By Arnim S. Holzer, Global Macro Strategist and William Visconto, Co-Founder, Portfolio Manager at Easterly/EAB Risk Solutions.

Much attention has been paid of late to the building of diversified portfolios to smooth out performance through the reduction of meaningful drawdown. This analysis looks at asset allocation and the importance of understanding the correlations of portfolio assets in arriving at more effective diversification for investors. Particular attention is paid to the relationship of fixed income as a diversifier in equity bear markets and the circumstances where its diversification value may erode.

Correlation volatility as expressed by the range of correlation is presented as an indicator to predict portfolio performance under stress. While some investment practitioners may also look at Beta and Covariance as important portfolio tools, this paper focuses on the fundamental factor of correlation as it is the driving force of directional offset. The analysis shows the benefit of incorporating consistent negative correlation exposure into the equity component of portfolios as an alternative to using fixed income to improve diversification during stressed markets. This approach appears to be a more consistent diversifier than fixed income. Specific attention is paid to the credit sector’s tendency to fluctuate in correlation to equities as well. Equity volatility under stress can be extremely disruptive. This analysis considers the value of systematic dedicated and stable negative correlation hedging within the equity sleeve of allocation in contrast to solely relying on the less stable negative correlation of the fixed income portion of the fixed income allocation. Suggestions for defensive equity allocations within a diversified portfolio are considered.

- Asset correlations are critical to the success of asset allocation performance.

- Correlations are much less stable and reliable than commonly perceived.

- Fixed income, traditionally a solid diversifier is vulnerable due to the low interest rate environment and may not offer much diversification benefit in a rising rate environment.

- Equity put strategies provide consistent negative correlation, particularly in stress events.

- Investors’ significant increase in lower quality fixed income potentially leaves them more vulnerable from a correlation perspective to equity moves.

- Synthetic strategies, such as a hedged equity approach, combining equity exposure and put overlay provide consistent portfolio diversification and opportunity for return.

- Given the low interest rate environment, there are risks that fixed income does not provide anticipated diversification. Blending hedged equity into portfolios could notably improve portfolio diversification.

Asset Allocation and Portfolio Diversification:

Will expected portfolio returns look like the past?

For the past 68 years advisors have been turning to Professor Markowitz’ Modern Portfolio Theory to reduce risk and improve the quality of investor portfolio returns. The important takeaway for investors is that blending the right assets in the optimal way can improve the risk and return of a blended portfolio over less diversified portfolios. Originally known as the theory of portfolio choice, the approach takes into account the forecast returns, volatility, and correlations of assets to arrive at optimal portfolios.

Less than 60 years ago work derived from Professor William Sharpe’s Capital Asset Pricing Model postulated that the return of an asset should be related to its risk. Expression of market risk often combines volatility of returns, forecasted returns, and correlation history to determine the best mix of assets. In order to manage the overall risk of disappointing their clients, advisors and managers have focused on keeping absolute and relative volatility low to improve the relationship between return and risk. Given the SEC disclaimer that past returns (and we extend it to correlations) are not indicative of future performance in making investment decisions, it is no surprise that actual experienced portfolio returns do not resemble the smooth forecasts provided to clients. Obviously, it is difficult to predict returns on individual stocks or the market in general. Another major issue is human behavior. Investors tend to panic sell at market bottoms and panic buy at market tops. This might not be the case if investors had faith in their diversification methodology and its soundness.

For investors it is asset class correlations that matter:

Volatility is the speed, but correlations are the road map

There has been much focus by advisors on managing overall portfolio volatility for their clients to eliminate the bumpiness of the performance ride. The thought that throttling down volatility alone may limit losses is inadequate and may be misleading to investors. A more important factor in asset allocation may be understanding both the stability and consistency of asset correlations in portfolios.

