How should SWFs and Asset Owners rethink crypto assets in 2026?

By Winston Ma, Partner of Dragon Global Family Office; Former MD, China Investment Corp (CIC)

In 2025, Bitcoin showed how spectacularly wrong price forecasts can be, after the initial optimism driven by President Donald Trump. Within days of taking office for the second time, he issued an executive order that repealed restrictions on cryptocurrency and introduced new favorable regulations as well as a presidential working group on digital assets. Again in March, Trump set up a new “strategic cryptocurrency reserve” that essentially consolidated the U.S. government’s bitcoin holdings.

Trump then signed the GENIUS Act in July 2025, which marked the United States' first major legislative step towards regulating stablecoins, which sparked huge market enthusiasm for the broad adoption of stablecoins and crypto assets in the financial world. When Bitcoin reached its all-time peak of $126,198 on October 7th 2025, it seemed that nothing could stop the crypto assets taking over the global monetary system.

Yet, despite optimistic forecasts, Bitcoin ended the year significantly below its peak, marking its first full-year loss since 2022 – along with many other crypto assets. There are many factors contributing to this drastic twist, but one thing is clear: we are not yet entering an era defined by one dominant form of new money – if cryptocurrencies are even to be deemed as money.

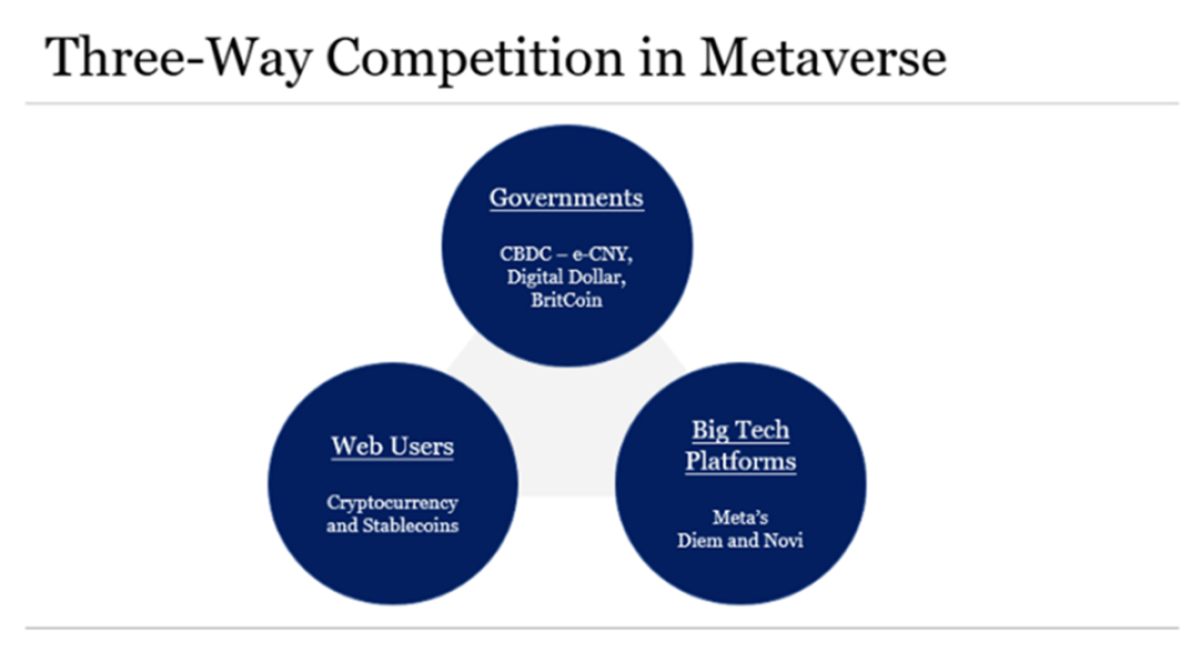

Figure 1: CBDC, Stablecoins, and Cryptocurrencies

Source: Book Blockchain and Web3 (Winston Ma, 2023 Wiley Publishing)

In fact, as we enter 2026, the global financial architecture is undergoing a three-way contest (See Figure 1 above) among sovereign central bank digital currencies (CBDCs), corporate-issued stablecoins, and decentralized crypto assets. For asset owners, understanding the dynamics among these three pillars is essential to navigating the next decade of monetary innovation, regulatory risk, and strategic capital allocation.

