By Chung-Hong Fu, Ph.D., Managing Director Economic Research and Analysis, Timberland Investment Resources, LLC.

Executive Summary

Lumber prices broke the $1,000 per thousand board feet (MBF) threshold, more than doubling the $400 average observed during the previous decade. Amid record markets for lumber, some investors are expressing interest in exploring whether investing in sawmills makes sense—in some cases as an extension to their timberland investment portfolios.

Several good arguments can be made for investing in sawmilling assets. First, the recovery of the U.S. housing market is creating an economic tailwind for building products that could be long-lasting. Some forecasts suggest that lumber demand could grow by 10 billion board feet (BBF), or 17 percent between 2020 and 2025. However, lumber output capacity in North America is only projected to increase by 3.3 BBF (or 4.6%). This suggests that lumber manufacturing capacity additions are falling short of new demand by close to 7 BBF, which is roughly equivalent to 25 large-scale sawmills. TIR believes this widening gap between lumber supply and demand can create opportunities for private investors to play a role in capitalizing on the expansion of the sawmilling sector.

A second argument in favor of investing in sawmills is that timber markets are very localized. Logs are bulky and it is expensive to transport them long distances. As a result, in the major timber-producing regions of North America, a variety of timber micro-markets have developed. For instance, the price of Southern pine sawtimber and chip-n-saw combined—the two log grades that are sawn and processed to manufacture lumber—have averaged as low as $15 a ton to as high as $32 a ton across the various micro-markets tracked by Forest2Market.

Investors in lumber manufacturing facilities can leverage the localized nature of wood markets to their advantage. Half to three-quarters of the expense associated with producing lumber is the cost of buying logs. One's ability to buy or build a mill in a timber market where log costs are comparatively low can have a significant influence on long-term performance. Our research has determined that a sawmill that is equipped with the latest proven technology and located in a reasonably-priced wood market in the U.S. South can be profitable when lumber prices are above $230 per MBF. In comparison, the price of Southern pine 2x4 lumber, when adjusted for inflation to current dollars, has averaged $440 per MBF for the past decade through 2020. Therefore, a "greenfield" mill, or a mill that is fully upgraded, can achieve operating profit margins of 40 to 60 percent through a lumber market cycle. At that level of profitability, an internal rate of return (IRR) above 20 percent is possible from a sawmill investment, depending on certain assumptions – such as construction costs and the use of leverage. This compares favorably with other types of investments in infrastructure and private equity.

Introduction

Timberland as a private equity investment option has existed since the early 1980s, with most investments being made through either commingled funds or individually managed accounts serviced by professional managers (timberland investment management organizations, or "TIMOs"). For four decades, the timberland asset class has been a viable option for diversifying portfolios that also contain stocks, bonds, and alternative investments. One logical extension of timberland investments that are often overlooked by investors is the primary manufacturing of timber. The business of manufacturing lumber or other solid wood products, of course, is quite different than the business of growing and harvesting trees. However, investing in sawmill assets can be an attractive option for investors who wish to complement the lower-risk profiles of their timberland assets by investing in higher-returning infrastructure and private equity-oriented opportunities that are higher in the value chain. Even investors that do not have exposure to timberland can find such investments to be additive and attractive. This white paper explains the nature, scope, and potential of such opportunities. It also profiles the types of investors that might be attracted to the concept of investing in sawmilling assets and explains why such opportunities might be compelling.

Investor Fit for Wood Products Manufacturing

Investing in a wood conversion facility can be a fit for a variety of investors. For timberland investors, it presents an opportunity to “move up the value chain.” For them, wood manufacturing can serve as a counterpoint to a timberland portfolio, as lumber markets can act as a natural hedge to timber markets. Periods of low timber prices that can undermine timberland returns can result in enhanced mill returns— and vice versa when timber prices are high.

