By Alex Zweber, CFA, CAIA, Managing Director, Investment Strategy, Parametric.

Protective hedges against equity market volatility were more effective in 2020 than in 2022. We explain the role of the volatility risk premium.

The financial hurricane of Q1 2020 blindsided equity markets. The S&P 500® collapsed -33.9% in just 23 days, realized volatility neared triple digits, and many highly leveraged strategies were wiped out entirely. But tail-risk hedges, which offer insurance-like payouts against sharp equity market declines, produced significant positive cash flows to the lucky few. Fast-forward to 2022: The markets delivered the worst first half of a new year since 1970, when the S&P 500® dropped -20%. Investors who had allocated to these same tail-risk strategies didn’t realize the same benefit as in 2020.

Why such a different outcome in 2022? The answer lies in the pricing of these options-based insurance policies. In short, portfolio protection has been consistently expensive on a relative basis, and the presence of a robust volatility risk premium (VRP) drives that relative richness.

What is the VRP?

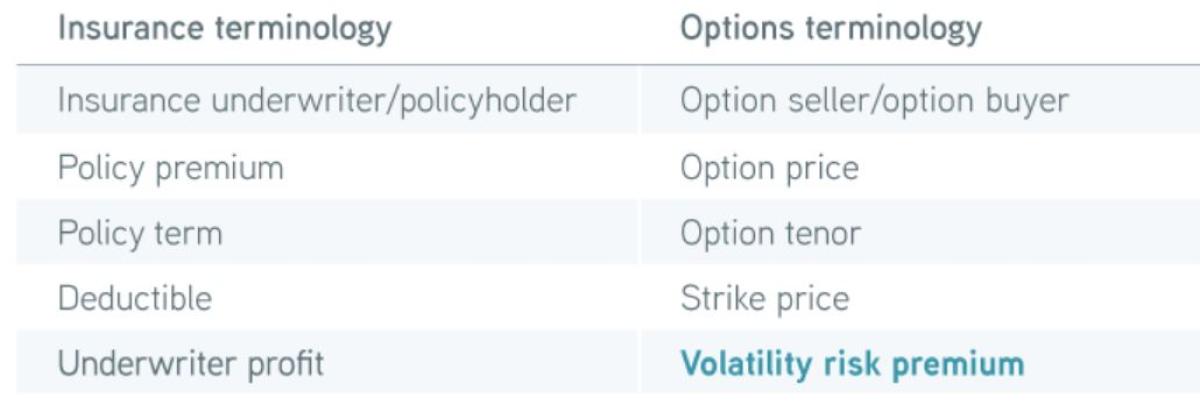

Just as we purchase insurance for homes and cars, investors can purchase insurance on their portfolios to hedge against unexpected market volatility. Like other insurance markets, options buyers don’t enter those transactions expecting a long-term profit. Profits instead accrue to options sellers—the party underwriting the risk that others seek to avoid—as insurance policies in a competitive marketplace are priced with an expected profit margin. For example, if 10 houses are estimated to burn down in an area each year, underwriters might price policies as if there would be claims on 20 homes, resulting in home insurance getting priced above its actuarial fair value.

Similarly, options contracts are priced with an expected or implied level of volatility, and this implied volatility has historically been persistently higher than what the market ultimately delivers. This excess volatility is known as the VRP, the tailwind that can ultimately create an expected profit for options sellers.

