By Steven Novakovic, CAIA®, CFA, Managing Director, Curriculum, CAIA Association.

My first exposure to the world of alternatives was in 2005, a time when hedge funds sat atop the world. The HFRI Composite index had only one negative year dating back to 1990, when the index fell a measly 1.45% in 2002. Further, many strategies with little to no beta—i.e., the group of strategies like Relative Value, Equity Market Neutral, etc., collectively referred to as absolute return—had yet to experience a losing year. The combination of a long history of sustained success and uncorrelated, absolute returns during a recessionary period, institutional investors were jumping headfirst into the hedge fund universe.

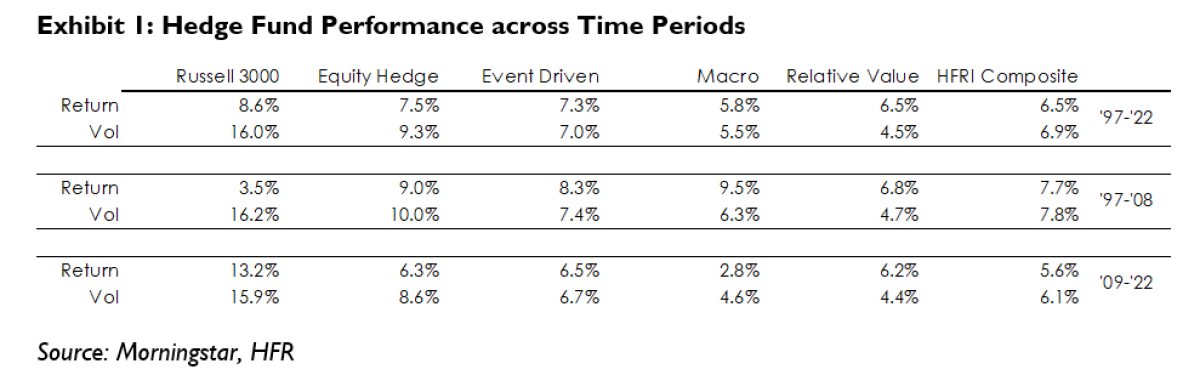

In retrospect, it seems as though I joined in at the tail end of the Golden Age. In the following years, the HFRI Composite index reported negative annual performance on five separate occasions and absolute return strategies struggled to generate, well, absolute returns. Exhibit 1 illustrates the tale of two hedge fund performance eras. From 1997 to 2008, hedge funds delivered exceptional absolute, relative, and risk-adjusted returns. While from 2009 to 2022, absolute, relative, and risk-adjusted performance all declined (and in the case of relative performance, was miserable). With much of this uninspiring performance taking place in tandem with a raging bull equity market, some institutional investors reversed course and gave up on hedge funds[i] by cutting allocations or outright exiting the universe.

