By Andreas Rothacher, CFA, CAIA Head of Investment Research at Complementa AG & Richard Sanders, CFA, Head of asset allocation and manager selection at Cöoperatie VGZ

The allocation to alternative assets such as private debt and infrastructure has increased significantly over the past decade. This development is not limited to portfolios of institutional investors. Wealth management clients are increasingly flocking to private assets too. This is supported by changes in regulation like the introduction of ELTIF structures in Europe or the call of the US government to make private investments accessible for individual retirement plans. Investors are attracted to private markets due to higher expected risk-adjusted returns and unique possibilities for sustainable investing, but are faced with the need to manage portfolios that are more complex. In two previous articles Strategic Asset Allocation: Practical Considerations for Alternative Investments and Strategic Asset Allocation: How to Implement Your Strategy we provided practical suggestions on how to deal with those complexities and in this article we zoom into managing the impact of liquidity risk on various facets of the investment process.

What is illiquidity risk?

Investing in illiquid assets impacts all parts of the investment process that asset owners typically follow, starting with asset-liability management studies.

First, the absence of deep secondary markets and lengthy purchase and sale processes creates uncertainty around the size and timing of cash receipts and capital that is called. This could lead to sizeable over- or under allocations to illiquid assets,1 as well as a challenge with executing de-risking when needed. It is also worth noting that a high quota of illiquid assets will tend to limit an investors flexibility to reallocate assets between asset classes. In practice this means that rebalancing can be delayed or transactions are smaller than originally intended. The denominator effect is a related issue. In case of significant market correction (e.g. 2022), quotas of illiquid assets can increase significantly without additional investments into illiquid assets. Particularly investors with a large share of assets that have high interest rate duration – such as pension funds– are at risk of adverse consequences of the denominator effect. The limited ability to rebalance can lead to large deviations from the agreed-upon investment strategy.2

Related to the absence of secondary markets is the risk that asset prices do not accurately reflect the value that would be achieved in a transaction at arms-length. Often, models are used to calculated prices of illiquid assets. This introduces model risk. As a result, investors might be in a situation where the value of an asset should be impaired, but prices do not yet reflect this. Generally speaking, “stale pricing” applies: prices of illiquid assets are less volatile than comparable liquid investments and tend to lag major market movements. This makes it hard to evaluate traditional risk measures and correlations of illiquid asset classes with other asset classes. Allocators need to resort to more qualitative judgment.

Information about individual illiquid investments is often proprietary and not widely available. This makes it increasingly difficult for asset owners to evaluate the quality of assets, in particular when external asset managers stand in between them and the flow of information. Just consider the bankruptcy of First Brands Group: some private market lenders were taken by surprise when discovering significant off-balance sheet liabilities. In that case, asset owners cannot rely on the asset manager alone to provide accurate and timely information about the quality of the loans. Investors will find it is hard to demand transparency above and beyond the standard information package every investor receives, especially when investing with established managers with sizeable strategies.

Practical solutions

Now that we outlined some of the challenges with investing in illiquid assets, we address measures investors can take to address illiquidity. We will include measures for different steps of the investment process. A combination of measures can help an investor to address illiquidity risk or at least mitigate some aspects of it.

Take illiquidity into consideration when conducting an ALM-study

Illiquidity must be discussed in the ALM process. Stale and lagging pricing creates artificially low correlation with liquid asset classes and low volatility. In an unconstrained optimization, this could lead to allocations to illiquid assets that expose the portfolio to a much higher risk than is suggested by traditional risk metrics. Therefore, for real-world portfolios it might make sense to add constraints to the optimization. This could include maximum allocations to certain asset classes or group of asset classes. It is good practice to use stress test to aid in setting maximum allocation, for instance by demanding that the share of illiquid assets does not exceed a certain threshold after taking the impact of rising rates or a crash in liquid markets into account.