For private equity and infrastructure investors, investing in a sawmill can be a way to expand beyond a few select sectors that are heavily subscribed. A great deal of private equity capital is channeled into a select number of markets and sectors, such as information technology, biotech, fintech, and digital health. Likewise, much of the investor capital designated for infrastructure has gone into solar and wind farms, pipelines, warehouses, and data centers. Consequently, placing capital in a sawmill project can be a way to extend or diversify one’s infrastructure or private equity allocations.

A third reason investors may be drawn to placing capital in a sawmill project is its environmental, social and governance (ESG) attributes. Facilities that manufacture lumber and wood panels often create jobs and support other forms of economic development – often in disadvantaged rural communities. As long-lived wood products, lumber and plywood products that are used for building and construction also store carbon, which means building with wood removes carbon dioxide—a “greenhouse” gas—from the atmosphere and thus helps combat global climate change.

Private Equity Exposure to Lumber Remains Limited

One of the most compelling advantages associated with investing in the sawmilling sector is that it is a relatively untapped investment arena. To date, very little private equity capital has gone into sawmill projects in North America. To our knowledge, only two fund managers are currently active in this space. In addition, while such activity cannot be categorized as private equity investing, another special-purpose acquisition company (SPAC) has acquired sawmilling assets in North America—and specifically in Canada. TIR has two theories that may explain why private equity activity in the wood products sector has been light. Private equity investment managers generally lack familiarity with the sawmilling sector because lumber and wood products manufacturing account for a relatively small segment of the economy—one that is overshadowed by other, more prominent and higher-growth industries, such as aerospace, renewable energy, telecommunications, transportation, and logistics. In addition, wood products producers have historically faced rounds of “feast or famine,” with repetitive periods of low profitability and losses. Given that private equity investors frequently utilize leverage, the cyclical nature of the industry, combined with its uneven profitability profile, has made it less attractive than other sectors for those investors operating in the context of the private equity business and investment model.

That said, interest could be changing. Investors are being drawn increasingly to the sawmilling sector by the strongest lumber market in history. Lumber prices broke past $1,000 per thousand board feet (MBF) in the first quarter of 2021—more than doubling the $400 MBF average observed during the previous decade. As markets for lumber set new records, more investors are exploring whether participating in opportunities to buy or build sawmilling assets makes good investment sense.

When Private Equity in Wood Products Manufacturing Makes Sense

There are three arguments investors should consider when evaluating opportunities to place capital in a lumber manufacturing facility:

1. Macroeconomic trends suggest growing demand exists or is developing for building products.

2. Investments by wood product companies in new or retrofitted manufacturing facilities have lagged current and projected market growth in the building products sector.

3. The diverse nature of a local wood market can be leveraged to create a competitive advantage for a milling facility that is targeted for capitalization.

