By Ros Bazany, Head of ESG and Impact at Antler, a global early-stage venture capital firm.

Key takeaways:

- Supporting founders at the earliest stage increases the probability of company and founder success

- Portfolio construction is a key risk management strategy where VCs must embrace diversification

- Those VCs who fail to expand on industry and geographic diversification will likely miss out on innovation, tech trends and thus return potential

I don’t know much about football, but having recently enrolled my eldest son into the Real Madrid kids club, I am learning more - particularly about Cristiano Ronaldo. Ronaldo was the team’s all-time top scorer in 2015-16 and, to my son at least, is one of the best players in the world. Ronaldo was scouted at 12, and he made his international debut at 16. With this new-found knowledge, I couldn’t help but make a comparison between VC and football.

Football scouts search all corners of the world to find exceptionally talented individuals. They look for skill, vision, mental strength, and character, which you could argue are similar to what VCs look for in entrepreneurs. In today’s world, VC scouts recognize that a sizable geographical footprint can be hugely beneficial to uncover talent globally. Just like football scouts, we see VCs supporting founders and aspiring entrepreneurs earlier in their journey, providing them access to a community, mentorship and, of course, capital.

Antler is a global asset manager that specializes in early-stage VC. We invest from Pre-Seed to Series C and have enabled over 15,000 founders to date, both through our pre-seed investment platform and our free online education platform Antler Academy. Supporting founders at the earliest stage isn’t just the right thing to do; it is the smart thing too. We learn from our interactions with founders at this earliest stage. It is widely known that 34% of startups close within their first two years. We can gather data on what leads to successful companies, founders, and teams early on. This understanding can significantly improve our probability of generating winners. In fact, my colleague Tyler Norwood, a Partner at Antler in the US, has written an essay on building a better pathway for founders, and he discusses Antler’s approach to increasing the probability of company and founder success.

Antler typically spends over 200 hours with teams before an initial investment decision. This should be seen as a risk management strategy. This allows time to assess and validate team relationships, business models, and create appropriate networks. It also has proven to mitigate both conscious and unconscious bias in our investment funnel.

Another risk management strategy, which is often less thought about in VC circles, is portfolio construction.

