By Michael A. Ervolini , Distinguished Fellow, FactSet Research Systems, Inc., and Matthew Gadsden, Senior Consultant & Head of Global Equities Research, JANA Investment Advisors.

Active Share and Portfolio Concentration - Metrics Not Prescriptions: Why merely increasing these measures is no formula for success.

PREFACE

High active share and greater portfolio concentration are hot topics within active equity management. Together they constitute what is commonly referred to as “high conviction” investing. It is generally accepted that all other things being equal both higher active share and greater portfolio concentration are not merely desirable, they are essential for delivering benchmark beating results. Belief in this duo is such that increasing both is commonly suggested as a precondition for success.

Numerous academic papers describe the positive relationship between high conviction and generating excess returns or what is commonly referred to as alpha. The research also argues that the presence of high conviction is not just correlated with alpha but is in fact predictive of future outperformance. Integrating these research findings together with their own internal needs, asset owners and third-party asset allocators (e g multifamily offices and outsourced chief investment officers) together referred to herein as asset owners/allocators increasingly are challenging what they perceive as excessive diversification within active equity portfolios and routinely pushing for higher conviction. For their part, many managers now promote high conviction as a key component of their portfolio management/construction regimes and presumably likelihood of delivering strong results. And while it is a fact that high conviction is associated with a number of successful equity funds it is by no means universally beneficial. To the contrary, simply increasing the active weight of a few positions and/or reducing the number of positions held can and does lead to lower performance with startling regularity. How can this be? The answer lies not in intent but in method or more precisely how higher conviction is implemented.

This paper begins with a brief review of the struggles plaguing active management. It then considers the origins and usefulness of the high conviction movement, describing its shortcomings as well as common reasons for poor implementation. The paper then presents five case studies of actual portfolios engaged in high conviction with mixed results. New metrics for quantifying skill and investment process which substantially enhance the ability to identify outperforming managers are then described. Finally, the paper concludes with a clear message to asset management companies and their clients that adoption of the revised best practices as outlined is essential to both the effective allocation of capital as well as continuation of a vibrant active management industry.

INTRODUCTION

Active equity management has struggled for the better part of two decades. Its problems stem from prolonged industry underperformance coupled with the growing acceptance of passive equity products. The results have included steady outflows from active management, massive downward pressure on active management fees and unprecedented levels of industry consolidation. Despite a somewhat banner year in 2020 with 43 of U S active equity funds exceeding their benchmarks (with similar results globally) investor perception of the industry overall remains cautionary 1

Not surprisingly, active funds continue to lose ground to passive funds in the battle for assets under management. According to a recent Morningstar report on 2020: “U S equity funds in particular saw 241 billion worth of outflows, which is more than four times the previous record of 58 billion in 2015. Consequently, active equity funds finished their seventh straight year of net outflows. Equity ETFs, on the other hand, saw inflows just north of 300 billion.2 Passive products now account for approximately 50 of professionally managed equities in North America and are rapidly approaching this level in Europe and Asia.

There remains significant demand for active equity management amongst pension schemes, endowments, sovereign wealth funds, and individual investors seeking alpha. The difficulty in identifying managers likely to outperform going forward, however, threatens to erode what remains of investor appetite for active asset management. Traditional metrics such as relative return, upside/downside capture, information ratio, tracking error, and multi factor alpha have proven to be of little to no help in this regard. New means for gauging manager skill have long been sought, leading to the study of high conviction investing.

THE ALLURE OF HIGH CONVICTION

Research over the past fifteen years has attempted to improve manager selection with the advancement of active share and greater portfolio concentration. While combined in achieving high conviction, these two portfolio management tools generally have been studied separately.

ACTIVE SHARE

In March of 2009 Martijn Cremers and Antti Petajisto shook up the active investment industry with the then novel idea of active share. Cremers and Petajisto defined active share as one half of the sum of the absolute values of the differences in weight between all positions held and their benchmark weights. The implication being the more that position weights differ from their benchmark weights the higher the portfolio active share and vice versa. Their research indicated that active share was positively correlated with fund outperformance historically and they went on to argue that it can be used to assist in capital allocation. In the words of the authors: “Active Share predicts fund performance: funds with the highest Active Share significantly outperform their benchmarks, both before and after expenses, and they exhibit strong performance persistence.3 Other researchers soon confirmed these findings and before long active share was among the mainstay metrics of manager/portfolio assessment.

