By Kathryn M. Kaminski, Ph.D., CAIA®, Chief Research Strategist, Portfolio Manager and Jiashu Sun Junior Research Scientist at AlphaSimplex.

Introduction

For the last few decades, if you asked when shorting bonds would be the trade of the year, you might get the classic response: when pigs fly. I guess we can say that pigs have been flying around in 2022—the short bond trend was a big mover last year. Although rates have been increasing, few strategies are short bonds outside trend following. Historically, short positions have not worked out well for those who took them on. To put this into perspective, Figure 1 plots the average quarterly return of a trend-following strategy in fixed income from 1990 to 2022, decomposed by periods with net long or net short positions in the asset class. On the right-hand side, we also note that prior to 2022, trend following has only been net short fixed income roughly 24% of the time versus roughly 76% long from 1990 to 2021. In comparison, the typical return for being net short in 2022 has been highly positive compared to the other 31 quarters since 1990 in which trend followers held short positions in fixed income. The contrast in performance from shorting bonds seems to indicate either a fluke or some sort of structural shift. Given that shorting bonds has been an investment pariah until 2022, we revisit some common myths and misconceptions for shorting bonds to help clarify why, when, and how often trend followers may be shorting bonds in the future.

Figure 1:

Two common myths and misconceptions about shorting bonds 1. Shorting bonds never works. 2. Higher rates mean trend followers will continually short bonds.

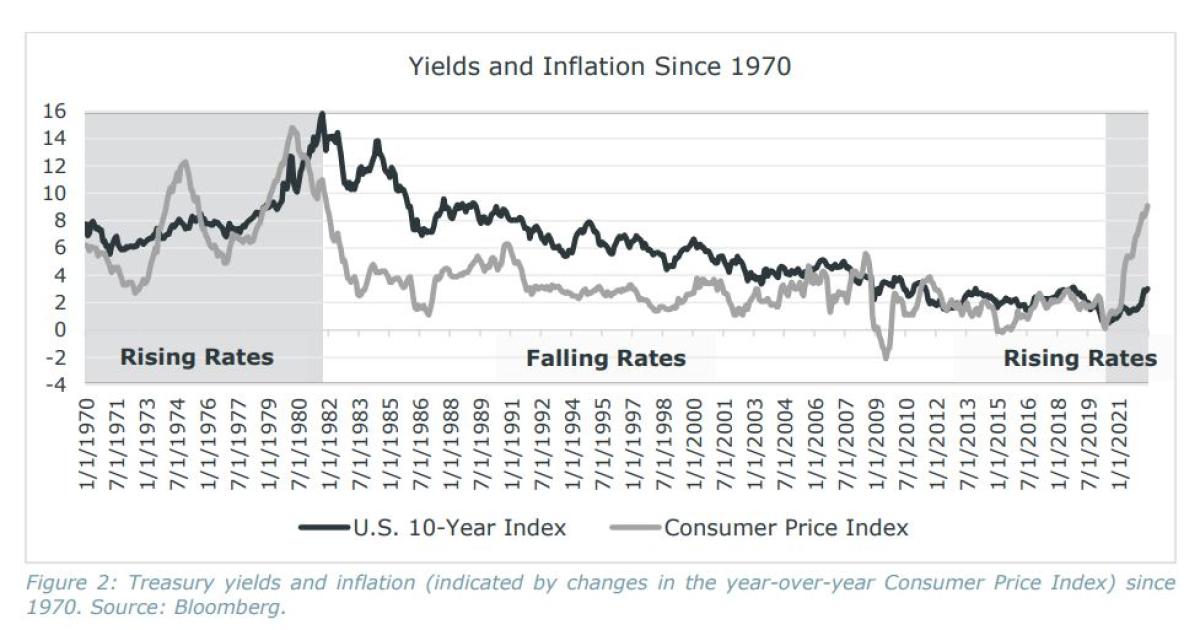

Myth #1 Shorting bonds never works. During the last 40 years, since 1982, we have generally been in a falling rate environment with very low inflation. Given this backdrop, it is not surprising that shorting bonds would not work well. Put simply, when rates fall, on average prices go up and it is generally better to be long. It may be instructive to look even further back to include a time period with both falling and rising rates. To do this, Figure 2 plots the U.S. 10-Year yield since 1970 versus inflation, for contextual reference. We denote three periods on this graph based on the peak and trough for interest rates (1) rising rates 1970-1982; (2) falling rates 1982-2020; and (3) 2021- present.