This is particularly true during stress events. While some investment practitioners may also look at Beta and Covariance as important portfolio tools, this paper focuses on the fundamental factor of correlation as it is the driving force of diversification. To reduce the risk of major drawdown, correlation is more important than forecasting the volatility of the markets or the asset classes perfectly. If volatility is incorrectly forecasted but correlations remain stable, there should be an offsetting asset that diversifies the volatility effectively. In essence, volatility is the speed of the car on a trip, but the asset correlations are the road map that guides the driver. If correlations (or the relationships between asset classes or funds) do not remain stable, a portfolio we think is diversified may actually perform very differently than projected. This is the dilemma of diversification under stress. This effect has been noted by many in the asset allocation world and has led to an almost uniform rejection of the static 60/40 rule for asset allocation. Investor portfolios tend to correlate much more than we expect under stress and that can cost portfolios tremendous value over time. So, while Modern Portfolio Theory and efficient portfolios are valuable planning tools, they rely significantly on forecasts and the assumption of the stability of correlations. If the timing of returns is important to an investor (near retirement or later in life expectancy) or if significant risk is taken in a part of the portfolio (such as equity or lower quality credit funds) it needs to be hedged with less risky assets. We believe looking for consistently low or negatively correlated assets can prove to be very valuable, particularly in stressed markets. What we will look at in this analysis is the stability and range of major asset correlations to the S&P 500 with a focus on fixed income and credit sectors. Many investors have been using this approach as a primary source of income and diversification against their equity holdings. If an asset or asset class has a wide range of correlation potential, it by definition, provides a wider range of hedged outcomes versus a negative equity market. If an asset has a tighter range of correlation potential, the hedged outcomes should be more predictable.

Fixed income sectors correlations versus the S&P:

A picture is worth a thousand words

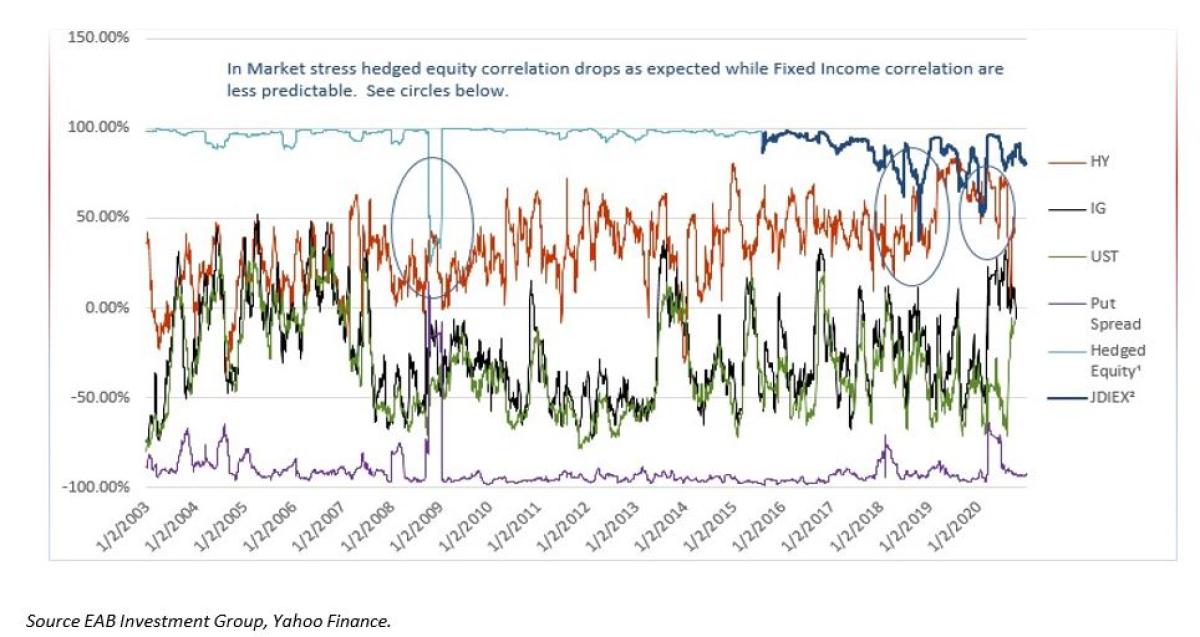

Fixed income has historically served two purposes in portfolios over the years. First, fixed income provides income to live off without having to sell principal, and secondly, fixed income historically provides a hedge that performs defensively when the economy or equities, in general, struggle. But over the past decade, with interest rates being lowered to zero or near zero, the fixed-income class has performed better than expected, increasing investor allocation in portfolios. As yields on Treasuries dropped, more importantly, investors have increased their allocations to corporate credit and non-investment grade credit to chase higher yields. This has created both principal gains (as interest rates drop) and solid income for investors as corporate yields maintain a spread over treasuries. This additional return, however, comes at a cost of lost diversification and greater correlation to equities. In contrast, an option-based hedged equity approach systematically reduces correlation to equities as equities drop significantly. This should be a consideration when evaluating diversifying strategies. As seen in the chart below the hedge equity approach responds quickly to equity downdrafts while the various fixed-income sectors have been more inconsistent. Surprisingly, the range of correlation (to S&P 500) variability is actually quite high and is an important consideration when evaluating portfolio diversification.

