By Brian A. Schroeder, the founder of OCIO Monitor, a specialty consulting firm that provides due diligence of investment consultants and outsourced chief investment officers.

The CFA Institute recently released its first draft of GIPS for OCIOs. I applaud the effort and feel it is a great first step. And like the original GIPS, once finalized, it will no doubt be revised over time.

This new GIPS for OCIOs will create a valuable tool for asset owners to evaluate and compare OCIOs for purposes of monitoring, hiring, firing, etc. For reasons that have been well documented and previously discussed, there can never be a true apples-to-apples comparison because of differing mandates, guideline restrictions and unique financial circumstances for every client.

Nevertheless, OCIOs will seek the Good Housekeeping Seal of Approval by becoming compliant with the forthcoming GIPS. An unintended consequence is the incentive to put a thumb on the scale. And having discovered many ways investment consultants and OCIOs can dress up performance, I believe creative manipulation is inevitable. Goodhart's Law will see to that.

Goodhart's Law can be summarized as, "When a measure becomes a target, it ceases to be a good measure." People want to appear better by beating the competition. The incentive to game the system and even commit fraud to create the illusion of outperforming is powerful. It happens more often than you think.

Here are two real possibilities I predict OCIOs will attempt.

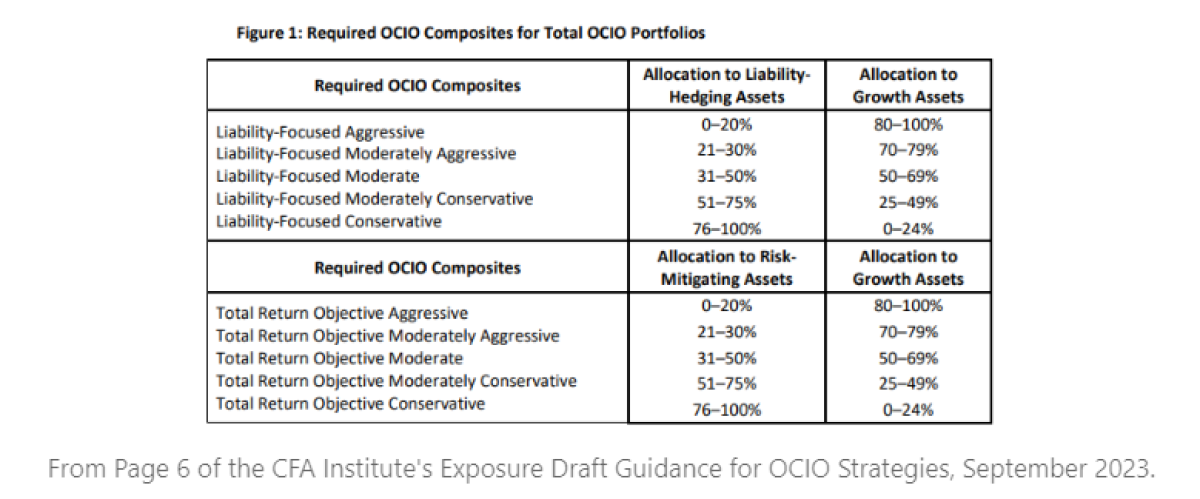

First, the draft proposal creates Required OCIO Composites that every Total OCIO Portfolio must be categorized into.

According to the draft, "Total OCIO Portfolios must be assigned to a Required OCIO Composite based on the portfolio’s target asset allocation, not the actual asset allocation weights." (Emphasis added.)

Ignoring for a moment the definitions of Growth Assets and Risk-Mitigating Assets, whose definitions are addressed in the draft proposal, one can easily speculate how Goodhart's Law will likely come into play.

OCIOs will likely create "Goodhart guidelines" with target allocations approaching a composite's upper bounds. For example, a client may have a combined target allocation to Growth Assets of 49%. But it is then managed staying within the allowable ranges producing a long-term average of 60%.

This is similar to OCIOs and investment consultants under-measuring beta for comparisons. They create custom benchmarks that are designed to be "slow" thus creating the appearance of outperformance, or Phantom Alpha.

