By Chung-Hong Fu, Ph.D., Managing Director Economic Research and Analysis, Timberland Investment Resources, LLC.

Introduction

Over the course of 2022 and 2023, the investment community saw one major announcement after another of institutional investment funds or organizations committing tens or hundreds of millions of dollars to the natural capital features of timberland assets. In many cases, these investments were made in the carbon sequestration potential of forests and their capacity to help the world address the challenge of global climate change. However, increasing amounts of this capital also were invested in some of the other environmental and social attributes of working forests – specifically their capacity to enhance biodiversity, protect watersheds, provide clean air, and stimulate rural economic development and job creation.

Regardless of how one defines natural capital, the underlying premise is an acknowledgment that investors have a role to play in making the world a better place for future generations. In this paper, we will show how the new wave of capital targeting nature-based solutions is reshaping the timberland asset space – causing its underlying value proposition to evolve and expand. The goal of the paper is to help investors better understand how these values can help advance their financial and non-financial (i.e., ESG1 ) objectives.

Climate Change: A Springboard to Investor Action

A growing segment of the investment community is becoming increasingly proactive in striving to address issues that affect society, the economy, and the environment. This is the foundation of the environmental, social, and governance (ESG) movement, which has been building momentum since a United Nations report first advanced the concept in 2005.2 An outgrowth of this is impact investing -- the conscientious use of capital to affect positive social and environmental change in addition to generating financial returns.

Many factors came together over time to put ESG and impact investing on investors’ agendas, but one of the key drivers has been the growing recognition that the world faces a climate crisis. In 2021 alone, both the Sixth Assessment Report from the Intergovernmental Panel on Climate Change (IPCC) and the United Nations’ 26th Climate Change Conference, which was held in Glasgow, Scotland, helped focus world attention on the threats posed by a changing climate. As a result, more than 140 countries pledged to reach zero net carbon emissions by 2050.

With public consciousness having been raised, both private companies and the investment community recognize that governmental action alone cannot successfully address the challenge. Some took on the mantle that the private sector can play a vital role in affecting environmental change and in building a more sustainable future. For example, the California State Teachers’ Retirement System set a goal in 2021 to put $1 billion-to-$2 billion to work in climate-friendly investments. In a similar vein, three of New York City’s pension funds announced their intent to place $8 billion in climate-change solutions by 2025.

In response to the growing interest in ESG and impact, a plethora of new products were introduced by global investment managers. According to Morningstar, mutual funds subscribing to ESG principles reached a record $51 billion in new commitments in 2020, more than double the amount added the previous year. By the end of the third quarter of 2021, total global assets managed by sustainable funds reached $3.9 trillion.

A logical outgrowth of impact funds is the promotion of nature as an investment opportunity. HSBC Pollination Climate Asset Management, for example, is a joint venture formed in 2020 to develop funds charged with the protection or advancement of the environment. The firm has joined the Natural Capital Investment Alliance – spearheaded by Charles, Prince of Wales – to place $10 billion in natural capital solutions by 2022.

Natural Capital Translated into Forest Investments

While many nature-based solutions are available, timberland is a leading option for institutional investors. Here are some examples of forest-related investment opportunities that developed within the past year.

- Apple announced in April 2021 that it had established the Restore Fund, which will invest $200 million in working forests that both capture carbon and generate a financial return. With the goal of removing one million metric tons of carbon dioxide from the atmosphere each year, the Restore Fund supports Apple’s goal of having a zero-carbon footprint across its operations, including it supply chain, its manufacturing activities, and its products.

- In October 2021, Oak Hill Advisors, a manager of $50 billion in assets, partnered with Bluesource, a climate solutions provider, to create a $500 million fund called the Bluesource Sustainable Forest Company, which will purchase or co-invest in timberland to develop carbon offset credits.

- The natural resource investment arm of Manulife, a large Canadian insurer, purchased close to 90,000 acres (36,000 hectares) of timberland in Maine in August 2021 with the objective of creating carbon offsets (credits). These offsets will be used to mitigate Manulife’s own emissions and any overages will be monetized in the voluntary carbon markets.

