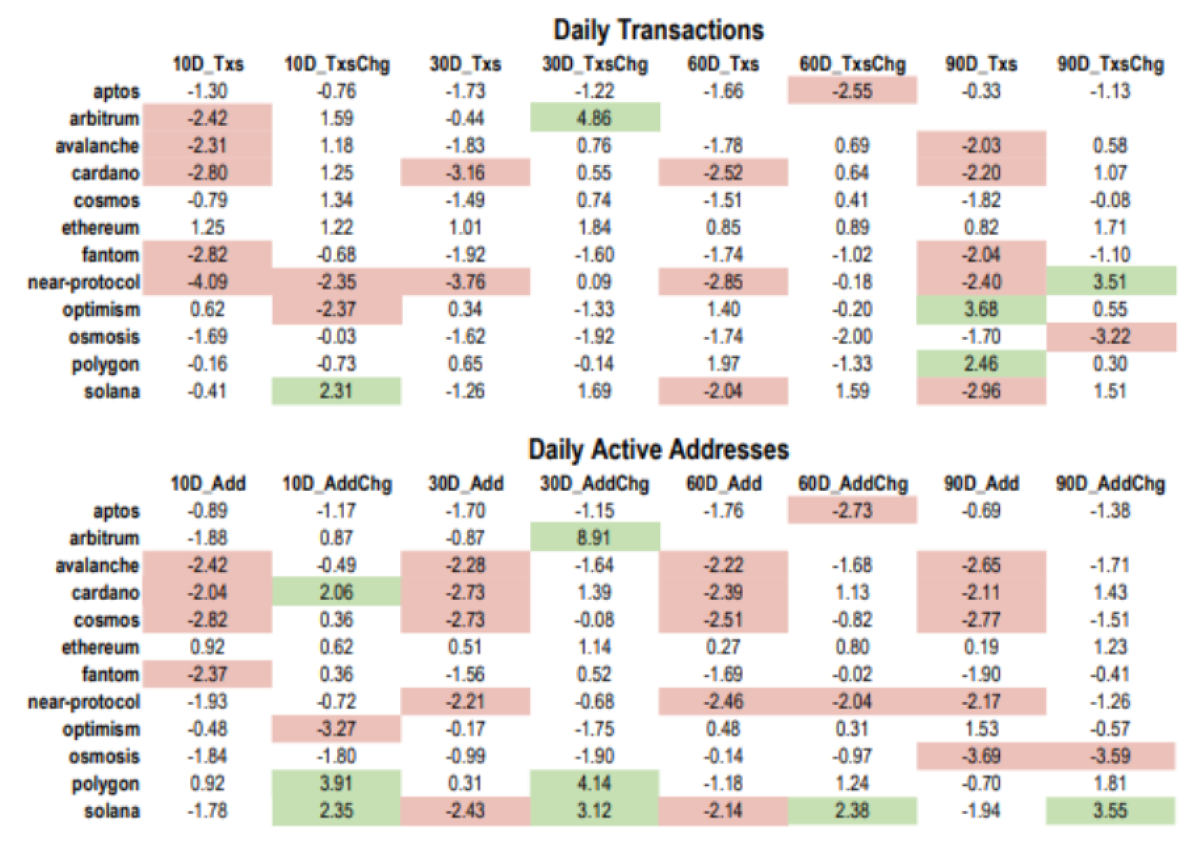

We collected this data for all blockchains with a relatively long history available on Artemis. We then used this fundamental data (both the level and the 30 day change) as the independent variable in a collection of univariate regressions to predict the dependent variable, which was future 10, 30, 60, and 90 day returns of that blockchain’s native token. The price data to calculate returns was sourced from Messari. The regressions needed to have at least 30 observations to run, but most had much more than that. Here are the coefficient t-statistics of those regressions. We highlighted in green/red any that were positively/negatively statistically significant.

Quick example to help with interpretation: The green 10.15 value in the top table for Osmosis’ 10D_FeeChg means that there was a positive significant relationship between the past 30 day change in fees paid by users of the Osmosis blockchain and future 10 day returns of the OSMO token.

If fundamentals undoubtedly mattered to future token returns, we would expect to see more green in the tables above. But most of the time there is no evidence that fundamentals impact future returns. There were more negative results than positive results, meaning if past fundamentals were strong, that meant lower future returns. Of the significant positive results, all but two were using the change in fundamentals to predict future token prices, perhaps suggesting that momentum in fundamentals is a more relevant measure to consider versus just the level of the fundamental metric.

In terms of the fundamental measures themselves, TVL appeared to have the strongest relationship with future returns. And then in terms of the blockchains, Near Protocol, followed by Cardano, were the two networks where fundamentals mattered most to future token returns. Ethereum the least.