What then beset active share is that demonstrated correlation morphed into widespread acceptance of a causal relationship the notion emerged that simply increasing active share would lead to excess returns. Soon managers began promoting their high active share as evidence that they were top performers and capital owners/allocators started including active share on their check lists. All was well with the world except for one thing: active share is no guarantee of future strong performance or identifying a skilled manager. In the excitement generated from the initial research findings active share was being used inappropriately. It’s not that high active share points to successful managers. Rather, it is those very strong managers with specific skills and processes who are able to implement high active share successfully and generate excess returns regularly. Cremers himself embraced this conclusion in a later paper when he observed: “It is only for managers with strong individual stock picking skills that a high Active Share may be beneficial.4 In other words, high active share is likely to magnify outperformance for skilled managers, but also magnify underperformance for unskilled managers.

HIGH CONCENTRATION

An important early contribution to the discussion regarding high concentration is found in “Best Ideas” by Miguel Anton, Randolph B Cohen, and Christopher Polk Anton et al compared the performance of a fund’s largest holding(s) to that of its remaining holdings. They observed: “We find that best ideas not only generate statistically, and economically significant risk adjusted returns over time, but they also systematically outperform the rest of the positions in managers’ portfolios. Their paper then implies a predictive quality regarding best ideas: “The level of outperformance varies depending on the specification, but for our primary tests falls in the range of 2.8 to 4.5 percent per year. This abnormal performance appears permanent, showing no evidence of subsequent reversal, even several years later.5

Anton et al were enamored by what they perceived as a new means of identifying manager skill. They also chastised industry practices for overall weak active returns. They state: “The poor overall performance of mutual fund managers in the past is not due to a lack of stock picking ability, but rather to institutional factors that encourage them to overdiversify, i. e. pick stocks beyond their best alpha generating ideas. This assessment appears to have led to their conclusion: “We argue that investors would benefit if managers held more concentrated portfolios. Logical as this recommendation appears, it ignores the complexities associated with reducing position count. Manager skills, investment processes and professional judgment are developed over many years within the context of specific strategies and highly idiosyncratic portfolio construction processes.

Among the practical considerations not addressed by Anton et al are the challenges faced by managers in applying their years of hard-earned know-how within a very different portfolio context. And while over diversification is often detrimental to portfolio performance there is an equal argument to be made that some level of diversification across active positions is desirable from a risk management perspective. At some point the benefits from greater concentration fall away as absolute and relative risks become untenable for either manager or client. Moreover, it is JANA’s belief that portfolio construction is a paramount consideration in assessing managers and we find nothing inherently wrong with diversification within individual portfolios.

“The shift to higher conviction can actually push a once alpha-generating portfolio into negative relative returns.”

UPS AND DOWNS OF HIGHER CONVICTION

Higher conviction clearly offers value to those able to effectively harness this investment approach - benefiting from the allocation of greater capital to a smaller number of outperforming positions. Yet the transition from low or modest conviction to higher conviction is not without risks. Extensive investigation by the authors makes clear this transition does not reliably improve even benchmark-beating portfolios nor does it dependably reverse underperformance. Most disturbing is that the shift to higher conviction can actually push a once-alpha-generating portfolio into negative relative returns. Disappointing outcomes from transitioning to higher conviction are generally due to poor implementation. Poor calibration of skills and investment processes is the most common culprit. Managers that alter their position count and/or active share absent a rigorous understanding of precisely how they generate alpha are doing so based on hunches. And such gambles are more apt to result in disappointing outcomes rather than the desired alpha. Here are four reasons why reaching for higher active share and/or higher concentration can backfire:

ADVERSE SELECTION

Consider a portfolio of 50 positions with 60 turnover wherein the manager will make 30 or so new buys each year. With a success ratio of ½ (winners/total buys) a skilled manager can outperform her/his benchmark regularly. Now if under a high conviction regime, the manager is selecting only 8 - 12 new positions each year, it is possible that the proportion of winning names can go down (so that the success ratio drops to 1/3. The onset of adverse selection can stem from a variety of forces with two common sources being a) a poor understanding of one’s buy process, thereby allowing the manager to unintentionally choose a higher proportion of weaker stocks than previously, and b) a heightened sense of angst that negatively impacts their decision making, possibly due to the belief (conscious or unconscious) that their career tenure is intrinsically tied to the successful morphing into a high conviction investor.

