By Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director, Content & Community Strategy, CAIA Association

What happens when all you do is win, win, win…no matter what?

In 2013, legendary producer-turned-meme DJ Khaled released an album called Suffering from Success, a poetic dissertation of what happens when one becomes too successful. The songs, of course, were terrible, but the album title perfectly predicted what happened to the infrastructure asset class throughout the 2010s.

In 2008, private infrastructure funds managed $60 billion. By 2026, that number hit $1.6 trillion. That's a double-digit compound annual growth, second only to venture capital among private asset classes. By every measure, infrastructure was winning. But as Khaled put it, success brings its own set of problems.

The Origins of Today’s Infrastructure

After the Global Financial Crisis, governments couldn't fund infrastructure anymore. Debts spiked and most fiscal and monetary policy decisions were focused on bailing out the big banks. Simultaneously, a growing body of research was screaming the same thing: we need better infrastructure and no one can pay for it! Stanford projected a $2.6 trillion U.S. funding shortfall through 2029 and McKinsey estimated global annual infrastructure needs at over $9 trillion. If governments wouldn't fund it, private investment would need to fill the gap.

From an investor’s perspective at that time, infrastructure started making a lot of sense. You could buy tangible assets providing essential services, things people needed regardless of economic conditions, and cash flows were stable and often inflation-linked through regulatory frameworks or long-term contracts. Assets had monopolistic positions too, meaning greater pricing power. For investors emerging from 2008, this was exactly what they were looking for: something that felt like a bond but paid like a stock.

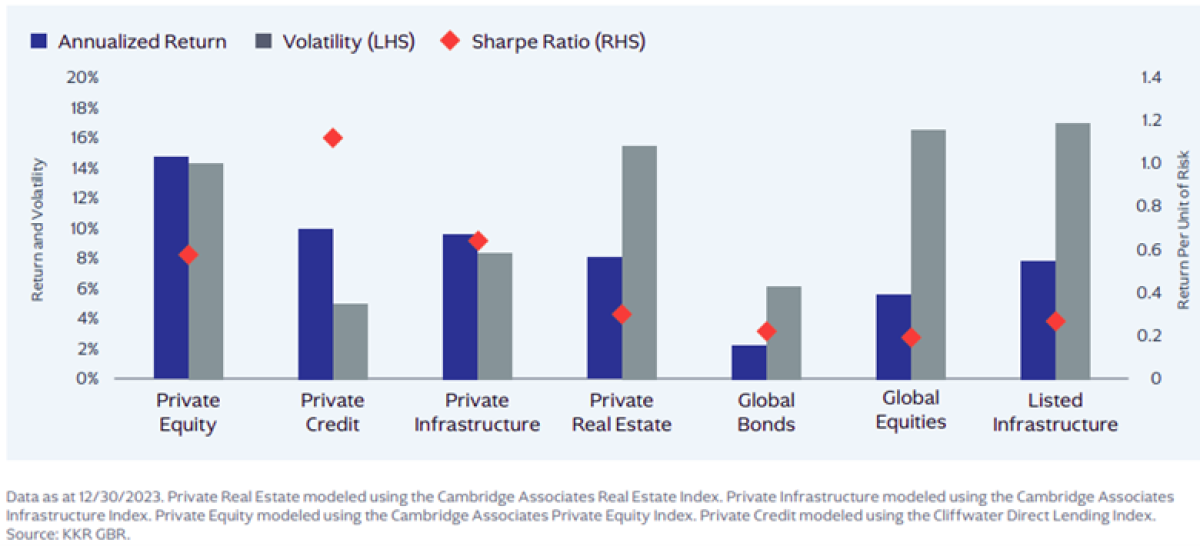

From 2016-2022, the dream was further realized: global infrastructure funds averaged ~11% annually with mark-to-market volatility that resembled something closer to public bonds, shown in Figure 1. Correlations with public markets sat between 0.6-0.8 during this period as well.

Figure 1: Asset Class Performance

Source: KKR. All important caveats around mark-to-market volatility not being a true apples-to-apples comparison in public markets apply.

By the early 2020s, infrastructure began suffering from its own success. In 2021, infrastructure funds raised a record $130 billion. GPs were desperate to deploy capital and valuations climbed. The boring infrastructure of the 2010s, mature utilities, toll roads, the stuff that delivered 8-10% IRRs started projecting lower returns while maintaining their operating complexity.

The asset class hit an inflection point. Easy, low-risk, high-yield deals disappeared. What remained was either expensive mature assets or risky, complex ones. Investors faced a choice: accept lower returns or move out the risk curve into territory that looked increasingly like private equity.

The Definition Explodes

Historically, infrastructure meant boring stuff: toll roads, airports, utilities, schools, characterized by long-lived physical assets, stable demand, regulated or concession-based frameworks ensuring predictable cash flows. Boring? Yeah. Useful for investors? Absolutely.