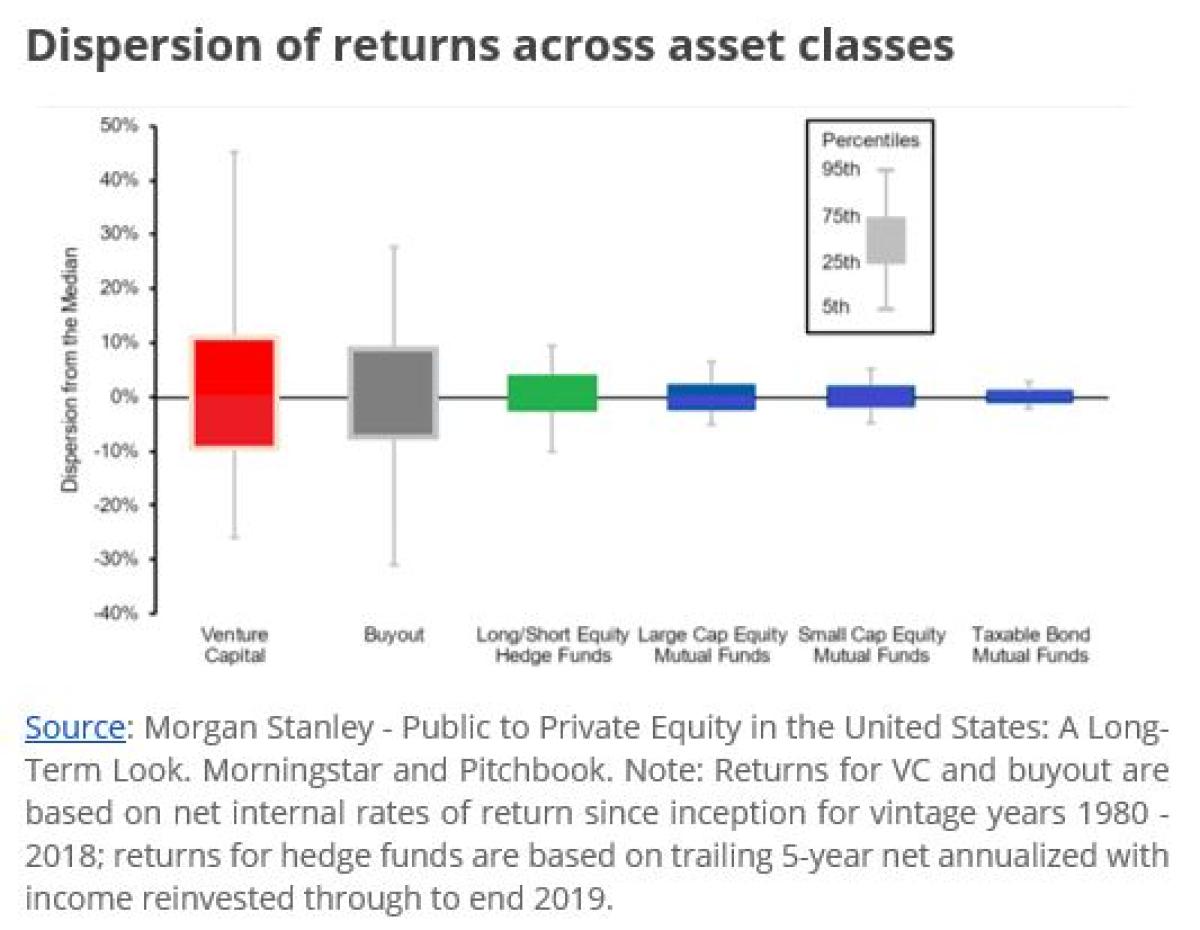

VC can be a challenging asset class to predict return, as illustrated in the dispersion chart below. One might suggest that manager selection is, therefore, of the utmost importance.