SLOW POSITION BUILD UP

Bringing relatively young, high-performing positions to full active weight can be a challenge even for managers with years of successfully managing high-conviction portfolios. For managers new to high conviction, the difficulties are amplified. Shifting from 75 basis points of full active weight to 225 basis points of full active weight requires overcoming well entrenched habits and processes. If the manager wades in slowly to achieving the new higher full weight rather than getting there in a timely fashion, the portfolio will lose out on a good bit of alpha due to strong names being undersized. While less problematic in a highly diversified portfolio, such foot-dragging can be disastrous for a high-conviction portfolio.

UNPRODUCTIVE INTERIM TRADING

Faced with fewer stocks to buy and sell with a high-conviction portfolio some managers use their newfound extra time to trade around position size (i.e. lots of adds and trims). This type of interim trading is one of the least calibrated or understood of investment skills. Studies by Cabot across hundreds of actively managed equity portfolios show that few portfolios gain from such activity. Examined in aggregate over multiple years, the data show that adding and trimming of positions mostly results in a negative impact on performance while a smaller fraction simply nets out to a zero benefit.

OVERSTAYING POSITIONS

Owning fewer active positions, as is the case in a high-concentration portfolio, generally involves having strong expectations or hope for each such holding (or why bother?). Behavioral research suggests that this type of concentration of capital or bets can ignite what is termed the endowment effect. Simply put, endowment involves overvaluing stocks in one’s possession for emotional rather than fundamental reasons. Consequently, they are frequently held much too long, well past their alpha-generating ability. Cabot’s work with active managers indicates that roughly one out of three portfolios reflect the endowment effect. This behavior typically costs over 100 basis points annually and its impact can be much worse in a high-concentration portfolio.

ACTUAL OBSERVATIONS

Five case studies reflecting Cabot’s analysis of actual portfolios involving high conviction are presented below

CASE STUDY 1: HIGHER CONVICTION LEADS TO LOWER RESULTS

A multi cap portfolio outperformed five out of six years between 2010 and 2015. During this time active share was 40 and the portfolio typically held 40 names. Beginning in 2016 the portfolio decreased the name count to 30 positions (25% decline) and increased active share to 60 (1.5x). The portfolio subsequently underperformed dramatically in four of the next five years. A substantial cause of this underperformance was a significant decline in the manager’s buying skill.

CASE STUDY 2: GREATER CONVICTION DISRUPTS WINNING STREAK

A mid cap portfolio had outperformed every year from 2011 through 2017. The manager then reduced the number of names held from 50 to 30 (40% drop) and increased active share from 35 up to 50 (1.4 x). The portfolio went on to underperform in 2018 and 2020. While the long-term impacts of higher conviction for this portfolio remains to be seen, the initial impact has been to destabilize the manager’s skills and introduce volatility into what had been consistently positive results.

CASE STUDY 3: MISSTEP THEN A REVERSAL

A large cap portfolio shifted to greater conviction only to reverse course after disappointing results. The portfolio delivered steady results for seven years (2006-2012) during which time the position count was 45 and active share was 80. The portfolio then decreased position count to 38 and increased active share to 90. The portfolio underperformed for the next three years. The portfolio subsequently reverted to its more historical position count and active share quickly resuming its delivery of outperformance. During this sequence the manager’s buying and selling skills initially declined and then bounced back post the higher conviction interlude.

CASE STUDY 4: CHANGING DELIBERATELY

An emerging markets portfolio steadily outperformed while slowly decreasing its position count, lowering its active share, and cutting its turnover in half over many years. Possessing strong skills and processes at the start this manager was able to slowly and deliberately refine portfolio construction/management thereby achieving greater conviction whilst maintaining very strong results. Possessing deep self-awareness and shifting toward greater conviction in a deliberate and measured fashion can help ensure, as in this example, that the changes implemented are for the best.

CASE STUDY 5: OUTSTANDING AMONG ITS PEERS

A U S large cap growth portfolio has consistently outperformed for over 20 years. Throughout this time period the fund has held 24 or fewer positions, maintained high active share and name turnover of roughly 20. Managing such a high-concentration and low-turnover portfolio requires tremendous skill, which this manager possesses. The manager is able to buy strong stocks that generate excess returns for years, reflected in the low turnover. The positions are sized and sold effectively, enabling the alpha generated from strong buying to remain in the fund and benefit its investors. Iconic of what comes to mind for a successful high conviction portfolio, the results would not be attained but for strong buying and a consistent buy process.