Why timberland? One estimate suggests the world’s forests can capture as much as 16 billion metric tonnes of carbon dioxide a year.3 As a result, investors are beginning to recognize that timberland can be a key, natural climate solution – one that also offers the potential to generate attractive levels of income and overall financial return. However, forests are attractive to impact investors for reasons other than their capacity to store carbon. TIR believes there are four reasons impact investors and natural capital funds are drawn to the asset class.

First, private timberland is perceived as plentiful and accessible to investors – with large tracts of land being available in developed markets like North America and Western Europe, as well as in emerging markets such as Latin America, Southeast Asia and Eastern Europe. In fact, an estimated 120-to-150 million acres (48-61 million hectares) of forests worldwide are suited for institutional investment.4

Second, the public has a strong and positive perception of forests – viewing them and their protection as being important for society. Their natural functions also support local communities with jobs and economic development.

Third, forests provide a wealth of nature-based products and services that can be monetized – not just carbon offsets, but also their capacity to provide clean air, protect watersheds, enhance and preserve biodiversity, generate clean energy, and provide opportunities for public and private recreation.

Fourth and finally, forests can generate ongoing cash flow through the sustainable growth and harvesting of timber.

Defining Natural Capital in the Timberland Asset Space

Timberland’s status within the impact investment sector represents a natural evolution of the asset class and its fundamental value proposition. It reflects the continual innovation of investors and managers to unlock value from a remarkably complex asset. When timberland emerged as a viable asset class in the 1980s, forests were simply valued for the timber that could be grown and extracted from them. Today, forests also provide a growing array of natural capital solutions that promise to have a positive impact on society and the environment – while also providing financial returns to those who own and invest in them.

This brings us to the definition of natural capital. At TIR, we define the term as follows:

NATURAL CAPITAL consists of the earth’s resources and ecosystems, and specifically their capacity to sustain and provide society with benefits. Virtually all forms of timberland that are held as long-term, investable assets qualify as natural capital, including both planted and natural forests.

NATURAL CAPITAL SOLUTIONS are the investment and management strategies employed to ensure that the natural capital attributes of a forest, or some other investable asset, deliver sustainable benefits to society and the environment. An equivalent term is Nature-Based Solutions. When specifically applied to addressing the threat of global climate change, the term is often adapted and expressed as Natural Climate Solutions.

The concept of natural capital did not emerge overnight. In fact, it has a lengthy history. The early groundwork was laid within the timberland asset class during the late 1990s and early 2000s when timberland investment management organizations (TIMOs) and their institutional and high-net-worth clients began exploring opportunities to monetize the ecosystem features of forest investments. This encompassed the broad category of non-timber values that forests possess or can be managed to create. For instance, selling a land base’s development rights through the use of conservation easements; developing wetland mitigation banks; and, utilizing portions of forested landscapes to develop solar energy and wind farms, are examples of monetizable, forest-based ecosystem services. The development of carbon offset credits is another, as is leasing forestland for recreational activities, like hunting, fishing, hiking, camping, and snowmobiling.

Soon after ecosystem services entered the lexicon of timberland investors, the term socially responsible investing, or SRI, also spread broadly across the institutional investment space. Institutional investors who were committed to SRI, for example, have supported local communities in emerging countries through investment in forest plantations and associated processing infrastructure. While SRI, in practical terms, is a call to “do good,” the term soon came to be viewed as too limited in scope because it did not fully encompass the environmental and governance values that also were of growing interest and concern to investors. This gave birth to the development of environmental, social and governance (ESG) investment criteria and risk-management protocols. Thus, the concept of SRI might be considered a precursor to the development of ESG-focused and impact investing.

Measuring the Natural Capital Features of Forests in Impact Investing

Timberland investment managers (TIMOs) and the new natural capital funds that are now active and available to institutional investors are building upon a foundation of opportunities that was established through the practice of managing investable forest assets sustainably and monetizing their varied ecosystem services. What has changed recently is that (1) investors are providing their investment managers with explicit ESG metrics against which their actions and performance will be measured; (2) investors are communicating specific impact goals that they expect their managers to help them attain; and (3) there is a growing body of ESG data across managers that allow for better comparison and benchmarking.