Chart 1. Long-term inter-asset trailing 3-month (60 trading days) correlations to S&P 500 since 2003

Contrary to popular belief and the assumptions of asset allocation models, the chart above illustrates that correlations are not particularly stable. Interestingly, the put strategy alone and the combination of the puts and the equity index (and JDIEX from its 8/31/2015 inception) were stable until the Lehman crisis, when the impact of the puts provided a reduction in correlation. In other words, the systematic use of options acts as a hedge to the equity portion of the portfolio. This diversification value stands in contrast to the other asset classes where correlations in some cases rose dramatically. Most notably (see circles), high yield moved from near zero levels in the weeks prior to the Lehman crisis to well over 40% trailing 3-month correlations in the months after. We see very similar behavior in the December 2018 and March 2020 periods. While it’s not the purpose of this document to forecast a crisis, it would seem to us that the holding of a fixed-income asset that has such a wide potential for correlation instability should be combined with a more diversified predictable hedge.

“Relying on the averages (correlation) could have precarious impacts should equities struggle.”

We theorize that correlation and the stability of correlation provide a better forecast of what could happen to a portfolio than a simple average or estimate of correlation. Looking at the data back to 2003, one can clearly see that investment corporate credit (the black line) and high yield (the red line), specifically show a very wide range of volatility, even turning significantly positive to equities periodically through history. High yield can possess a positive correlation to equity and has at times under times of stress. While average correlations could justify a significant allocation to high yield, it must be recognized that relying on the averages when stress correlations can have such a large effect could have precarious impacts should equities struggle.

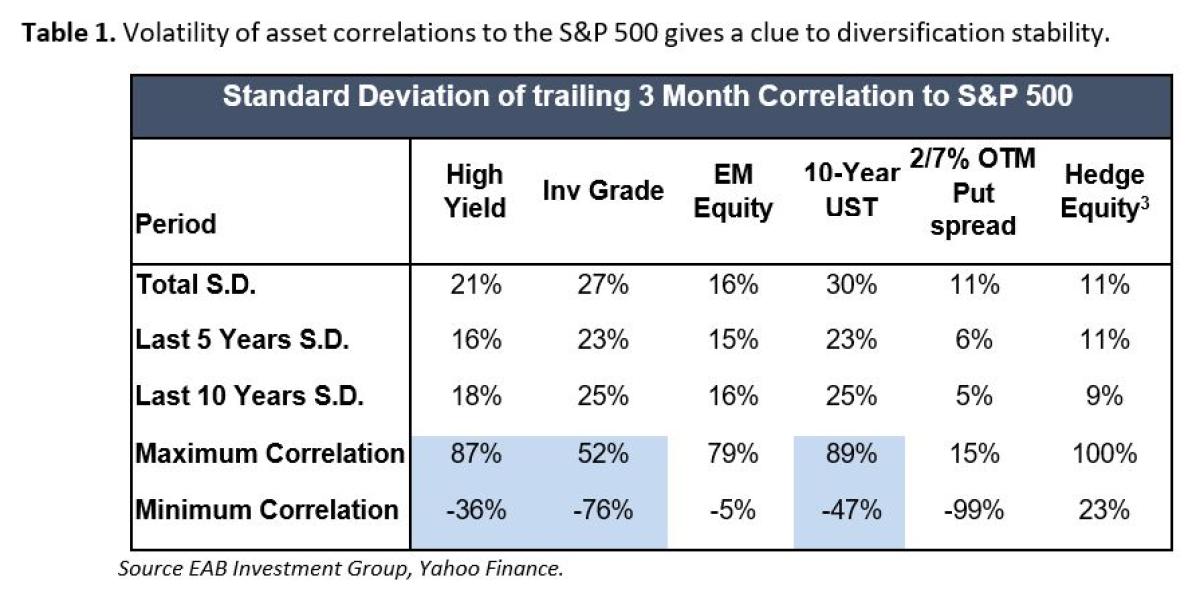

Another way to look at correlations is to calculate the actual range of the correlations versus their mean as an indicator of diversification stability. From Table 1, one can see that fixed income correlations have a relatively high range of correlation to equity. The US 10-year bond correlation, surprisingly led in volatility of correlation, but the investment and high-yield credit sectors also showed a much wider range of diversification effectiveness than perceived by practitioners. As can be clearly seen in the table, the S&P put strategy and the combined synthetic/ JDIEX strategy show a much tighter range of correlation, with the put strategy becoming less volatile over the past 5-year period.