Macro-Economic Trends Favor More Lumber Capacity

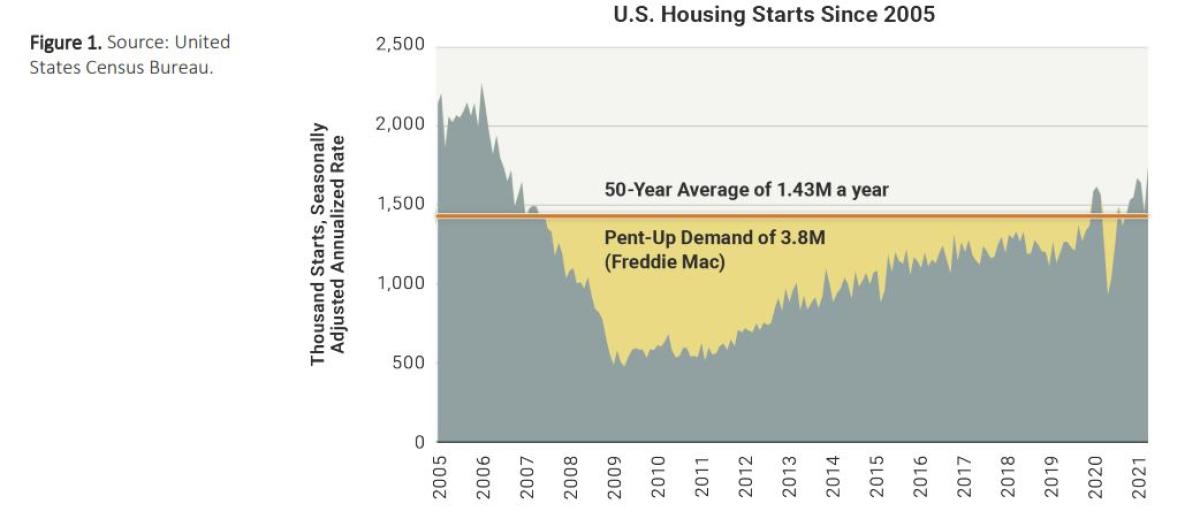

The current recovery of the U.S. housing market is creating an economic tailwind for building products that could be long-lasting. In the decade following the Global Financial Crisis (GFC) of 2008, new home construction fell well below fundamental demand. After peaking at 2.1 million in 2005, housing starts plummeted to a quarter of that level when the economy bottomed out as a result of the GFC. Meanwhile, market analysts generally agree that the U.S. needs to add 1.4 to 1.5 million new homes per year to keep pace with population growth and the need to replace its aging stock of existing homes. By 2020, Freddie Mac—a leading government-sponsored provider of mortgage financing—estimated that the housing deficit had reached 3.8 million homes (Figure 1).1 To catch up, housing starts need to remain above the 50- year average annual rate of 1.4 million homes for the next decade.

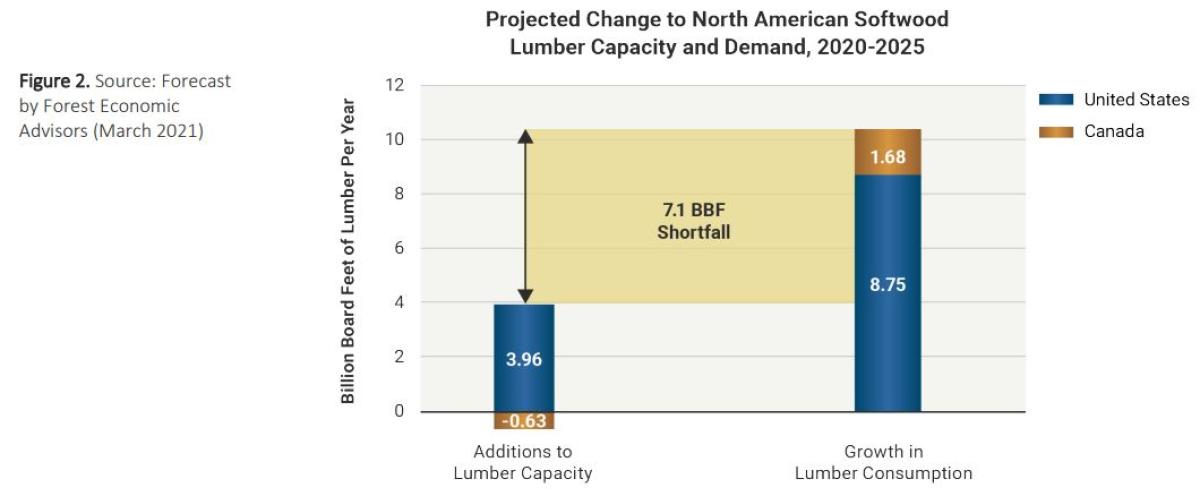

Economists predict that as home construction ramps up, lumber consumption in the U.S. and Canada will increase from 59 BBF in 2020 to 70 BBF by 2025 (Figure 2).2 Although demand may grow by 10 BBF, or 17 percent, over that five-year period, lumber capacity in North America is slated to rise by only 3.3 BBF (or 4.6%). This suggests building products manufacturing capacity additions are falling short of new demand by close to 7 BBF. This is roughly equivalent to 25 large-capacity sawmills.