The degree to which a TIMO is managing its clients’ assets in accordance with ESG standards and principles now can be assessed by independent third parties. For instance, the Sustainable Forest Initiative (SFI) and the Forest Stewardship Council (FSC), two, independent, non-profit, non-governmental organizations (NGOs) exist to promulgate forest sustainability standards and to assess the degree to which large forest landowners and managers are operating in conformance with them – granting certified status to those who comply. Organizations that cover general environmental disclosure and scoring – such as CDP5 – also are becoming more active and influential. Because of the transparency these independent organizations can provide, timberland investors now can be more confident that the forest assets they own are being managed in accordance with strong ESG and impact principles.

Broadening the Investment Spectrum Within Timberland

The development of such standards and the increasing use of verifiable metrics, in turn, has enabled timberland investment managers to explore and develop new solutions and products for meeting institutional investor demand for ESG and natural capital investment opportunities. The breadth and variety of these products (and the investment managers who offer them) have expanded rapidly in recent years. Several timberland managers have pivoted toward natural capital solutions with funds focused on forest-based carbon sequestration and other types of ecosystem markets. New entrants have emerged as well. JPMorgan Chase & Co., a major U.S. bank, purchased an established TIMO, Campbell Global, in 2021 to create a platform that would allow it to participate in the offering of natural capital solutions, including forest carbon investment opportunities. Non-profits also have entered the space. For instance, The Nature Conservancy, a global conservation group that focuses on preserving biodiversity, has created an impact investing unit called NatureVest that pools private capital into funds for impact investing. As mentioned earlier in reference to the actions of Apple, many other corporate entities also are taking meaningful action – pledging millions of dollars to acquire forests both to make a positive impact on the world and to offset their own carbon emissions footprints.

Three Main Forms of Timberland Investing in ESG

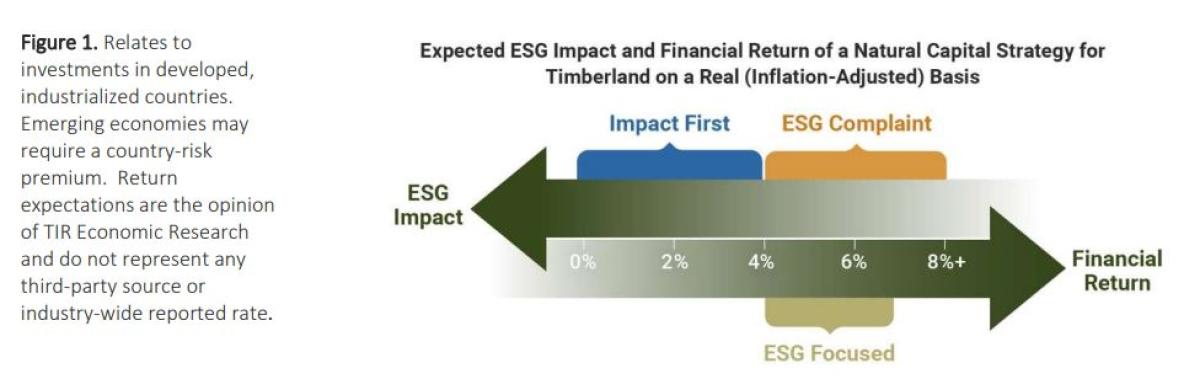

The number of options (products and investment managers) can make it difficult for institutional investors to select an impact or ESG-focused investment option that best aligns with their objectives. However, to generalize, natural capital strategies fall into one of three categories: (1) ESG compliant; (2) ESG focused; (3) impact first. What follows are summaries of each.

ESG Compliant

A timberland portfolio that has an ESG-compliant strategy maintains a primary objective of maximizing return while mitigating risk to acceptable levels. Timberland investment managers who serve institutional clients practice sustainable forestry, and most have adopted core ESG principles. TIMOs recognize that operating in this way is increasingly a prerequisite for accepting capital from the growing body of environmentally-conscious investors. Investors interested in timberland therefore can generally be confident that most funds or accounts served by timberland managers are ESG compliant. Of course, some timberland investment products or funds are more heavily focused on ESG outcomes than others. As a result, investors still must perform due diligence to ensure that a given manager’s ESG qualifications are consistent with their objectives.