First, decentralized digital assets have steadily carved out a legitimate, if volatile, role in the global financial system. The “permissionless” public blockchains have achieved what no central bank or corporation has: open, censorship-resistant settlement infrastructure that operates 24/7 across borders without intermediaries. In countries plagued by inflation or capital controls, their citizens already use crypto not as speculation, but as daily money. However, because of remaining regulatory uncertainties, direct allocations by SWFs (sovereign wealth funds) in cryptocurrencies remain limited, but a growing number are taking first steps, recognizing that digital assets may eventually play a meaningful role in diversified portfolios.

Second, stablecoins emerged to solve crypto’s volatility problem—and in doing so, became the bridge between legacy finance and the digital-native economy. U.S.-regulated stablecoins, particularly those pegged 1:1 to the dollar (e.g., USDC), are being actively promoted by Treasury and State Department officials as extensions of dollar hegemony. Major tech companies and financial institutions are poised to be stablecoin issuers under the US GENIUS Act in 2026 (or more likely, in 2027, depending on its implementation rules).

Third, enter CBDCs— as the state’s response to the rise of decentralized and corporate digital money. 137 countries and currency unions, representing 98% of global GDP, are exploring a CBDC, according to Atlantic Council statistics. China’s e-CNY is robust, with over 300 million wallets and real-world use in transport, retail, and government disbursements. But its most significant innovation arrives in 2026: interest-bearing e-CNY, which means the Chinese CBDC is advancing into an era of "digital deposits”, from "digital cash".

The CBDC network is expanding globally. In late 2025, China and the UAE executed the first cross-border CBDC payment under a CBDC platform, bypassing SWIFT and dollar intermediation. Saudi Arabia, Thailand, and others are expected to join in 2026. Overall, China is finding creative ways to expand the usage of its CDBC, domestically and globally.

In short, in this three-way digital currency war, there are no signs of a clear, dominant winner just yet. This is best illustrated by the parallel developments in the UAE, where

- Mubadala, the SWF in Abu Dhabi, has disclosed its investments in crypto ETFs;

- ADQ, another SWF in Abu Dhabi, is collaborating with IHC (UAE Royal Holding) and FAB (UAE commercial bank) to develop UAE Dirham-Backed Stablecoin; and

- The UAE government is in the pilot phase of launching its CBDC, the Digital Dirham

For asset owners, a three-way digital currency war makes the concept of digital assets more complicated than ever. The new dynamics demands an evolving mindset for the asset owners: digital assets are not monolithic. To achieve “selective positioning”, they must distinguish between different instruments and assess how various components of the digital asset ecosystem might serve specific strategic functions.

For starters, asset owners should make clearer distinctions between the technologies that power digital assets and the assets themselves. Is crypto intended as a macro hedge? (e.g., Bitcoin as digital gold), as exposure to next-generation financial infrastructure? (e.g., Ethereum for tokenized assets), or stablecoin payment rails as infrastructure assets in the future monetary system?

More specifically, for sovereign wealth funds, they have additional links to the sovereign CBDCs of their own countries (if applicable), especially for those who are affiliated with or even directly owned by their central banks. There are complex questions beyond fiduciary standards. Will the digital asset posture be read as a signal of national stance or geopolitical positioning? Is our digital asset strategy aligned with our nation's CBDC roadmap (and regulatory framework)?

For instance, for SWFs with strategic development mandates, while they may see opportunities

in blockchain infrastructure or digital finance platforms aligned with broader economic

development goals, the new CDBC developments could mean that CBDC‑adjacent infrastructure investments would be viewed as of higher priorities, because they are more directly supporting national growth agendas.

In summary, 2026 may well be the year where the interesting dynamics between sovereign investment funds and sovereign digital currencies to develop, which will bring profound implications to the private crypto and corporate stablecoin markets. For state‑owned investors, this makes digital asset allocation as much a policy and diplomacy issue as a pure investment choice.

About the Contributor

Prof. Winston Ma, CFA & Esq., is an investor, attorney, author, and adjunct professor in the global AI-digital economy. He is a partner of Dragon Global, an AI-focused family office (CIO - Chief Investment Officer of the StorageBlue Capital Management), and he is also the Executive Director of Global Public Investment Funds Forum and an Adjunct Professor (on Sovereign Investors) at New York University (NYU) School of Law. Most recently for 10 years, he was Managing Director and Head of North America Office for China Investment Corporation (CIC), China’s sovereign wealth fund. Prior to that, Mr. Ma served as the deputy head of equity capital markets at Barclays Capital, a vice president at J.P. Morgan investment banking, and a corporate lawyer at Davis Polk & Wardwell LLP. Mr. Ma is the author of more than 10 books on SWF funds, digital economy, and global geopolitics, including The Hunt for Unicorns: How Sovereign Funds are Reshaping Investment in the Digital Economy and most recently“Blockchain and Web3” (among 2024 “six must-read blockchain books” by TechTarget).

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/