By Nora Pickens, Managing Director of Investments at Mill Creek Capital Advisors.

Fixed income markets have steadily declined since early 2022 when investors began acknowledging the potential for above-trend inflation and aggressively priced in fed funds rate hikes. Over this period, the yield on the benchmark U.S. 10-Year Treasury Bond rose by over 200 basis points, accompanied by a surge of 500 basis points in short-term rates. This market rerating has triggered a cascading impact on all risk assets, including the private debt markets. The asset class includes debt securities that are typically originated and owned by non-bank institutions and do not have centralized exchanges for trading on a regular basis.

The private debt market can be divided into two broad categories: direct lending and “everything else.” Direct lending typically involves originating floating-rate debt with intermediate-term maturities to small- and medium-sized companies. Corporate credit risk, or a firm’s likelihood of paying back a loan, is the key consideration for lenders when analyzing a deal. Over the past decade, it has accounted for roughly half of the total capital raised mostly due to ease of scalability, access, and favorable return profile. The “everything else” category covers a wide range of highly varied, niche strategies such as aircraft securitization, equipment finance, and real estate mezzanine loans that have “non-corporate” related risks.

Private debt opportunities have been in existence for decades but accelerated after the Global Financial Crisis (GFC) due to regulatory changes like the Dodd-Frank Act. The new policies increased bank lending costs and led to the proliferation of alternative capital firms eager to fill the void. Since 2010, assets managed by private debt funds have increased 5.6x to $1.4 trillion.1

However, given the sector’s relatively short history, holders of private debt are facing their first true test of sustained rising interest rates. Thus far, the sector has taken the change in stride. Favorable economic conditions have kept a lid on impairments and defaults. At the same time, private debt originators have benefited from expanded deal pipelines as the traditional banking system has retreated.

Private debt markets are remarkably diverse, though, and not all strategies are created equal. Despite the favorable performance year-to-date, we anticipate a higher-for-longer interest rate environment will benefit certain strategies over others. Below, we discuss a few key themes that we believe will be important for optimizing risk-adjusted returns going forward, with a focus on semiliquid alternative funds (though these considerations can be extrapolated to other investment structures as well).

Maturity vs Duration

An appealing feature of many private lending strategies is the floating-rate nature of the underlying investments. It displays low correlation to traditional fixed income and provides protection against duration risk. When base rates rise, private yields also increase, offsetting the price degradation typically seen in traditional bonds. This real-time coupon reset means most of the more popular private debt strategies in the market today — namely middle market direct lending — manage portfolios with zero duration.

In a declining interest rate environment, it’s easy to overlook the distinction between duration and maturity. When yields steadily drop, borrowers are inclined to refinance loans once call protection expires, or even earlier, depending on deal terms and if breakeven calculations turn positive. This results in accelerated cash returned to investors and loans repricing to prevailing market economics. However, in a rising-rate environment where credit spreads and Secured Overnight Financing Rate (SOFR) floors increase, borrowers tend to de-lay refinancing until closer to the stated maturity date. In the case of direct lending, this can mean upwards of 5–7 years post close.