ESG Focused

In contrast to an ESG-compliant strategy, an ESG-focused portfolio has a dual objective of generating strong ESG outcomes as well as a competitive financial return. The achievement of ESG objectives has equal footing with the generation of investment performance. Often that means developing or capitalizing on a forest’s capacity to offer one or several types of ecosystem services – which are then monetized to provide both tangible societal benefits and financial returns. One example is selling a conservation easement that restricts future development on a forested tract – and doing so at a market price and with an allowance to continue growing and harvesting certain types of timber. Another ESG-focused strategy entails harvesting a forest less intensively to prime its capacity to absorb and store more carbon, which, in turn, can help facilitate the generation and future sale of carbon credits.

Impact First

The most aggressive type of natural capital investment strategy is called impact first. Sometimes also described as high-conviction impact investing6, this kind of strategy is typically adopted by investors who want to create a measurable legacy of positive impact on society and the environment – and are willing to accept a lower return, or even forego a return altogether – to do so.

An organization that wants to be net-zero in carbon emissions is a prime candidate for an impact-first forest investment. Such investors can purchase forestland to capture carbon and use it to offset and mitigate their own carbon footprints. Since these carbon credits are “retired” and never sold in the market, no income is generated. Once the carbon is registered, harvest rates are reduced, which can cut into the income generated from timber sales. The overall financial performance also might be lower than with a traditional timberland investment.

That is just one example. Impact first natural capital investment can take many other forms, too. Some other impact-first strategies include reducing carbon emissions by protecting forests in emerging countries that are vulnerable to forest loss (known as REDD+)7 ; training and hiring native peoples to work in forestry or wood products manufacturing jobs or capitalizing the development of such infrastructure in poor or disadvantaged communities; and protecting forests that have high scenic or biodiversity values and making them accessible to the public for recreational uses.

Return and Impact Tradeoff Across Strategies

Across the three main natural capital strategies, each serves a different type of investor. A timberland investor who wants to be a responsible global citizen and is also focused on financial performance, can choose an ESG-compliant strategy that targets a real (inflation-adjusted) return, which will typically fall in the range of 4 percent-to-8 percent (see Figure 1). Investors who want to achieve competitive returns through a strong ESG mandate can expect real, life-of-investment returns that are similar to those that might be generated by an ESG-compliant strategy, but with a lower ceiling. Finally, those who embrace impact-first strategies might expect real performance of 4 percent or less, which typically falls below the return profiles of traditional (ESG-compliant) timberland investments.

Essentially, natural capital investing in timberland encompasses a broad variety of choices for generating returns and having impact (see Figure 2). This “optionality” can be used to capture higher returns or allow for diversification that reduces risk exposure.

Conclusion: Building the Right Natural Capital Portfolio with Timberland

Investing in forest-based natural capital solutions is a broad, fluid, and evolving concept. It gives investors wide latitude to establish and interpret how they wish to participate in the sector. For an ESG-or-impact-minded investor, it is important to first ask how financial performance ranks relative to non-financial goals because there could be tradeoffs that need to be considered. The next step is to ask what type of impact is important. Is addressing climate change through carbon sequestration a priority, or is a primary goal adding rural jobs and serving disadvantaged communities? Determining which outcomes will be most important can help an investor winnow and select from the available strategies.

TIR also recommends thinking holistically. Natural capital investors (and their chosen managers) need to understand the net impact of their portfolio strategies because they could produce secondary effects. Just because one can sequester carbon in trees, for example, that does not mean that it is the best ESG-focused objective for a particular forest. In certain cases, a more impactful approach may entail managing that forest to provide clean water, to promote local employment, or to grow generations of trees that then can be converted into durable products, like lumber and furniture, which lock up sequestered carbon for generations. This is how a qualified timberland investment manager can help by understanding and educating clients about the ESG and impact-related tradeoffs that may need to be made when building and managing a forest portfolio.

Adjusting Expectations of Return

As previously mentioned, the strong interest in natural capital solutions has stimulated a significant influx of investor capital. The spillover effect is the potential for capitalization rate and discount rate compression for forest assets that are rich with natural capital features.