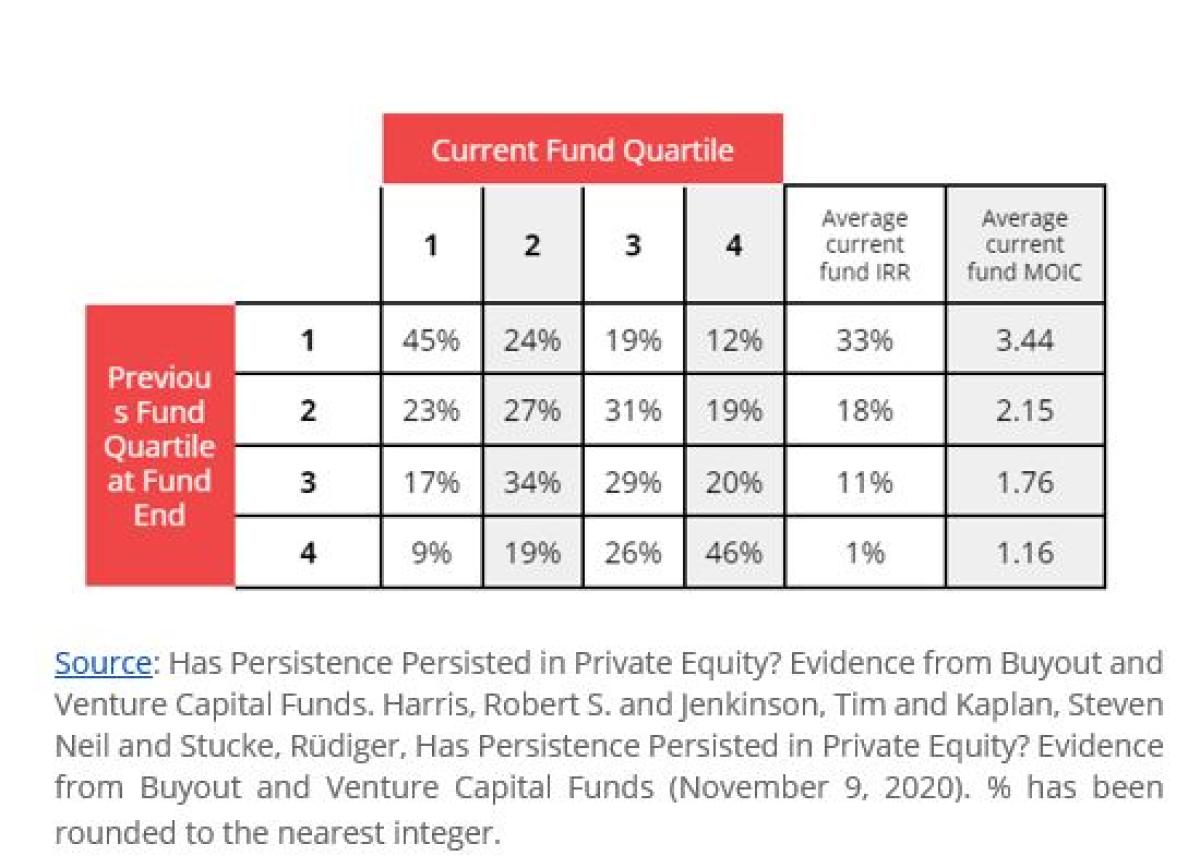

Research shows that the top quartile funds tend to deliver subsequent funds with similar return profiles. However, if I were a betting person, I would want a higher probability than 45% for repeatable top quartile returns across fund vintages. So, what can VCs do to improve this number?

The typical VC manager may invest in about 30 portfolio companies. Several articles published in the last few years provide evidence that this approach to portfolio construction is all wrong. An article in Institutional Investor concluded that “the golden rule for investors into the venture asset class must be - build a portfolio of 500 startups, with 100 companies being the absolute minimum”. Their model shows a larger portfolio of diversified companies significantly decreases return dispersion and increases average return. Antler funds will typically have over 100 diversified portfolio companies once fully invested.

The calculations and simulations validate this theory. The startup landscape today also supports this logic. The globalization of VCs is in full swing - emerging tech hubs have even shown some recent results of outperformance vs. the mature tech hubs such as San Francisco and Silicon Valley. Entrepreneurs can start their businesses anywhere in the world (and still scale globally) - it is cheaper and easier than ever before. Governments worldwide recognize the power of entrepreneurship and innovation to create GDP growth and job creation and are investing heavily in initiatives to attract startup talent to their cities. This set of complementary factors, coupled with Gen Z’s natural affinity to entrepreneurship, means we can expect more companies to be launched and no shortage of choice for VCs.

VCs who have robust due diligence processes and embrace diversification - not only by sector and geography but also founder profile - will increase their probability of finding not just great but the best founders.

So, the question is: why aren’t all VCs embracing diversification in portfolios? Here are three reasons we often hear from the industry and our response.

1. Our LPs do not want a diversified portfolio

If you go to any global asset manager’s website - be it BlackRock, Schroders, or Vanguard - they will have a discussion paper about the power of diversification in portfolio construction. This is across asset classes, within portfolios, and by manager and style. The largest institutions and asset allocators follow this lead in their portfolio construction. Why would their VC allocations be any different?

