By Mathias Neidert, Managing Director, Head of Public Markets and Kunal Chavda Director, Fixed Income at bfinance.

Rising interest rates and inflationary forecasts continue to underpin strong demand for Leveraged Loans, thanks in large part to their floating rate characteristics. Yet investors seeking to introduce dedicated exposure to this asset class can face significant implementation challenges.

The latest data on manager searches for bfinance clients has revealed a heightened appetite for Leveraged Loans over the past year, while Investor Poll (April 2022) showed a significant minority of asset owners planning to introduce or increase exposure to this asset class.

In practice, however, investors entering this space have encountered notable obstacles. Available pooled funds are often not appropriate for their specific needs in areas such as credit quality, regional exposures, and ESG. While segregated mandates do enable more flexibility, they can create complex administrative burdens for investors—exacerbated by the fact that a significant proportion of custodians are not well-equipped to provide appropriate support.

In this brief article, we tackle three implementation questions that investors are likely to face when considering their approach to this asset class.

Dedicated mandate to leveraged loans or diversified strategy?

Investors can gain exposure to this asset class either through a dedicated Leveraged Loans strategy or through a diversified strategy such as Leveraged Finance or Multi-Asset Credit: these offer exposure to a variety of sub-sectors and the capability for active allocation decisions. Yet investors should be aware that Leveraged Loans typically represent only a small proportion of these diversified strategies—although this figure does vary considerably. In UCITS funds, for example, Leveraged Loan exposure is capped at 10%.

(To read more about Leveraged Finance Strategies, read Multi Sector Fixed Income: Back in Focus. An upcoming white paper will examine the universe of Leveraged Finance strategies in more detail.)

Which types of manager and strategy can be considered?

Investors that decide to pursue a specific allocation to this asset class will find a healthy universe of fixed-income managers offering Leveraged Loan strategies. These include traditional fixed-income houses, private credit managers that have launched specialized vehicles, and collateralized loan obligation (CLO) managers. Whilst the majority offer both pooled funds and segregated accounts, some—particularly those running high CLO asset bases—are not able to offer an open-ended pooled fund vehicle.

Most of the available pooled funds have open-ended structures, though there are also a number of closed-end funds (e.g. a five-year lock-up with a one-year ramp-up). Interestingly, while private credit managers do often voice a philosophical preference for closed-end structures, an increasing number of them offer open-ended strategies—often used by investors in their own private debt funds to take care of committed capital that has not yet been called and subsequent disbursements (see Tackling the Committed Capital Conundrum).

We see a further distinction in the strategy universe between strategies that take a ‘buy-and-hold’ approach versus those that are focused on active trading. CLO managers and private credit managers with Leveraged Loan strategies don’t typically tend to be very active in rotating portfolio exposures, whereas a higher proportion of managers in more traditional fixed-income houses see trading as a source of alpha generation. On a related note, we also find that the strategies run by traditional fixed-income houses tend to have a higher proportion of widely syndicated loans with deeper secondary market liquidity, whereas strategies run by the more ‘alternative’ managers tend to feature a higher proportion of credits that are thinly syndicated or structured by the lenders themselves.

Importantly, a manager’s decision to offer an ‘evergreen’ structure doesn’t mean that the underlying strategy is well-suited to an evergreen model. CLO managers have strong capabilities in structuring securities and managing them for the first two or three years but tend to take a more hands-off approach as the loans mature.