Wood Product Companies May Not Close the Demand Gap Alone Major lumber producers clearly recognize these macroeconomic trends and have made significant investments to expand their manufacturing capacity in anticipation of a housing recovery driving demand and pricing for their products higher. However, as was mentioned earlier, these investments are likely to fall short. The extraordinary surge in lumber prices above $1,000 MBF in 2021 indicates that growth in manufacturing capacity is not keeping pace with rising demand for lumber and other wood-based building products.

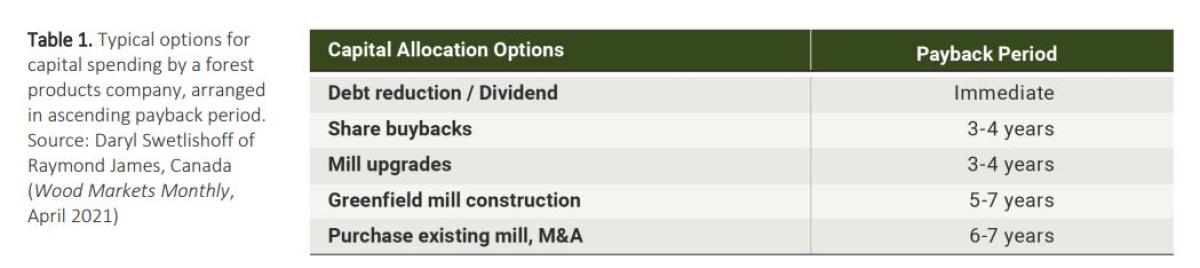

This capacity shortfall is being driven by the collective need among wood products companies to balance their capital allocations against their need to reduce debt, pay dividends and execute share buybacks. These tradeoffs are a reflection of the fact that most companies typically prioritize their capital spending activities and favor those with shorter payback periods (Table 1).

Given the capital allocation options available to lumber and wood products manufacturers, most make share buybacks and upgrades to their existing facilities higher priorities than building new, "greenfield" mills. This is because mill construction projects offer longer payback periods due to the fact that it normally takes two years to build a new facility – and an additional year to see the mill ramp up to its full production capacity.

For these reasons, wood product manufacturing companies, whether they be public or private, tend to be conservative when making large capital investments. Evidence of this is the fact that, despite growing demand for building products, and the availability of large volumes of competitively priced raw timber in the Southeast, which is already the largest timber-producing region in both North America and the world, mills are only being retrofitted and expanded at a rate of two to three per year. Likewise, the number of "greenfield" mills being constructed also has lagged demand, with only one or two new mills being constructed per year. This measured pace of growth by lumber manufacturers has created an opportunity for private equity investors to fill the capacity gap at a time when both current demand and future demand expectations are robust.

Private Equity Can Make Targeted Investments in Low-Cost Wood Markets

The third and final reason private equity investment in sawmilling assets can be successful is that while lumber is a commodity, our most productive working forests are geographically localized.

With a commodity like lumber, a common market exists—one that is accessible to all sellers. A private equity investment that is made in a single mill, or investments that are made in a select number of mills, can perform well because end-use product pricing tends to be uniform and consistent. In other words, a single mill owned by one or more private equity investors can sell its lumber into the market and obtain the same pricing that a corporate player which may own several mills can generate. In addition, breaking into the market is a relatively straightforward exercise. This is evidenced by the low level of market concentration that characterizes the sawmilling sector. The four largest softwood lumber producers in North America are West Fraser, Canfor, Weyerhaeuser, and Interfor. On a combined basis, these four companies own 93 sawmills, yet, as of 2020, they only had a combined market share of 28 percent (28.4 percent to be precise).3 This means the industry remains relatively fragmented, with smaller producers competing and co-existing side-by-side with much larger ones.

In contrast to lumber markets, timber markets are localized. Logs are extremely bulky and expensive to transport long distances. For this reason, most of the timber purchased by sawmills to support their manufacturing operations is harvested within 100 miles (160 kilometers)—and, in most cases, typically from no more than 60 miles away (~100 kilometers). As a result, this creates a plethora of timber micro-markets in the major wood-producing regions of North America, including the U.S. South and the Pacific Northwest. Timber markets where competition for logs is acute tend to be characterized by higher prices and more volatility than those where there are fewer and smaller log buyers.