The illiquidity aspect can also be addressed by introducing a liquidity penalty into the optimization function. For instance, one can deliberately adjust risk measures of illiquid asset classes higher than what would be inferred from the data or introduce a penalty factor for illiquid asset classes alongside risk and return measures. In addition, more diversification of the portfolio can be enforced by penalizing portfolio concentration.

Correlation and risk metrics of illiquid assets classes can also be based on comparable liquid asset classes. For instance, one could assume that on a suitable horizon – say one year – direct lending spreads are highly correlated with single-B rated high yield bond spreads and senior bank loans spreads. The correlation of direct lending with other asset classes such as stocks can then be backed out from the correlation of high yield bonds and stocks.

Liquidity stress testing should also be incorporated in ALM-studies. Asset mixes should be sufficiently liquid under stressed market conditions. This is especially relevant for investors that have interest-rate derivative or inflation derivative portfolios with a long duration, as they require liquid collateral when real or nominal rates move adversely. It is best practice to pre-define a liquidity waterfall and use haircuts to simulate the effect of forced selling under possibly stressed market circumstances. As the 2022 Gilt crisis showed, even highly illiquid investments such as private equity can be sold quickly, but very deep discounts need to be considered.

Implementation

Since allocations in private market asset classes cannot be adjusted quickly, investors who include such asset classes should have an allocation plan for building, maintaining and adjusting allocations. The investment team and managers should have a clear understanding of how much capital should be deployed in each vintage year. In a broader sense, this is an element of liquidity planning. This involves planning to ensure the ability to service capital calls and any other potential payments (e.g. pension pay-outs). Investors should position themselves in such a way as to minimize the probability of becoming a forced seller. Liquidity can dry up in times of market turbulence, and the redemption of investments may be subject to redemption fees, penalties and gating.

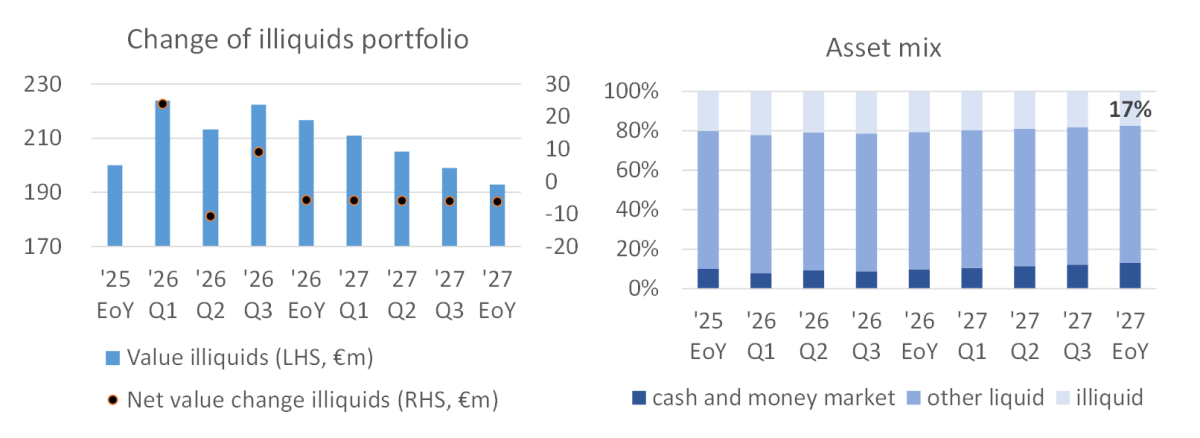

To illustrate in what way investing in illiquid assets can create an investment conundrum we look at a hypothetical situation of an investor that has a sizeable illiquid investment program, initially investing 20% of a EUR 1bn balance sheet. 20% is also the target exposure for illiquid investments. At the end of the 2025, there are outstanding commitments to fund capital calls and at the same time there are (uncertain) distributions from the illiquid asset portfolio. The two charts at the top of Figure 1 show the expectations of the development of the portfolio per end of 2025. Expected distributions outweigh capital calls and the portfolio is expected to run off and arrive at 17% allocation by the end of 2027. The decision is made at the start of 2026 to commit €40m capital to illiquid investments and that money is expected to be called in the 8 quarters after the end of 2026.

