By Hunter Hopcroft, Managing Director of Portfolio Solutions for Armada ETF Advisors, an ETF issuer focused on quantitative REIT research and asset management.

First Industrial (FR), Rexford Industrial (REXR) and Developing the Investor's View of Valuations

A primary attraction of public REIT investing is the data provided by the large and (usually) liquid private real estate market. Because institutional real estate assets are relatively homogenous within asset classes, the private market can provide a more-or-less real time appraisal of the assets sitting on REIT balance sheets. This naturally creates a desire to adjust public REIT disclosures to calculate a public-to-private comparable valuation of the assets.

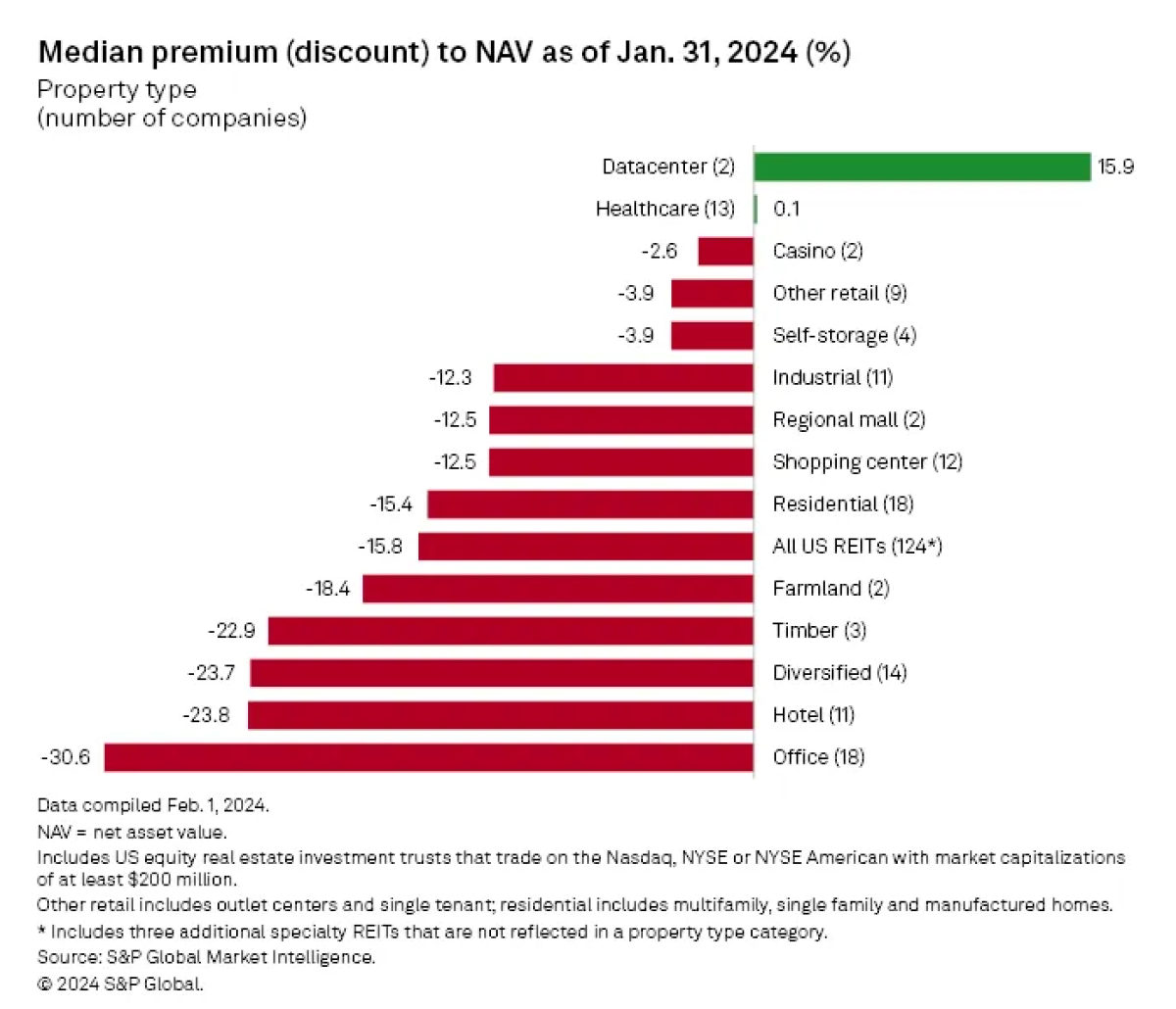

S&P Global released a US REIT NAV monitor last week that put the median REIT at a 15% discount to Net Asset Values (NAVs). Analysts use a variety of methods to arrive at NAVs, but the underlying logic is that the value of assets implied by equity market cap, and by extension enterprise value, will deviate from the fair market values of those assets. Do these discounts create a compelling entry point for REITs? Historically REITs trade at a slight premium to NAV, but determining these values, and any perceived discount or premium, should only be an input to an investment process, not a thesis in itself.

