By Anish Butani, Managing Director, Private Markets, and Kathryn Saklatvala, Senior Director, Head of Investment Content at bFinance.

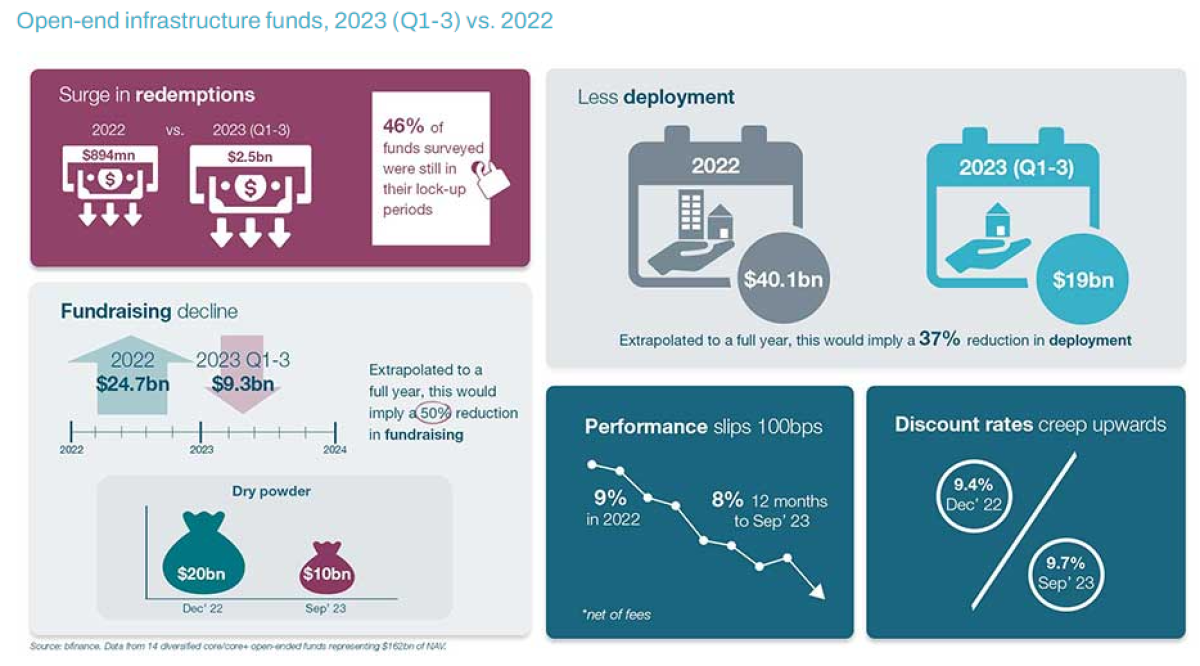

The year 2023 brought a slowdown in fundraising across private infrastructure funds – and private markets more broadly. While weaker investor sentiment is frustrating for closed-ended vehicles who may not reach their desired sizes, open-ended strategies can face more chilling consequences: gates, long queues, sub-optimal selling and even performance problems for the investors that remain. Open-ended infrastructure funds, however, are weathering the change of climate well so far. Fundraising is down and redemptions have shot up, but the attractions of core/core+ assets continued to support net inflows.

This article is part of a Liquid Private Markets series. Read Part 1 (Private Credit) here.

One year ago, we tracked a dramatic expansion in the number of open-ended infrastructure funds (see The explosive growth of open-end funds). Yet 2023 brought a change in dynamics. A new bfinance manager survey suggests that fundraising likely declined by 50% year-on-year: a sizeable drop, albeit less severe than 80% figure estimated by Infrastructure Investor for their closed-end counterparts.

Meanwhile, overall redemptions from open-end funds more than doubled. This figure could well have been worse were it not for the high proportion of funds that were still in their lock-up periods due to relatively recent launch dates (46%). Indeed, there were further fund launches in this period, with long-anticipated new offerings arriving from BlackRock, Macquarie and M&G (to name a few).