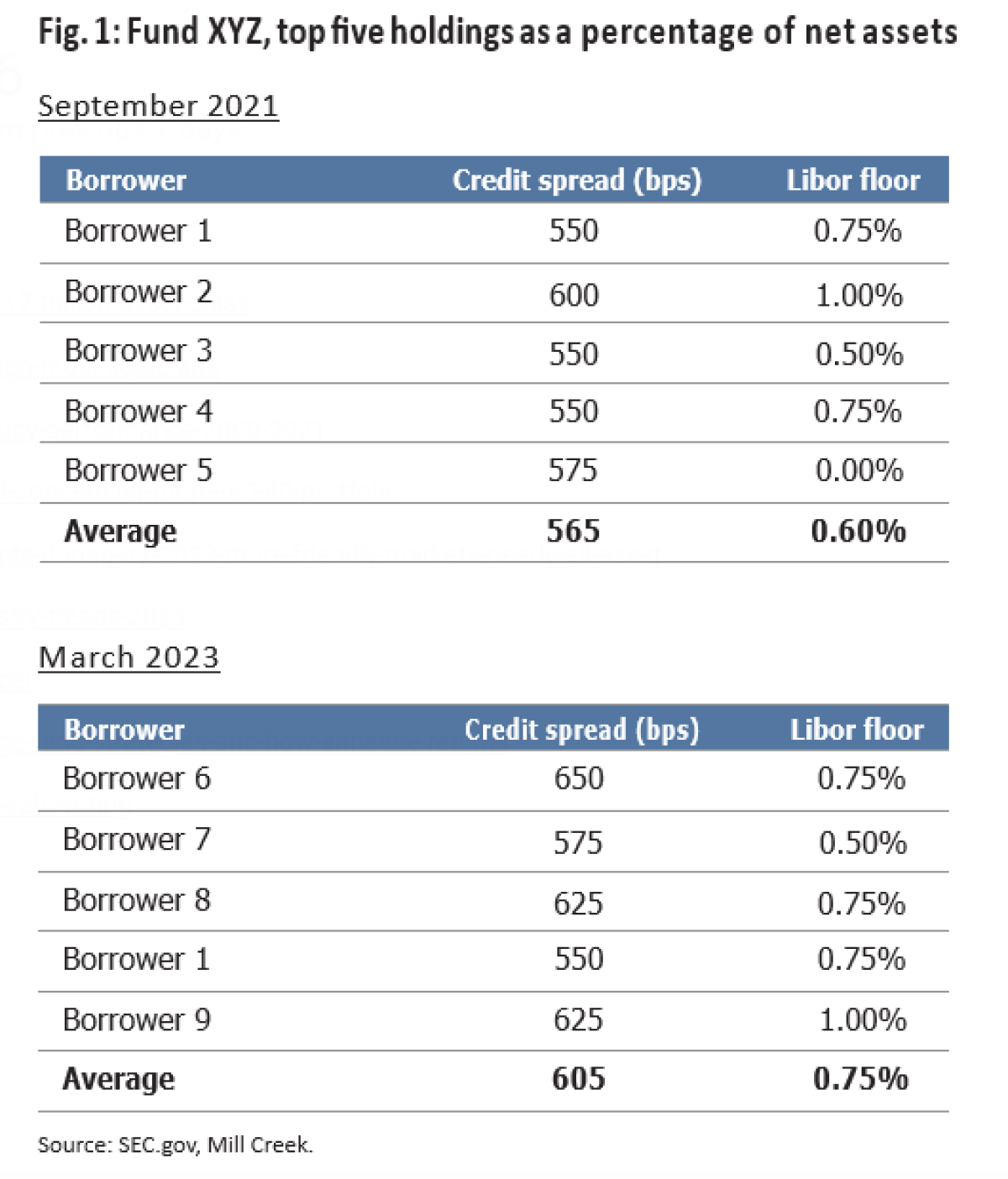

The changing interest rate environment has impacted portfolio compositions across strategies. For example, in 2021, a large semiliquid alternative credit fund in the market, held loans with floors that ranged from 0.0% to 1.5% (Fig. 1). The fund invests in directly originated loans issued by upper middle-market companies. Its top five exposures, as a percentage of net assets, had an average credit spread of 565 basis points. Fast-forward two years and the floors now extend to 2%, while the average spread has increased to 605 basis points. Borrowers are disincentivized to refinance given the additional expense, so the assumed time to principal pay-back lengthens.

As a result, investors should expect a lower distribution to paid-in (DPI) multiple during the earlier years for closed- end structures and reassess payback period assumptions in semiliquid vehicles with runoff share classes. Of course, regular coupon payments will continue to provide a source of funds that can be redeployed as desired. But updating assumptions around liquidity across the board will be important to navigate the evolving environment effectively.

Return Attribution

Lower turnover in private loan portfolios can lead to lower ancillary revenues generated from call protection, origination fees, closing costs, etc. These revenue streams can account for up to a quarter of a fund’s performance, depending on the strategy. For instance, a fund returning 8% may have derived 6% from current income and 2% from “other” fees.