I am going to partially elucidate that process focusing on First Industrial Real Estate Trust, a mid-sized REIT that owns approximately 65 million square feet of industrial assets. The purpose of this analysis is not to uncover some truer, higher fidelity approach to deriving net asset values, nor is it to make an investment judgement about First Industrial (yet). Any process of a valuation is only half the work of investing. The harder, more interesting work is developing a differentiated view of the future that will impact that valuation.

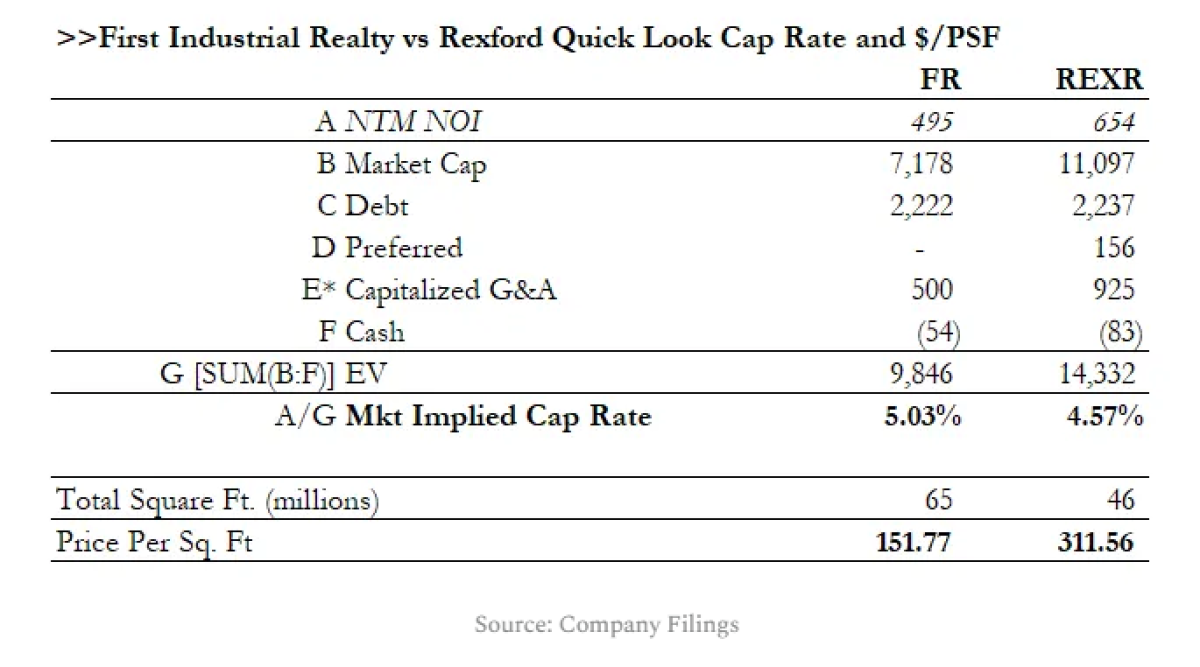

Quick Look

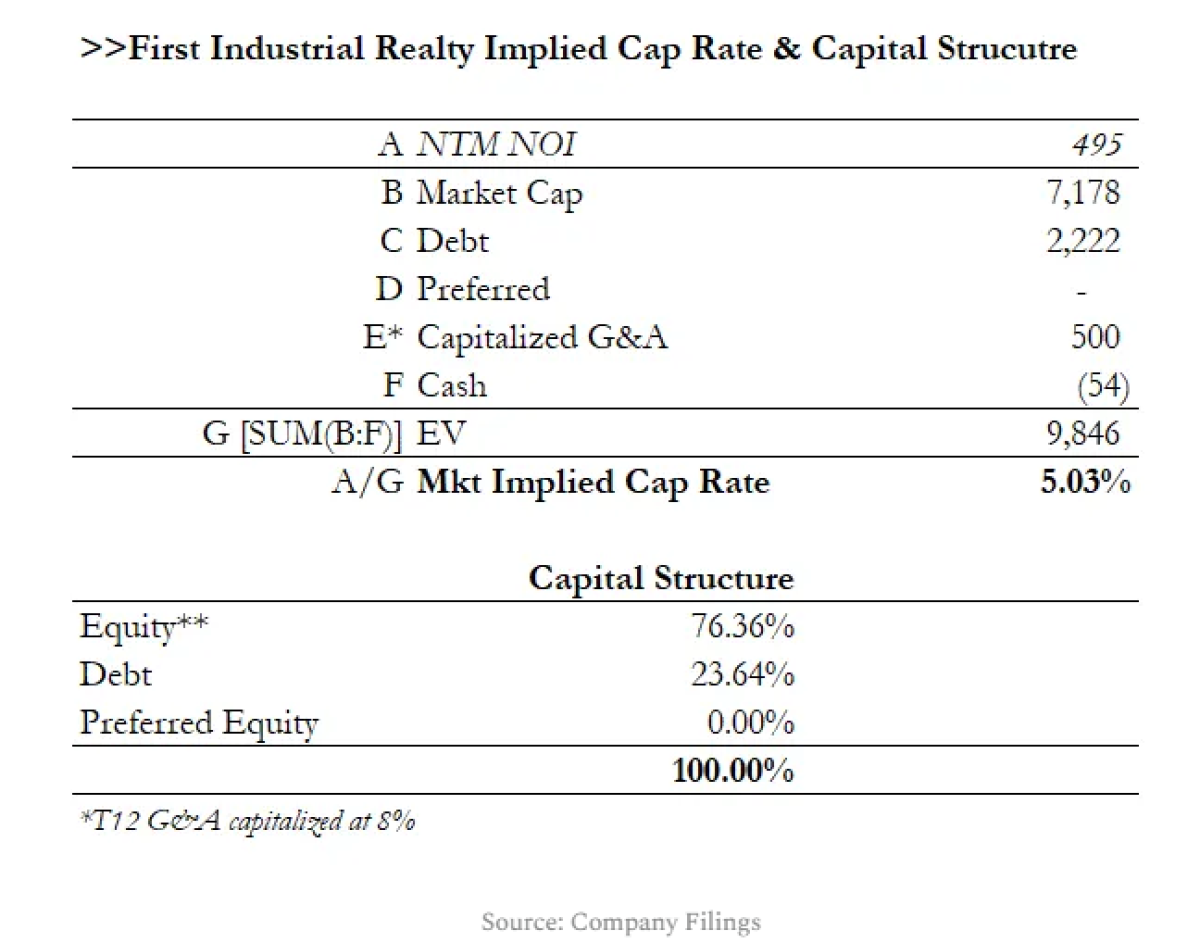

Like any multiple, cap rates are more valuable as a relative measure. Ignoring briefly cost of capital concerns, what cap rates really signal is prospective growth. After all, why would one accept a paltry spread against risk-free options if not for the potential growth in the numerator? Below is my "quick look" at the implied cap rate for First Industrial. It admittedly makes a handful of simplifying assumptions.

Foremost, I ignore some realities of a true private market transaction, for example, how NOI would be impacted by taxes. Our goal here is not to be investment bankers, rather to quickly and consistently arrive at a view of how the market is pricing the growth prospects of a REIT's underlying portfolio.

One brazenly unscientific element is adjusting for the "platform value" of the internally owned REIT manager. I put a 12x multiple on the trailing 12 months General & Administrative expenses and remove this from the enterprise value. The market presumably puts some value on the infrastructure and talent of the management team and this step helps adjust enterprise value to reflect, as closely as possible, how the market is valuing the underlying real estate.