Figure 2:

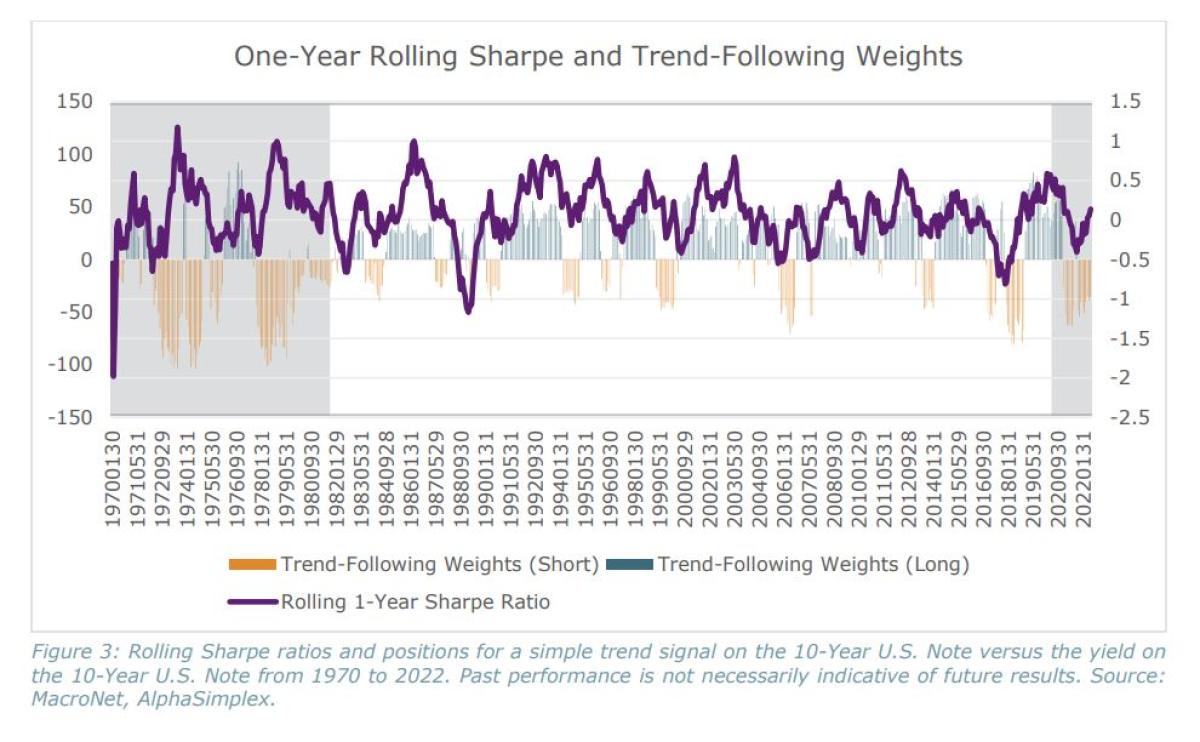

To examine how a trend-following strategy might perform and what position it might take in fixed income, we consider the U.S. 10-Year Note and create a synthetic futures return series to examine the signal direction over varied interest rate regimes since 1970. Figure 3 plots a typical trend signal (long/short) and its rolling Sharpe ratio using the U.S. 10-Year Note from 1970 to 2022. We note a few features. First, during the rising rate period the strategy is more often short, and vice versa. Second, the Sharpe ratio is generally positive across time, suggesting that during a rising rate environment it might be favorable to be short and in the falling period it might be favorable to follow long trends.

