By Luis Olguin, CFA, emerging markets corporate portfolio manager on William Blair’s emerging markets debt (EMD) team.

Corporates are becoming an ever more important part of emerging markets hard currency debt investments. In this video, Luis Olguin, CFA, a portfolio manager on William Blair’s emerging markets debt (EMD) team, explains the advantages of a corporate allocation to emerging debt portfolios; how investors navigate corporate risks, which are different from sovereign risks; and our approach to making a corporate allocation to emerging markets hard currency debt portfolios.

Watch the video or read the recap: Why Corporate Credit in an Emerging Markets Debt Portfolio? - William Blair

Corporates are becoming an ever more important part of emerging markets hard currency debt investments.

What are the advantages of a corporate allocation to emerging markets debt portfolios?

There are several advantages to a corporate credit allocation in the current market environment.

First, corporates are predominately of lower duration than sovereigns—a key performance driver in times of higher and more volatile interest rates.

Second, over 80% of the corporate bonds we analyze currently trade at a positive spread to their respective sovereign. For a manager that is able to appropriately navigate these credit risks, this additional yield can be additive to performance.

Third, the diversity of corporates also provides for an assortment of investment drivers above and beyond a sovereign’s credit quality. While sovereign risk is a driver of corporate bond returns, corporate credit drivers can at many times dominate, particularly when the sovereign credit landscape is stable or improving.

How do you navigate corporate risks, which are different from sovereign risks?

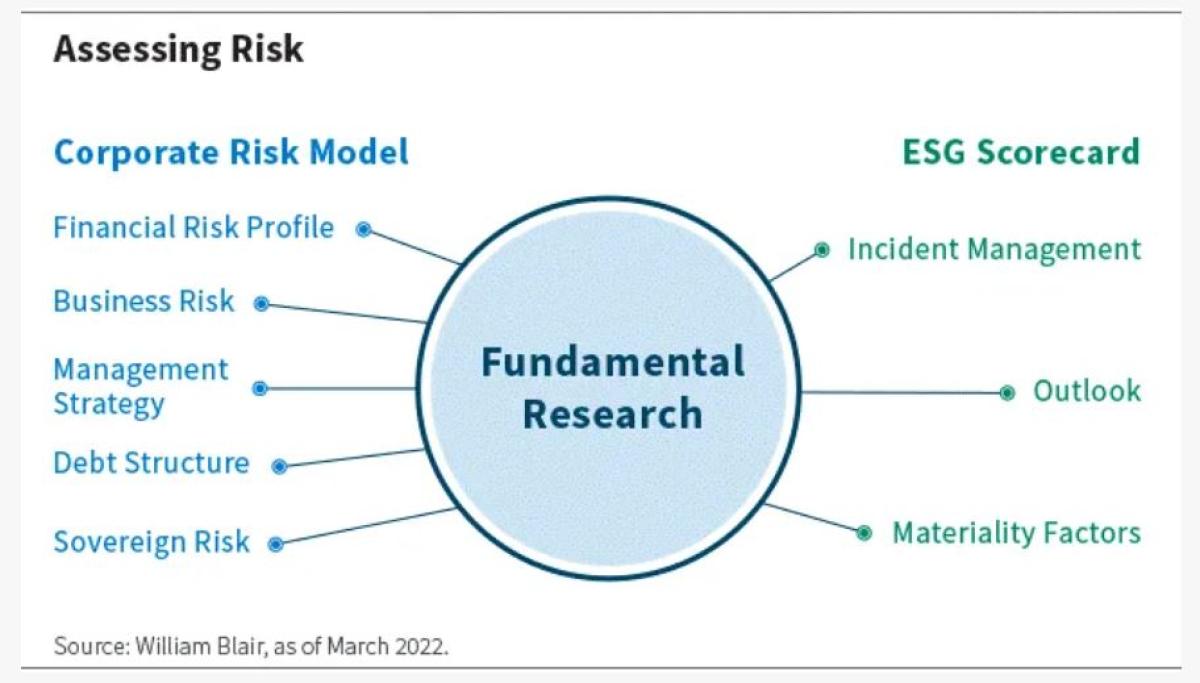

We assess corporate fundamental risks through our corporate risk model and environmental, social, and governance (ESG) scorecard.

Our corporate risk model views credit risks through a multi-angle approach.

We look at an issuer’s financial risk through a financial model with a focus on credit trajectory and potential downsides.

An issuer’s business risk is annualized by studying its industry’s competitive environment and the issuer’s market position within it.

We assess a company’s management strategy by scoring its policies, track record, and growth plans.

One of the most important risks in corporate analysis is the debt structure risk. This looks at an issuer’s maturity profile and its debt composition, which is crucial to assess the likelihood of default.

Last but not least, we assess the issuer’s degree of sovereign-related risks by examining the country’s macro, political, and regulatory environment, as well as the probability of a sovereign ratings change given their effect on corporate issuer ratings.

Our ESG scorecard is our tool to analyze an issuer’s ESG risks. We have built this scorecard based on SASB materiality factors, our assessment of what is material, and a double materiality framework based on sustainability and business impacts. Our analysis is done through informational engagement with issuers and complemented with third-party sources leading to an overall score for ESG pillars, an incident management assessment, and an outlook for the issuer.

What is your approach to making a corporate allocation to emerging markets hard currency debt portfolios?

Blair's process begins by taking the sovereign and corporate universes and applying ESG-related exclusions for global norm violators and controversial sectors, as defined by William Blair’s internal policies.

We then duration match corporates and sovereigns by country and by applying our proprietary beta-bucketing approach.

Using external ratings as a guide, we limit the max credit rating differential as a way to limit excess credit risk.

We then run a valuation screen, focusing on the historical spread relationship between the corporate and sovereign. This is important as we aim to enter a trade when historically more attractive.

Our fundamental analysis now takes a key role. Using our corporate risk model and ESG analysis, our analyst team provides their fundamental assessment of the issuer. This assessment and the valuation screen are then reviewed on a monthly basis by portfolio managers for potential investment.

Complementing this process is our ongoing monitoring as well as our formal bi-weekly performance assessment, which is performed by the whole emerging markets debt (EMD) team in an open discussion.

Read the original research here.

About the Author:

Luis Olguin, CFA, is an emerging markets corporate portfolio manager on William Blair’s emerging markets debt (EMD) team.

He is also a member of the ESG leadership team for William Blair Investment Management. Before joining William Blair, he was a senior portfolio manager on NN Investment Partners’ EMD team. In that role, he had global portfolio management responsibilities for emerging markets corporate credit as well as analyst duties across the Latin American oil and gas, metals and mining, and industrials sectors. Previously, he was head of equities for AFP Habitat, a pension fund in Peru. During this time, he was also a professor at the University of Lima, where he taught several courses on investment management. Before that, he was a director with financial and managerial responsibilities for a family-owned conglomerate in Peru. He also spent eight years in fixed-income research and portfolio management roles at ING Investment Management (NN Investment Partners’ predecessor). Luis received a B.B.A. from Emory University’s Goizueta Business School.