If interest rates remain higher for longer and the tenor of underlying securities extends, the contribution from these ancillary sources will shrink. The increased income from rising base rates will tend to offset this decline. However, investors should understand that a rise in SOFR will not necessarily result in a direct 1:1 increase in performance. Returns often consist of a combination of yield plus non-core revenues that fluctuate based on evolving economic, rate, and capital market environments.

Managers can counter yield degradation in semiliquid vehicles by owning floating-rate paper and diluting legacy investments with new deals funded by inflows. A stagnating or net outflow scenario is more challenging to manage. Niche strategies that hold shorter-maturity paper recycle assets quickly and experience less compression of non-core revenue as a result. Therefore, during due diligence on potential investments, it’s important to understand historical return attribution, future composition changes, and capital flow trends.

Leverage Facilities

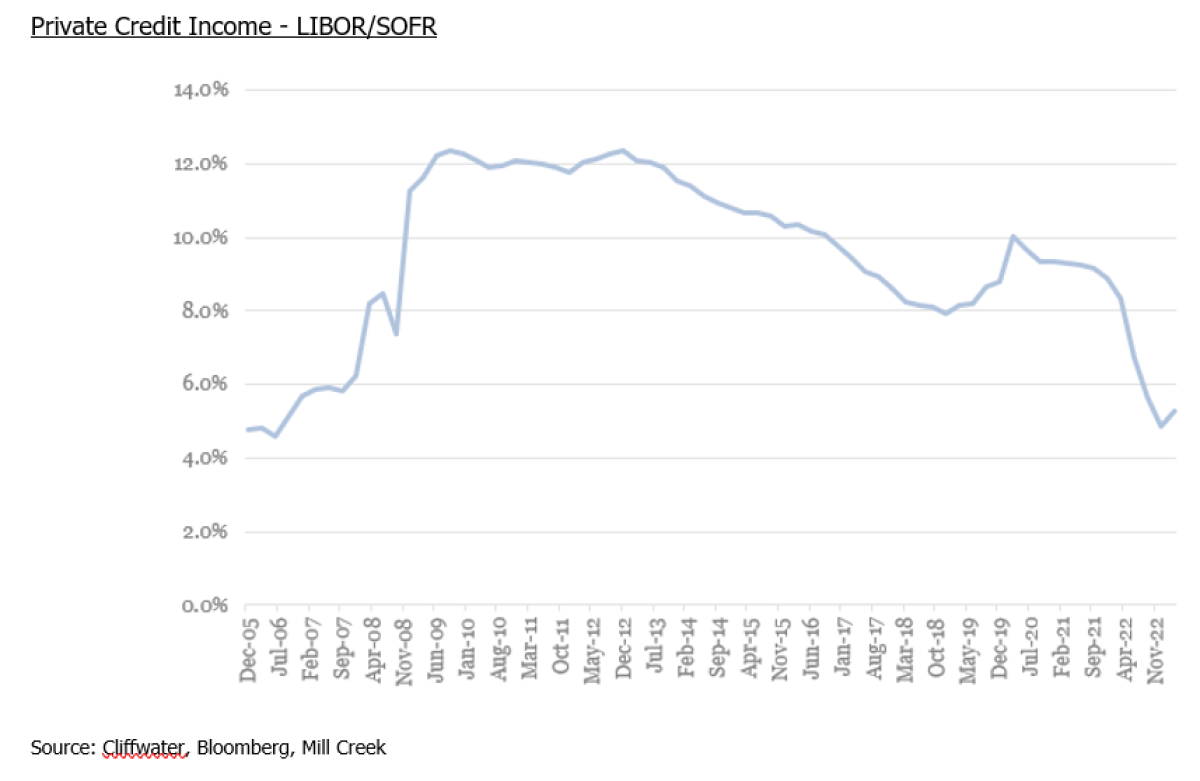

Private credit strategies traditionally relied on leverage to finance investments and boost returns. Over the past decade, asset managers have benefited by earning an outsized spread between the cost of funding and coupons earned from their investments. The difference between income returns of the Cliffwater Direct Lending Income Index (CDLII) and one-month LIBOR/SOFR serves as a useful proxy for the funding environment. From 2010–2020, the CDLII- LIBOR/SOFR spread averaged 10.4% (Fig. 2). During this period, funds enjoyed healthy levels of floating-rate income while locked into low-cost debt, with near-zero impairments or defaults.