These examples shed light on both the potential rewards and implementation challenges of high-conviction portfolios. Lowering position count and/or increasing active share works for some managers and not for others. The reason, as observed across scores of portfolios analyzed by Cabot, is that high conviction is best suited for highly skilled and disciplined managers those able to regularly identify stocks that outperform and who possess and use a consistent buy process working with rigorously developed unambiguous feedback. Absent any of these qualities the shift to higher conviction is fraught with uncertainty more likely to lower future results as to increase them.

BREAKTHROUGH METRICS

There clearly are managers who have found their way successfully to high conviction investing. Others that are trying to shift to higher conviction are learning that the path to stronger results is not straightforward nor without peril. The path can be made both clearer and less risky when such transitions are supported with rigorous feedback concerning skills and investment process. Two such advanced metrics involving the buy skill and the buy process are used to demonstrate the advantages of applying best practices to manager/fund assessment.

PERSISTENT SKILL

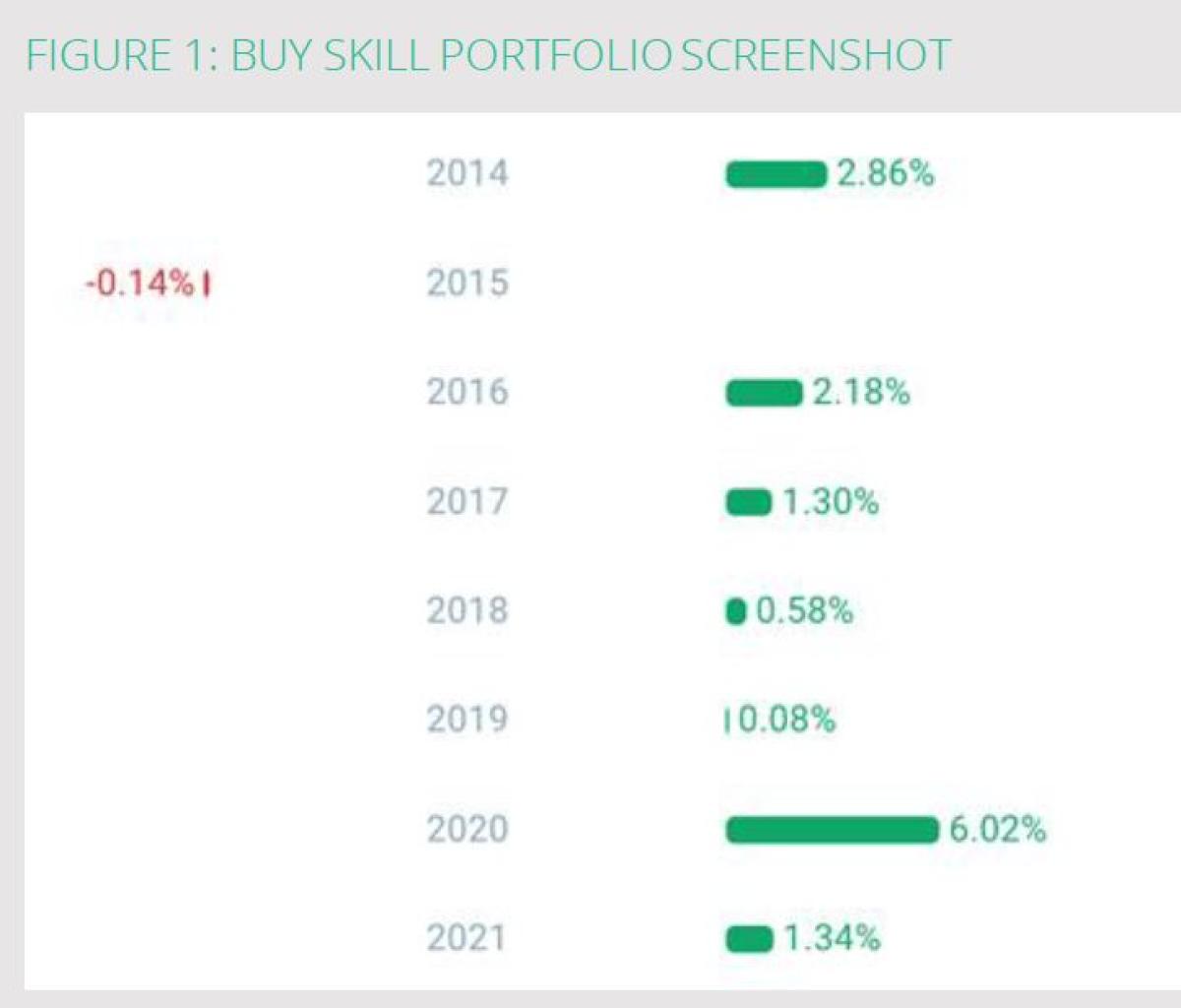

Figure 1 shows the buy skill for a highly talented manager. The green bars indicate years in which new buys went on to become winners and red bars indicate years when new buys underperformed. This manager clearly delivers consistently strong buying with a positive result in seven of eight years. A strong buy skill like this is commonly the

cornerstone of successful high-conviction managers.6

ASSURING REPEATABILITY

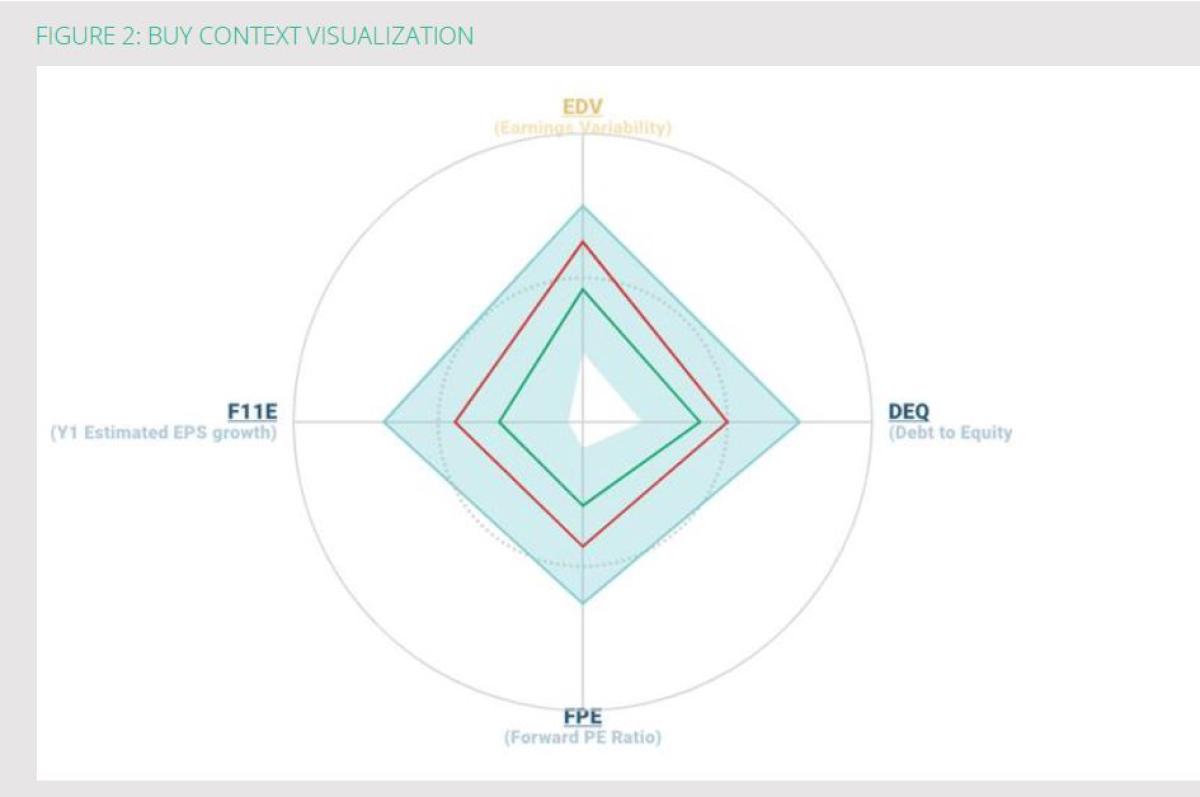

The second quality demonstrated by successful high-conviction managers is a process that leads to repeatable stock selection. Figure 2 depicts a visualization of a buy process. The four axes reflect varying stock attributes or fundamental factors which best describe the portfolio’s buy process (developed with the help of machine learning) The green shaded areas further indicate the level of the attribute associated with the portfolio’s winning buys. The red shaded area denotes the level of each attribute reflected in the losing buys. Note that specifically for this manager, stocks with relatively lower levels of each attribute at time of purchase generally go on to be winners. 7 Examining this diagram for several time periods illuminates exactly how consistent the buy process is over time.