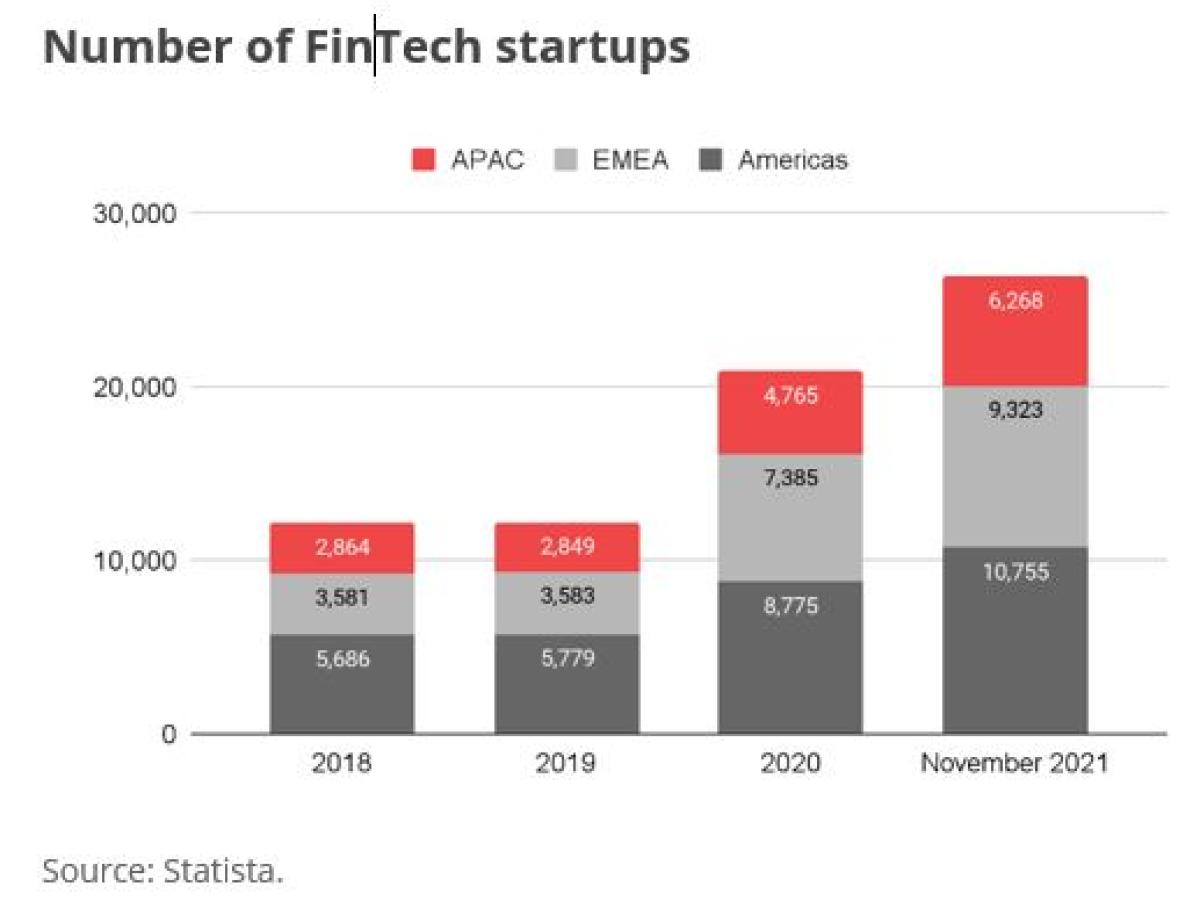

The MSCI World Index consists of 1,542 companies. Asset managers may select the top 10% as their high conviction stocks for a global equity fund, giving a portfolio of around 150 companies. The pond for VC managers is a much larger one to fish in. Two simple examples neatly illustrate this point. 1,436 startups were launched in India in 2021 alone, and currently, over 26,000 fintechs exist globally. One may even go so far as to say that VCs could even offer greater diversification opportunities than public markets, particularly given the concentration challenges we see across indices today.