The benefits of disciplined continuous put buying create a level of negative correlation and diversification stability that is difficult to find in fixed income. For investors and advisors where the sequence of returns is critical and there is concern about the potential for powerful bear equity markets, we would consider careful attention to portfolio stress correlation potential. Clearly, any multi-asset class funds or risk parity-based strategies that assume correlation stability are also at risk of negative surprise as a result of correlation instability. While the concept can be applied to multiple asset classes, our sense is that the fixed income class should be a primary focus because of the extreme Central Bank stimulus provided and the potential that this stimulus may, albeit slowly, be withdrawn in the future.

Fixed income and why coupon diversifies equity returns:

If one looks at the data prior to the recent Central Bank Quantitative Easing (QE) period, there was a distinct benefit to holding a mix of stocks and bonds. Much of that benefit derived from the fact that medium-term US government bonds provided an income flow that moderated the impact of equity downdrafts in all but the most severe equity bear markets. In the 1980-2000 period with the 10-year US government bond rates averaging approximately 6%, the coupon yield of the bonds alone in a 40% bond allocation portfolio could offset 2.4% of any equity market loss (40% x 6% annual coupon). But since the “tech wreck” (2001) short interest rates have been dropped to near zero by the Fed and long rates have been cut in half by the significant demand for government bonds that QE has fostered. In today’s marketplace, the same allocation would only provide an approximate 0.4% offset (assume a 1% annual coupon x 40%). In addition, in today’s post-QE lower interest rate world, the outcome would need to take into account another factor connected to the relationship of interest rates to bond value called duration.

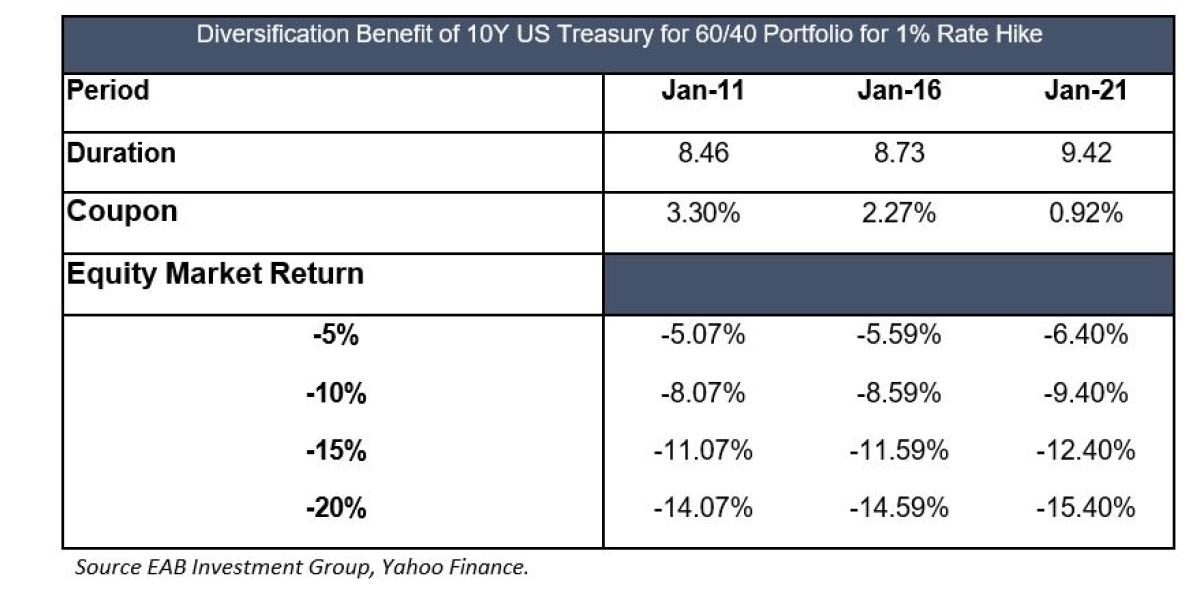

As rates go lower, the average maturity and duration of a bond get longer as a greater proportion of its cash flows come at principal maturity. While the reduction in coupon is an obvious negative for diversification, another often overlooked risk is the impact of lower rates on bond volatility because of the impact on average life or duration of the bond or portfolio. The duration measures the sensitivity of the bond or portfolio to changes in interest rates. We will focus on interest rate hikes for this analysis because rates seem to have limited downside. What follows in Table 2 are hypothetical examples of what returns may look like at various levels of interest rate hikes to bonds and 60/40 portfolios.