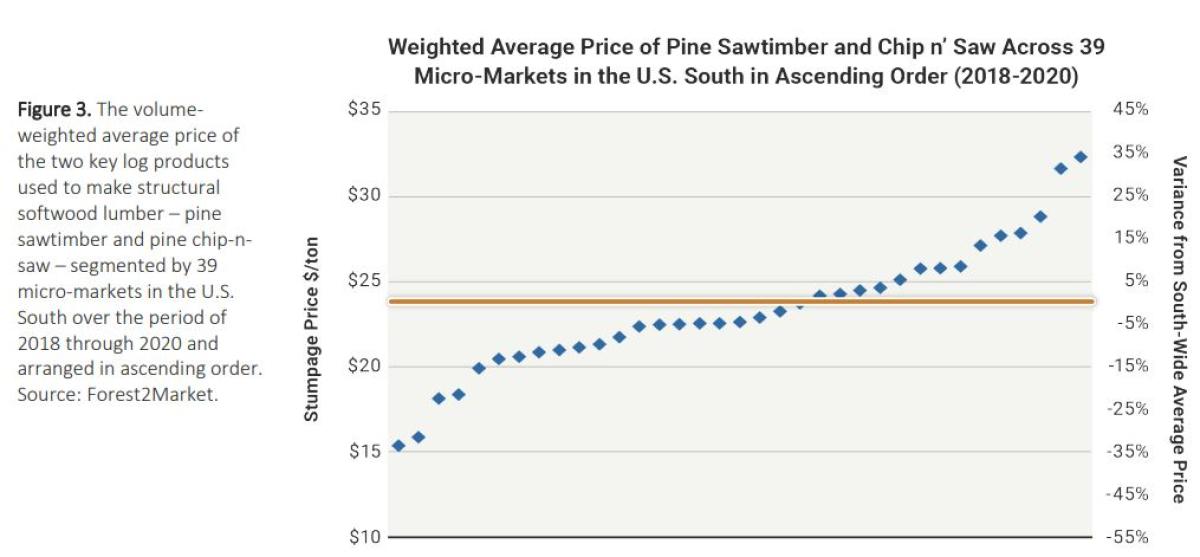

These differences in local wood markets can be dramatic. The timber price reporting service, Forest2Market, for example, has identified close to 40 different micro-markets across the U.S. South alone. The price of sawtimber and chip-n-saw combined – the two log grades that are purchased and sawn to produce lumber—has been a low as $15 a ton—to as high as $32 across the various micro-markets Forest2Market tracks (see Figure 3). This range equates to an average that is 35 percent above and 35 percent below the South-wide average.