Today, the spread has collapsed to 4.8% and borrowers are facing late-cycle dynamics, transforming favorable tailwinds into headwinds. Managers who secured long-term, fixed- rate financing before 2022 will continue to benefit from their prudent decisions. Nevertheless, we anticipate some performance erosion for leveraged funds needing to raise credit facilities within the next 12 months given the narrowing asset-liability spread. This reality will likely lead to deleveraging, with blue-chip managers in a position to outperform due to strong banking relationships and the ability to secure below market funding.

Our Positioning

Direct lending has been a popular and successful strategy to date, but we believe a higher-for-longer interest rate environment entails looking elsewhere to generate attractive risk-adjusted returns. Specifically, we are positioning our clients’ private income portfolios toward short-term strategies that exhibit high turnover, low corporate credit risk, and minimal leverage. We believe these investments are better equipped to earn a consistent illiquidity premium over prevailing market rates and incur less impairments during the next credit cycle.

Short-term, small-balance real estate loans are an example of the type of strategy we currently consider attractive. The loans in this strategy are typically floating rate, backed by a first-lien mortgage on residential properties, and less than $1 million on average. Importantly, the loans generally mature in 12 months from issuance. In a rising-rate environment, this benefits investors in two key ways:

- Low reinvestment risk: Roughly 25% of the fund’s in- vested capital is paid back every quarter. The rapid turn- over effectively “resets” the portfolio’s weighted average yield to market while also benefiting from deal fees col- lected on new transactions throughout the process.

- Downside protection: As a senior secured lender, the manager looks to the asset for repayment first. But a strong alignment of interest is created from the bor- rower’s significant cash equity investment (typically 35– 50% of building value) into each deal. A high turnover strategy means that these large equity infusions occur regularly at current real estate valuations, providing downside cushion to each loan. This helps shield the portfolio from loss under a range of stress scenarios.

Over the course of 12 months, the portfolio has cycled through all investments and expected investor returns closely follow the prevailing interest rate environment whether rising or falling. In other words, returns are driven less by the absolute level of rates and more on idiosyncratic risk factors such as quality of the underlying collateral, project management, and ability to exit a loan through refinancing or sale of the property. Any misstep underwriting these deal considerations can lead to underperformance of the investment. Additionally, on a relative basis, we expect the strategy’s returns will lag longer maturity opportunities when yields are falling given the lower sensitivity to interest rates which tempers price appreciation.

In summary, while doubling down on term premium in the public and private markets was successful in the past, we believe that a well-diversified allocation to differentiated private credit strategies will deliver value to portfolios in the new era of volatile and rising interest rates.

Footnotes:

1. Prequin

Disclosure

This document is for educational and informational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This document has been prepared by Mill Creek Capital Advisers ("MCCA"). Any views expressed above represent the opinions of MCCA and are not intended as a forecast or guarantee of future results. It is not intended to provide, and should not be relied upon for, particular investment advice. Certain information contained in this document has been obtained from sources that MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this document are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this document. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this document or its contents. We are not soliciting any action based on this communication and it does not constitute any advertisement or solicitation or offer, inter alia, to buy or sell any security in any jurisdiction.

About the Author:

Nora Pickens serves as Managing Director of Investments at Mill Creek Capital Advisors, LLC. She has primary responsibility for evaluating fixed income and alternative credit strategies across MCCA’s investment programs.

Prior to joining MCCA in 2017, Nora was Director at FS Investments, where she helped launch focused investment programs and conducted investment research. Prior to FS, Nora was a Credit Analyst at Standard & Poor’s with primary research coverage of the energy sector. She previously held various analyst positions at Bear Stearns and Goldman Sachs.

Nora earned her Bachelor of Arts in business economics from Brown University and received an MBA from the Yale School of Management. She holds the Chartered Alternative Investment Analyst (CAIA) designation. Additionally, Nora serves as a member of the Board of Directors at CAIA Pennsylvania.