Table 2. The duration impact of low rates makes even government bonds more volatile.

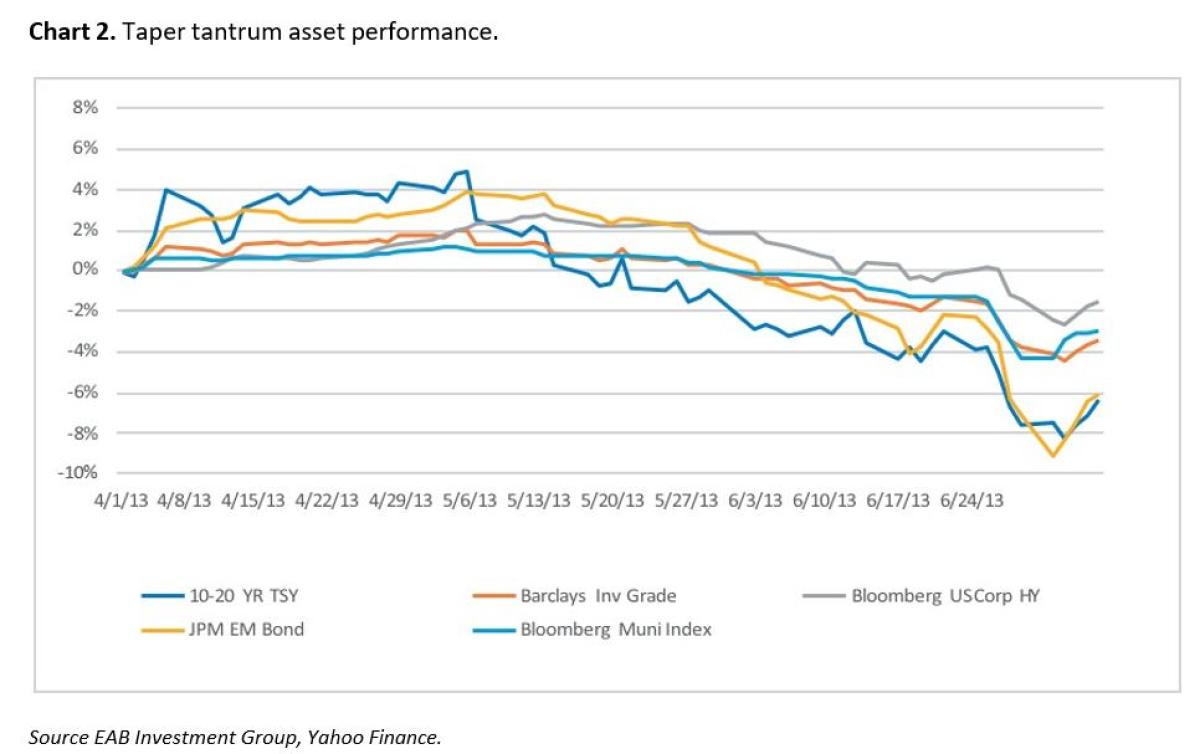

The Bloomberg chart above shows the performance of well-known bond indices. The extreme negative performance of fixed income occurred during these two months in 2013 on the threat of tapering as the Fed had not set in stone any commitment. The -6.38% loss for that period in corporate bonds (Barclays Investment Grade) and -9.81% for the 10-20-year Treasury led to negative annual returns for these fixed income categories for the year. While this is an anecdotal example, we think a true tapering process could potentially hurt holders of long bonds and credit strategies to a greater degree over a longer period of time. If an eventual equity downdraft were to occur, as they have historically later into a Fed hiking regime, credit-oriented portfolios could suffer twice as both fixed income and equities suffer. This relationship is clearly seen in the correlation data around the May 2013 correction. We think this example, while only one single observation, is intuitive and instructive for current investors concerned about diversification and drawdown limitation.