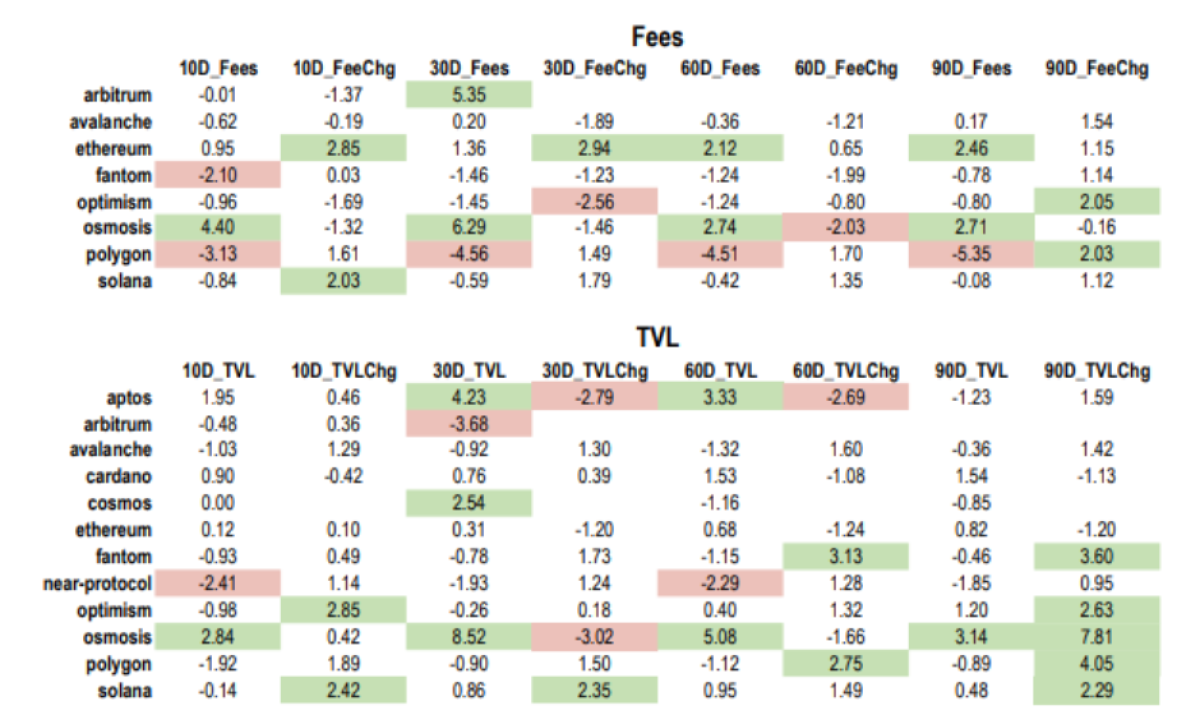

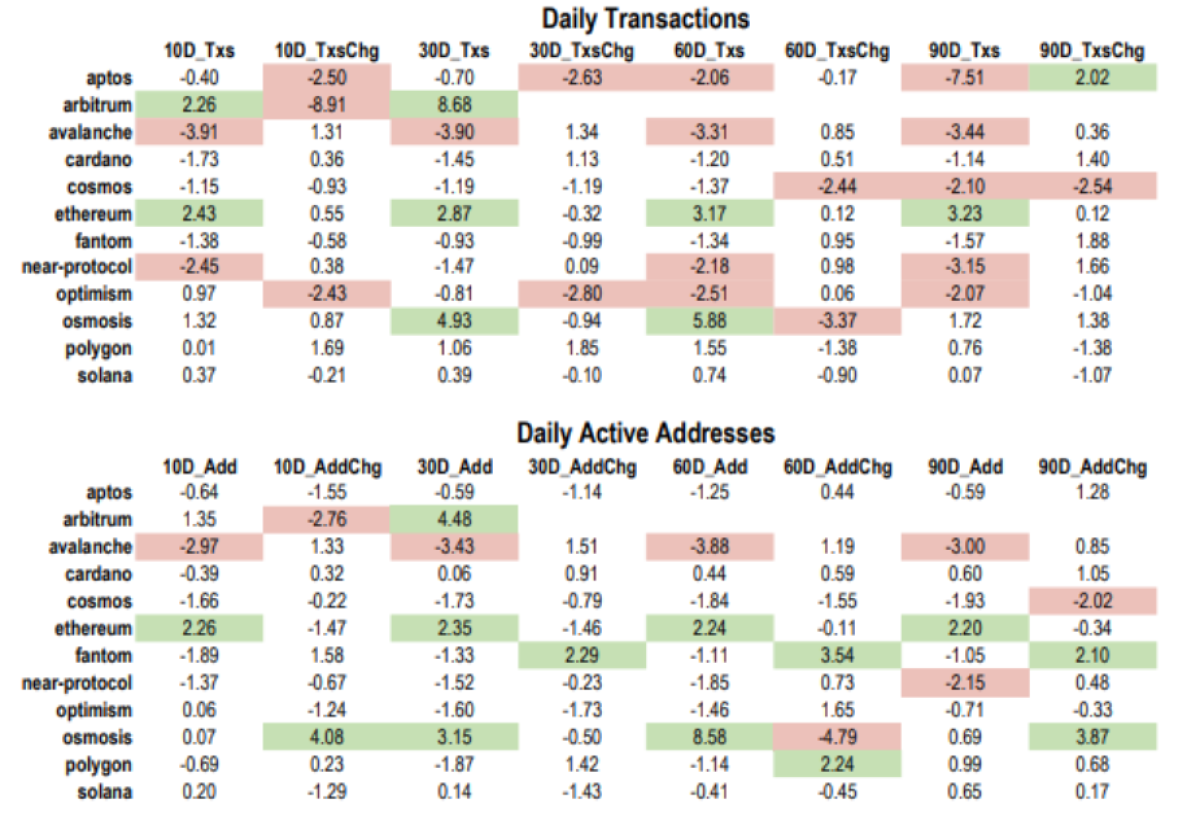

Next, let’s flip the equation and see if a token’s past returns meant stronger future fundamentals. We use the past 10, 30, 60, and 90 day returns in the blockchain’s native token to predict the level of the fundamental metrics as well as its future 30 day change. A few ex-ante ideas here: (1) markets are forward-looking and anticipate future blockchain developments and activity, (2) if a token outperforms, it may attract attention which could lead to higher on-chain activity, and/or (3) in theory the blockchain, which could hold its native token in its treasury, would have more resources to spend on developing the protocol or incentivizing people to use their blockchain if their token recently appreciated.

Similar to the tests before, most of the time there is no evidence that past returns impact fundamentals. But, unlike the tests before, there were more positive results out of those that were significant. From a fundamentals standpoint, past returns appeared to have the strongest relationship with fees. And from a blockchain standpoint, Osmosis and Arbitrum were the two networks where past returns mattered most to future fundamentals. Cardano the least, which is interesting because Cardano was one of the networks where fundamentals mattered most to future returns.

Conclusion: What Are the Investment Implications?

The evidence above points to an imperfect relationship between blockchain fundamentals and future token returns. Intuitively we know that blockchain fundamentals tell us about adoption, which is key since network effects are so important for this technology. But we also know that there is much more at play that drives digital asset prices.

In 2022, macro was a major driver since crypto was impacted by some of the same things impacting traditional markets, including rate hikes to combat rising inflation. In 2023, the attention has shifted to regulation. Sentiment and virality are additional important factors to consider (think PEPE’s and Bitcoin Ordinals’ meteoric rises this year).