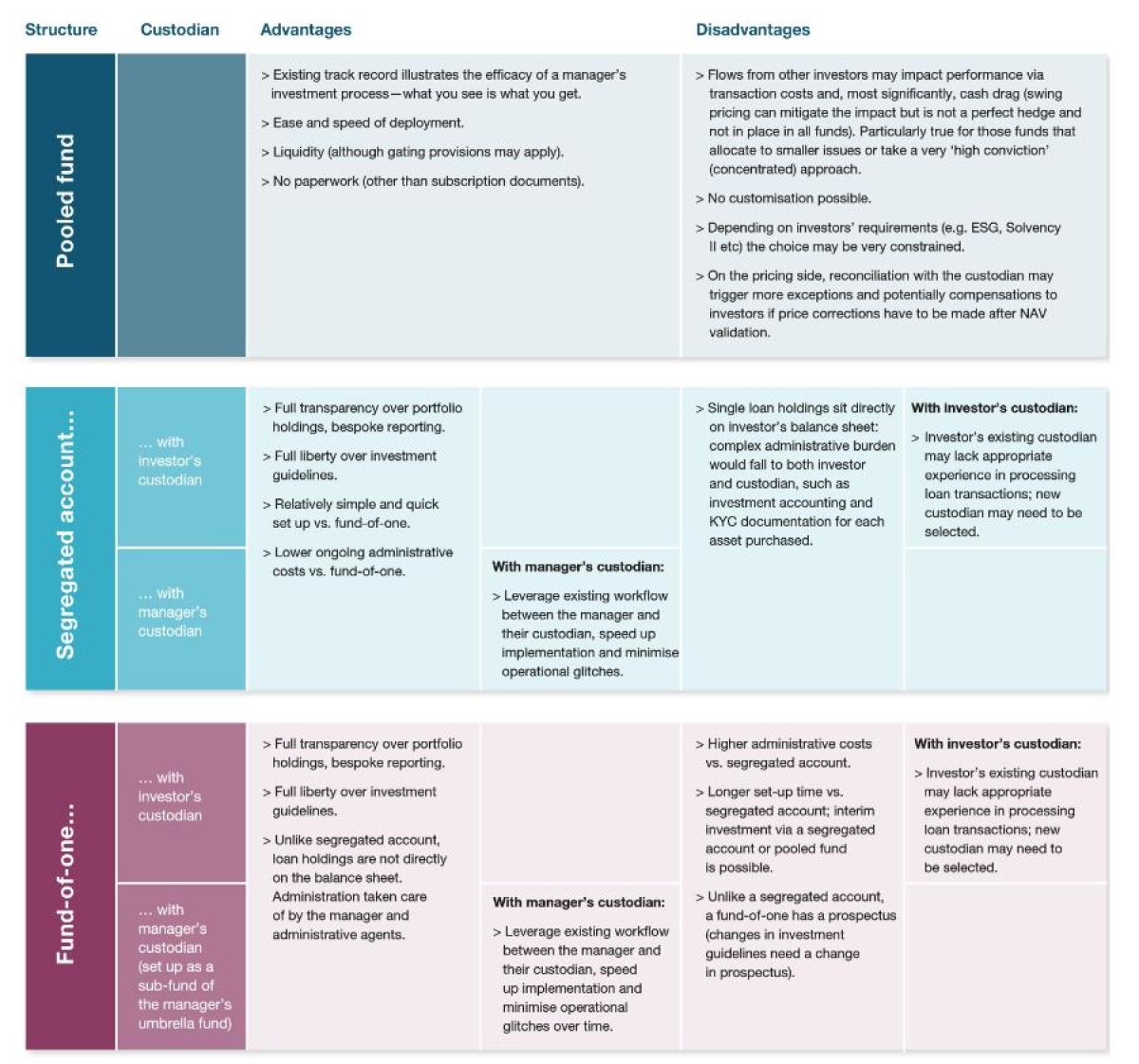

Pooled fund, separately managed account (SMA), or fund-of-one?

When investing in Leveraged Loans, asset owners need to make crucial choices about the type of vehicle they wish to use. Many investors find that pooled funds offer an inadequate range of options to fit their needs on subjects such as ESG/sustainability, credit quality, regional exposures or liquidity.

On the positive side, many Leveraged Loan managers are willing to structure dedicated solutions (fund-of-one or segregated account) for larger investment amounts. The cut-off tends to be around $75 million, although the figure does vary between managers and can be affected by the investment style: a diversified approach may well require a higher minimum threshold than a high-conviction strategy.

A brief summary of the pros and cons of pooled funds, segregated accounts, and funds-of-one is shown in the table below. Liquidity challenges, cash drag, flexibility, and cost are all relevant considerations. Importantly, the table highlights the differences involved in using an investor’s custodian versus a manager’s custodian (the former is often chosen or imposed, despite the operational pitfalls).

Segregated mandates are typically 5-to-10 basis points (bps) cheaper than funds-of-one, as well as faster and easier to set up. Yet benefits may often be outweighed by the considerable ongoing administrative burden that segregated mandates create for the investor, including accounting requirements and anti-money laundering processes (e.g. Know Your Customer (KYC) checks to honor for each new loan underwritten). This makes funds-of-one preferable in many cases. Not all managers have experience in setting up funds-of-one, but the process is relatively straightforward for any manager that is used to setting up pooled funds.

The topic of the custodian is crucially important. Our recent work for clients in this space has indicated that a substantial proportion of custodians do not have what we would view as the appropriate experience and capabilities to administer these assets and process both primary and secondary loan transactions. It is vital to seek evidence of those capabilities and references from asset managers. Investors should not underestimate the risks involved in this area. Although settlement certainty has increased—and settlement time has decreased—thanks to improvements in pricing, valuation measures and overall transparency, the investment process remains document-heavy and manual. Settlement delays should not fundamentally affect the economics for the investor, thanks to ‘delayed compensation’ arrangements (which kick in after ten days in Europe and seven in the US), but slow settlement can mean that a manager does not have the funds available to make a subsequent purchase or honor redemptions. This can lead to a reliance on credit lines (a form of short-term leverage) or carrying higher cash balances (creating a drag on returns).

Conclusion

Given the diversity of this asset class, the different investment approaches available and the implementation considerations in play, investors should try to consider the widest possible range of Leveraged Loan managers and strategies that may suit their core objectives. Managers are able to meet diverse needs with dedicated mandates (SMA or fund-of-one), but custodians’ capabilities should be scrutinized with particular care and the investor’s willingness to select another custodian for this specific mandate may be highly relevant when deciding on the appropriate path.

About the Author:

Mathias Neidert is the Head of Public Markets and a member of the firm's Senior Management Team.

He joined bfinance as a Senior Associate in March 2008 focusing on manager research and selection in fixed income. He was named Head of Public Markets in 2014, managing a team of asset class specialists in charge of investment advisory within listed equity and fixed income. Before joining bfinance he worked for RBC Dexia in Luxembourg, most recently as Product Manager for Investment Analytics services. Mathias started his career in the investment fund industry in 2003. He is a CFA Charterholder and holds a master’s degree in business administration from the University of St. Gallen (Lic. Oec. HSG) in Switzerland.

About bfinance

bfinance is an award-winning specialist investment consultancy with a range of services including manager research, fee/cost benchmarking, risk analytics, performance monitoring, asset allocation, and investment policy design, ESG advisory and more. Headquartered in London with offices in nine countries across four continents, the firm is known for exceptional client servicing and high-quality research execution (based on independent customer research). Clients include pension funds (DB and DC), sovereign funds, endowments, foundations, insurers, family offices, financial institutions, wealth managers and other investor entities.