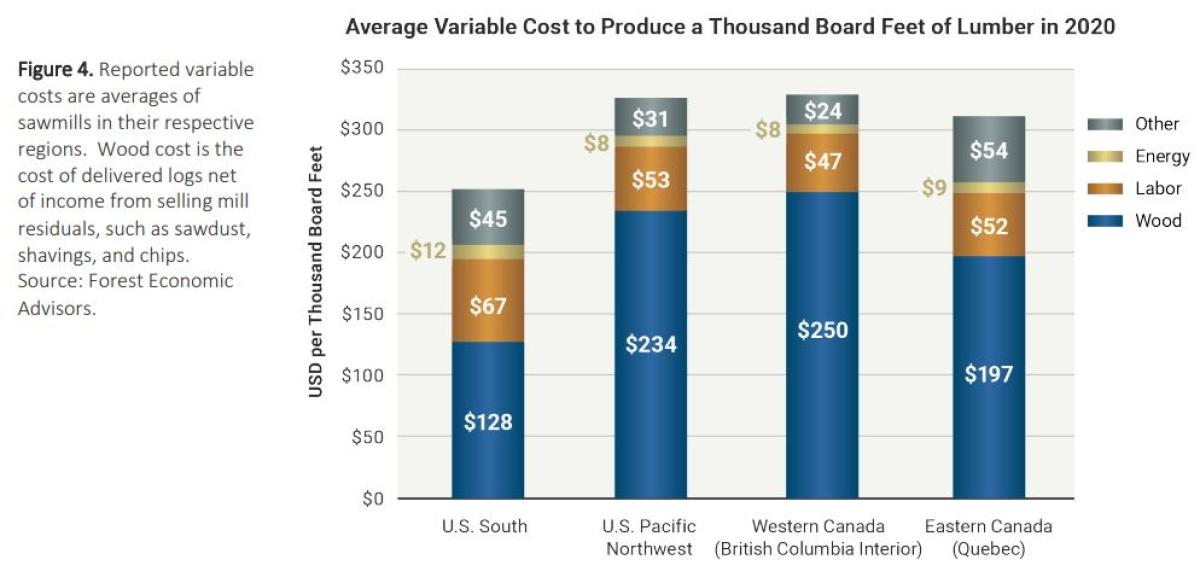

Investors in lumber manufacturing facilities can exploit the localized nature of wood markets to their advantage because half to three-quarters of the cost of manufacturing lumber comes from the cost of purchasing logs (Figure 4). This means that private equity investors are well positioned to influence the long-term performance of a sawmill investment by choosing to operate in areas where logs are plentiful and where log pricing is low due to slack competition.

Performance Potential of a Sawmill Investment

Beyond wood costs, another factor that can determine the success of a sawmill investment is productivity. By productivity, we mean how much lumber can be produced from a log. Fortunately, advances in mill technology in the last three decades have greatly increased the efficiency of how logs are converted into lumber.

In the 1980s, industrial softwood sawmills needed 5.4 tons to produce a thousand board feet of lumber.4 By the early 2000’s, however, the average rate dropped to 4.6 tons. Following the Global Financial Crisis, many sawmills in the United States, including many in the South, underwent expansions and equipment modernizations. Also, many smaller and less efficient mills were shut down. Today, mills in the South only need 4.3 tons of timber, on average, to make one thousand board feet of lumber. This is a 25 percent productivity gain relative to prevailing conditions in the 1980s. Furthermore, additional gains are anticipated for the future. In fact, new mills that make use of "best-in-class" processing technologies can run at conversion rates of 4.0 tons or less.