I think this loose, complicated relationship with fundamentals might mean that we as an industry are not yet ready for fundamentals-based asset pricing models, risk models, and factor-based portfolios. We do think fundamentals are still important to monitor - to understand adoption like we mentioned earlier, to understand staying power (a network that is relatively well established is hard to wipe out - think Solana post-FTX), etc. But it should be only one part of a broader set of metrics and considerations to take into account before investing in a project.

Unlike rain’s relationship with fires, we expect this relationship between fundamentals and future token returns to change as the asset class matures, fundamentals are appreciated more broadly, and there are clearer connections between on-chain activity and token value accrual.

Footnotes:

[2] Example source: https://www.cbsnews.com/sacramento/news/record-rain-could-mean-a-higher-risk-for-fires-this-year/

[3) T-statistics with an absolute value above 2 are considered to be statistically significant.

[4] Note that Fees and TVL are measured in USD here. We also converted these fundamentals to be denominated in the blockchain’s native token, and it made no material impact on the results.

About the Author:

Alex Botte, CFA, CAIA, is responsible for the investment risk framework, chairs the Risk Committee, and contributes to content, portfolio analytics, research, and client engagement. Alex was previously a Vice President at Two Sigma, where she produced investment management-related content and helped with the development of the firm's factor-based risk analytics platform, Venn. Prior to Two Sigma, she was at AQR Capital Management, where she most recently served as a Product Specialist for the firm’s Global Asset Allocation strategies. Prior to AQR, she worked in Prime Services at Barclays. Alex holds a Bachelor’s of Science in Applied Economics and Management from Cornell University.