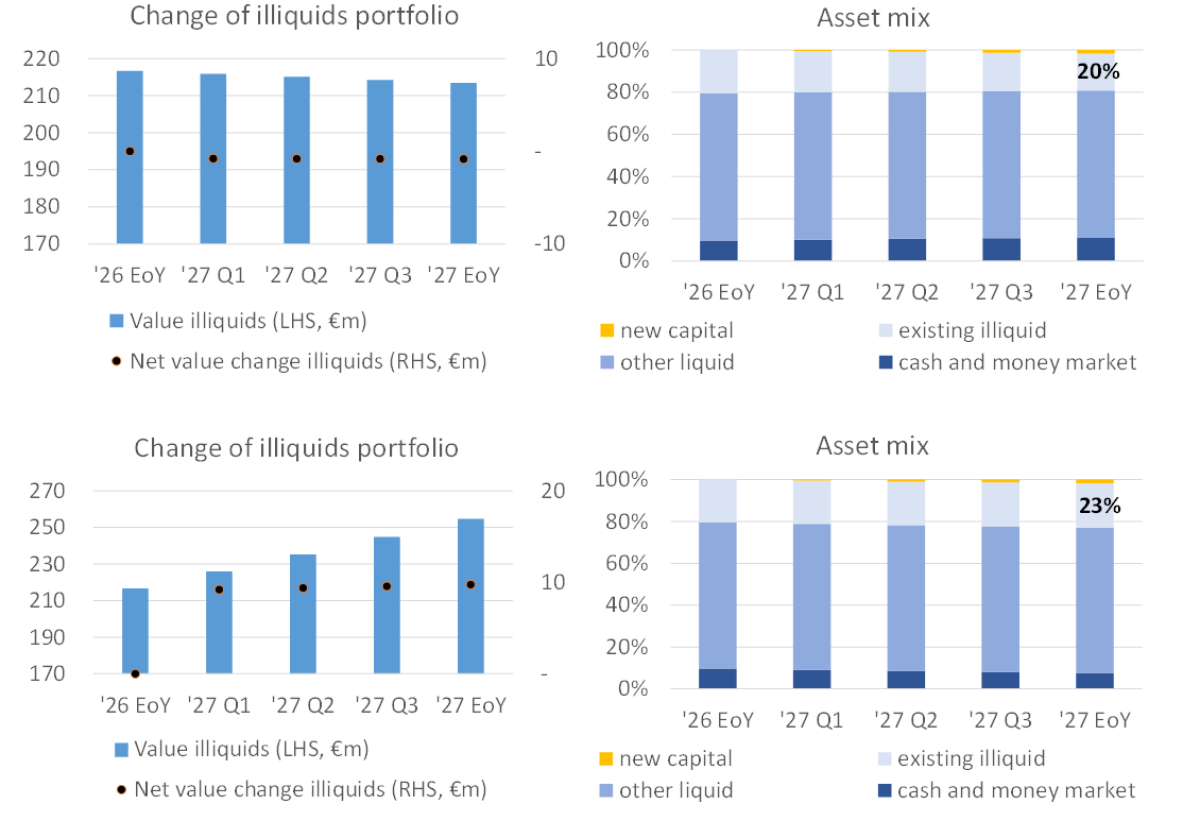

Fast forward to the future: the middle panel shows the development of the portfolio with this additional capital based with realizations in line with the expectations formulated at the end of 2025. As everything went as planned, the allocation to illiquid assets by the end of 2027 is 20%, exactly on target.