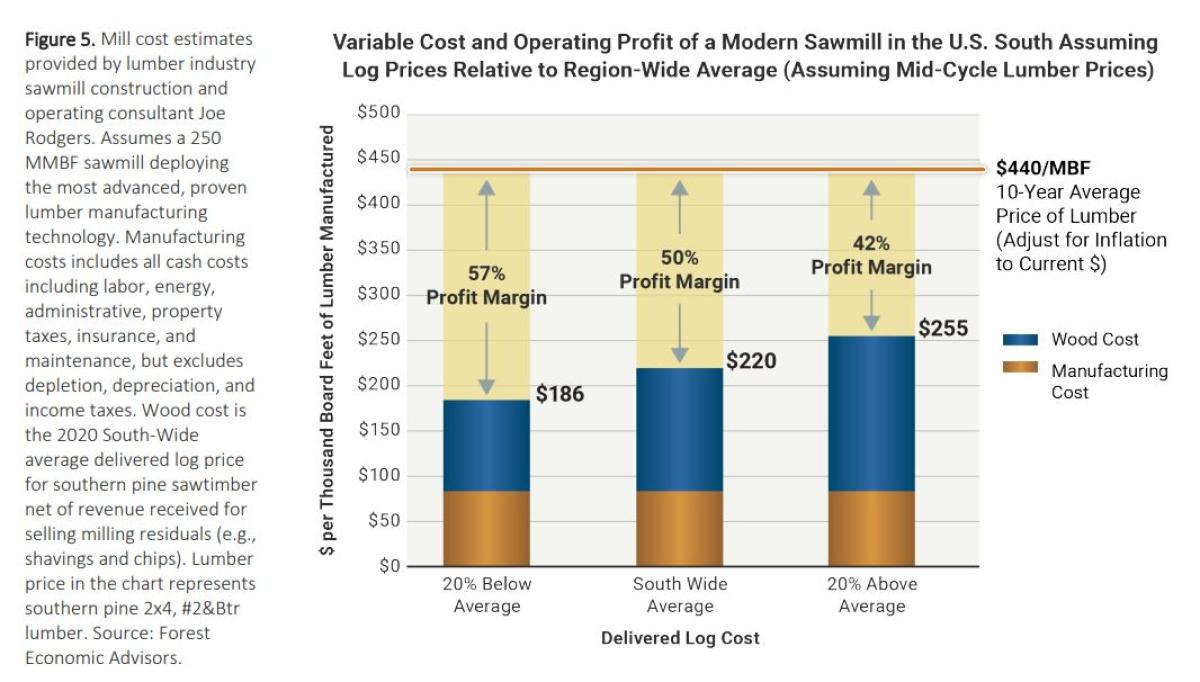

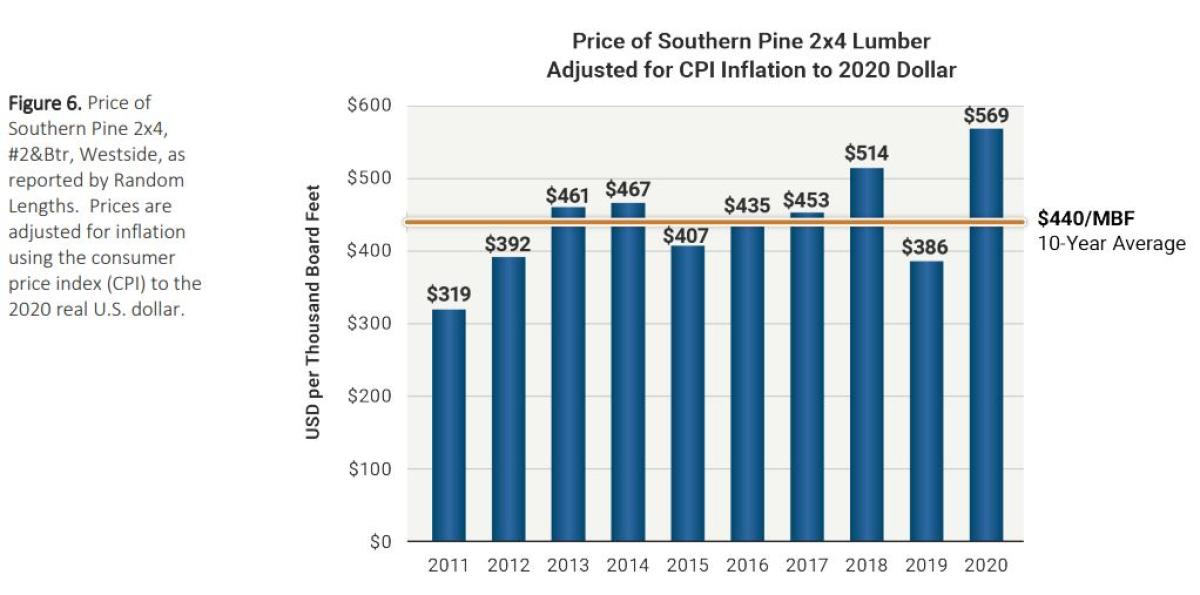

Given the increased efficiency these improvements have allowed, investments in wood product facilities are compelling under the right conditions. TIR's research has determined that a sawmill that is equipped with the latest proven technology and that is located in a reasonably-priced wood market in the U.S. South can be profitable when lumber prices are above $230 per MBF (Figure 5). In comparison, the price of Southern pine 2x4 lumber, when adjusted for inflation to current dollars, has averaged $440 per MBF for the past decade through 2020 (Figure 6). Therefore, a “greenfield” mill, or a mill that is fully upgraded, could see operating profit margins average 40 percent to 60 percent across the average lumber market cycle. At that level of profitability, an internal rate of return (IRR) above 20 percent is possible from a sawmill investment, depending on certain assumptions, such as those relating to construction costs and the use of leverage. This compares quite favorably with other types of investments in infrastructure and private equity.