Number of FinTech startups

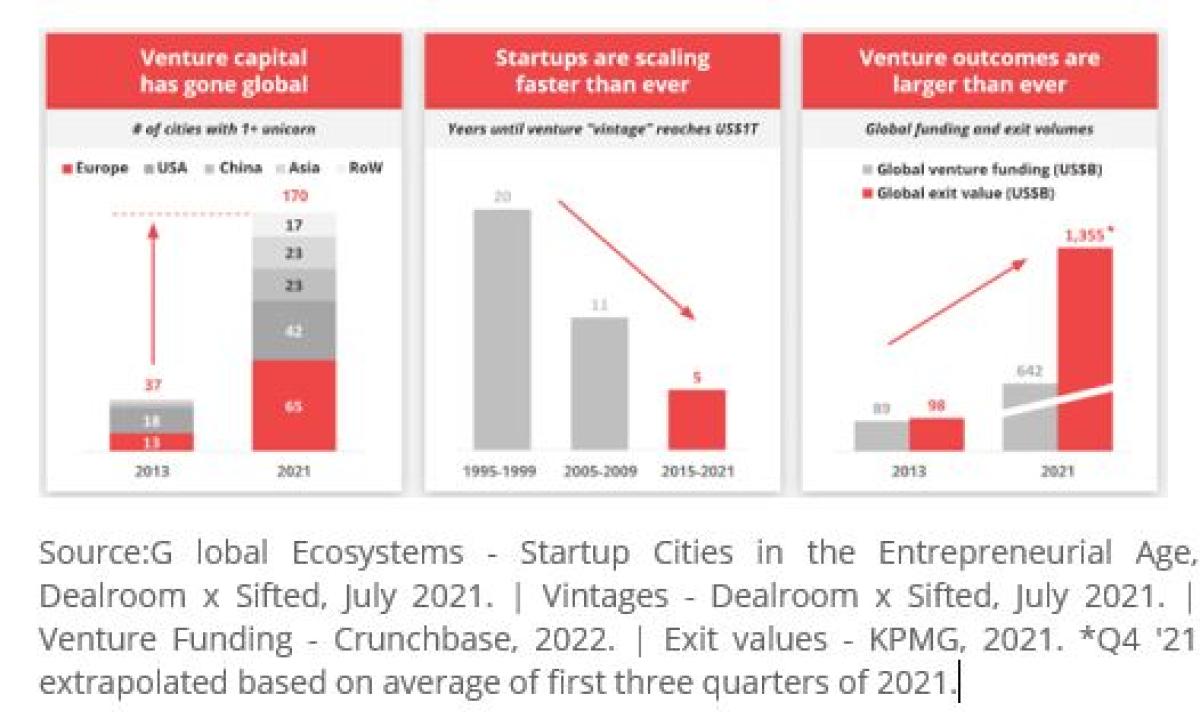

The VC industry is still considered a relatively new asset class for investors, but it is quickly being recognized as an untapped resource for asset allocators to offer both high return potential and low correlation to traditional public markets. An allocation to VC could prove advantageous as the general market environment points to a far more challenging ride ahead, with higher inflation risk, political tensions, and interest rates, and a more volatile time with retail investors and option traders driving valuations in all directions. We have seen asset allocators become perceptibly more comfortable with the liquidity differential between VC and public markets. This demand is corroborated by the record level of global VC investments last year - over US$620B in 2021, easily doubling the 2020 figure.

The pace of assets shifting into this asset class will continue to accelerate. A number of recent surveys have shown allocations expecting to go to more than 15% for institutional investors. VCs can learn from the large global asset managers about portfolio construction and the importance of diversification; they have been doing it a lot longer. There are, of course, big differences between VCs and these asset managers. One of which is resources. This leads us to the next pushback we hear from the industry.

2. It is too difficult operationally for VCs to provide a truly diversified portfolio

The trend of companies staying private for longer has existed for some years, as has the increasing startup acquisition rate of big tech. A dramatic shift, however, in the last two years has been the rise in new business applications. According to the Census Bureau's Business Formation Statistics, around 4.3 million business applications were filed in 2020 in the US, which is 51% higher than the 2010-2019 average.

Over the years, we have seen some regions naturally gravitate toward certain sectors, for example, the Nordics to energy, Canada to digital tech and AI, Central and Eastern Europe to enterprise software, Southeast Asia to fintech, and India to SaaS and Web3. This may be due to demographics, regulation, government support, or simply a country’s landscape and/or behaviors and culture. The point is that every city and tech hub can offer diversity within its ecosystem and among others. The key is developing the founders in the right way to understand the business challenges they are trying to address and how to commercialize them.