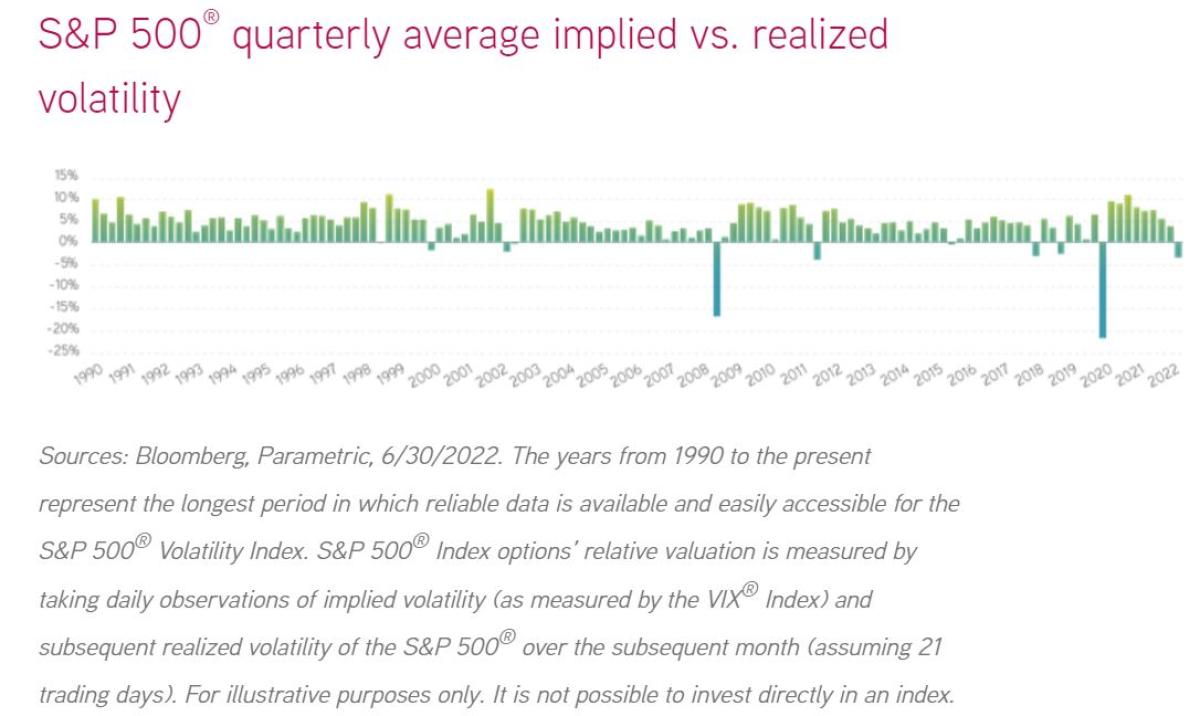

We most commonly measure the VRP as the difference between the implied volatility (IV) and subsequent realized volatility (RV) of the underlying security. The difference represents a relative value measure for volatility, and a positive VRP implies a tailwind for option sellers. As shown in the chart below based on historical data for the S&P 500®, IV exceeds RV in approximately 85% of the observations dating back to 1990 across a range of market environments. The size and persistence of this insurance risk premium reflects behavioral factors, such as loss aversion; structural factors, such as an imbalance of natural longs and shorts; and economic factors, such as the added value of convex assets with negative correlations.

Why should investors seek out the VRP now?

The most meaningful excess returns in traditional insurance markets have historically come on the back end of a significant event. Short-term losses for underwriters lead to rapid repricing of insurance and an expanded opportunity set in subsequent periods. This has also been the case historically with options-based VRP strategies: Persistently positive VRP has been most pronounced after a volatility event, improving opportunities for those willing to underwrite risk when risk aversion is at its highest.

In our view, this characterizes the environment of the past two-plus years as the destructive financial storms of early 2020 significantly altered the supply–demand dynamics in the options market. The long-term VRP—as measured by VIX® minus subsequent realized S&P 500® volatility—has averaged about four volatility points since 1990. But it’s averaged over 6.5 points since Q1 2020, leading to some of the most profitable periods for options-selling strategies in the past decade.

We see support for these recent trends to continue. Based on both investor consensus and forward volatility curves, we expect volatility to remain elevated against a challenging backdrop for traditional equity and fixed-income investments. While investors with long-term horizons are particularly well-suited to benefit from the historical tailwinds of the VRP, we believe the current environment—one of heightened investor concern, muted return expectations, and rising short-term rates—is especially compelling for prudent VRP strategies to shine.

How should investors harness the VRP?

We believe the best method of implementing a VRP strategy includes a focus on diversification, efficiency, accessibility, and transparency. This can be accomplished using listed options contracts on broad-based equity indexes. Rather than make active bets or forecasts on the direction of markets or volatility, investors should consider using a research-driven approach that aims to get in the path of a persistent risk premium effectively and consistently. Risk management is also a key element of a rules-based portfolio construction process: The sale of fully collateralized put and call options can help VRP investors avoid leverage.

Consider as well how home and auto insurance underwriters seek to diversify across property types and geographic areas. In a similar fashion, well-constructed VRP strategies can diversify across option tenors, strike prices, start and end dates (laddering of expirations), and underlying indexes. The end result is a low-cost, consistent approach that aims to deliver a diversifying risk premium to the end investor.

The bottom line

Many investors use VRP strategies to enhance returns while reducing overall portfolio risk. These VRP allocations may supplement existing equity portfolios, replace traditional low-volatility equity and hedged-equity strategies, or serve as a highly liquid component within an alternative asset allocation. The persistence of the VRP means these strategies don’t have to rely on market timing or active market bets to offer compelling diversification or potentially enhanced returns. That can be a useful tool in navigating portfolios through today’s challenging markets.

About the Authors:

Alex Zweber leads the investment team responsible for Parametric’s liquid alternative strategies. He has more than 15 years’ experience working in portfolio construction, trading, and portfolio management across both futures and options. In his various positions, he has worked closely with institutional and high-net-worth clients and their consultants to address investment and risk management needs. Previously, he was responsible for supporting the development and distribution of Parametric’s strategies in Europe and before that served as a senior portfolio manager on Parametric’s volatility risk premium solutions. Alex began his career in investment management in 2006 with the Clifton Group, acquired by Parametric in 2012.