Summary and Recommendations

To conclude, industries that convert timber into wood products, such as lumber, can provide attractive investment opportunities for private equity investors that have an infrastructure and project finance orientation. Sawmills that are reconstructed or built from scratch with the latest technologies can remain profitable across the lumber market cycle. Returns improve further if the mill is located in a low-cost wood market. This type of investment is well-suited for investors with patient capital and long-term outlooks. Such investors are typically willing to accept the year-to-year risk and volatility associated with participating in a commodity-driven market in order to achieve returns on par with those that can be achieved through venture-type investments or participation in opportunistic infrastructure funds.

Investors with timberland portfolios should note that it is not necessary for mills to be vertically integrated with forest resources. Mills can operate successfully without being co-located with a timberland base that is also under its control. Instead, most wood product manufacturers in the U.S. rely on active private markets—purchasing logs from a wide variety of private forestland owners.

If an investor is considering a private equity investment in a sawmill or another type of wood manufacturing facility, selecting the right manager can be a critical decision. Such managers should have the expertise and capabilities to scope, model, and execute a well-conceived sawmill investment. This includes having the ability to (a) identify a suitable "greenfield" location or an existing sawmill that is available for purchase; (b) navigate the myriad of regulatory, policy, and permitting processes associated with such undertakings; (c) negotiate for the best possible state and local incentives; (d) hire talented senior management to lead the sawmilling enterprise; (e) oversee equipment retrofitting or construction and the ultimate operation of the facility; (f) attain the highest level of ESG standards, and (g) execute an exit strategy that will maximize returns.

Footnotes:

1 Freddie Mac, “One of the Most Important Challenges our Industry will Face: The Significant Shortage of Starter Homes” (April 15, 2021).

2 Forest Economic Advisors: Long-Term Timber Forecast (March 2021).

3 Forest Economic Advisors, “The ‘Top 10’ 2020 Canadian Lumber producers Survey Reflect the Impacts of the Covid-19 Pandemic on the Industry” (April 27, 2021),

4 Source: Forisk Consulting.

About the Author:

Hong oversees all economic and market analysis and forecasting for TIR and plays a key role in the development and implementation of the firm’s investment strategy. He was a founding member of TIR and was instrumental in establishing the firm’s research-driven investment ethic.

Hong began his career at Temple-Inland Forest Products Corporation where he served as a resource utilization specialist and business analyst. In these roles, he provided economic and research analysis services that were used by senior executives within the company to make strategic decisions across a range of issues, including asset securitization, acquisitions, and resource and business optimization. Prior to joining TIR in 2003, Hong served as a senior investment analyst with Global Forest Partners where he performed global timber acquisition analysis, created a variety of decision support models, and directed currency risk management analysis. Hong is recognized in the timberland investment arena for his measured and comprehensive analysis of the trends and events that drive investment performance and that influence the long-term risk and return profile of the timberland asset class. He writes extensively on these and related topics and is frequently consulted by market participants and analysts, including the news media, for his unique and well-informed perspectives. Hong is a graduate of Northwestern University where he received a BS in biology. He also earned an MS in environmental management at Duke University and an MBA at Columbia University. He received his Ph.D. in forest economics at North Carolina State University.

Disclaimer This paper is provided for the education of its readers. The opinions and forecasts made are for informative purposes only and are not intended to represent the performance of an investment made through Timberland Investment Resources, LLC. No assurances are made, explicit or implied, that one’s own investments in timberland or with Timberland Investment Resources, LLC specifically, will perform like what has been described in the paper.