By Christoph Junge, Head of Alternative Investments at Velliv; Denmark’s third-largest commercial pension company.

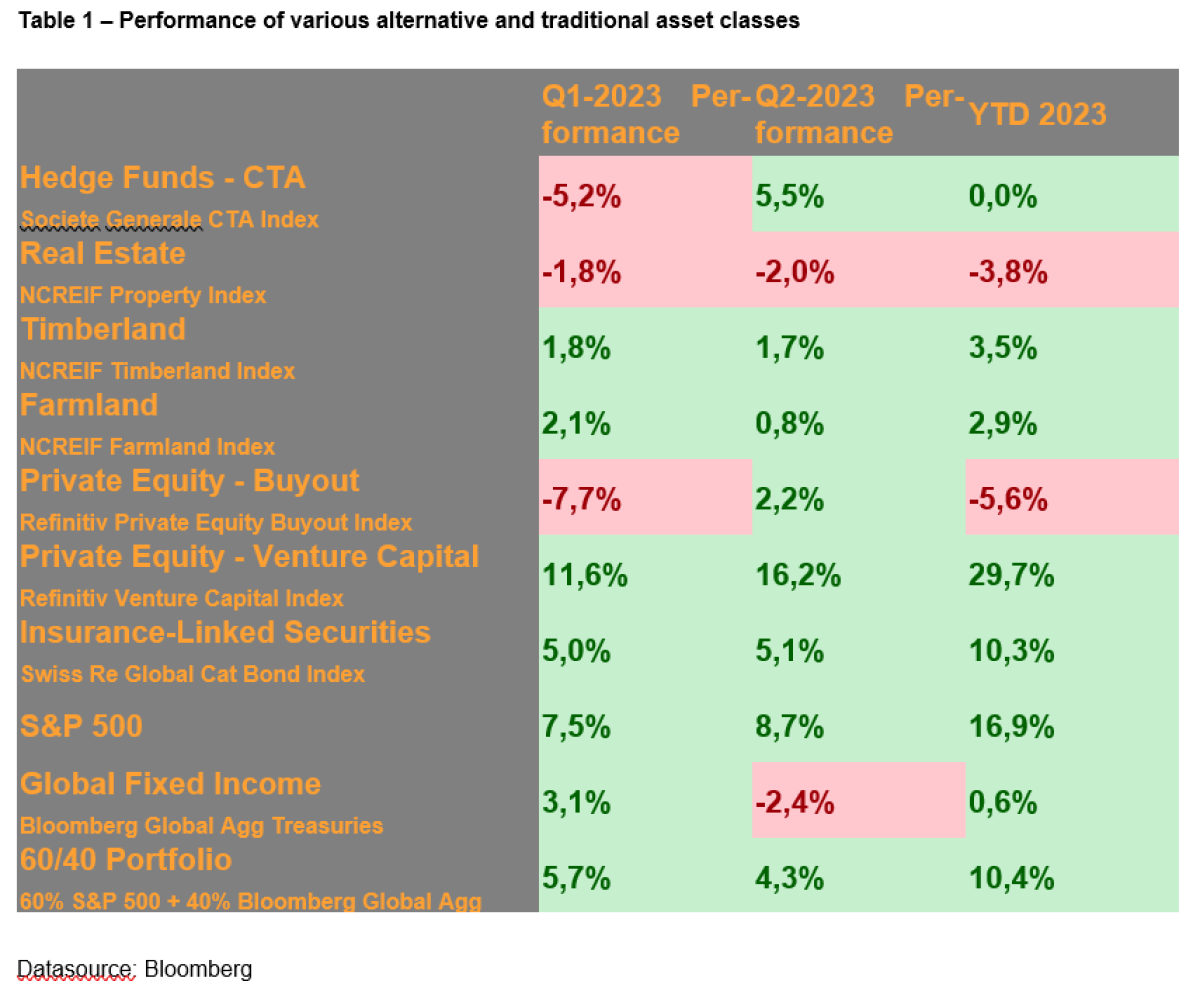

After a rough start to the year, with three small- to mid-size US banks failing over the course of five days followed by the forced merger of UBS and Credit Suisse, the second quarter was more smooth sailing for most of the asset classes covered in this column. Real estate is the only alternative asset class that posted losses while ILS are having record breaking returns. CTA recovered their losses from the first quarter. Alternatives continue to show dispersion both across asset classes and within asset classes on sub-asset class and manager level.

Listed assets, in this column S&P 500 and global government bonds, had mixed outcomes in the second quarter with equities being up even more and bonds being down. A widely used benchmark for a balanced portfolio consisting of 60 pct. equities and 40 pct. bonds, gained 4,3% entirely driven by equities. This brings the performance up to 10,4% for the first half of the year. This is more than an investor typically could expect for a whole year let alone for six months.