Focus on SoCal

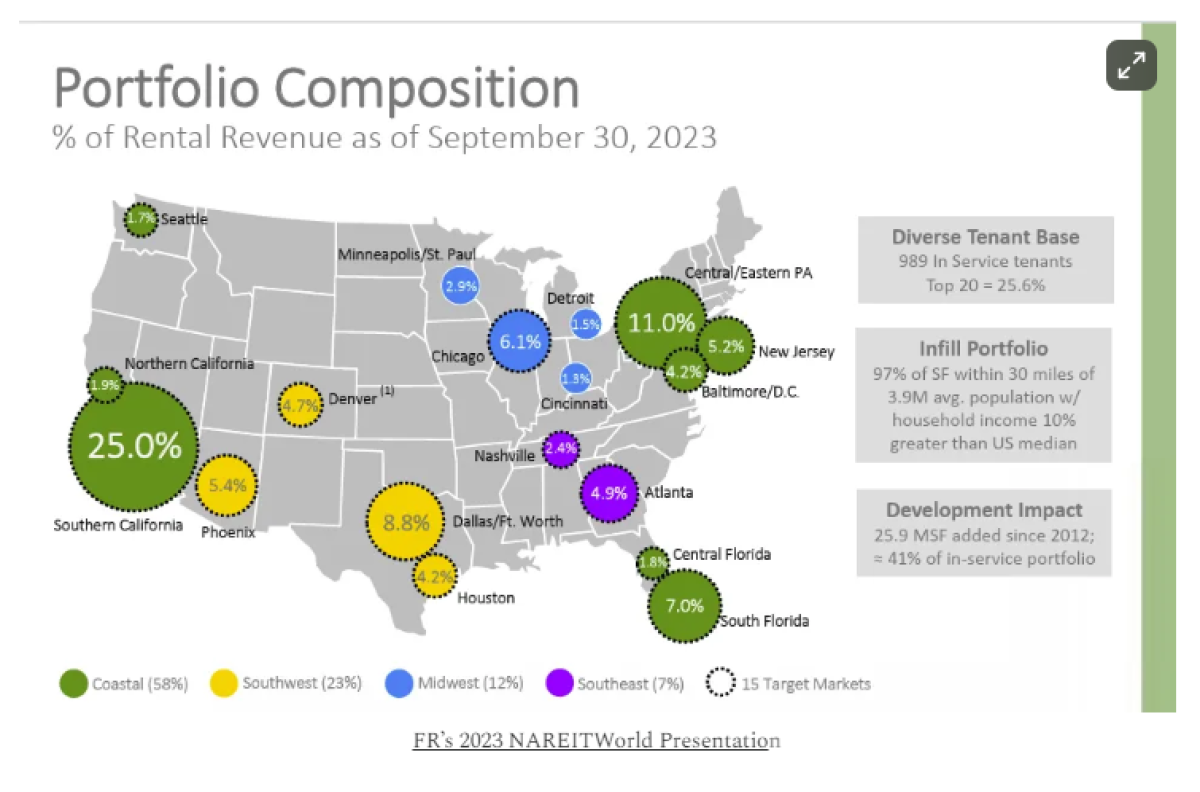

FR owns primarily logistics properties with an average facility size of ~150,000 square feet in Coastal and other supply-chain critical geographies. Half of the portfolio (32 million square feet) is in four major markets: Southern California, Eastern/Central Pennsylvania, Dallas-Ft. Worth and Chicago.