The bottom panel shows what happens if the plans are derailed; let us assume that after committing the €40m, the investor learns that the planned distributions over 2026 and 2027 are pushed back by another year. Instead of plugging a 3% allocation gap (17% allocation to illiquid investments in case no new capital was committed vs 20% expected), by the end of 2027 the allocation to illiquid assets is instead expected to be 3% above target.

Figure 1: Charts on the left: stock of illiquid assets and mutations. Charts on the right: asset mix. The top panels reflect expectations at the end of 2025. The middle and bottom panel show the realization of those expectations when additional commitments are made to illiquid assets during 2026. The middle panel reflects a base case situation with the same assumptions for distributions as the top panel. The bottom panel shows what happens if expected distributions are delayed by one year.

Due to the nature of illiquid markets it is hard to forecast when capital will be invested and when it will be returned. As investors in private equity now realize, when market circumstances change, private equity firms struggle to return cash to their investors. Investors can rely on estimates of deployment and repayments by their external asset managers or internal teams, but supplement this with stress testing or scenario analysis on the expected cash flows. A second way to deal with these implementation issues is recognize in ALM studies that the exposure to the illiquid asset class will naturally deviate from the target and stress test the asset mix when both ramp-up of the portfolio and distributions are significantly above and below target.

There is unfortunately no silver bullet as investors are ultimately at the mercy of external developments when making the decision to commit capital, but with careful planning and using stress testing to maintain adequate buffers the risk can be managed.

Operational set-up

Investing in illiquid alternative assets is not only more complex to model but also in the day-to-day handling of the investments. The staffing of the investment team, as well as of the back-office team should be appropriate for the complexity of the respective portfolio of an investor. Besides internal resources, this can also include external partners such as specialized investment consultants and investment reporting services. An organization needs to have appropriate systems and adequate personnel to handle any pending capital calls. A higher asset base or significant internal resources may help to manage more complex portfolios. As a rule of thumb, organizations must find a suitable asset allocation that matches their size and team resources available and build up additional resources over time (where needed).

It is well-understood3 that the dispersion of manager performance in illiquid asset classes can be high. For these reasons, manager selection in alternative assets is even more crucial than in traditional asset classes. Organizations therefore need to invest time into designing a manager selection process. Investors may want to consider diversification within asset classes by including dimensions such as manager, sector and vintage years.

Conclusion

Over the past decade the share of alternative assets in institutional and private wealth portfolios has increased significantly. Consequently, portfolios have become more complex and illiquid. Investors are well advised to develop a clear understanding of their liquidity needs. This in turn will allow them to define quotas for illiquid asset classes in their strategic asset allocation. When it comes to implementing an allocation to illiquid assets liquidity planning and investment planning are key elements to build up asset classes and manage cash flows. Within illiquid asset classes diligent manager selection and diversification along multiple dimensions are key aspects to mitigate selection risk.

About the Contributors

Andreas Rothacher is the Head of Investment Research at Complementa AG. In his role, he advises institutional clients on strategic asset allocation and manager selection. In addition, he is a co-author of Complementa’s annual Swiss pension fund study (Risk Check-up). He is also the author of various articles and publications. Andreas is the Chapter Head of the CAIA Zurich Chapter and a member of the CFA Swiss Pensions Conference Committee. Before joining Complementa, he worked at a German family office and held various roles at UBS and Credit Suisse.

Richard Sanders is an experienced asset allocator focusing on fixed-income portfolios for institutional investors. He advised sovereign wealth funds, pension funds and insurance companies on manager selection and asset allocation and managed the liquid investments of insurance firm NN Group. He now heads the asset allocation and external manager selection activities at Cöoperatie VGZ, a Dutch healthcare insurance organisation.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/

- For small investment pools with few limited partnership investments this problem of under- and overallocation can even be magnified.

- The aforementioned issues are amplified when an investor is faced with cash outflows, such as the case of a mature pension fund.

- See “Guide to Alternatives”, J.P. Morgan Asset Management, Q4 2025.