Funds have evidently reduced the pace of deployment activity (potentially down by a third) despite the net inflows. “Managers are very keen to deploy right now, with pricing definitely looking attractive,” says Anish Butani—who heads bfinance’s infrastructure manager research—in interview below, “but they are deploying more slowly in a weaker fundraising environment.” Performance has also declined a little: the post-Covid recovery play saw open-ended funds deliver returns averaging nearly 9% (net of fees) for the 12 months to December 2022, but this slipped 100bps to nearly 8% in the 12 months to October 2023.

Below, Butani discusses current challenges, the rapid evolution of the open-ended fund landscape and his outlook for the sector. “In 2023, this was clearly still a net inflow asset class,” he emphasises. “It has shown notable resilience compared to open-ended real estate… Despite the lower returns experienced in 2023, investors largely preferred to remain invested.”

Q: How do you view the change in fundraising/redemptions for open-end infrastructure?

I would say that the slowdown appears to reflect the current fundraising environment across infrastructure (and private markets more broadly), rather than a decrease in the appeal of this sector. In 2023, open-ended infrastructure clearly remained a net inflow asset class. It has shown notable resilience compared to open-ended real estate. There were no signs of distress, forced sales or gating. Investors largely preferred to remain invested, demonstrating confidence in the asset class. Infrastructure did not fall off a cliff in the way that real estate did: it held its value and continued to deliver a return, albeit a slightly lower one.

It's worth noting that many funds (46% in our study) were in lock-up periods: in general they do not permit redemptions within the first four years or so following launch, and a number of funds that were launched during the pandemic period offered very attractive fee discounts for the first few years for those early founder investors. Even for mature funds, investors do face a penalty for redemptions.

The continued growth and differentiation among new open-end fund launches, especially in sectors such as mid-market, renewables, and so-called infra 2.0, are interesting areas to watch. Investors and managers should stay agile and responsive to market changes.

Q: Why did the number of open-ended infra funds grow so rapidly during the pandemic?

The 2020-2022 period saw a dramatic surge in the number of open-ended funds, as discussed in an earlier report. In many cases, these were asset managers expanding their product suites beyond closed-ended vehicles.

The rapid growth of the open-ended fund landscape had a number of drivers. To some extent, of course, there was a bit of ‘jumping on the bandwagon’ as managers saw competitors raising open-ended vehicles and wanted to get on board. These strategies are mostly core/core+, but even a number of value-add players saw that they were missing out on a fundraising opportunity. Yet there are also some important fundamental factors.

One is the desire for an evergreen ‘anchor’ for investors’ allocations. As investors increased their commitments to this asset class, there emerged a demand for a permanent or 'forever' cornerstone in portfolios. This can be complemented by closed-end value-add funds to give a diversified and well-rounded approach. Open-ended funds typically target returns that are broadly in line with investors’ expectations for infrastructure allocations (around CPI plus 4-5% net of fees), which helps to affirm a role at the heart of portfolios.

"Some infrastructure assets are better suited for an evergreen-type vehicle"

Another important factor has been the evolving awareness that some infrastructure assets are better suited for an evergreen-type vehicle versus while others may be more appropriate for a closed-end vehicle. As first-generation (closed-end) infrastructure funds matured in the mid-2010s, it became evident that certain assets, such as utilities and operational renewables with long-term contracts, would be better suited for a permanent capital structure. This led to the development of the 'supercore' concept, which focuses on assets that don't necessarily require an exit strategy, delivering low-risk predictable cash flows. Today, the majority of open-end funds are still core-focused, emphasising stable and predictable cash flows, though there has been a shift towards core+ (e.g. platform buildouts and renewables development) in search of higher returns.

The 'forever invested' concept also has the added benefit of boosting investor Total Value to Paid In (TVPI): being continuously invested in open-ended funds over extended periods could theoretically result in a higher Multiple on Invested Capital (MOIC), thanks to the benefits of compounding and the option to reinvest dividends.

Q: How do you currently view the advantages and disadvantages of open-ended funds versus their closed-ended counterparts?

Open-ended funds do still offer faster deployment of capital: funds are typically called within twelve months, in contrast to the three-to-four-year period often seen with closed-ended funds, though we are keeping an eye on the slowdown in deployment (see above). Furthermore, open-ended funds often have an existing seed portfolio that investors can evaluate before deciding whether they would like to be involved, as opposed to the blind pool risk associated with closed-end funds.

