By Richard Bookstaber, Ph.D., co-founder and Head of Risk at Fabric.

If you're hedging using leverage, you're cooking with gasoline.

For financial markets, nothing is as violent as the mixture of leverage and illiquidity. Usually this plays out in hedge funds because that is where leverage resides. And in stretching for alpha, that is where positions become concentrated beyond the point that they can make it out the door when margin calls come knocking.

At the opposite end of the spectrum lie pension funds. Staid, sober, with boards that govern to safeguard the trust of pensioners whose financial wellbeing depends on prudence buttressed by rigorous risk management. Well, at least that’s the U.S.

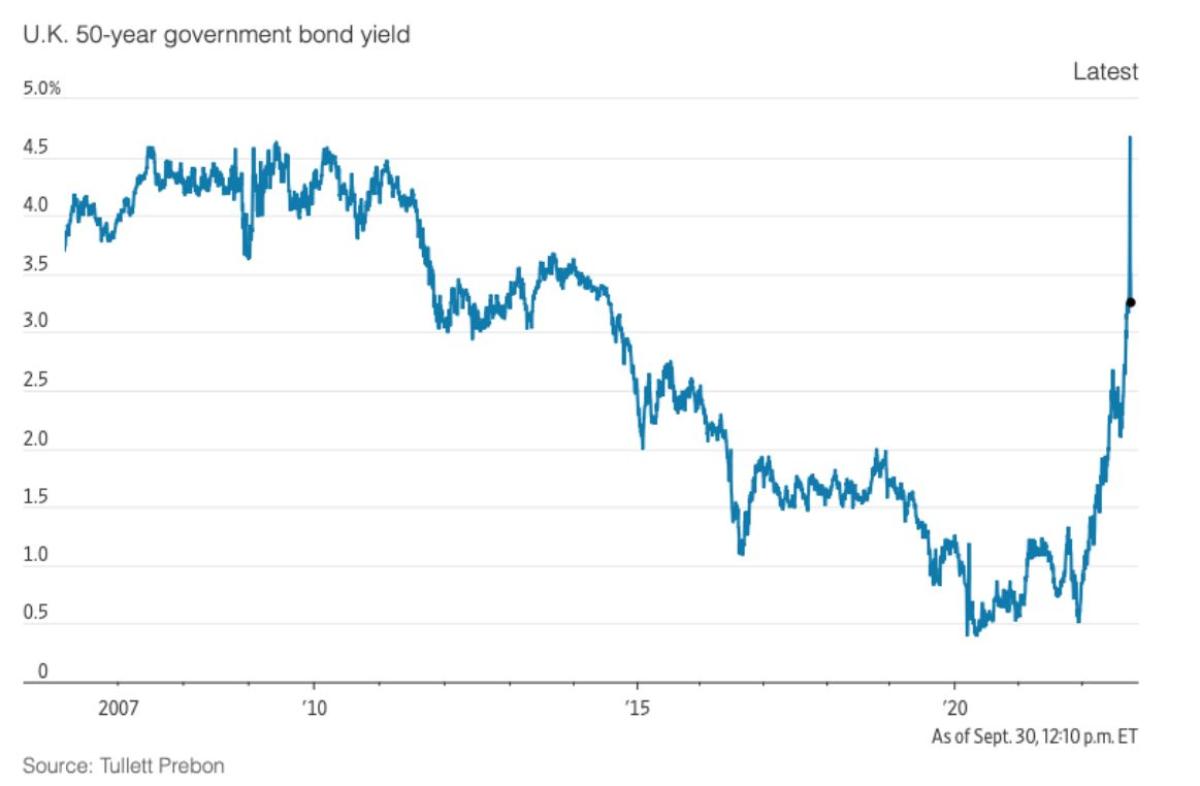

In the U.K. things have taken a turn toward the leverage-liquidity cycle usually reserved for hedge funds. And have done so in a way that is missed by risk systems that simply count marbles — that cannot grapple with the nonlinear dynamics arising from leverage and liquidity that got things there.

I can’t help but comment on the irony of having the safest and most prudent of institutions not only become embodied in a crisis, but be the fuse that starts it going. And with this happening because the pensions were trying to reduce risk. The wonder of financial engineering is that it can turn just about anything to be riskier than people think possible. I’m sure no one at the pensions was saying, “Let’s take a flier, lever up, and see what we can do.” Financial engineering is the only field of engineering where in proper application it tends to make things riskier.

How did they do it here?

My mantra for the sort of risk we see in the UK pensions, what I call material risk, is “leverage, liquidity, and concentration”.

Source: Tullett Prebon via the Wall Street Journal.

At Fabric, we model risk in a way to account explicitly for leverage and concentration, and through those two, the possible illiquidity that might arise in the event of forced liquidation. (You can’t assess that sort of illiquidity by looking at day-to-day trading; it is like trying to assess the adequacy of egress in the event of fire by seeing how well things work on typical days.) I do this using agent-based models, which are designed to deal with the non-linear dynamics that occur when we see events like have transpired over the past week with the Gilts.

We need to use these sorts of methods to understand material risk and crisis risk. I go through how the current approaches wedded to standard economics fail to account to this type of risk and how new methods overcome these limitations in The End of Theory, (Princeton University Press, 2017).

The basic theme of the book is that the mechanistic underpinnings of neoclassical economics, which stretch back over 150 years, create limitations on dealing with the dynamics of financial crises. You can’t work through market dislocations if you make the assumptions necessary to put things down as a neat set of equations. And economics and finance likes equations. The blind spots that result, which I put under the name of the four horsemen of the eco apocalypse, are: Emergent phenomena, ergodic processes, computational irreducibility, and radical uncertainty. To overcome these issues we need a simulation approach that allows for dynamic interactions. My solution is with agent-based models.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Rick Bookstaber has held chief risk officer roles at major institutions, most recently the pension and endowment of the University of California. He holds a Ph.D. from MIT.

Fabric distills today’s market dynamics into intuitive and actionable risk narratives, allowing the advisor and client to act with a shared understanding.