Portfolio Defense, a timely allocation for equity and fixed income credit risk:

For the purposes of this analysis, we will use a systematic out-of-the-money 2-month expiry put spread strategy as a defensive equity approach. When one analyzes the correlation of the 2-month S&P 500 2%- 7% out of the money (OTM) put spread performance correlation against the S&P, its steady negative correlation and its reduction of correlation to the S&P during stressed periods becomes obvious. Of course, this makes sense to the average investor as the puts are buying the rights to sell the S&P 500 itself at a designated price that could be higher than the market price at that time, generating a profit.

Should the S&P not drop below that price, however, the cost of the puts would be lost. The combined equity index and put simulation shown above demonstrates that this type of put rebalancing and option strike price range offers an efficient manner in which to defend equity exposure. The JDIEX track record shows consistent performance within that expectation. The strategy still participates to some extent in equity returns should the markets be positively skewed. In major bear market moves, the hedged equity strategy has generally performed better than the lower-rated credit funds which become unstable in their correlations to equity as shown in the chart above. When combined with an equity index the puts provide a less correlated alternative to equities under stress than low-quality credit approaches do, thus more predictability. While this hedged equity approach would pay a low dividend annually, part of which helps fund the cost of the put strategy, its appeal is its consistent negative correlation of returns under extreme stressed equity markets. As one examines the return stream of the puts approach, the stability of its correlation is evident as is its value under stress. By combining the underlying index with the put approach, which can often be a cost (similar to insurance) a new return stream is generated that has some of the characteristics of equity and some of the defensive characteristics an investor wants in stress markets. This alternative, in our view, warrants an allocation of investor portfolios to hedge both lower-quality credit risk and equity risk.

While we have presented some of the weaknesses of Modern Portfolio Theory optimizations with regard to correlation estimates, if one were to look at the post-QE environment to construct an efficient portfolio, the Hedged Equity approaches would still garner allocations. Using traditional techniques, our models consider a range of 18%-20% to be a reasonable allocation for moderate to aggressive investors but higher for conservative investors who need to generate total returns higher than current market coupons allow. It’s important to note that the last several years have been relatively favorable for diversification as interest rates have been dropped to near-zero levels. We believe at current low coupons it is only prudent to forecast much less effective fixed income diversification and forecast resulting higher fixed income volatility. Given these current conditions it would seem investor use of hedged equity would improve overall diversification significantly.

As a result, we feel confident in our baseline consideration for investors who are particularly concerned about volatility spikes, or extreme equity market events, potentially higher allocations to hedged equity may be justified. For the aggressive investor, we would recommend the allocation would mostly come from the equity allocation and for the conservative investor, a greater proportion would come from the credit portion of the portfolio. One special case to evaluate is income-only investors that use no equity at the moment. For these investors where the correlation to equities may be hidden in increased credit exposure, the lower correlation hedge equity could be an appropriate way to improve diversification.

About the Study:

While the study is based on data and its analysis, the approach taken and communicated is not meant to be a quantitative treatise. Certainly, the math upon which the study rests can be presented but is not necessary for the conclusions drawn. The daily data in this study goes back to January of 2003, which we believe is a significant enough time period for the conclusions drawn. For the purposes of evaluating the hedged equity approach we combined the synthetic strategy with the JDIEX strategy from its inception 8/31/2015. The team also evaluated various trailing correlation periods, in particular trailing 3-month and trailing 6-month correlations. We found negligible difference between the behavior of 3- and 6-month correlations (data available upon request) which display similar paths and ranges of correlation.

We chose the 90-day period because this more closely represents the frequency of market participant rebalancing and the tendency of the market to process downdrafts within a fairly compressed period of time. We also find trailing 3-month rolling correlations smooth out very short-term changes but are reflective of the real experience investors face throughout the life of their portfolios. The data was sourced from publicly available and reliable sites on Bloomberg, Yahoo Finance, and EAB Investment Group. There can be no guarantee, as with all simulations, and studies that these results will exactly mirror those experienced in these strategies going forward. The simulations are based on indices (with the exception of JDIEX the fund EAB manages as subadvisor) and, as such do not include fees and expenses investors might experience in actual funds. The analysis on the various hypothetical fixed-income performance scenarios is based on financially accepted modeling techniques and is for illustration only and not meant to represent actual returns or a forecast of actual fixed-income returns.

Definitions:

Alpha: The excess return of the fund relative to the return of the benchmark index is a fund’s alpha.

Beta: A measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole. Beta is used in the capital asset pricing model (CAPM), a model that calculates the expected return of an asset based on its beta and expected market returns.