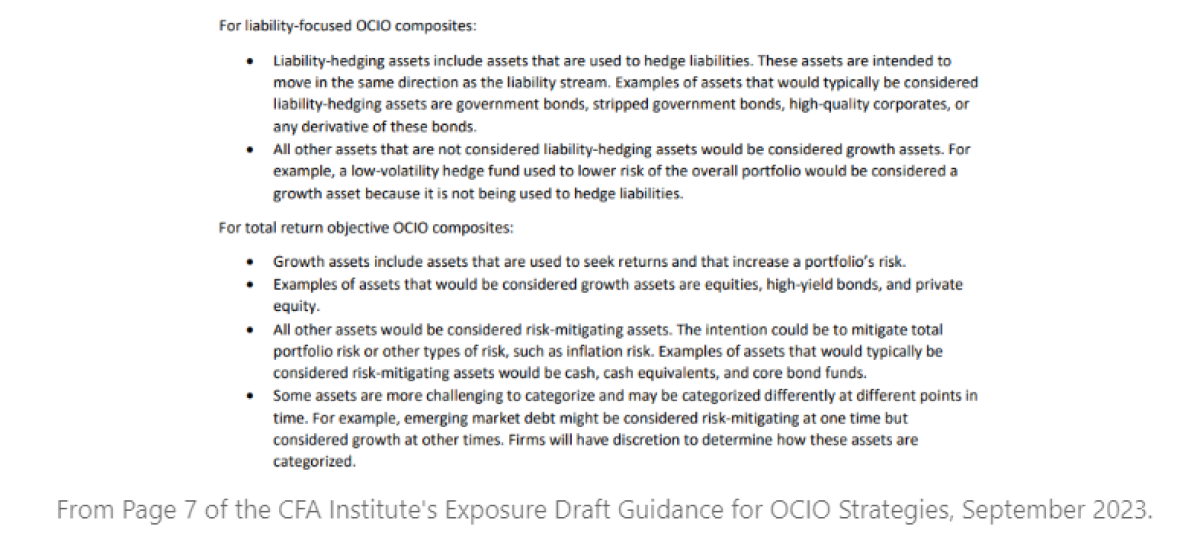

Second, let us now turn back our attention to the definitions of Growth Assets and Risk-Mitigating Assets per the proposed guidelines. These are shown below.

Defining and categorizing asset classes is a difficult task. Many asset classes are not specifically covered in the bullet points, but are described generally, and subject to interpretation leaving "discretion to determine how these assets are categorized."

For example, following the language above, an OCIO may classify a value-add real estate fund that is highly leveraged as a risk-mitigating asset. Could a short duration, quality constrained, high yield strategy be argued to be a risk-mitigating asset and not a growth asset? How might a convertible bond strategy be categorized? One can easily see how this aspect can be abused.

The draft proposal does include a Sample OCIO Strategy GIPS Composite Report on pages 18-21. If OCIO firms indeed follow this example point by point, then there will be greater disclosure that should illuminate if there is any gaming and perhaps dissuade OCIOs from putting as heavy a thumb on the scale. Regardless, asset owners, search consultants and competitors will still have to get into the weeds to discern such differences.

Will There Be Independent Verification?

In the Sample OCIO Strategy GIPS Composite Report it states, "Jaxx Investments has been independently verified for the periods 1 January 2010 to 31 December 2022. The verification report is available upon request."

The draft proposal does not appear to require independent verification. So, this appears to be an extra expense that would voluntarily be undertaken by each OCIO. But if an OCIO does not, will the CFA Institute perform a review? Perhaps they will perform random audits? Might the CFA Institute certify firms to be independent verifiers of its GIPS compliance?

Could Poor Performing OCIOs Appear Superior?

Yes, that is a possibility. OCIOs that use both Goodhart strategies detailed above to game the system will have a real advantage. It may even be that poor performing OCIOs rank higher than OCIOs that create more value-add, but lag by comparison due to a more ethical GIPS compliance methodology.

Webcast on monitoring OCIO performace with The Retirement Space.

About the Author:

Brian A. Schroeder is the founder of OCIO Monitor, a specialty consulting firm that provides due diligence of investment consultants and outsourced chief investment officers. He has over 30 years of investment experience, as both an institutional manager and consultant.