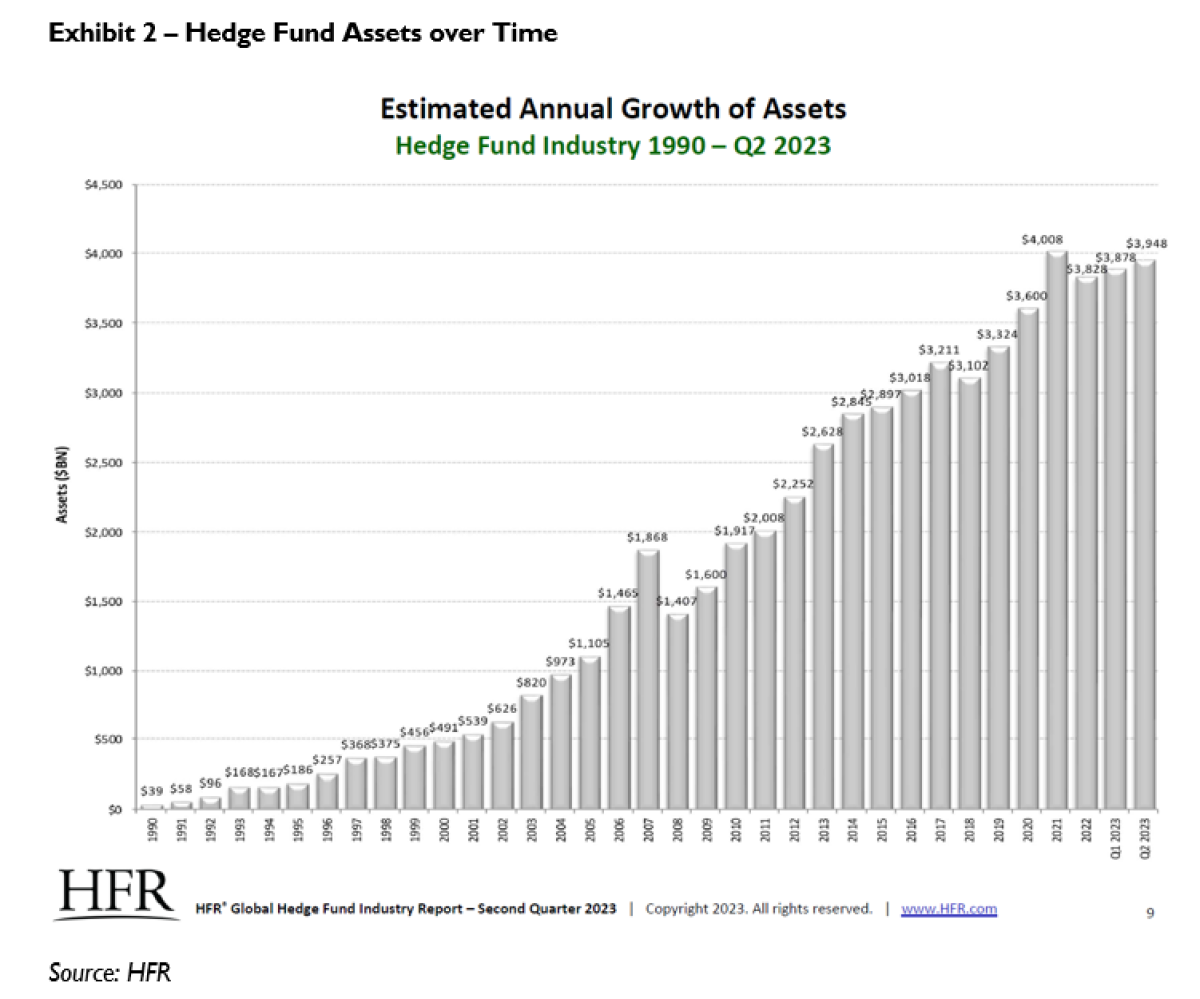

So, what happened? Why did hedge funds suddenly lose their mojo? Was it simply the classic story of too many investors rushing in, resulting in too many assets going after too few opportunities? Or perhaps, too many unqualified managers launched funds, thus diluting the overall universe performance? After all, prior to 2005, the hedge fund universe was still a relatively tiny corner of the market with less than $1 trillion in assets (see Exhibit 2). A decade later, the industry was nearly triple the size commanding almost $3 trillion. To answer that question, we need to critically evaluate and understand the underlying drivers of performance for hedge funds.

Hedge Fund Performance Attribution

For any investment, the total return can be broken into three components:

- cash

- beta

- alpha

Let’s consider each through the lens of a hedge fund.

Cash: Perhaps because we went over a decade in an environment with rates near zero percent, it was easy to forget how important a contributor cash can be to the return for hedge funds. Cash returns contribute to performance in two main ways:

Short Rebate: when shorting a security, investors are required to hold cash collateral in their brokerage account. This collateral is often invested in cash-like securities and earn interest. A portion of this interest is then passed along to the short seller in the form of a short rebate.