Cabot and JANA have observed that top-performing portfolios invariably reflect both a consistently strong buy skill and a process that leads to purchasing stocks of similar characteristics over time. These qualities enable the manager to deliver outperformance more often than not and, when calibrated rigorously, they form the building blocks upon which additional skill and process refinement can be built.

UPGRADING BEST PRACTICES FOR ASSET OWNERS / ALLOCATORS

Identifying equity managers likely to outperform going forward is no mean feat. Sorting out which managers are more likely to generate ongoing alpha is sufficiently trying that many industry experts advocate that large capital sources simply revert to capturing the beta of public equities as inexpensively as possible (i e passively) while increasingly looking for alpha elsewhere. As compelling as this idea is on the surface it has the effect of throwing out the baby with the bathwater JANA and Cabot have found that active equity managers can play a highly useful role within overall asset allocation plans. Our work together has focused on pension schemes, but the insights are applicable to all investors.

Pension schemes, sovereign wealth funds, endowments and individuals want and need to generate excess returns over time. Abandoning traditional active equity management is far from a necessary condition for pursuing alpha. Best practices now require going beyond what the portfolio did in terms of results and getting a clear understanding of how those results were generated. Doing so supports even more confident allocations to active equity.

The types of questions that must now be answered include:

Which skills drove performance?

How consistently were investment processes used?

How repeatable are recent results, based on quantified skills and processes?

Is the manager clear about her/his strengths and shortcomings, at a rigorous level?

Are changes to portfolio construction/management really helping?

What is the manager doing today to be a better investor tomorrow, and the days after?

Rigorously developed answers to questions like these elevates the asset owner/allocator manager relationship to new heights. Both parties can share a common data-driven understanding of not only how well the portfolio is performing but exactly how (on average) the manager’s skills, processes, and professional judgment are impacting the results. This level of insight provides more than greater transparency, it substantially reduces the information asymmetry that frequently exists between managers and their clients. The result is a more even footing with regard to not just the past but also the likelihood of the portfolio delivering alpha going forward. Additionally, this shared deeper knowledge enables asset owners/allocators to ride out difficult periods a manager invariably will encounter doing so with a well-reasoned assessment of the manager and the likelihood for the portfolio results to rebound in a timely manner.

This is the new world of active equity management. One where all participants have a deeper understanding of the unique value add of each portfolio manager. This enhanced due diligence allows asset owners/allocators and managers to work together with greater effectiveness, with each relying more on rigorous facts and less on inferences or intentions. JANA is beginning to integrate these new analytics into aspects of its business. These analytics are, to be sure, complementary to the exacting efforts JANA is known for regarding portfolio analysis, process reviews and evaluating the human side of equity managers. Equally important is that the new metrics described also enable managers to attain maximum self-awareness and use this new knowledge to improve. Put simply, what are best practices for asset owners/allocators are also best practices for sustaining and even growing active equity management overall.

CONCLUSION

Shifting to higher conviction works when the manager possesses a deep, fact-based understanding of her strengths and shortcomings and uses this knowledge to guide the path…” The active equity industry is in the throes of a wrenching realignment. Lower fees, continued mergers and acquisitions, and the struggle to maintain assets under management are just a few signs. Active managers are, of course, taking many steps to strengthen and reposition their businesses. In large part these efforts are not directly addressing the two most pressing issues facing the active equity management industry as a whole.

1. The need for active equity managers to become intensely self-aware about their skills and investment processes, and to use this more rigorous knowledge to regularly improve and

2. Providing asset owners/allocators with better feedback about manager skills and investment processes, so as to heighten the confidence they have in their allocations to active equity.