Covariance: Covariance is a measure of the directional relationship between the returns on two risky assets

Modern Portfolio Theory (MPT): A theory on how risk-averse investors can construct portfolios to optimize or maximize expected return based on a given level of market risk, emphasizing that risk is an inherent part of higher reward.

Put: An option contract giving the owner the right, but not the obligation, to sell a specified amount of an underlying asset at a set price within a specified time. The buyer of a put option estimates that the underlying asset will drop below the exercise price before the expiration date.

Quantitative Easing (QE): An unconventional monetary policy in which a central bank purchases government securities or other securities from the market in order to lower interest rates and increase money supply.

S&P 500 Index: An index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe.

Standard Deviation: Measures historic volatility and is the measure of the dispersion of a set of data from its mean. The more volatile the data, the higher the deviation.

Synthetic Options: A combination of stocks and/or options that return the same payoff characteristics of another options strategy. If the market begins to move against a cash or futures position it is losing money in real time. With the protective option in place, the hope is that the option will move up in value at the same speed to cover the losses. This is best accomplished with an at-the-money option but they are more expensive than an out-of-the-money option. In turn, this can have an adverse effect on the amount of capital committed to a trade. Even with an at-the-money option protecting against losses, the trader must have a money management strategy to determine when to get out of the cash or futures position. Without a plan to limit losses, he or she can miss an opportunity to switch a losing synthetic position to a profitable one. Also, if the market has little to no activity, the at-the-money option can begin to lose value due to time decay.

Footnotes:

1. Hedge Equity is the synthetic back test of the current JDIEX strategy

2. JDIEX based on live mutual fund performance.

3. Hedge Equity data set included both the synthetic strategy and live JDIEX performance

About the Authors:

Arnim Holzer is the Global Macro Strategist and Client Portfolio Manager at Easterly EAB Risk Solutions.

He has over 40 years of global macro and multi-asset experience. Arnim has served as Chief Investment Officer, Strategist, Portfolio Manager, and Client Service and Marketing executive at several firms over the past 30 years. His investment philosophy is a unique blend of fundamental, technical and, quantitative disciplines honed over the years of working with many of the top firms and investors in each of these disciplines. His particular macro skill is understanding the relationships of correlation and volatility in the optimization of portfolio construction and return generation. Prior to EAB, Arnim founded a tail risk consulting firm, ASH Strategy, LLC, where he developed a novel multi-asset hedging approach for institutional, high-net-worth, and family office investors. For 6 years he managed or served as senior strategist on multi-asset funds or strategies at Deutsche Asset management and Scudder. While at Deutsche he was the portfolio manager on approximately $3 billion of assets in domestic and offshore multi-asset funds. He also founded and managed a multi-asset offshore hedge fund at Israel Discount Bank of New York. Arnim received his undergraduate Economics degree from Princeton University and his MBA-finance from Fordham University. He holds a Series 7 and 65 Registered Representative securities registration.

Bill Visconto is the Chief Operating Officer and Portfolio Manager at Easterly EAB Risk Solutions. Prior to EAB, Bill was a head volatility trader at McGowan Investors LLC.

His responsibilities were to implement the firm’s strategy in the volatility arbitrage space and deploy the firm’s capital to maximize returns. Before joining McGowan, he was Co- Founder of Volare Capital, a hedge fund that pursued statistical/volatility arbitrage strategies in index and single stock options. Bill was the Head of Portfolio Management and Trading Floor Operations for PFTC Advisors and PFTC Trading. At PFTC, he was responsible for managing a team of 4 portfolio managers and 17 floor traders. PFTC Trading was one of the largest liquidity providers in the United States. Bill received his B.S. in Marketing from the University of Scranton. He holds his FINRA Series 7, 63, 65 licenses and is a CFA Level 3 Candidate.

About EAB Investment Group:

EAB Investment Group, LLC specializes in risk mitigation strategies and works with hedge funds, family offices, high-net-worth individuals, investment companies and other advisors. EAB Investment Group uses equity and index option strategies based on a proprietary process with the goal to reduce portfolio risk and increase the probability of success. A deep understanding of options pricing enables EAB Investment Group to manage carry and attempt to mitigate costs over time, and potentially optimize monetization.