Unencumbered Cash: at any given time, investment managers will maintain a cash balance that is typically low single digits; however, hedge funds that invest in derivatives markets tend to keep higher levels of cash on hand given the high use of margin with derivatives. This balance is held in cash-like securities and earns interest.

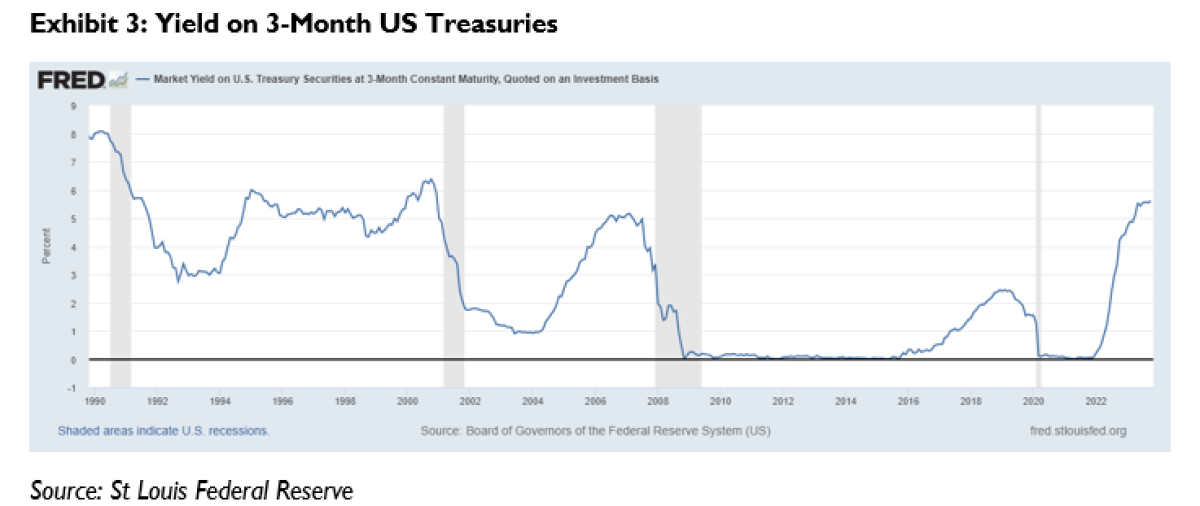

Everyone knows the story, that from 2009 through 2022, short-term interest rates were near zero, excepting a brief stretch from 2016 to 2020 when they reached a peak of 2.5%. Often forgotten, is how “high” rates were prior to 2008, notably investors survived much of the 1990s with rates above 5%.

One of my favorite stories on hedge fund return attribution is related to the cash return component. I was conducting due diligence on an equity hedge fund manager, and they provided performance attribution on a per year basis broken into three categories: “Longs”, “Shorts”, and “Other”. The footnote for “Other” indicated this included “management fees, expenses, and other items.” Unsurprisingly, this “Other” category contributed negatively to fund performance in every year except one, in the early 2000s. I asked the manager what happened that year, did they cancel all management fees that year and instead pay LPs to invest in their fund? As it turned out, the hedge fund manager had a rather substantial short book that year, and the short rebate earned during that time more than offset the management fees and expenses incurred throughout the year. Amazing! Can you even imagine? (Also note the hedge fund manager didn’t keep the short rebate for themself – how admirable.)

That story helps explain why, when I started, the common benchmark for absolute return strategies was T-bills + 5%. It was understood (and expected) that as a base, these strategies should generate a cash return, simply due to the structure/mechanics of hedge fund investing. Furthermore, early in the hedge fund industry, it was more common to see incentive fees accompanied by hard hurdle rates equal to cash. A clear recognition by the manager that they earn a cash return as a baseline and should not receive an incentive fee on cash interest.