High conviction investing involving both concentrated portfolios and high active share have been studied as exemplars of successful modern equity management. And while it is frequently the case that high conviction portfolios match or exceed their benchmarks, there is little evidence that shifting to higher conviction in and of itself benefits portfolio performance nor is high conviction the only approach to achieving benchmark-beating returns regularly. To the contrary, there are many portfolios whose performance has suffered as a result of adopting a high-conviction approach and many whose results remain strong using reasonable diversification. This is not to suggest that high conviction is without merit. The truth is that shifting to higher conviction works when the manager possesses a deep, fact-based understanding of his/her strengths and shortcomings and uses this knowledge to guide the path toward holding fewer names and/or building the active weight of positions.

JANA is using metrics like buy skill and buy process currently to strengthen its equity manager investment due diligence programs. These metrics complement JANA’s well-honed processes, expanding their understanding of the strengths and shortcomings of any equity manager. They allow JANA and the manager to focus more on facts and less on intent or soft explanations. They provide a totally new level of transparency that both supports the manager’s self-awareness and ability to improve while also placing JANA on a more equal footing with the experts that they recommend to their clients for investing.

Advancements within the active management arena invariably begin with a small group of industry participants whose thought leadership makes common practice what once was a novel idea. Our industry is once again poised at such a moment. This one involves the use of rigorous feedback so that all can see not just who surpassed their benchmark last month, last year, or longer but also who is likely to do it again and again. Answering this basic question is now part of equity management best practices.

Endnotes:

1. “SPIVA U S Scorecard 2020 Standard Poor’s, March 11, 2021

2. Jeff Benjamin, “Mutual fund assets continue to decline in 2020 Investment News online, January 21, 2021

3. Martijn Cremers and Antti Petajisto ,,"How Active is Your Fund Manager? A New Measure That Predicts Performance," the International Center for Finance at the Yale School of Management, March 2009

4. Martijn Cremers, “Active Share and the Three Pillars of Active Management Skill, Conviction and Opportunity”, Financial Analyst Journal, 20165. Miguel Anton, Randolph B Cohen, and Christopher Polk, “Best Ideas” Volume 4 Volume 21 of Working papers, Harvard Graduate School of Business Administration, first posted 23 Mar 2009 and last updated (March 2021 Available at SSRN https :://ssrn com

6.Michael A Ervolini,“Time to Buy”, available at www/cabotintech com/essays

7.Michael A Ervolini,“Managing Equity Portfolios: A Behavioral Approach to Improving Skills and Investment Processes”, MIT Press, 2014

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Authors:

Michael A. Ervolini, Distinguished Fellow, FactSet Research Systems, Inc. FactSet makes financial decisions work. It’s done through the delivery of highly curated information such as company fundamental data, ESG data, quantitative factors, regulatory compliance and much more combined with industry leading analytics and services. The Company supports decision-makers across all financial industries including banking, asset management, private equity, hedge funds, insurance companies, pension funds, investment advisory, sovereign wealth funds and endowments.

Mike is best known for his work involving the application of behavioral finance, psychology, and neuroscience to decision making under uncertainty. Mike has written extensively on the challenges of active management including his book: “Managing Equity Portfolios – A Behavioral Approach to Improving Skills and Investment Processes,” MIT Press.

Mike joined FactSet in June of 2021 when the Company purchased Cabot Investment Technology, Inc., of which Mike was Founder and CEO. Cabot is the leading developer and provider of behavioral analytics for active equity management. Prior to Cabot Mike was the Founder and CEO of Charter Research LLC, a fintech business that developed and marketed high performance analytic software for the commercial mortgage-backed securities (CMBS) industry. Charter was purchased by Standard & Poor’s, a McGraw-Hill company. Previously Mike worked for AEW Capital Management LLC of Boston and Latimer & Buck, Inc., a division of Legg Mason.

Mike brings to FactSet over 35 years of senior executive experience in finance, asset management, analytics, sales and marketing. In addition to furthering the integration of the Cabot technology across the FactSet platform Mike is spearheading the Company’s enhanced thought leadership efforts and guiding FactSet’s expansion within the so-called front office or C-suite.

Mike earned a BA in Economics from Rutgers University and a MS from the University of Pennsylvania.

Matthew Gadsden is the Head of JANA’s Global Equities Research Team, and responsible for capital markets and investment manager research across JANA’s client base.

In his dual role, Matt also consults to a range of super and non-super Implemented Consulting clients but also contributes to servicing one of JANA’s largest Traditional clients. Matthew holds a Bachelor of Business (Economics & Finance) from RMIT and a Master of Applied Finance from Macquarie University.