By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

We borrow the All-Weather asset allocation framework developed by Bridgewater to show that Private Debt can serve as a core portfolio holding because of its risk-adjusted performance across market environments.1

All Weather is intended to capture real returns available from traditional asset classes but weight them in a way – including leverage – that increases return over traditional stock/bond asset mixes for the same level of risk. While the concepts underlying All Weather were not new, Bridgewater successfully commercialized All Weather and today it is a part of many institutional portfolios and, in a few instances, replaces traditional asset allocation all-together.

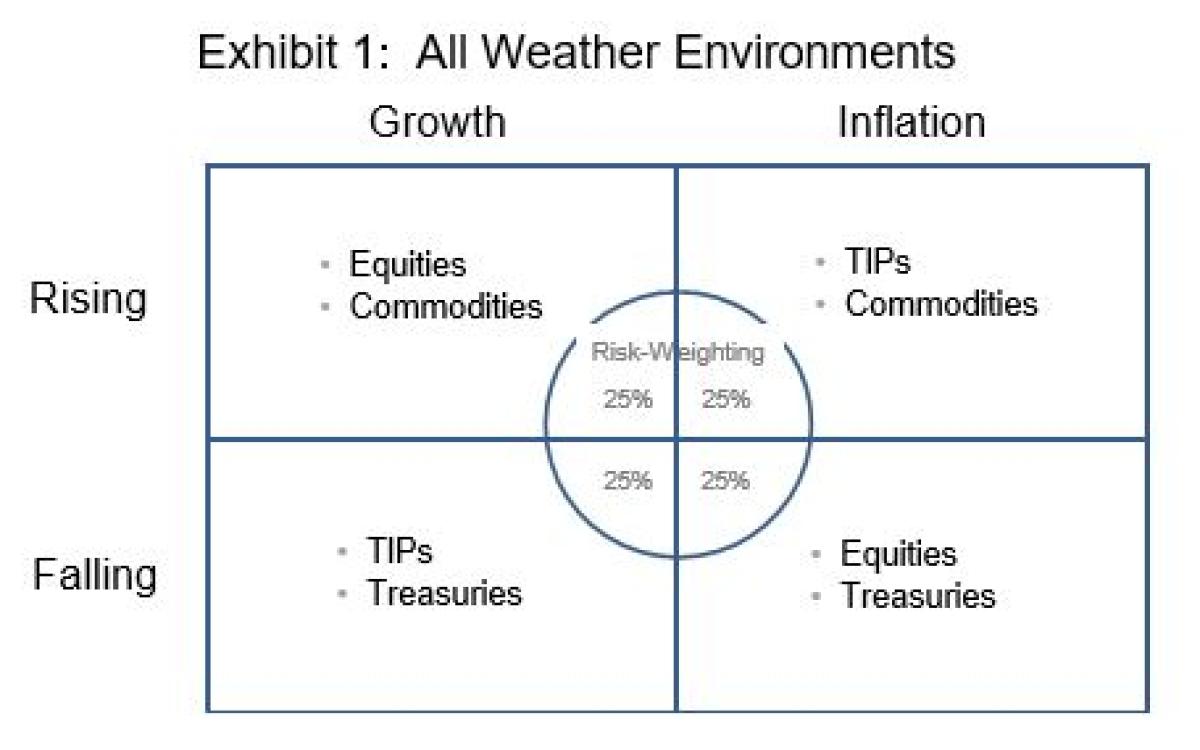

In explaining All Weather, Bridgewater created a useful heuristic, copied in Exhibit 1, that gave investors a more intuitive understanding of the covariances and weighting scheme that underly the strategy.

They posit four economic environments and distinguish which asset classes should perform well in each. Presuming equal probability across environments and equal return-to-risk ratios for each environment portfolio, then the optimal allocation is an equal 25% risk weighting across the four portfolios. Leverage is commonly associated with the All Weather and is generally applied to Treasury and TIPs allocations to increase their risk to levels equivalent to Equities and Commodities.

