By William (Bill) J. Kelly, CAIA, CEO of the CAIA Association.

Retirement plans were once qualified in every sense of the word. While being a qualified plan was mostly an IRS tax stricture in the 1920s to allow for the tax-advantaged deferral of retirement benefits, eventually the DOL and ERISA arrived on the scene and the notion of qualified (and quality) took on much higher meanings. In essence, the employer under a (qualified) defined benefit plan made certain contractual commitments to their employees that must be funded, audited, disclosed, and insured, and often protected and prioritized in the event of bankruptcy. The employee had to provide an honest day’s work over a clearly defined vesting period and the rest was up to the employer. Said employer had the resources and balance sheet to hire actuaries, treasury functions, and outside managers to navigate a thicket of investment and longevity risks, and when they came up short, the employer had to top-up that plan off their own balance sheet. Pretty complicated, but qualified people and entities were taking care of a complex series of risks that so many of us are simply unqualified to manage ourselves.

This column has written about the retirement crisis in various forms since its inception about a decade ago. Too Big Too Frail is now six years old and the problem has gotten even worse, when we are now potentially throwing a bit of gasoline under the siren song of democratization. That too has been covered here and Democratization Without Education made some of these same points a half decade ago. Yet as an industry, we continue to ignore the long term and obvious fiscal consequences, while we focus on giving the investor more ways to gain private market access via increasingly liquid wrappers, because that is what they are more qualified to want and to understand. I do wonder how the qualified investor squares that circle with the long-term, money-in-the-ground approach that is highly correlated with wealth accumulation in private (and public!) markets.

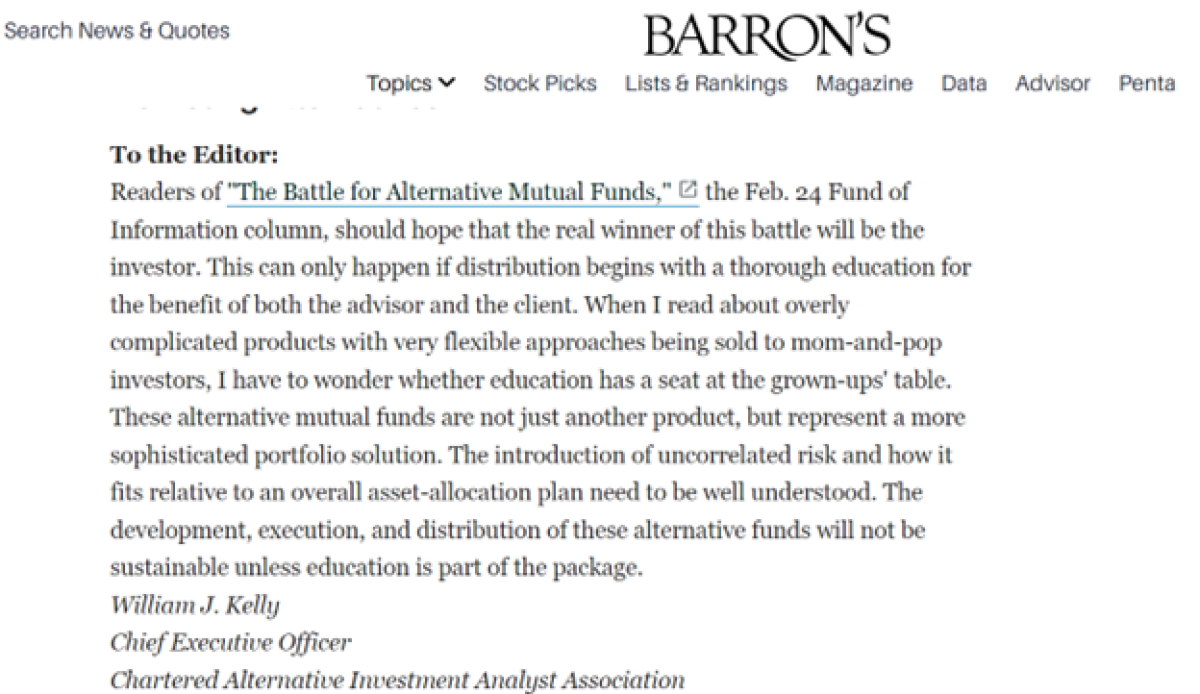

I joined CAIA Association just over 10 years ago and in that first quarter of my tenure in 2014, Barron’s wrote an article entitled The Battle for Alternative Mutual Funds. It clearly made the point of “the difficulty of the ongoing quest to incorporate alternative investments into mutual fund format” prompting me to fire off the following letter to the editor making a plea on behalf of the (unqualified) client:

And what lessons did we take away from this first wave of complex strategies packed into liquid wrappers? Very few I am afraid, as the “biggest winner” back then was the “very flexible” $21B Mainstay Marketfield fund (MFLDX). So flexible in fact that its current AUM flexed its way all the way down to $82M, looking a bit more like the “biggest loser” with assets of 0.4% of its 2014 self.

Another profiled fund was BXMMX which was a collaborative offering from Fidelity and Blackstone where the former had retail name recognition, and the latter knew something about fund selection in a multi-manager offering at a time when fund assets stood at $1.2B, only to be shut down about two years later. The staying power of these products proved fleeting, but maybe this time around it will be different? I am not so sure.

Spring is here in the northeast along with certain rights of passage … the crocuses have bloomed in my window box and Larry Fink’s latest annual letter popped in my inbox too. The latter is more nuanced on the E and the S, but the G and our collective governance responsibilities to “rethink retirement” get a fair amount of the ink this year and I am loving that. It is an excellent and actionable read about how to save and spend into retirement with due emphasis on the significant role of capitalism and the capital markets. More access is clearly part of the plan but through innovative models like the Superannuation Guarantee that we see in Australia and even some states in the US (a refrain I have often used myself— see minute 18 here with Ed Murphy). Under said structure, investment decisions are once again made by more qualified investors on behalf of less qualified beneficiaries.

Demographics in most developed countries are skewing older and life expectancies, thanks to advances in health care and lifestyle choice, are now making the octogenarian seem young and spry. Longevity risk is upon us, and we have no organized plan to address it, and this too is a particularly important part of Fink’s narrative.

Read the letter, reflect upon it, and commit to becoming part of the solution. History has taught us that leading with a democratized and more liquified offering will gather more assets in the short term, but our professional responsibilities should transcend us to a place where we all think more about long-term wealth accumulation, and outcomes that are far better correlated to the expectations and lifespans of the investors we serve.

Seek education, diversity of both your portfolio and people, and know your risk tolerance. Investing is for the long term.

About the Author:

William (Bill) J. Kelly, is the CEO of the CAIA Association with 30+ years in institutional asset management in successive CFO, COO, and CEO roles. A former CEO of Boston Partners and one of the founding partners of the predecessor firm, Boston Partners Asset Management, he's a global speaker and advocate for shareholder protection. Bill serves as Chairman of Boston Partners Trust Company and is an Advisory Board Member for the Certified Investment Fund Director Institute, which seeks to bring the highest levels of professionalism and governance to independent fund directors around the world. As a member of the board of the CAIA Association, Bill also represents CAIA in similar capacities via their global partnerships with other associations and global regulators.