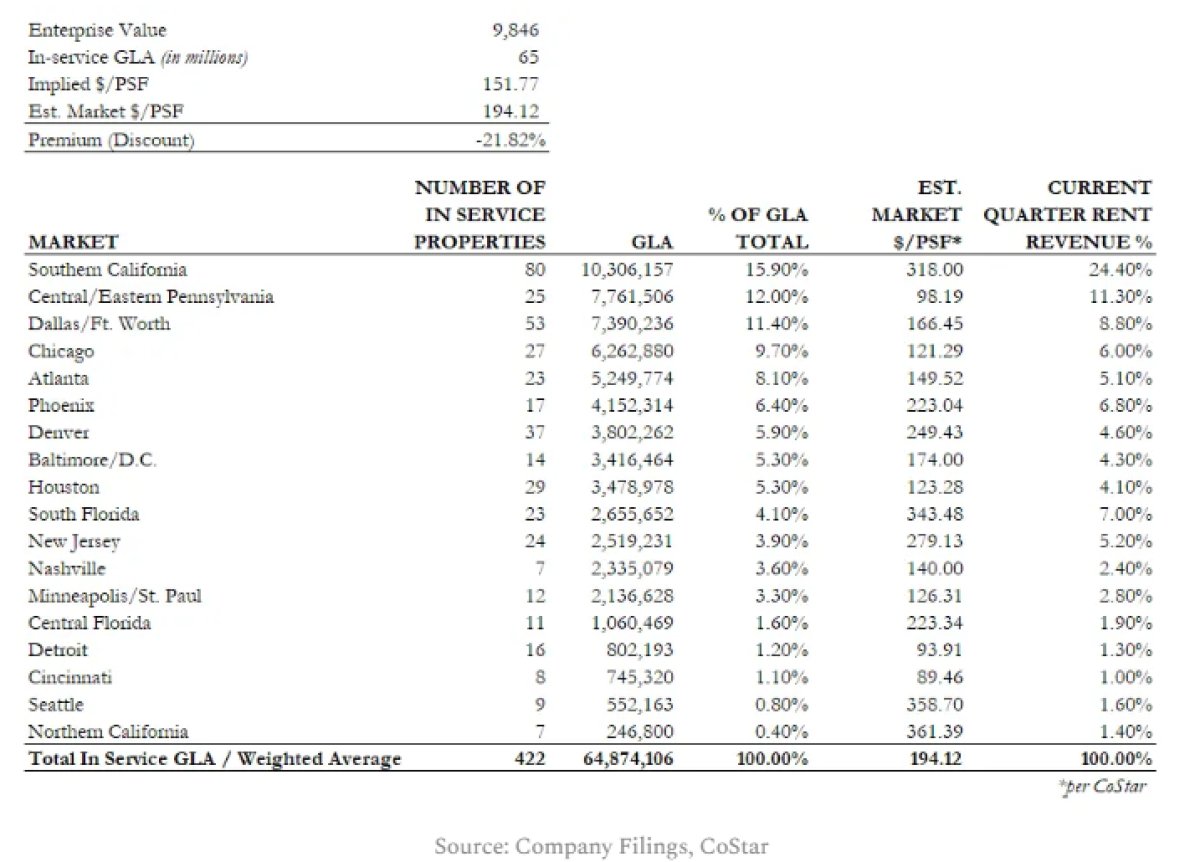

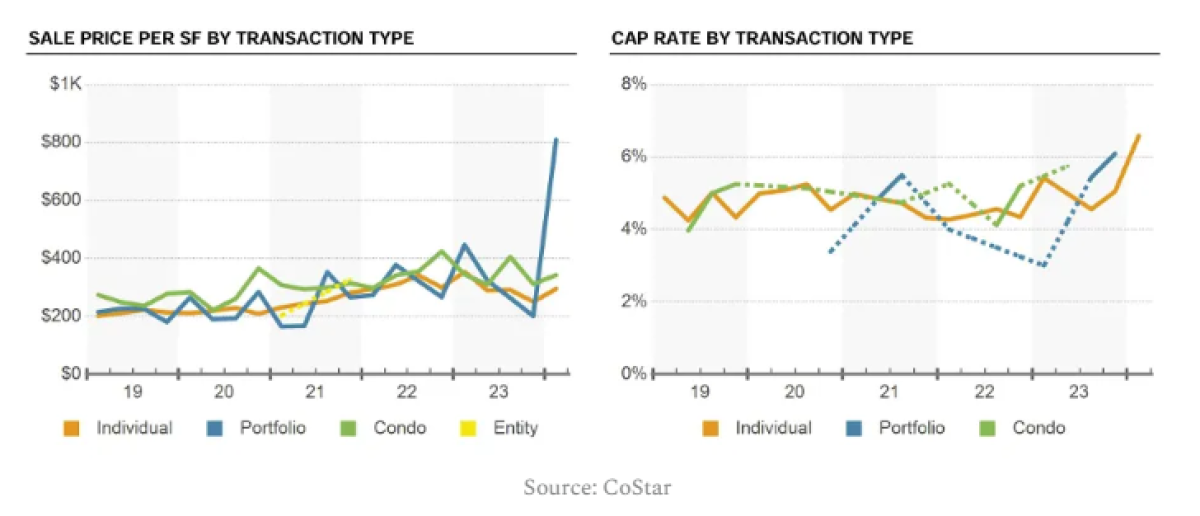

Returning to our adjusted enterprise value calculation, FR's industrial portfolio is priced at $152 per square foot. We rationalize this number looking at CoStar's reported sales price per square foot estimates for these markets. Weighting these estimates by FR's geographic exposure produces a price per square foot of $194, a 28% premium to the current market price. But is it really?