Over the past 15 years, the definition exploded. And this expansion is where most of the new capital actually goes.

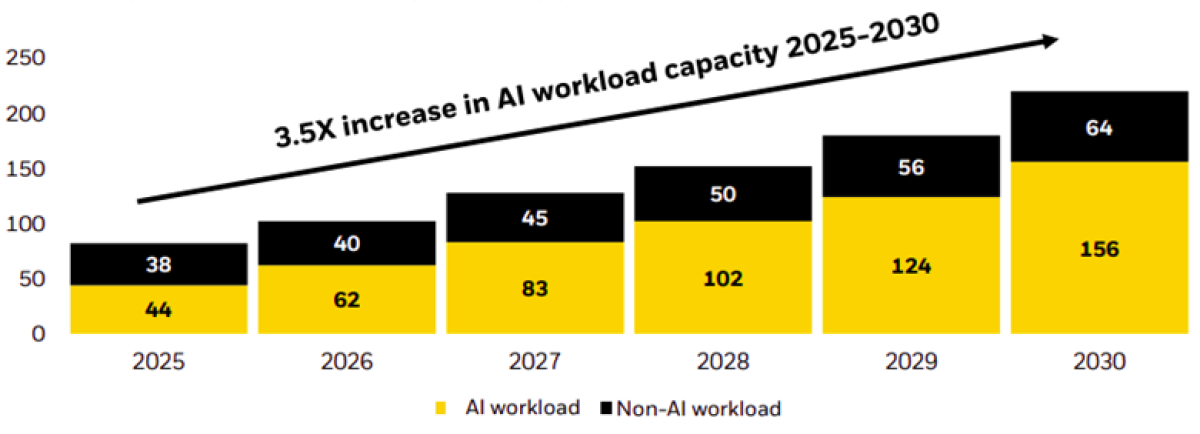

Digital Infrastructure is the most striking example. Telecom towers, fiber networks, data centers, 5G systems, once considered niche, technology-driven projects, are now effectively the new utilities. Explosive data usage and cloud services due to the growth of AI adoption have made digital connectivity as critical as water or power. The demand is inelastic. Many assets now feature long-term contracts with improving risk profiles. Telecom towers and fiber networks migrated from "core-plus" to core or even “super-core” status as their cash flows became predictable. Today, McKinsey projects data center capacity will nearly quadruple by 2030, as shown in Figure 2.

Figure 2: Estimated global data center capacity demand, gigawatts

Source: McKinsey, retrieved from BlackRock

Perhaps data centers are becoming the new highways: From 1950-1989, roughly 25% of American productivity gains came from gaining access to interstate highways. Perhaps we will see similar macro implications for economic growth.

Renewable Energy & Clean Power became central to infrastructure allocation. A decade ago, this was nascent, subsidy-dependent, and venture-like. Today, it's an important pillar of the climate-proofing our economy. Clean energy shifted from subsidy-dependent to market-competitive in many regions. The scale of need is enormous: roughly $9 trillion annually in physical assets for energy transition through 2050. That imperative has spurred dedicated energy transition funds and increased capital allocation to higher-risk greenfield projects: offshore wind, storage, grid upgrades that governments are unable or unwilling to fund alone.

Conventional Energy & Utilities tell a different story. Natural gas pipelines and fossil-fuel power plants, once considered low-risk cash cows, now carry transition risk as economies shift to cleaner energy. A gas distribution network, traditionally "super-core," may need costly repurposing for hydrogen alternatives, pushing it into a higher-risk category. These assets require what I'd call a "facelift" in terms of which specific assets matter and what risk-return expectations should be.

Transportation & Logistics remain core portfolio elements: toll roads, airports, and seaports. But there's still enormous maintenance and repair work ahead. According to BlackRock, U.S. bridges require nearly $375 billion in repairs over the next decade, about half of Japan's roads and tunnels will soon be over 50 years old, and nearly 20% of England's water supply is lost to leaks. This represents substantial opportunity for brownfield upgrades and reinvestment just to keep the traditional backbone of our economy functional.

The new edition of infrastructure ranges from ultra-stable, regulated utilities to greenfield renewable projects to innovation-supporting digital connectivity. This means investors now need to think about infrastructure the way they think about equity markets, looking through the broad label and into sector and risk differentiation.

The Political Will Variable

So where does this leave infrastructure in a portfolio context? We've got two parallel opportunities: the unsexy but essential work of maintaining and upgrading the physical backbone, and the high-growth potential of digital infrastructure becoming as critical as those physical networks once were. Infrastructure portfolios now need to hold both.