Figure 3:

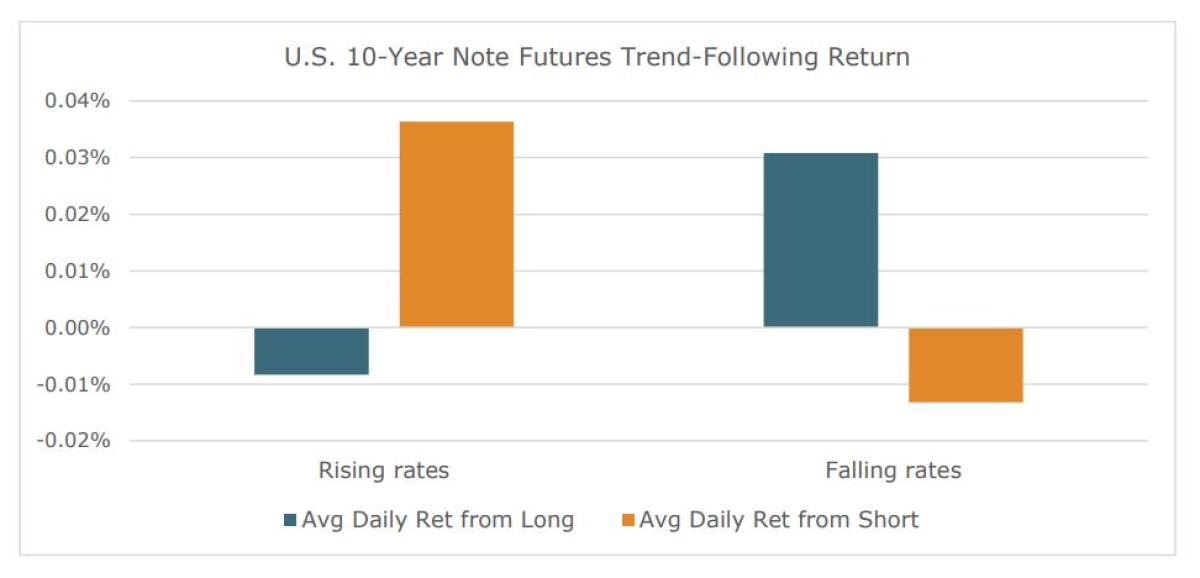

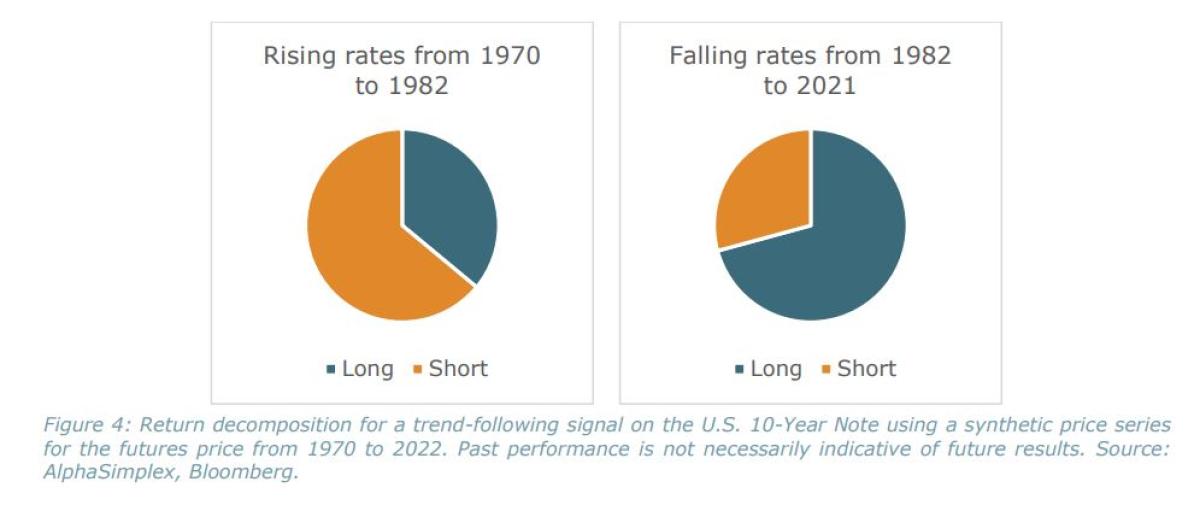

To examine performance more explicitly by regime, Figure 4 plots the average monthly return decomposed by long or short for both rising and falling rate environments as well as the frequency of being long or short. From this graph we can see clearly that during the falling rate period the strategy tended to be long more often (71% vs 29%) and to have better returns when long. On the other hand, during the rising rate environment, the strategy is more often short than long (64% vs 36%) with better returns from short positions.