Let's focus on Southern California, where CoStar estimates private market values at $318 per square foot. FR has 16% of their leasable footprint in SoCal and it accounts for over 25% of their rental revenue. Using Rexford Industrial , which owns 45 million square feet exclusively throughout Southern California, as a public market comparable shows a tighter implied cap rate and price per square foot closer $310.

Part of this spread has to do with nuanced differences in their portfolios. Rexford focuses exclusively on this market and tends to lease to smaller companies than First Industrial. They also lease for other uses besides logistics and can drive rental rates through specific amenities and smaller leases. Rexford earns a blended rate of $15.22 per square foot in this market versus $10.46 per square foot for First Industrial -- although FR has some large renewals coming this year.

You could continue this analysis further, looking at county by county occupancy, the age of the portfolios and lease roll-offs. Perhaps most importantly FR pursues ground-up land development as its primary growth strategy while REXR focuses on traditional acquisition and repositioning. Higher rates and construction costs will squeeze FR's development margins. Somewhere an enterprising analyst is no doubt crunching these numbers, and while all of these factors may contribute to a perceived discount to NAV, they are not fundamentally reasons why the discount exists.

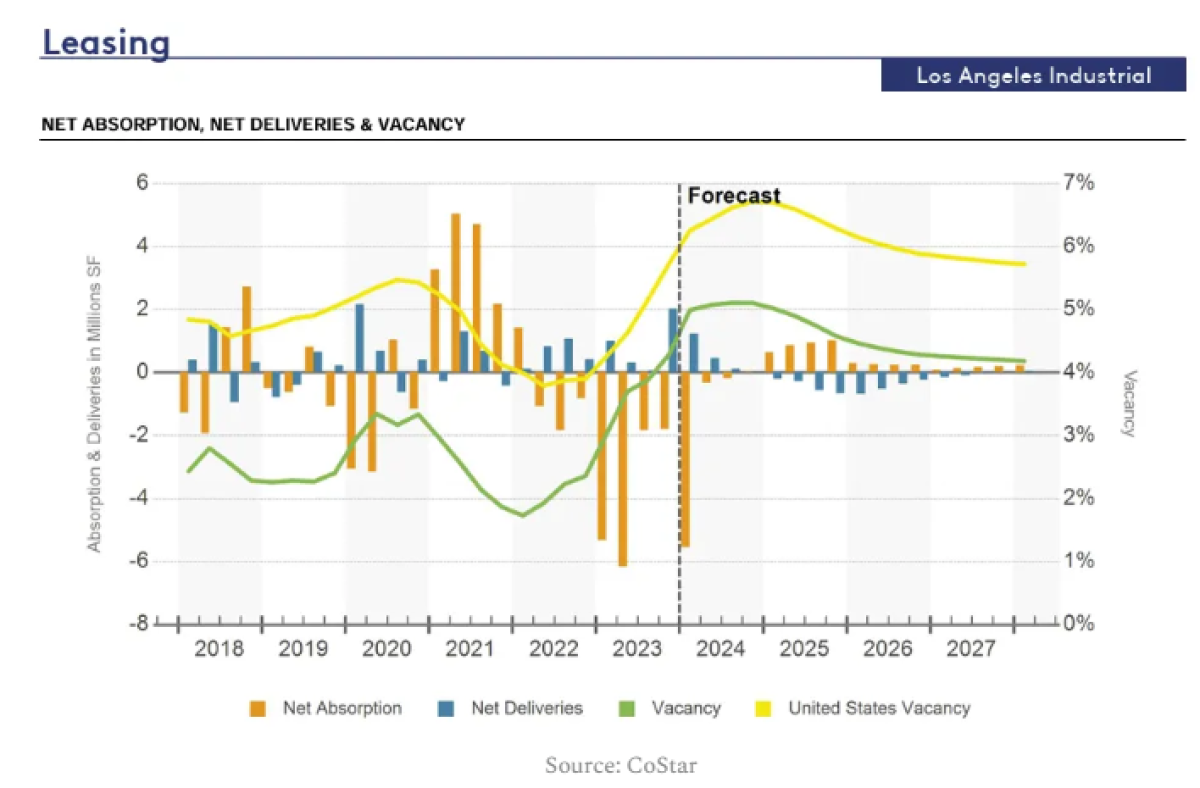

FR's next four largest markets (Central Pennsylvania, Dallas, Chicago & Atlanta) by both leasable area and rental revenue have an estimated blended market value of $170 per square foot, a more modest 11% premium to the current market price. The market is signaling further deterioration of Southern California industrial, and specifically logistics facilities as consumer spending softens and supply chains orient away from Asia.