Important Risk Information:

All information herein is from sources generally available to the public and believed to be reliable but have not been independently verified. No representation or warranty can be given with respect to the accuracy or completeness of the information, and is subject to updating, revision, and amendment. EAB disclaims any and all liability relating to this information, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, this information. Subscribers to any service provided by EAB Investment Group should consult their own financial advisors, legal counsel, and accountants as to financial, tax, legal, and related matters concerning their subscription to EAB Investment Group’s service. No part of this presentation constitutes financial, tax, or legal advice. EAB Investment Group reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. The securities or sectors discussed herein are for informational purposes only and do not represent client portfolios managed by EAB Investment Group; it should not be assumed that any of the securities or sectors discussed herein were or will be included in such portfolios.

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. The information in this document is provided solely for general education and information purposes and do not represent a particular portfolio managed by EAB Investment Group. No statement contained herein should be construed as a recommendation to buy or sell a security or futures contract or to provide investment advice. Supporting documentation for any claims, comparisons, statistics or other technical data in this document is available from EAB Investment Group, LLC upon request. EAB is a registered investment adviser. Registration does not imply a certain level of skills or training. More information about the firm, including its investment strategies and objectives, can be found in EAB’s Investment Group’s ADV Part 2, which is available, without charge, upon request.

This information has been prepared solely for informational purposes only. This information is for the use of the intended recipients only; it may not be reproduced or disseminated, in whole or in part, without the written consent of EAB Investment Group LLC (“EAB Investment Group”).

James Alpha Advisors, LLC serves as the Advisor to the James Alpha family of mutual funds and related portfolios. James Alpha is a related entity to James Alpha Management, a family office and diversified asset management firm specializing in identifying, seeding, and growing alternative investment strategies for institutional and individual investors. EAB Investment Group, LLC is an SEC-registered investment advisor specializing in risk mitigation strategies. EAB Investment Group, LLC serves as the subadvisor for JDIEX. Both firms’ form ADVs can be found at www.adviserinfo.sec.gov.

Derivatives may be volatile, and some derivatives have the potential for loss that is greater than the Portfolio’s initial investment. If the Portfolio sells a put option, there is risk that the Portfolio may be required to buy the underlying investment at a disadvantageous price. If the Portfolio sells a call option, there is risk that the Portfolio may be required to sell the underlying investment at a disadvantageous price. If the Portfolio purchases a put option or call option, there is risk that the price of the underlying investment will move in a direction that causes the option to expire worthless. The Portfolio’s ability to achieve its investment objective may be affected by the risks attendant to any investment in equity securities.

Shares of ETFs have many of the same risks as direct investments in common stocks or bonds. In addition, their market value is expected to rise and fall as the value of the underlying index or bond rises and falls. It is possible that the hedging strategy could result in losses and/or expenses that are greater than if the Portfolio did not include the hedging strategy. The use of leverage by the Fund or an Underlying Fund, such as borrowing money to purchase securities or the use of derivative, will indirectly cause the Fund to incur additional expenses and magnify the Fund’s gains or losses. Because a large percentage of the Portfolio’s assets may be invested in a limited number of issuers, a change in the value of one or a few issuers’ securities will affect the value of the Portfolio more than would occur in a diversified fund.

The Portfolio will borrow money for investment purposes. Leveraging investments, by purchasing securities with borrowed money, is a speculative technique that increases investment risk while increasing investment opportunity. The dollar value of the Portfolio’s foreign investments will be affected by changes in the exchange rates between the dollar and the currencies in which those investments are traded.

Past performance is not a guarantee nor a reliable indicator of future results. As with any investment, there are risks. There is no assurance that any portfolio will achieve its investment objective. Mutual funds involve risk, including possible loss of principal. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund. This and other information is contained in the Fund’s prospectus, which can be obtained by calling 888.814.8180 and should be read carefully before investing. The Saratoga Advantage Trust’s Funds, including all of the James Alpha funds, are distributed by Northern Lights Distributors, LLC, member FINRA/SIPC. 11/11© Saratoga Capital Management, LLC; All Rights Reserved. Saratoga Capital Management LLC, EAB Investment Group LLC, and James Alpha Advisors, LLC are not affiliated with Northern Lights Distributors LLC. For additional Fund literature visit www.JamesAlphaAdvisors.com or www.SaratogaCap.com.

THE OPINIONS STATED HEREIN ARE THAT OF THE AUTHOR AND ARE NOT REPRESENTATIVE OF THE COMPANY. NOTHING WRITTEN IN THIS COMMENTARY OR WHITE PAPER SHOULD BE CONSTRUED AS FACT, PREDICTION OF FUTURE PERFORMANCE OR RESULTS, OR A SOLICITATION TO INVEST IN ANY SECURITY.