Figure 4:

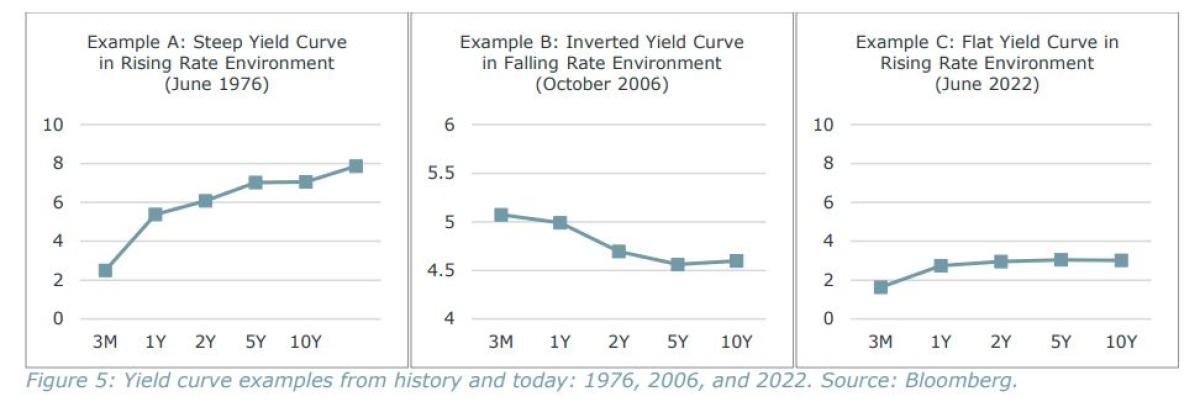

Reality: Shorting bonds doesn’t work well in a falling rate environment but can work well in a rising rate environment. Myth #2 Higher rates mean trend followers will continually short bonds. Using a longer data set, we found that trend following will favor short signals in rising rate environments and long signals in falling rate environments. These are general themes; during both rising and falling rate periods market conditions have also varied across business cycles and through different macroeconomic trends. Across these periods, it is not only the level of interest rates that matters but also the slope of the yield curve. Figure 5 plots three different yield curves to demonstrate why the slope may also matter. From Figure 5, we note different types of curves: inverted, flat, and steep. Inverted curves occur when short-term interest rates are higher than longer-term interest rates, which is often seen as a sign of a recession. Flat curves suggest little-to-no term premium for holding longer-term bonds, while a steeper yield curve implies a term premium for holding longer-term debt. The shape of the curve can vary over regimes. For example, we can see steep yield curves in a rising rate environment (Example A) or inverted curves during a falling rate environment (Example B). The current yield curve is roughly flat but has slightly inverted for short periods, as in the month of June 2022.

Figure 5:

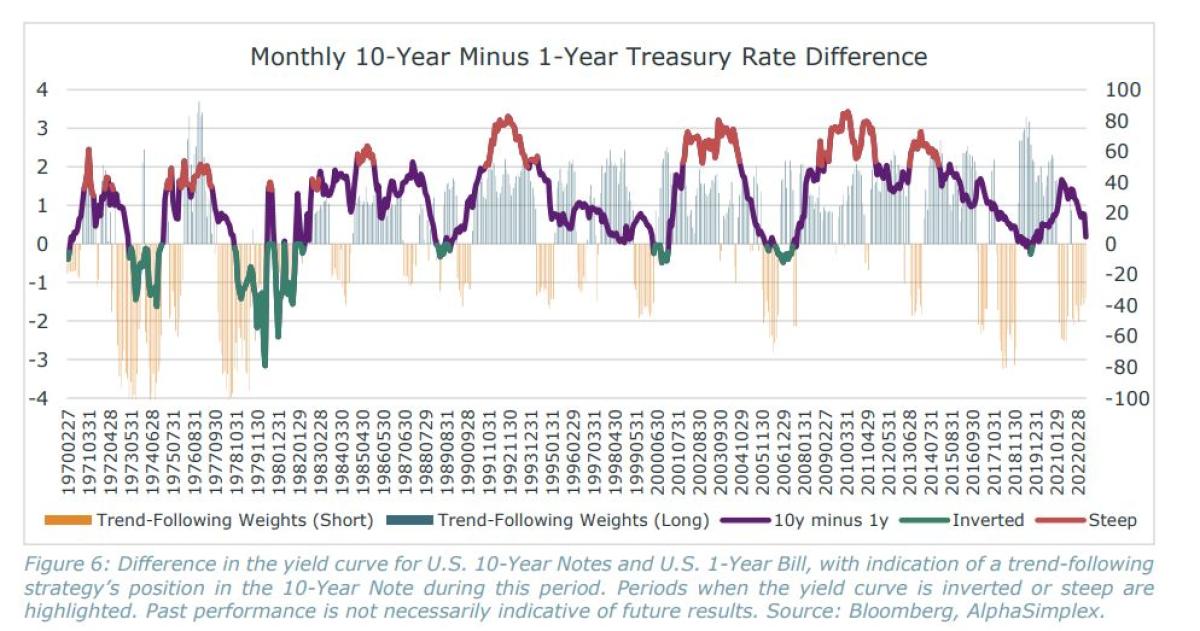

To examine this in more detail, we can consider the slope of the yield curve and consider how trend signals might behave. Figure 6 plots the slope of the yield curve versus typical trend positions in the U.S. 10-Year Note, highlighting inverted and steep periods in history over both rising and falling rate periods. From this figure, we can see that a trend strategy tends to be short when the yield differential is low, decreasing, or even inverted. In contrast, when the curve is steep the trend signal has tended to be long.

Figure 6:

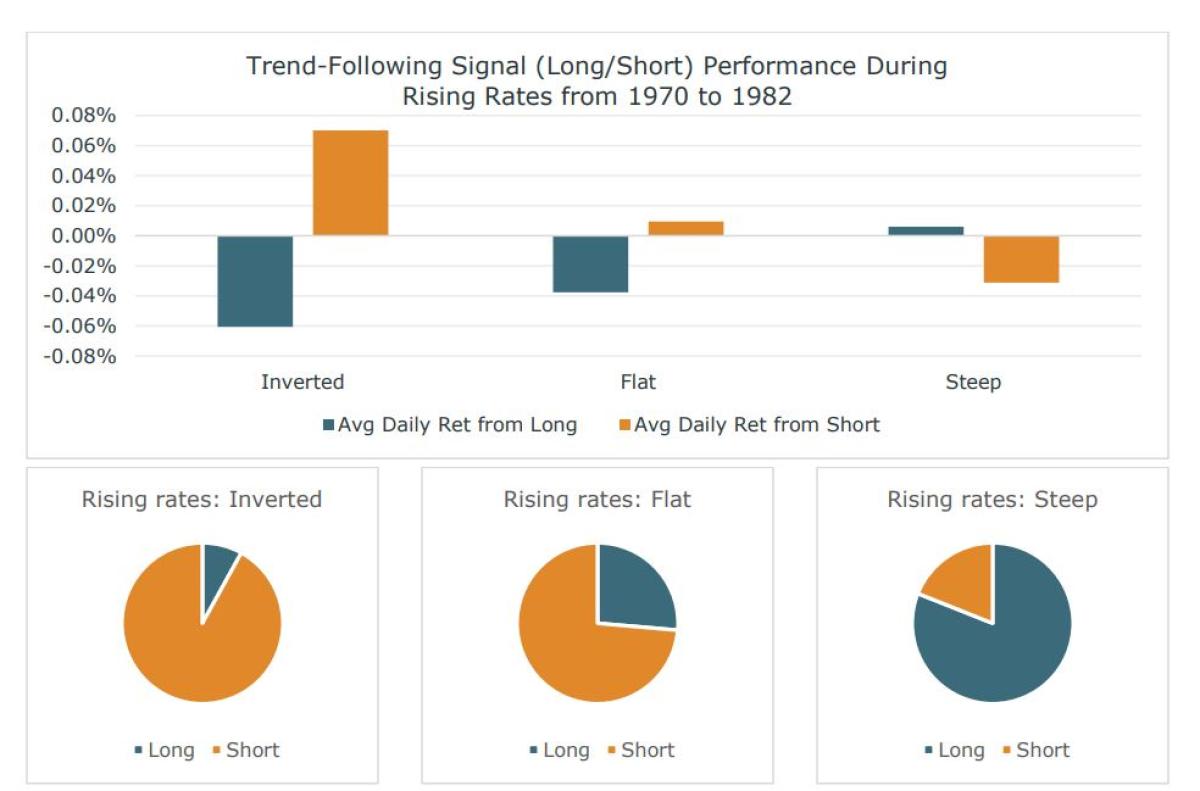

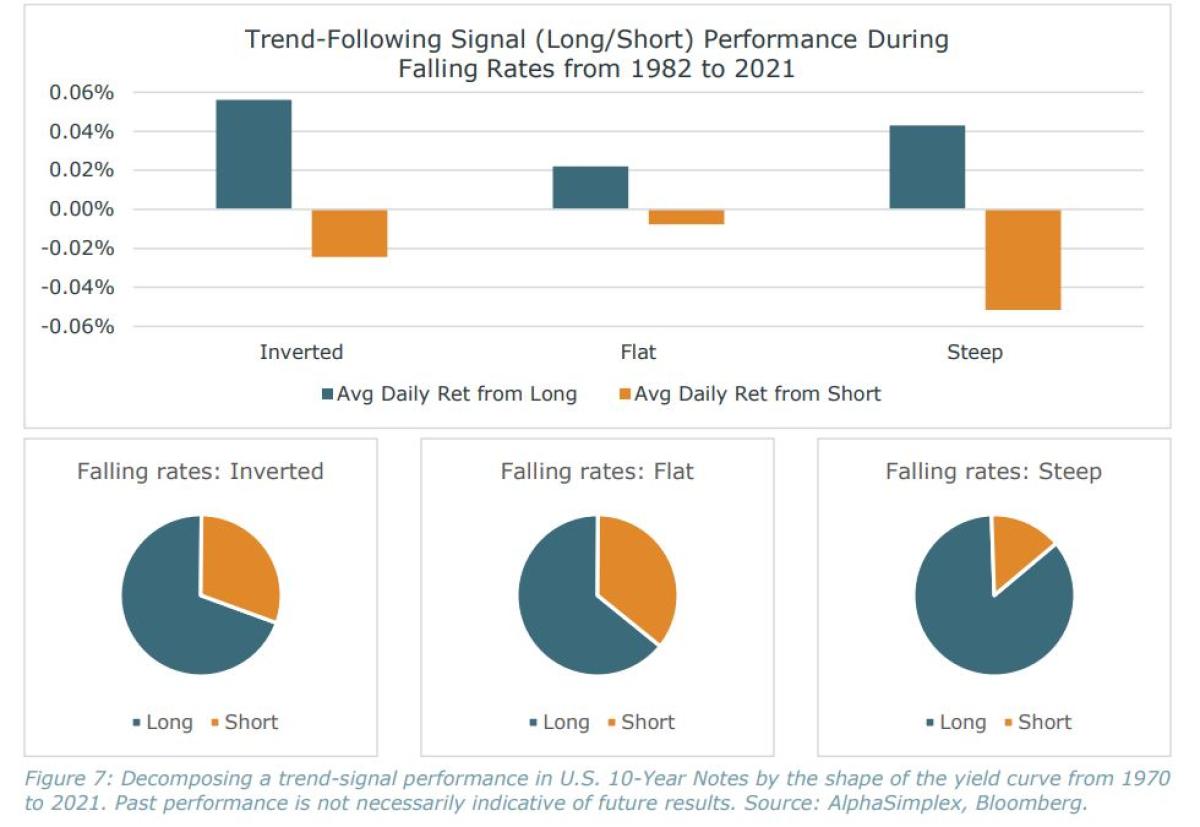

The next question we could consider is whether it would have been preferable to be long or short during these different scenarios, similar to the analysis in Figure 4. Figure 7 summarizes some key statistics for trend following in bonds during periods with different yield curve shapes (inverted, flat, or steep) for both falling and rising rate periods.