We certainly do not anticipate a lack of investment opportunities for VCs going forward. But those not fully embracing industry and geographic diversification will likely miss out on innovation, tech trends and thus return potential.

The challenge of resources can also be confronted by the use of data, strong communication, and operational efficiencies. Antler has launched in 21 cities around the world in 3 years, in both developing and developed countries, and we continue to expand. Over the last 18 months alone, we have launched in countries such as Brazil, Japan, Vietnam, France, Indonesia, and South Korea.

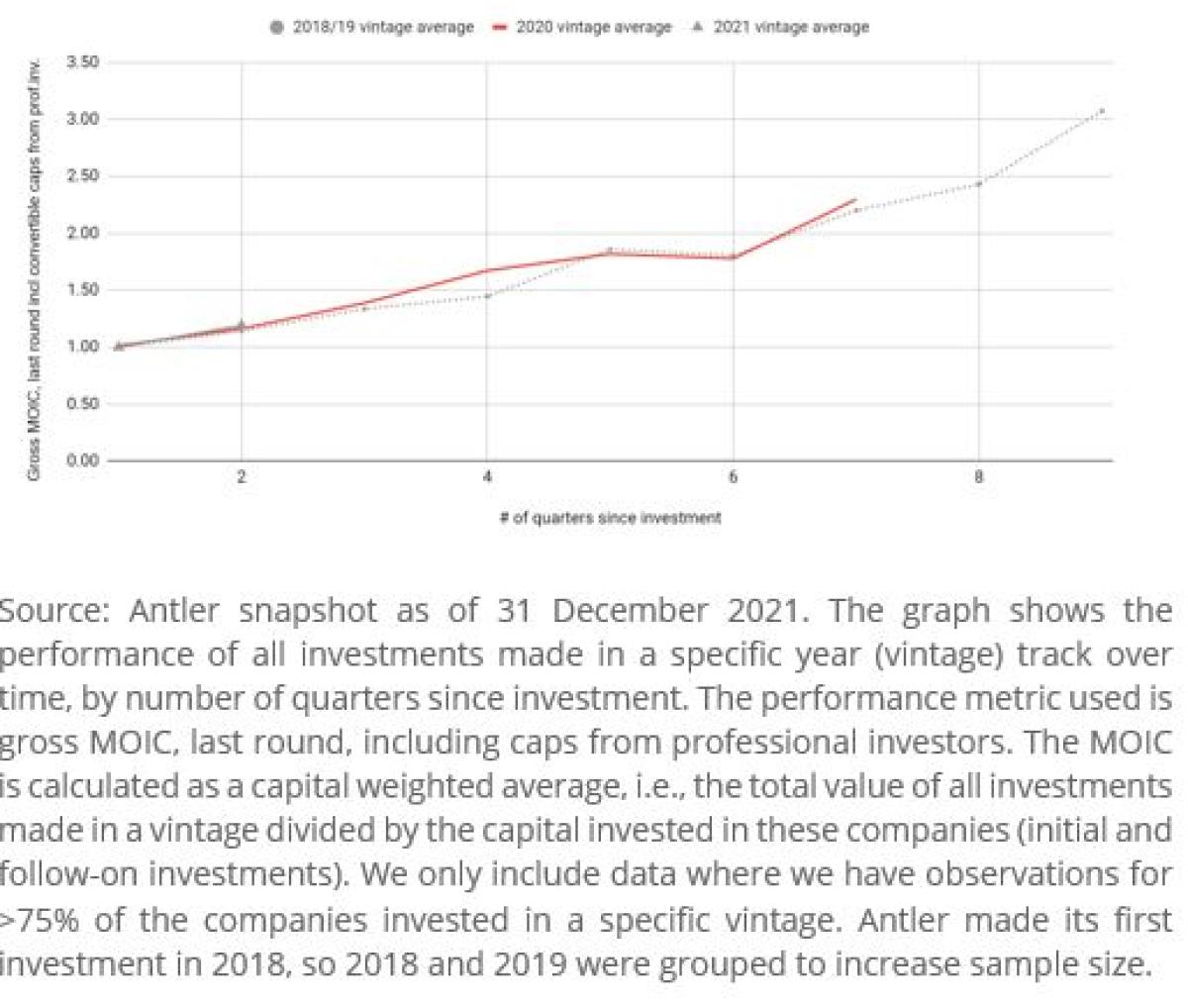

The chart below shows the performance of all investments made by Antler in a single year across our locations around the world. It reveals that the Antler model, so far, is proving to deliver consistent QoQ growth. With a 3+ year track record and over 400 investments to date, we believe our approach offers something entirely different from what the VC industry has seen before. Data forms the backbone of Antler’s ability to launch new locations in a repeatable, efficient, and nimble manner.

Antler quarterly performance evolution since initial investment (grouped by vintage years)

Antler has built a proprietary data platform that gathers data on founders and portfolio companies that is used as a tool for investment teams across locations to make more informed investment decisions. Founders also leverage this data platform for hiring, networking, collaboration, and cross-fertilization of products and services.

Antler has developed a sustainability health check to support founders and our investment teams to monitor and track key non-financial factors as a company matures. We want to use data to educate and empower our portfolio companies and set the right foundations for best practices from the start.

3. Founder level diversification is hard to represent

2021 saw the birth of over 890 unicorns (private companies valued at over US$1B). With this number reaching a record high, we would argue that it is now more important to understand where these unicorns are coming from rather than the total. This figure represents over 170 cities worldwide that have at least one unicorn. These cities will naturally have different founders with varying backgrounds, beliefs, nationalities, experiences, and gender.

For those VCs focused on specific geographies or industries, we can see how their founder set may represent a specific, and perhaps limited, profile. For those truly global managers with actual boots on the ground, I suspect the challenge is really that they lack the data to reflect the diversification of founders rather than the lack of founder diversification itself. The next question for the VC industry should be: if your founder base does not exhibit diversification, then what are they doing to better represent minority groups or support underserved communities?