Infrastructure is unfortunately no longer part of this column as the used benchmark is not updated on Bloomberg anymore. The other benchmarks consisting of unlisted funds are not updated for Q2 yet. I will try to find a suitable replacement for future columns.

But before we dig into the numbers, I want to remind you of a few technical facts of importance.

- Most alternative investments, aside from liquid alternatives, are long-term investments. To evaluate the performance over a single quarter has limited explanatory power.

- There is always a time lag between reported returns and public market returns due to the illiquid nature of the underlying investments.

- The benchmarks chosen for Private Equity and Venture Capital are liquid replication benchmarks. Over longer timeframes, they have historically given a somewhat reliable picture of the asset classes, however over a shorter horizon they typically overstate the movements in the market (both up and down), according to my own analysis.

- Alternative investments are very heterogenous in their nature with huge dispersion also on the manager level. The realized returns of an investor will most likely deviate from the benchmark level returns.

CTA, a sub-asset class from the hedge fund universe that is known for using trend-following models, recovered their losses from the first quarter during the second quarter and ended the first half with a flat performance.

Short-term interest rates and currencies, especially the Mexican peso and Japanese Yen, were major performance drivers. Commodities, a major performance driver in 2022, had some headwinds in Q2, especially the whipsawing oil market.

After the – for some strategies - brutal losses in Q1, the dispersion on the manager level increased even more during Q2 (and further into Q3) and the difference between top and bottom performer on my watchlist of trend-following funds is a staggering 1730 bps. after the first two quarters – ranging from +5,6% to -11,7%. And there will most likely be other funds with even more extreme outcomes. All of this with the benchmark being flat. This acts as a friendly reminder that both manager selection, diversification across several strategies and portfolio construction is key in this space. In general, the slower trading models performed better this year, as the faster models got whipsawed more often.

Real Estate, as represented by the NCREIF Property Index, an unlevered index of directly held properties in the US, continued downwards and ended the quarter with a loss of 2,0%. Office was again the laggard with a loss of 5,8%. Hotels were the only sub-asset class with positive returns of +4,0% while retail was nearly flat with a minor loss of 0,2%. Both sectors were hit hard by the Covid crisis and are now recovering from low levels.

Both timberland and farmland continued to show resilience and posted positive returns of 1,7% and 0,8% respectively. While all four timberland regions had positive gains in the second quarter, the US Northwest region had the highest return of the second quarter at 1.86%, comprised of 0.34% EBITDDA and 1.52% appreciation returns. The Total Timberland Index had a 11.13% rolling one-year return, comprised of a 2.73% EBITDDA and

8.23% appreciation return, according to NCREIF. The farmland returns were driven by annual cropland returns (also known as row crop like wheat and corn) delivering 1,7% while permanent cropland like almond plantations were down by 0,6%. Over the prior four quarters, the cumulative total return for farmland was 8.19%, resulting from an income return of 3.28% and appreciation of 4.80%, as reported by NCREIF.

Private Equity had a mixed start to the year with Buyouts down and Venture Capital up. Buyouts recovered some of the losses during Q2 while Venture continued to shoot for the stars. This holds true at least for the liquid replication benchmarks used in this column and worth remembering that this comes after a disastrous year 2022 for especially Venture Capital. But as mentioned, these are liquid replication benchmarks and VC follows tech stocks. Compared with NVIDIA, that is up 189,5% during the first six months, the 29,7% posted by the VC index are less impressive. But comparing a single stock to a broad basket is not a fair comparison either.

When looking at “true” private equity markets, the picture is not exactly rosy but not bad either.

On the negative side is the exit volume. While US PE exit activity was slightly higher in Q2 compared to Q1, it is still on a depressed level. Exits to corporates are the most likely exit route at present and are now accounting to close to two thirds of all deals, according to Pitchbook data. The deal activity on this side of the pond is – while still being below 2022 numbers – recovering. Exit value hit 68 billion EUR in Q2, which is up by close to 29% compared to Q1, according to a report from Pitchbook.

Even though deal activity is undeniably down especially compared to the red-hot market witnessed in 2021, there are still exits and still good exits, as one GP in Vellivs portfolio made a spectacular exit during summer app. 60% above Q1 2023 valuation at an eye-watering EBITDA multiple.

And although fund raising activity has slowed down a bit compared to 2021, there is still activity and the industry is on the way to raise more cash than during 2022. But it is a tale of two markets: while mega-funds are growing bigger and bigger, smaller emerging managers are struggling to attract money from investors. One example is CVC, for instance, that managed to raise €26 billion for CVC Capital Partners Fund IX, which is one of the biggest PE funds ever raised. Another example is Permira who closed Permira VIII above target, with total commitments of €16.7 billion.

And GP’s who manage to raise capital are also deploying capital, which will keep the market open.