Today, far fewer hedge fund managers have retained this compensation structure in their legal documents. For more than a decade, the lack of a cash hurdle was immaterial, and this omission easily went unnoticed. However, with cash rates nearing 5%, this omission can be quite costly. Applying a 20% incentive fee when capturing a full 5% cash rate results in net returns 1% lower. If we expect hedge funds to generate mid-to-high single digit net performance, this 100 bps fee drag represents a material reduction in absolute returns.

I would not expect higher interest rates to cause hedge fund managers to become introspective and proactively (re)introduce cash hurdles into their incentive fee structures. Instead, it will be incumbent upon LPs to push back and require the inclusion of a hard hurdle. Certainly, some GPs will call the LPs bluff, but with 9,000+ hedge funds to invest in, perhaps LPs should focus their attention on those committed to abiding by the “Partner” in General Partner.

Beta: By definition, absolute return strategies should exhibit little to no beta to equity and/or fixed income markets. In practice, this tends to play out, albeit with some strategies still maintaining modest beta (i.e., 0.2). Irrespective, LPs should not seek or expect meaningful beta capture in these strategies. (Side note: LPs should be vigilant in uncovering “hidden” beta in absolute return strategies and take due action.) Given that, what’s the point of discussing beta and hedge funds? Because beta (or the lack thereof), plays a significant role when analyzing relative returns.

When beta markets exhibit modest returns (as was the case from 1997 to 2008), having a (near) zero beta isn’t a major hinderance. However, when equity markets, for example, go through a period of robust returns like we experienced from 2009 – 2022, the lack of beta is a major relative headwind. During this 11-year period, absolute return strategies effectively generated 0% from their cash return and 0% from beta. All while equity beta compounded at 13% per year. That placed all the performance weight for hedge funds on the shoulders of alpha. Good luck finding 13% annualized (net of fees) alpha in just about any market. Hedge funds were doomed to exhibit poor relative performance over that time period. From 1997 to 2008, even in the absence of alpha, hedge funds would have looked relatively decent, given a positive cash return and weak performance in beta markets.

Alpha: Historically, this is why LPs were willing to pay hedge funds a 20% incentive fee…for an uncorrelated return stream produced via skill and expertise that cannot be replicated in other fund structures or traditional investments. In absolute return strategies, how do hedge funds apply this unique expertise in their portfolio? While there are several manifestations, identifying (mis)valuation spreads between two or more securities is a commonly understood trade. This could be via M&A arbitrage, convertible arbitrage, a variety of other arbitrage strategies, carry trades as seen in macro funds, or simply in a market neutral long/short equity fund via pair trades. An entire category of hedge funds (relative value) is dedicated to earning a return on spread conversion.

These spreads exist due, in part, to market inefficiencies. There is no question, over the last two decades markets have become increasingly efficient, whether through the growth of technology, the increase in the number of hedge fund managers, or the changes in market regulations, among other tailwinds. It is hard to argue that markets are as inefficient today as they were back when Ken Griffin (founder of Citadel) was trading convertible bonds in his dorm room in 1989. As such, I would argue that T-bills + 5% is no longer realistic for an absolute return hedge fund benchmark, simply recognizing increased efficiency in markets.