Per CoStar, Los Angeles is experiencing a wave of supply deliveries that are pressuring absorption. Interestingly, because of the regulatory environment CoStar reports that construction starts may continue in spite of weakening fundamentals simply because they were put into motion years prior. CoStar,

Many projects now underway were planned years earlier due to development challenges in entitlements and permitting, so developers are more likely to carry projects forward even as broader market conditions soften.

Discounts to NAV tell you more about the fundamentals of the markets a REIT operates in than they expose some glaring inefficiency in REIT share prices. As an investor you must develop a vision of the future that either justifies the discount or gives cause for it to close.

Nearshoring as an investment thesis has begun to take hold, even become consensus. Geopolitical tensions continue to gum up international trade routes. The memory of stocking shortfalls during COVID have encouraged diversity of supply chains, but not a total disavowal of just-in-time inventory. Savannah, Georgia is poised to be one of the fastest growing industrial markets in the Country. Its port, the second largest on the East Coast and the fourth largest in the US is benefitting from these trends. Per Globe Street,

Georgia Ports Authority (GPA), which operates the port, has invested $374 million to create the largest on-dock rail facility in the Western Hemisphere. It is also constructing a number of inland ports to enable goods to be transported efficiently by train, instead of on busy highways.

In September the International Longshore Warehouse Union (ILWU) and The Pacific Maritime Association (PMA) reached a new labor agreement after the prior contract had expired in summer of 2022. The ILWU, which represents dockworkers from Washington state to California has not been timid about disrupting the ports during negotiations. Deliberate slowdowns, understaffing, even going so far as to not stagger shifts during mealtimes have cost retailers billions in the past. Importers began shifting volume to East Coast ports in response to the uncertainty around the negotiations.

The new six-year contract secured dockworkers a 32% salary increase. With the threat of labor related slowdowns removed, some of that import volume has begun to return to the Port of Los Angeles.

In September, the contract between The International Longshoreman (ILA) and The United States Maritime Alliance (USMA) will expire. Like their West Coast counterparts these organizations represent the dock workers and terminal owners of the East Coast ports respectively.

Harold Daggett, President of the ILA is already preparing workers for a strike saying, "It’s time for foreign companies like Maersk and MSC to realize that you need us as much as we need you." The relative truth of that statement gets to the core of the negotiations. A major point of contention for the ILA is automation. Daggett told members in a “fiery speech” at their July conference,

If foreign-owned companies like Maersk and MSC try to replace our jobs with automation, they are going to get a painful reminder that longshore workers brought these companies to where they are today.

Will the Ludditen position of the ILA bring East Coast ports to a halt, reorienting supply chains back to the West Coast? Will higher interest rates and construction costs finally forestall industrial development in Los Angeles? In concert, these events could dramatically change the outlook for the Southern California industrial market, and in turn, the share prices of both First Industrial and Rexford.

The thoughtful public REIT investor does not need to model the next 12 months of First Industrial lease renewals, tune the sensitivity of development margins nor become a geopolitical analyst. No, instead to understand where the industrial market is headed, they should begin learning the machinations of labor negotiations, surveying the viability of port automation technology and developing a view of the future not yet captured in public market prices.

Net asset values, truly any type of valuation, can help give you a clearer-eyed view of the present, but they cannot fundamentally tell you the future. The hard work of investing is not in simply organizing ever more minute details, it is in having the boldness to envision future states not yet fully realized.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Hunter Hopcroft is the Managing Director of Portfolio Solutions for Armada ETF Advisors, an ETF issuer focused on quantitative REIT research and asset management.

Prior to joining Armada, Hunter was the Alternative and Real Assets Portfolio Manager for an RIA based in Richmond, Virginia. In that role, he directed allocations to private equity, hedge funds, REITs, and Structured Products. Previously, he was a capital markets advisor for a consulting firm focused on large-scale timber acquisitions.

Hunter has advised on capital formation for both emerging real estate sponsors as well as institutional groups and serves on the investment committee of a private equity real estate fund.