By Jack Farley, at Blockworks and host of Forward Guidance podcast.

Bond markets are supposed to be boring. If bonds are fun, usually it means you’re doing it wrong.

Except for last year. Bonds stopped being boring in 2022 when they started going down a lot. As their prices fell, their yields rose substantially. But yields on shorter-duration bonds (ones that mature and get paid back) rose much faster than yields on longer-duration bonds, largely because they are more under the influence of the Federal Reserve and other central banks, which control the overnight rate. In 2022, the 2 year-yield rose in anticipation of central bank hiking the overnight rate (known in the U.S. as the “Fed Funds Rate”).

Now, it’s a completely different ball game.

Many central banks have paused or stopped raising interest rates, and some central banks are even cutting them. The market now assigns a >60% chance that the Federal Reserve is done hiking rates.

This should be good for bonds. And it is. But the chaos in the bond market continues. Why?

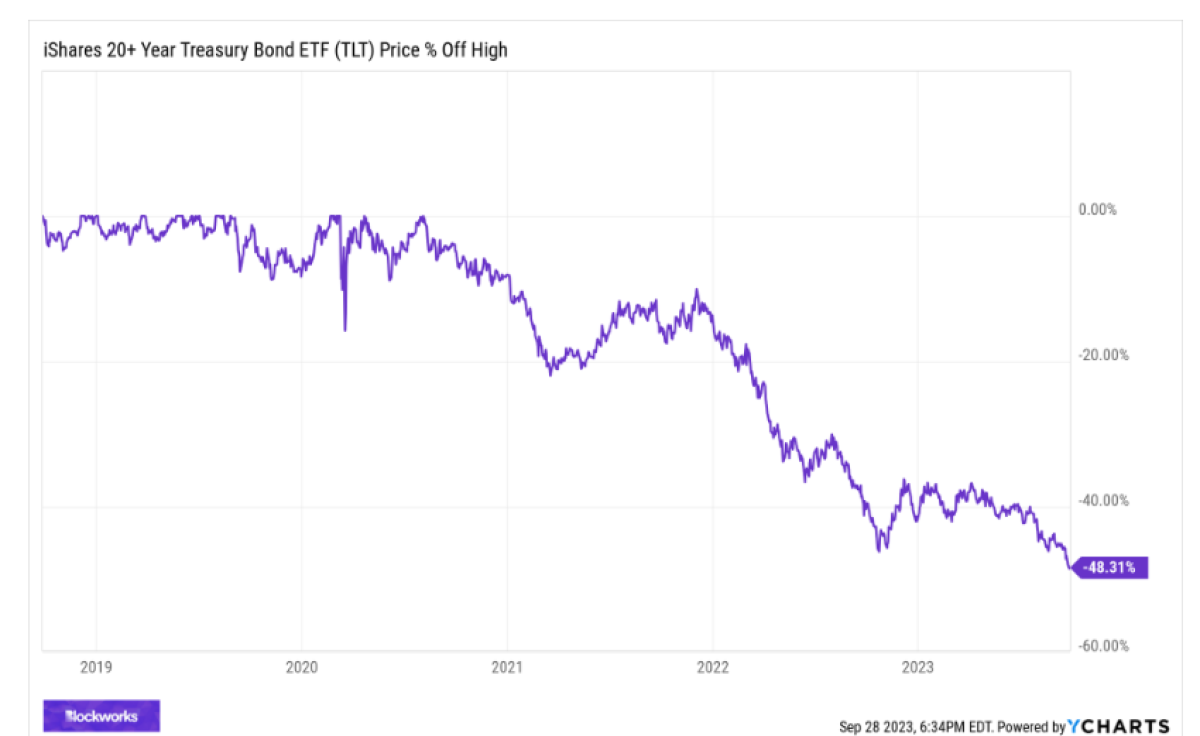

The first reason is that short-term yields continue to rise as expectations that the Federal Reserve will cut rates are priced out of the market. The second reason is that the U.S. government is issuing a TON of bonds to fund its fiscal deficits. Both reasons are causing bond investors lots of pain:

What’s interesting is that now, unlike in 2022, yields on long-term bonds are rising more than yields on short-term bonds:

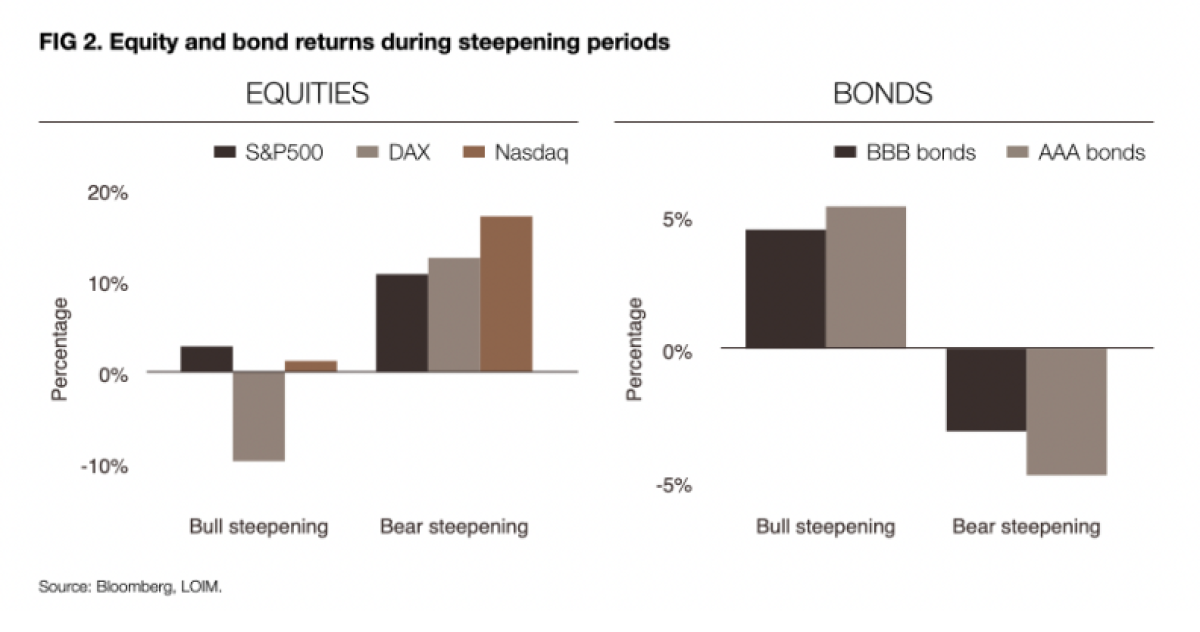

This is known as “bear steepening” because the yield curve is steepening (long-term yields rising faster than short-term yields) and bonds are selling off (“bear” market in bonds).

Bear steepening is not very common. Often it occurs after a recession bond bull market at the beginning of a new economic cycle, such as in 2009 and 2020. This may be why bear steepeners are often quite bullish for risk assets:

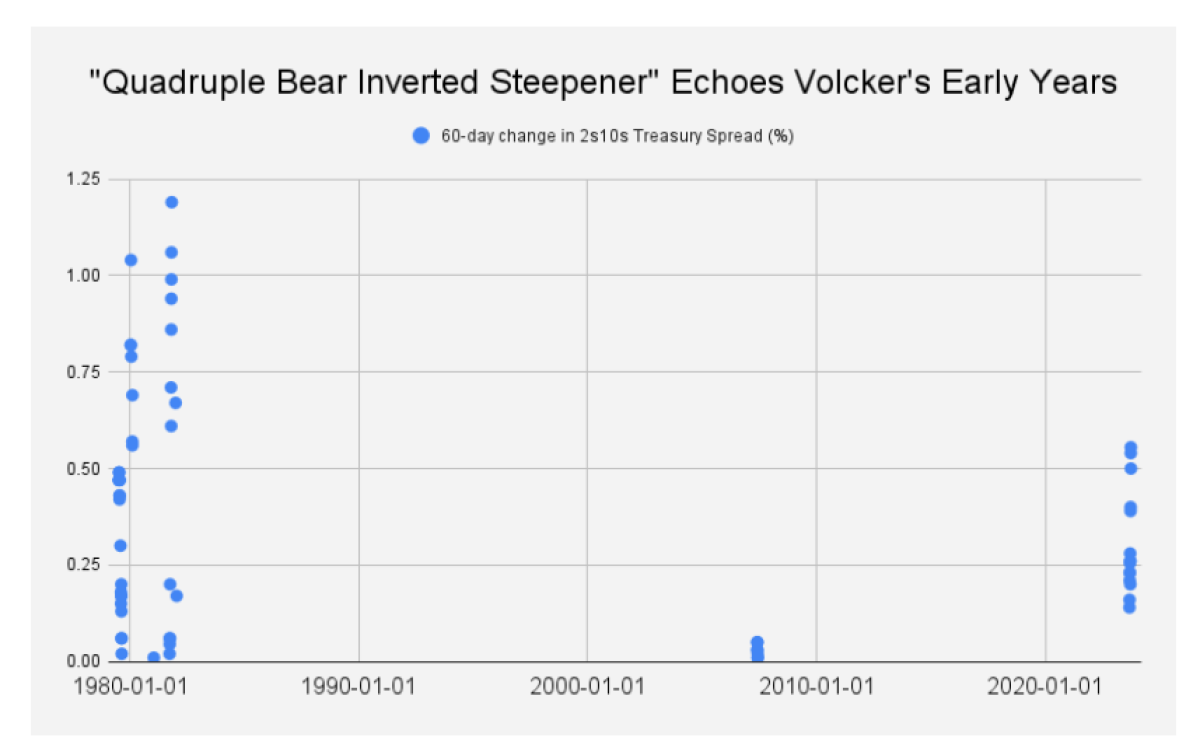

But the ongoing bear steepening is of a very special kind. While bear steepening itself is somewhat rare, bear steepening during a prolonged (200-day) bond bear market in bonds is more unusual. And a “quadruple bear steepener” that has continued to steepen on a rolling 5-day, 60-day, and 200-day basis in the midst of a prolonged bond bear market is rarer still.

But to get the true blue moon of bond market moves, introduce the inverted yield curve (a bond market where short-term rates are already higher than long-term rates). The bond market yield curve market has been inverted since the spring of 2022, and it has caused many economists and analysts to forecast a recession, prognostications which have so far not played out (although they still may).

A “Quadruple Bear Inverted Steepener” has occurred just 0.5% of the time going back to 1976. Nearly all have occurred in 1979, 1980, 1981, during the early tenure of Paul Volcker’s as Chair of the Federal Reserve:

The parallels between then and now jump out: the U.S. government flooded the market with long-duration bonds, and the market was adjusting to the reality that the Federal Reserve would maintain interest rates at restrictive levels for a sufficiently long period of time in order to tame inflation.

The key difference is that the economy is much, much better now, unlike in 1981, when it had just exited a short-lived recession in 1980 and was about to enter another one.

The silver lining is that, should this parallel hold, long-term yields might be close to peaking, as they did in 1981. What followed was a 4-decade long rally in all major asset classes, and the creation of several others.

But I would warn against taking backtests too seriously. Over the past 2 years, bull cases for bonds that have relied on macro backtests have aged very poorly.

You never get to walk in the same river twice, because the river is different, and so are you.

I’ve often found that headlines such as “chaos in the bond market” often mark the end of the chaos, rather than its beginning. This sentiment analysis would suggest that bond yields may find a local top in early October. The only issue is that the investors who recently have been taken to the woodshed just a few days ago thought the exact same thing.

About the Author:

Jack Farley is a videojournalist at Blockworks and host of the Forward Guidance podcast.