Antler has no criteria for the initial founder application process - it is open to all. Antler has received over 100,000 applications from founders representing over 100 different countries. A grant is offered to founders where financial support could be beneficial. Antler’s funded founders represent 70+ different nationalities worldwide, and 33% of portfolio companies have at least one female founder. We continue to expand to different tech ecosystems, using a repeatable process that will enable communities all over the world to contribute to economic growth, job creation and solve the world’s greatest challenges.

Founder diversification is underpinned by bias mitigation in the investment process. Let’s ruminate on this and consider the inadequate level of VC funding to female entrepreneurs. The industry average for funded portfolio companies with at least one female co-founder remains just over 11%, according to Crunchbase. If we look at the female vs. male founders ratio throughout the Antler investment funnel (at application, cohort, and funding), it is consistent at 25%. This tells us that once founders are given the opportunity, receive the proper support and coaching over a substantial period, they can be successful, regardless of gender.

Football is a sport that can bring communities together; it can offer opportunities to individuals who have great talent but are just not sure how to channel or improve their skills; it is also a big moneymaker. The top 5 football clubs are worth over US$22B, and each of them is searching for their next big star. They scout for players at the earliest stage, develop them, give them financial support and guidance that they hope leads to a sustainable, strong, and successful player. Not everyone will reach the status of Cristiano Ronaldo, but give them the right tools, and they will certainly try. This is balancing risk and reward, just like using diversification as a risk management tool. VCs taking a similar approach to working with founders have the advantage that a turf toe won’t take their entrepreneurs out of the game.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Ros Bazany is Head of ESG and Impact at Antler, a global early-stage venture capital firm. Prior to this, she spent 14 years working in the finance industry, covering institutional and intermediary clients at the global asset manager Schroders and the hedge fund BlueCrest.