By the STANDARDS BOARD FOR ALTERNATIVE INVESTMENTS (SBAI).

Short Selling and Responsible Investment

There is much debate in the alternative investment industry about the role of short selling in responsible investment in general and specifically in net zero frameworks. In this thought piece we discuss the importance of short selling in the transition to a low carbon environment and suggest how it should be accounted for in net zero frameworks.

At the SBAI, our work in Responsible Investment is deliberately not prescriptive on the implementation of Responsible Investment at individual asset managers and institutional investors. We believe there are many ways of approaching this to meet different objectives.

We believe that short selling is an important tool aiding price discovery and efficient markets and laid out our reasoning for this in a previous thought piece “Gamestop and Short Selling”. In this thought piece we specifically talk about the role of short selling in responsible investment.

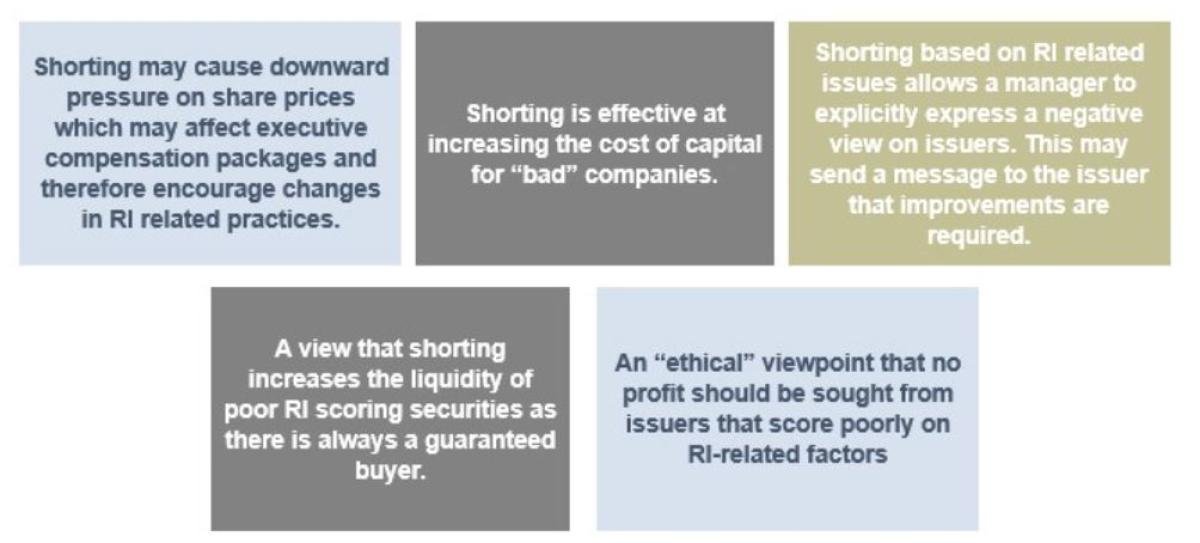

Short Selling and Responsible Investment in General

As with any responsible investment tool, careful thought needs to be given to the objective of the portfolio and the philosophy of both the asset manager and the institutional investors. Through discussions in our Responsible Investment Working Group, we have encountered a range of views on the use of short positions in responsible investment including (in no particular order):

You can read more on the conversations that asset managers and allocators should be having when discussing approaches to responsible investment in our Toolbox Memo on Implementation of RI in ELS Strategies.

Short Selling and Net Zero

The starting point for any net zero discussion is to understand what carbon emissions we are discussing. In this case, we are looking at the emissions from the universe of all issued stocks and bonds i.e., the carbon exposure of the market portfolio.

We believe there are many ways alternative investment strategies can influence the reduction of these emissions including supplying new capital to low-carbon companies, engagement and stewardship on carbon-related issues, and influencing the market price of companies with different carbon intensities.

The third point above, influencing the market price of companies, is an important one and often neglected when discussing net zero frameworks. Supplying new capital and engagement can typically only be achieved with a sub-set of instruments – IPOs and secondary offerings provide new capital and long-only equity positions provide the best opportunities for engagement. Market price influence, however, can be effective with a range of instruments – including derivatives and short positions.

Which type of influence a portfolio may exert is linked to its actions defined by the instruments traded which are linked to the objectives of the portfolio or the investor. Through our Responsible Investment Working Group discussions we have identified at least three ways that investors think about carbon in portfolios:

It is broadly accepted that short positions can be netted against long positions when assessing the risk exposure to carbon. There is more debate, however, when it comes to looking at carbon emissions from a net zero perspective.