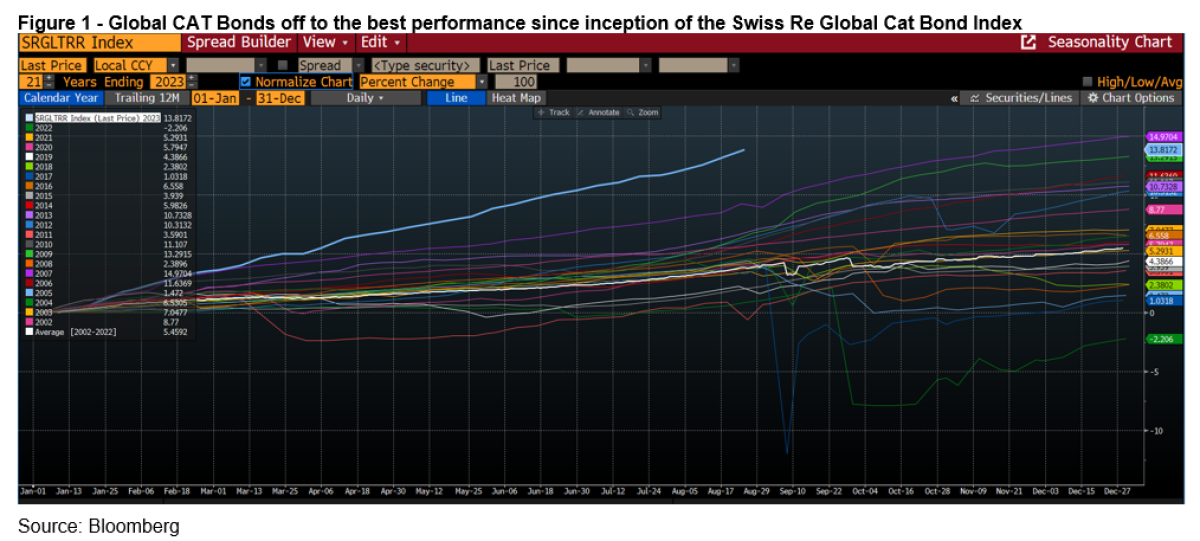

Insurance-Linked Securities (ILS), often also referred to as “CAT Bonds” (catastrophe bonds), continued its strong performance and posted a gain of 5,1% for the Swiss Re Global CAT Bonds Index, bringing the total return during the first 6 months of the year to 10,3% - one of the strongest performances among the alternative asset classes covered in this column and the strongest first half since the inception of the index. This is driven by both higher spreads (e.g., insurance premium) and higher rates on the collateral – and of course no major catastrophe.

As outlined in my Q4 2022 column published in February 2023, a lack of capital in the ILS market was driving up spreads, leading market participants to calling it “one of the best entry points for investors in decades”. So far, they got it right. But it is too early to celebrate as the hurricane season runs from June 1st to November 30th, which leaves still plenty of time for losses to come. The National Oceanic and Atmospheric Administration (NOAA) expects the 2023 hurricane season to be “above normal” due to record-warm sea surface temperatures. With that being said, what matters is not only the number and strength of hurricanes but also the number of landfalls and the region of the landfall. A hurricane that never makes landfall does not matter while a category 5 hurricane making landfall in Miami would be devastating, not only for the people affected but also for the asset class. As of August 25th, there was no major event impacting the asset class, bringing the YTD performance up to 13,8%. This is the strongest performance since the inception of the Swiss Re Global Cat Bond Index in 2002.

Conclusion: The second quarter was more smooth sailing than the first and alternatives contributed with positive returns – at least the majority. Real estate is the exception to the rule and is suffering from both a strong rise in interest rates that eventually led to rising cap rates (there is no linear relationship between interest rates and cap rates) and especially the office segment is suffering also from more structural challenges.

Real assets like timberland and farmland are so far having a good year and manifest their role as an inflation hedge. The old saying coined by Mark Twain “Buy land, they're not making it anymore” seems still to hold true.

If there won’t be any major natural catastrophes during the remainder of the year, ILS is on course for a record-breaking year and might even end up being the best-performing asset class.

Private equity is keeping somewhat up so far despite the headwinds.

The – by some – anticipated ‘significant losses’ on alternative investments (real estate, infrastructure, and private equity) have at least not crystallized yet. Not in private capital benchmarks nor in the reported returns by Danish pension funds.

But as Tom Petty said: The future is wide open.

About the Author:

Christoph Junge is Head of Alternative Investments at Velliv; Denmark’s third-largest commercial pension company. He is a Chartered Alternative Investment Analyst and has more than 20 years of experience from the financial industry in both Denmark and Germany. He has worked with Asset Allocation, Manager Selection as well as investment advice in, among others, Nordea, Tryg, and Jyske Bank.

Besides working as a Head of Alternatives, Christoph teaches a top-rated course on Alternative Investments. Read more at http://www.christoph-junge.de