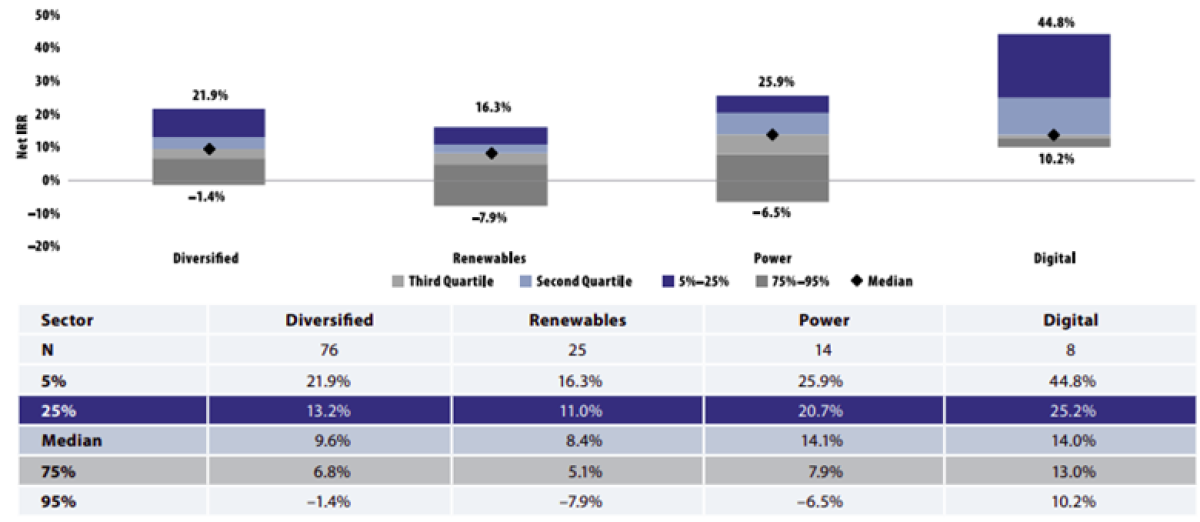

But infrastructure performance has widened dramatically. Cambridge Associates shows median returns under 10% for diversified infrastructure but around 14% for digital, shown in Figure3. More importantly, return distributions tell you something about geopolitical risk. Digital infrastructure has extreme positive skew like venture capital, while renewables and power have left-skewed distributions.

Figure 3: Infrastructure Returns by Strategy Type, Vintages 2009 - 2020

Source: Cambridge Associates

The real question is how these dispersion figures might look when you overlap political will. Extreme left skews come from governments stepping in too heavily, slowing things down, or getting caught in infighting, especially with legacy businesses. You see this most in traditional utilities and energy assets in politically fractious environments. Germany's clear infrastructure agenda acts as an enabler, while U.S. fragmented decision-making becomes a constraint.

So infrastructure has had to become something broader than it has been: part fixed-income replacement, part growth allocation, and increasingly, a bet on political ambition. Political environment isn't a footnote to infrastructure investing generally, but it will likely become a primary driver of which assets deliver and which disappoint.

Putting It All Together

In the early days of private infrastructure, the asset class was supposed to solve two problems simultaneously: the government funding gap and the investor need for income and stability. But that solution required expanding the asset class so dramatically that it now encompasses both the boring stability investors originally sought and the complexity and risk of private equity. Compounding this with the idea of geopolitical competition and transformational change means you're not just investing in assets anymore. You're making a bet on which governments have their act together.

Just because infrastructure has suffered from its own success a few times, doesn’t mean your portfolio can withstand anotha one.

If you want to learn more about infrastructure’s evolution, John and I discuss infrastructure’s evolution on Capital Decanted.

About the Contributor

Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP is Managing Director, Content & Community Strategy at CAIA Association. His industry experience lies in private wealth management, where he was responsible for asset allocation, portfolio construction, and manager research efforts for high-net-worth individuals. He earned a BS with distinction in finance and a master of finance from Pennsylvania State University.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/.

[1]Cambridge Associates - Powering the Future: Infrastructure Trends, Performance, and Portfolio Impact (2025) https://www.cambridgeassociates.com/insight/powering-the-future-infrastructure-trends-performance-and-portfolio-impact/

[2]BCG - Infrastructure Strategy 2025: How Investors Can Gain Advantage as the Asset Class Matures (March 2025) https://www.bcg.com/publications/2025/investors-gain-advantage-asset-class-matures

[3]BlackRock - Infrastructure and Skilled Trades (2026)https://www.blackrock.com/corporate/insights/global-insights/infrastructure-and-skilled-trades

[4]McKinsey - The Cost of Compute: A $7 Trillion Race to Scale Data Centers (April 2025) https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers

[5]McKinsey - The Data Center Balance: How US States Can Navigate the Opportunities and Challenges (August 2025) https://www.mckinsey.com/industries/public-sector/our-insights/the-data-center-balance-how-us-states-can-navigate-the-opportunities-and-challenges

[6]CAIA Association - Where We're Going, We Really Need Roads (September 2023)https://caia.org/content/september-2023-where-were-going-we-really-need-roads