There are disadvantages too, however. The pressure on managers to deploy capital can be intense, especially if fees are based on Net Asset Value (NAV), potentially leading to a rush in deployment and exposure to vintage concentration and early-year pricing trends for newer funds.

Additionally, performance fee structures based on unrealised NAV can be problematic, although clawbacks and carry ceilings can help. While the first wave of open-ended funds had classic carry structure based on valuation, it’s worth noting that more recent fund launches have structured performance fees differently with mechanisms put in place to mitigate these risks (portion of yield, dual test and so on). Now, with interest rates and inflation rising, we are seeing some managers reconsider their carry structure – not an immediately attractive change from investors’ perspective, but acceptable if it improves manager alignment.

Q: What’s your outlook for open-ended infrastructure funds now?

"In practice this really depends on the outlook for core/core+, since open-ended funds typically focus on this area."

We are often asked whether core is actually less attractive in a higher interest rate environment, due to being more highly leveraged than value-add infrastructure. The reality is more nuanced. With less capital available to chase core/core+ assets and discount rates edging higher, there is likely to be a downward impact on pricing, presenting more attractive opportunities for buyers. Managers are very keen to deploy right now, with pricing definitely looking attractive, but they are deploying more slowly in a weaker fundraising environment.

There are several forces at play when it comes to return expectations in core. First, you’ve got discount rate assumptions: to what extent are managers passing on movements in base rates? Managers that took a long-term view on risk free rates when valuing or acquiring assets at the tail end of the last cycle have been under less pressure to increase discount rates, while managers that took a more aggressive approach (using a lower risk-free rate) have been under more pressure to increase those discount rates. Next there are cash flow assumptions. (Should business forecasts be revisited to reflect higher inflation? When do assets need to be refinanced and will debt servicing requirements change?)

From an asset allocation perspective, investors still look to core/core+ infrastructure as a bedrock of allocations in this asset class, while exploring opportunities across the risk/return spectrum. We don’t see the allocations to core/core+ changing meaningfully going forwards.

As an aside, when thinking about core/core+, it’s worth thinking about the comparative attractions of infrastructure debt in today’s higher interest rate environment. We’re seeing parts of the investment grade infrastructure debt space offering all-in returns of 6%—not a dissimilar magnitude to core infrastructure equity in the last cycle . It’s hard to compare infrastructure debt with core infrastructure, of course, not least because the holding period is very different. But it’s a subject that I am seeing investors thinking about.

The landscape of open-ended infrastructure funds has undergone a transformation, shaped by evolving investor expectations, strategic fund management and market dynamics. While the pace of fundraising (and fund launches) has slowed, the sector continues to attract strong interest. The recent rollercoaster—Covid lockdown, high inflation, higher rates—has allowed these strategies to demonstrate resilience. Investors and managers alike will need to remain vigilant and adaptable over the coming years, ensuring that strategies align with ongoing shifts in investment conditions.

About the Authors:

Anish Butani is a Managing Director in the Private Markets team at bfinance and leads the firm’s coverage of the infrastructure asset class. Since joining bfinance in 2017, Anish has advised a broad range of clients globally in allocating over $10bn to the infrastructure asset class.

Kathryn Saklatvala joined bfinance in 2016 and oversees the firm’s investment content, thought leadership publications and investor research. She has also, since January 2020, been Chair of the firm's ESG and Responsible Investment Committee. An experienced writer, editor and researcher focused on investment management and institutional investors, Kathryn was previously a Managing Editor at Euromoney Institutional Investor. She holds a BA (Hons) and an MA from the University of Cambridge. Other previous roles include Editor of the Institutional Investor Networks, Director of the Sovereign Investor Institute and Associate Director of the European Institute. She has spoken and moderated at various industry conferences (OECD, World Bank Group, AVCA, IRN, Institutional Investor), been quoted occasionally in the press (Financial Times, Responsible Investor, Citywire) and been interviewed by the BBC on sovereign wealth fund trends.