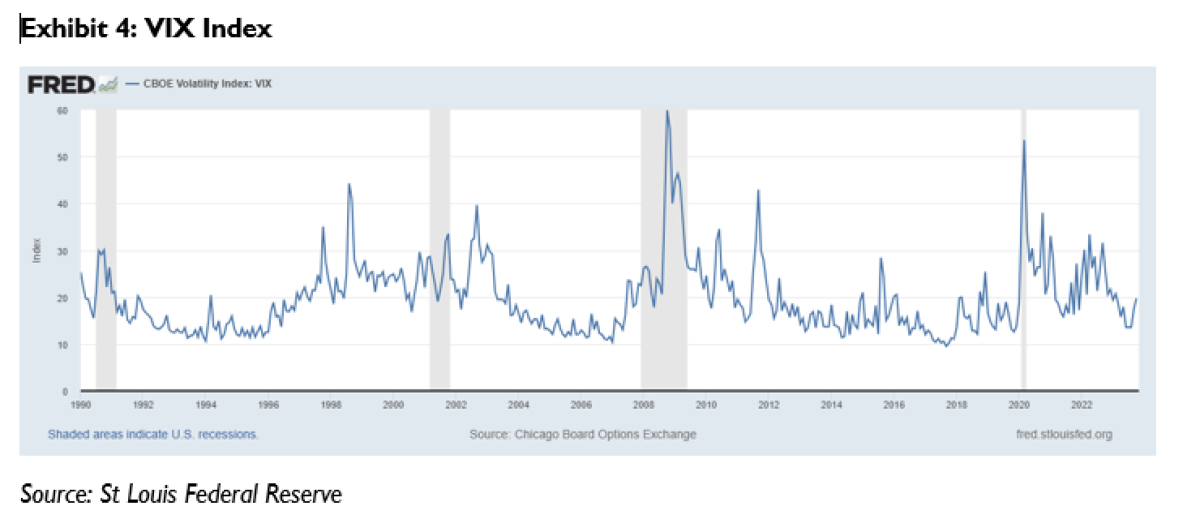

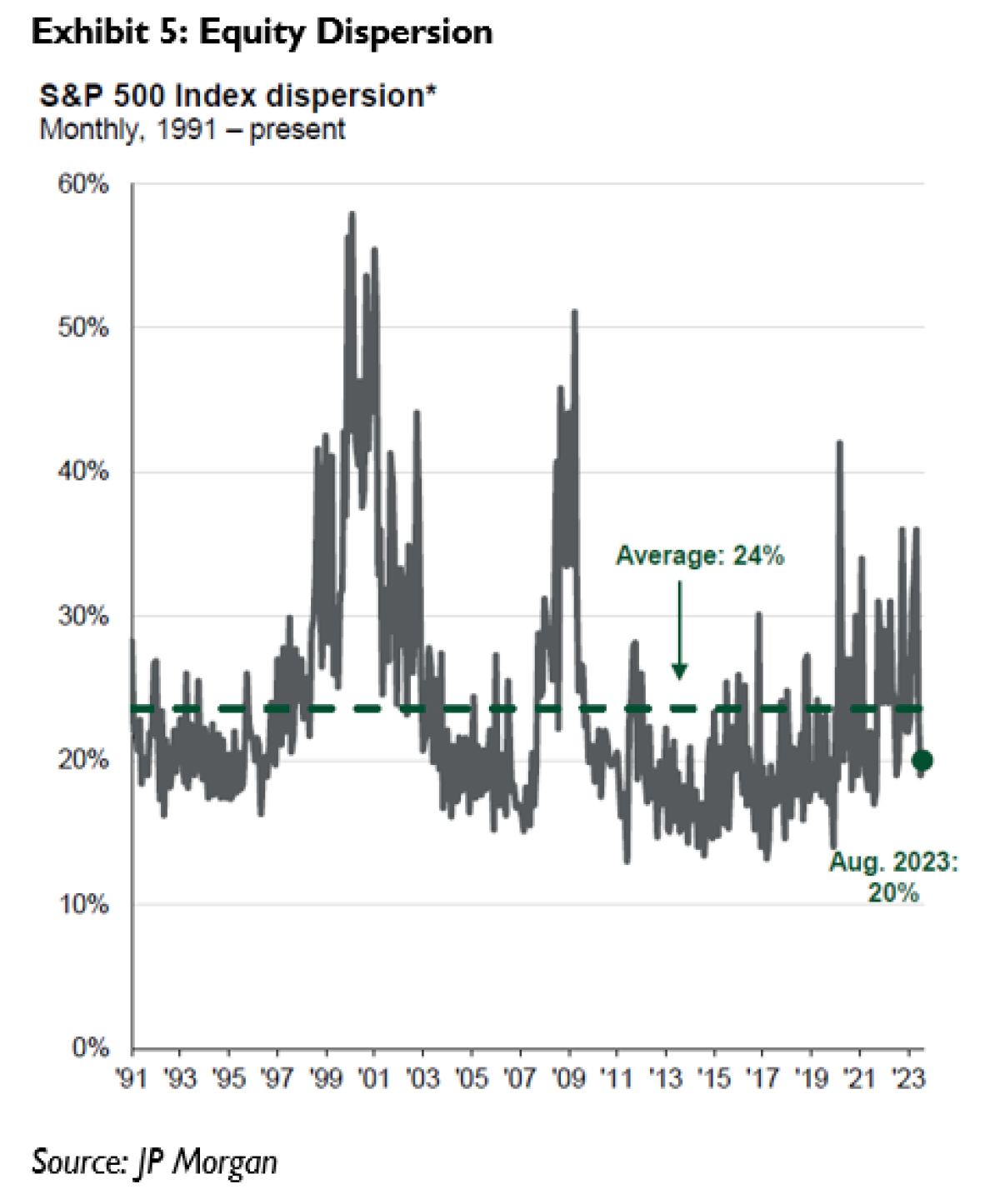

However, irrespective of market (in)efficiency, spreads also widen and narrow over time simply due to regular market movements, driven in part by volatility. Related to volatility is the concept of dispersion, or the degree of variation in the returns of securities (which contributes to valuation spreads). Research shows a strong correlation between alpha and dispersion[i] and a strong link between volatility and dispersion.[ii] Greater volatility and dispersion in the market is likely to lead to wider spreads and a larger opportunity set for relative value hedge fund strategies.

You may not be surprised to see this, but volatility (Exhibit 4) and dispersion (Exhibit 5) were more favorable pre-2008 than post 2008.

Volatility and dispersion ticked up in 2022, before declining again in 2023, and as it turns out, 2022 was one of the best years for hedge funds on a relative basis, while 2023 is shaping up to be a ho-hum year.

Bringing it all together

All of this to say, I’m not calling for a hedge fund renaissance, nor the return of the 1990’s era of performance. However, for investors who swore off hedge funds and vowed never again, this may be a time they’re worth revisiting. The lens from 2009 to 2022 was understandably awful for hedge funds. Given the trifecta of zero interest rates, raging beta markets, and low volatility/dispersion (combined with greater market efficiency), absolute return hedge funds didn’t stand a chance.