Figure 7:

From Figure 7, we see a distinctly different pattern for falling rate periods versus rising rate periods. In general, being long has been positive over the entire falling rate period regardless of the shape of the yield curve. Over time, trend strategies have tended to be long, particularly when curves are steep or flat. During rising rate periods, the results for long or short signals are more mixed. Short signals are more common and preferable during periods when the curve is inverted or even flat.

On the other hand, during a rising rate environment when the curve is steep, long positions are more common and better performing than short positions. This demonstrates that when we are in a rising rate environment, it can be preferable to take short positions—unless we see higher rates and a steep yield curve, when it may be preferable to be long despite a rising rate environment. Overall, Figure 7 highlights the point that both long and short positions can lead to positive (or negative) performance, depending on both the rate environment (rising or falling) and the shape of the curve (steep, flat, or inverted). The benefit of a trend-following strategy is that it can take either long or short positions in bonds, depending on prevailing trends, either of which may lead to positive performance during different rate environments and various yield curve shapes. Reality: It is the change in rates that impacts trend positions, not the level. Trend following can be either long or short during rising rate environments, depending on the shape of the yield curve.

Summary

The first half of 2022 favored short bond trade as markets seem to signal a structural change in interest rate regimes.

During the recent 40-year period of low inflation and falling interest rates, shorting bonds has generally been seen as a foolish trade. In this paper, we consider two common myths and misconceptions of shorting bonds. We demonstrate that trend-following strategies will tend to be best suited to taking short positions in bond markets when rates are rising and/or the curve is inverted; by contrast, these strategies tend to be long bonds when rates are falling and/or the curve is steep. This analysis demonstrates that if we are truly in a rising rate environment, shorting bonds will not just be a fluke but a common theme for trend strategies as rates continue to rise.

About the Author:

As Chief Research Strategist at AlphaSimplex, Dr. Kaminski conducts applied research, leads strategic research initiatives, focuses on portfolio construction and risk management, and engages in product development. Dr. Kaminski is a member of the Investment Committee.

She also serves as a co-portfolio manager for the AlphaSimplex Managed Futures Strategy and AlphaSimplex Global Alternatives Strategy. She has over 10 years of industry experience. Dr. Kaminski joined AlphaSimplex in 2018 after being a visiting scientist at the MIT Laboratory for Financial Engineering. Prior to this, she held portfolio management positions as a director, investment strategies at Campbell and Company and as a senior investment analyst at RPM, a CTA fund of funds. Dr. Kaminski co-authored the book Trend Following with Managed Futures: The Search for Crisis Alpha (2014). Her research and industry commentary have been published in a wide range of industry publications as well as academic journals. She is a contributory author for both the CAIA® and CFA® reading materials. Dr. Kaminski is a Senior Lecturer at the MIT Sloan School of Management and has taught at the Stockholm School of Economics and the Swedish Royal Institute of Technology, KTH. Dr. Kaminski earned an S.B. in Electrical Engineering and Ph.D. in Operations Research from MIT where her doctoral research focused on stochastic processes, stopping rules, and investment heuristics. Dr. Kaminski is also a CAIA® Charterholder

As a Junior Research Scientist at AlphaSimplex, Ms. Jiashu Sun focuses on applied research and supports the portfolio management teams.

Ms. Sun joined AlphaSimplex in 2021. Prior to this, Ms. Sun gained experience as a research assistant at the Columbia Business School and the University of Chicago Booth School of Business. At the Columbia Business School, Ms. Sun worked on worked on structural estimation models, hedge fund activism, and portfolio specialization. Ms. Sun earned both a B.A. in Finance from Peking University as well as an M.S. in Financial Economics from the Columbia Business School.