Investors in forest-based natural capital solutions should therefore communicate clearly with their TIMO managers about the allowances they wish to make regarding generating lower financial returns in exchange for producing more significant impact and ESG-related outcomes.

Trust But Verify

This speaks to the importance of manager selection and oversight. Investors should assess whether a timberland investment manager’s track record, skills, and experience align with the natural capital investment strategies and products they are offering. Greenwashing or greenwishing are risks to an authentic ESG or impact strategy. Greenwashing is the practice of exaggerating or misrepresenting the ESG character or impact potential of an investment strategy. Greenwishing is the expectation that an investment will produce more social and environmental benefits 11 than are possible with a particular investment strategy. For these reasons, it is important for investors to perform focused and comprehensive due diligence on prospective investment managers and their product(s), and to ask for regular updates concerning their compliance or adherence to accepted ESG standards and principles. This includes the metrics used and the best practices to be employed by management. For impact-first strategies, investors can and should request independent impact verifications in relation to the performance of their portfolios.

Closing Words

Capital inflows into timberland, like other asset classes, will ebb and flow over market cycles. Right now, we are seeing a wave of new investor money-seeking natural capital solutions. Will it last? Regardless of how the cycle proceeds, the asset class has been transformed in lasting ways due to the growing influence of ESG-focused and impact investing. Natural capital solutions, such as forest carbon capture, are here to stay and have become an important and fundamental dimension of timberland investing. This has expanded the value proposition of timberland and provided institutional investors with a broader and more varied array of options for participating in the asset class. This means that timberland investors who are seeking (a) the best possible risk-adjusted return, (b) an enduring legacy for future generations, or (c) something in between, now have a variety of attractive and interesting options to consider.

Footnotes:

1 ESG is Environmental, Social and Governance, which are three tenets of good investor stewardship.

2 United Nations Environment Programme Finance Initiative (UNEP FI): “A Legal Framework for the Integration of Environmental, Social and Governance Issues into Institutional Investment.” (2005).

3 Laura Messchendorp, “Stumped for Answers: Forestry, Carbon, Capture, and Biodiversity.” Preqin (November 10, 2021).

4 Gresham House: “Investing in Timberland: An International Perspective.” International Forest Business Conference 2020.

5 CDP Global (www.cdp.net) is a global non-profit organization that who helps companies and municipalities disclose and manage their environmental impacts.

6 Preqin: “ESG in Alternatives: Navigating the Climate Crisis.” (2021).

7 REDD+ is Reduced Emissions from Deforestation and Forest Degradation where the plus (+) represents sustainable management of the forest and protection of the carbon stocks. Source: United Nations Framework Convention on Climate Change (https://redd.unfccc.int)

About the Author:

Hong oversees all economic and market analysis and forecasting for TIR and plays a key role in the development and implementation of the firm’s investment strategy. He was a founding member of TIR and was instrumental in establishing the firm’s research-driven investment ethic.

Hong began his career at Temple-Inland Forest Products Corporation where he served as a resource utilization specialist and business analyst. In these roles, he provided economic and research analysis services that were used by senior executives within the company to make strategic decisions across a range of issues, including asset securitization, acquisitions, and resource and business optimization. Prior to joining TIR in 2003, Hong served as senior investment analyst with Global Forest Partners where he performed global timber acquisition analysis, created a variety of decision support models and directed currency risk management analysis. Hong is recognized in the timberland investment arena for his measured and comprehensive analysis of the trends and events that drive investment performance and that influence the long-term risk and return profile of the timberland asset class. He writes extensively on these and related topics and is frequently consulted by market participants and analysts, including the news media, for his unique and well-informed perspectives. Hong is a graduate of Northwestern University where he received a BS in biology. He also earned an MS in environmental management at Duke University and an MBA at Columbia University. He received his Ph.D. in forest economics at North Carolina State University.

Disclaimer This paper is provided for the education of its readers. The opinions and forecasts made are for informative purposes only and are not intended to represent the performance of an investment made through Timberland Investment Resources, LLC. No assurances are made, explicit or implied, that one’s own investments in timberland or with Timberland Investment Resources, LLC specifically, will perform like what has been described in the paper.