We believe that short selling influences the market price of companies in a similar way to selling or divesting from an asset. Short selling can also be used in broader ways to influence the transition to net zero such as:

- Allowing a manager to explicitly express a negative view on issuers for carbon-related policies. This may send a message to issuers that improvements are required either through short activism or public disclosure of short positions (required in some jurisdictions),

- Causing downward pressure on share prices for issuers that are high carbon emitters. This increases the cost of capital and could impact executive compensation packages encouraging carbon emission-related changes, or

- Helping uncover hidden carbon risks that are inappropriately priced in the market.

While there are many strategies that hold controversial assets, including high emitters, in an effort to influence the transition, assets that remain high emitters will in the future likely be held by investors who care less. Shorting allows responsible investors to have influence beyond divesting and can help accelerate the transition to net zero. If selling an asset has relevance for net zero-materiality, we believe that short-selling also should. It extends an investor’s impact beyond shrinking the emission footprint of their own portfolios.

When creating net zero reporting frameworks, we believe it is important to provide investors with full transparency for all positions that can be used to aid the global transition to net zero. There is some disagreement in the industry about whether long/short portfolios should be reporting gross or net and we believe this depends largely on the objectives which can differ as we discussed above.

At the SBAI, we advocate for reporting of long, short, and net positions to investors, we would also support the separate reporting of cash and derivate positions. Reporting in this consistent way means institutional investors can aggregate the data in a way that allows them to measure against their own objectives and gives transparency into any net calculations and the types of influence the portfolio can support.

Benchmarking Carbon

Concerns have been raised about the use of net carbon emissions in reporting frameworks including:

- Treating short positions as if they are carbon offsets,

- Concerns reporting of net numbers may give rise to greenwashing, and

- Use of short positions to “beat” a long-only benchmark.

We are not supportive of frameworks that specifically rule out net numbers, but we are not advocating the use of short positions as carbon offsets. We believe the comparison to carbon offsets is flawed. Carbon offsets are real-world instruments used to reduce carbon emissions; when accounting for carbon emissions of issued stocks and bonds, creating long positions does not create carbon, and selling or short selling does not reduce carbon. These trades result only in the transfer of the accountability for the carbon between investors.

Concerns that reporting net numbers will result in greenwashing are best addressed by requiring full transparency of long, short, and net positions giving investors a complete view of carbon emissions to make well-informed investment decisions. In fact, not reporting short positions or derivatives can create loopholes and opportunities for greenwashing. Firms could window-dress average carbon intensities, for example, by adding long positions in sustainable stocks and hedging these risks with derivative short positions resulting in an increase to the portfolio’s average ESG score.

Benchmarking is difficult and many net zero frameworks advocate for the use of long-only benchmarks, we don’t believe this is an appropriate benchmark for many alternative investment strategies. As an example, a market-neutral fund will aim to have a net delta of zero. If short positions are included in emissions calculations, this strategy would appear to have beaten a long-only benchmark without efforts to do so. In a similar way, a short-biased portfolio could appear to be significantly beating this benchmark.

We don’t believe the exclusion of short positions when reporting carbon emissions is the solution to the benchmarking issue. It is more accurate to adjust relevant benchmarks, for example by using the fund’s net delta. To “beat” this adjusted benchmark, asset managers would need to show improvements beyond the portfolio’s natural net delta. For example, a market-neutral portfolio would have a benchmark of zero and a short-biased fund would have a negative benchmark. Asset managers would therefore have to demonstrate improvements relative to this adjusted benchmark to claim influence on reducing carbon emissions.

Conclusion

We believe that shorting can be an important tool in responsible investment and the transition to net zero and that net zero frameworks should acknowledge this contribution.

We believe that long cash, long derivative, short cash, short derivative, and net positions should all be reported separately for carbon emission-related metrics. This ensures full transparency to investors, and we believe reduces the risk of greenwashing when compared to frameworks that advocate for partial transparency – i.e., reporting on a subset of positions only.

We believe that setting benchmarks or targets based on the net delta of the portfolio would be more appropriate than the use of long-only benchmarks. This means managers must demonstrate an influence over and beyond where the portfolio would naturally sit through its long, short or market-neutral bias.

You can find more of our work on Responsible Investment in our Responsible Investment Toolbox.

Original Article Post: Short Selling and Responsible Investment (sbai.org)

About the SBAI

We are a global active alliance of asset managers and allocators dedicated to advancing responsible practice, partnership, and knowledge. We ensure the quality and effectiveness of the alternative investment industry through responsible standards and the exchange of ideas. In short, we solve for better.

We are supported by over 150 asset manager signatories with approximately US$ 2tn in AUM and over 90 institutional investors responsible for US$ 4tn in assets. At our core is an active community committed to knowledge sharing, informed dialog, and innovation. Together our community of asset managers and allocators create real-world solutions to tomorrow’s industry challenges.

The SBAI was established in 2008 as the Hedge Fund Standards Board (HFSB) creating the Alternative Investment Standards which we continue to be the custodian of. We are a non-profit organization governed by a Board of Trustees comprised of senior leaders from asset managers and allocators.