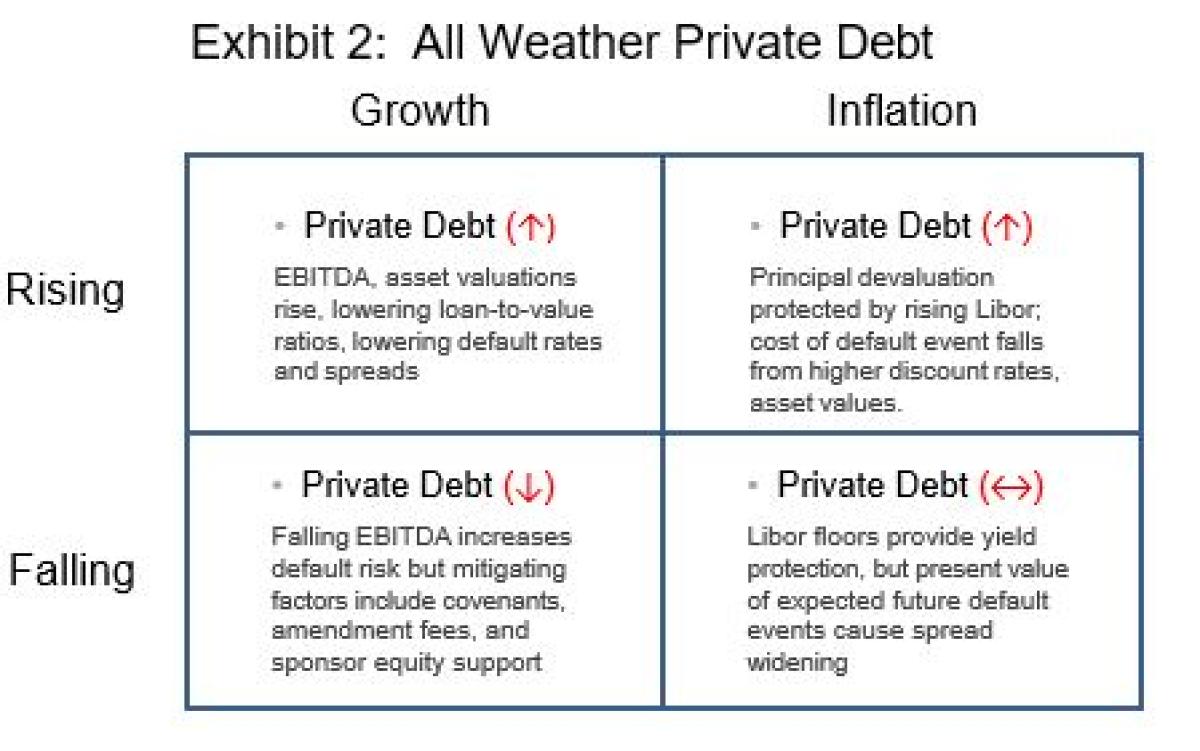

Private Debt strategies were largely unavailable to investors in 1996 when Bridgewater first fashioned their All-Weather asset allocation strategy. Exhibit 2 maps the expected performance for Private Debt for each All-Weather environment.

Private Debt should perform best in Rising Growth. Improving EBITDA, spread compression, and fewer defaults are most apparent, but so also is the protection Private Debt provides from increasing (real) interest rates by way of its

floating Libor reference rate. Rising Growth is also characterized by higher M&A activity which can bring additional prepayment fees and reinvestment opportunities to Private Debt.

Private Debt should also perform well in Rising Inflation when stocks and bonds would likely both suffer negative returns from higher nominal interest rates. Private Debt would benefit from a rising Libor reference rate and perhaps more security underlying loans, as EBITDA and asset values inflate from inflation.

A Falling Inflation environment may have a mixed impact on Private Debt. Private Debt yields might initially decline with falling interest rates, but the presence of “Libor floors” in most middle market loans might partially or fully protect existing yields. In the current environment, Libor floors have become very valuable. On the other hand, a decline in interest rates during Falling Inflation can increase the expected cost of future defaults by increasing their present value. Strong underwriting by lenders is a mitigating factor.

The COVID crisis represented a Falling Growth environment with a first-order negative impact on Private Debt from falling company EBITDA. However, as we have also seen, middle-market lenders have several built-in protections that limit adverse effects. These include (1) loan covenants that force borrowers to almost immediately negotiate with lenders to preserve loan value, (2) additional fees to lenders in exchange for the granting of loan amendments, and (3) additional cash equity support from sponsor-backed borrowers. There is little doubt that Private Debt and Equities are correlated in the Falling Growth environment, but they are different in that Equities have shown dramatic drops in value while Private Debt, due to attendant protections, have experienced only single digit declines.

Private Debt has performed at or above its long-term expectation in three of the four All Weather environments and in the fourth Falling Growth environment, any decline in value is likely to be muted. Most important, we have shown elsewhere that Private Debt returns exhibit low volatility and its inclusion in a diversified portfolio does not depend upon low and stable cross-correlations that form the basis of All Weather portfolio construction.2

Footnotes:

1This paper is not meant to be an endorsement of the All Weather (i.e., risk parity) portfolio approach. Separately, see Cliffwater Research – Risk Parity, January 2018, for a discussion of All Weather as an alternative to more traditional asset allocation.

2See Private Debt: Opportunities in Corporate Direct Lending, Stephen L. Nesbitt (Wiley Finance, 2019)

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Steve Nesbitt is the Chief Executive Officer and Chief Investment Officer of Cliffwater, and is primarily responsible for the day-to-day management of Cliffwater Corporate Lending Fund (CCLFX) and the Cliffwater Enhanced Lending Fund (CELFX), an SEC-registered credit interval fund focused on the US corporate middle market.

Steve is recognized for a broad range of investment research. His papers have appeared in the Financial Analysts Journal, The Journal of Portfolio Management, The Journal of Applied Corporate Finance, and The Journal of Alternative Investments. His private debt research led to the creation of the Cliffwater BDC Index, measuring historical BDC performance, and the Cliffwater Direct Lending Index, measuring historical performance for direct middle market loans. Steve authored the book, Private Debt: Opportunities in Corporate Direct Lending, Wiley Finance (2019) which provides the analytical and empirical underpinnings of the private debt market.

Stephen L. Nesbitt snesbitt@cliffwater.com

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.