Where we stand today, with interest rates (possibly) higher for longer, normalized expectations for beta, and more reasons for volatility (heightened geopolitical risks, inflation, interest rate uncertainty, etc.), Cash + Beta + Alpha may add up to something worth investing in.

[i] https://www.reuters.com/article/us-pensions-calpers-hedgefunds/calpers-dumps-hedge-funds-citing-cost-to-pull-4-billion-stake-idUSKBN0HA2D120140916

[ii] http://www.hedgefundinsight.org/longshort-equity-outlook-improving-on-correlation-and-dispersion-changes/

[iii] https://www.spglobal.com/spdji/en/documents/research/research-dispersion-measuring-market-opportunity.pdf

About the Author:

Steve Novakovic, CAIA, CFA is the Managing Director, Curriculum for CAIA Association. In this role, he is responsible for managing the CAIA Charter curriculum, ensuring the content remains relevant and reflects current trends in the institutional asset allocator space. He joined CAIA Association in 2022 and has been a Charterholder since 2011. Prior to CAIA Association, Steve was a faculty member at Ithaca College in Ithaca, NY, where he taught a variety of finance courses including Cryptocurrencies, Alternative Asset Management, and Wealth Management, among others. Before entering academia, he worked at his alma mater, Cornell University, (B.S. 2004, MPS 2006) in the Office of University Investments. In his time at Cornell University, Steve invested across a variety of asset classes for the $6 billion endowment. His twelve years at Cornell generated substantial insight into endowment management and fund investing across the alternatives and traditional landscape.