By the STANDARDS BOARD FOR ALTERNATIVE INVESTMENTS (SBAI).

Introduction

Crypto assets were once the purview of retail investors, but more recently the asset class has gained attention from institutional investors and asset managers. There are dedicated crypto funds specializing solely in digital assets, however, more traditional hedge fund managers are now allocating to this asset class. In a Q1 2021 survey, it was identified that there are more than 800 cryptocurrency or blockchain investment funds with just under half of these being hedge funds[1].

For a dedicated crypto fund, it will be obvious that crypto assets are included in the investment mandate, but this is not the only place they can appear in an allocator’s portfolio. A 2021 study by PWC and others identified that one-fifth of hedge funds are investing in digital assets with an average exposure of 3% of the portfolio. In addition, one-quarter of hedge funds who have not yet invested confirmed that they are planning to invest[2].

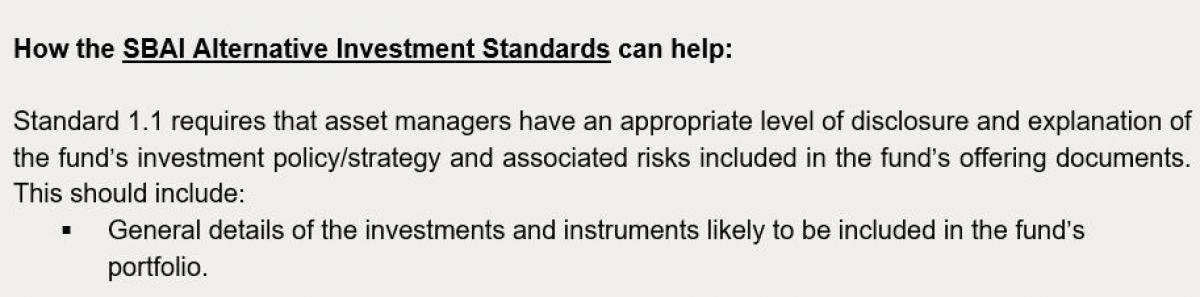

Institutional allocators conduct operational due diligence (ODD) on the underlying managers and funds that they invest in, including elements such as counterparties, valuation, and conflicts of interest. Crypto assets operate using different infrastructure than more traditional asset classes, therefore any ODD must take account of certain risks that are more prominent within this asset class. The SBAI’s Alternative Investment Standards help asset managers apply the required controls to satisfy an ODD process and specific standards are referenced throughout this memo.

This SBAI Toolbox memo looks at:

- Key areas of ODD for crypto assets, including custody, trade processes, valuation and asset verification, conflicts of interest, and regulatory risk.

- Other ODD considerations include a brief look at crypto-assets and responsible investment.

- The appendices contain a list of ODD questions for investors to ask and a glossary of common crypto-asset terms[3].

Investment Mandates

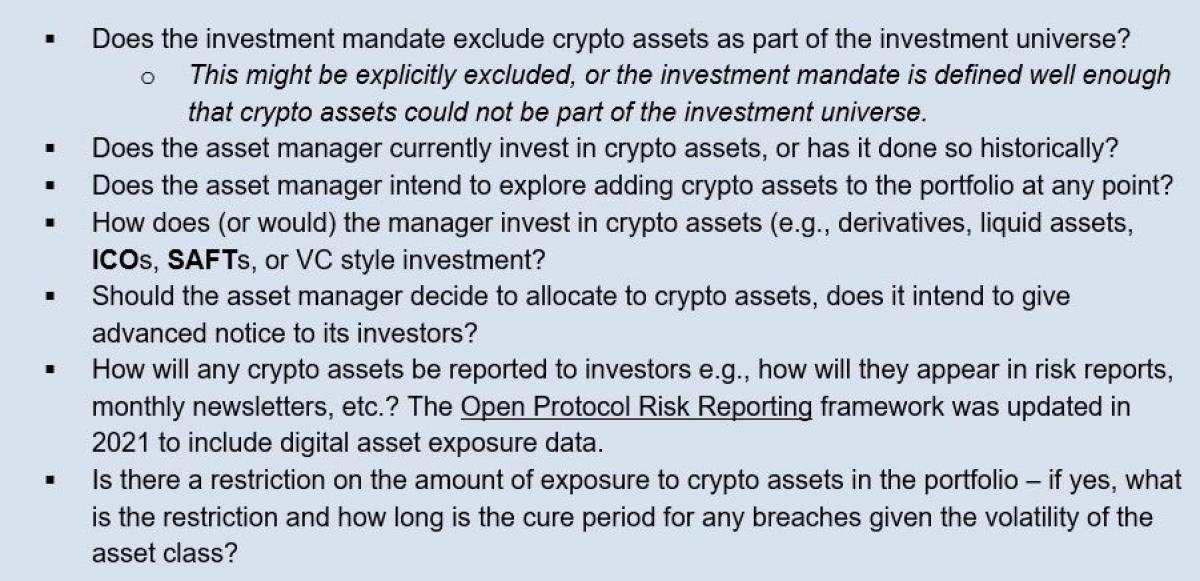

Most fund governing documents define the fund’s investment universe quite broadly meaning crypto assets may not be excluded from the investment universe of traditional hedge fund strategies. Allocators should explore this in initial and ongoing due diligence, particularly in macro or currency-based strategies.

It is important to discuss the scope of crypto assets that may be considered, this could include liquid assets (and their derivatives) such as Bitcoin or Ethereum, Initial Coin Offerings (ICO), Simple Agreement for Future Tokens (SAFT), or venture capital style equity positions in companies within the crypto ecosystem. Asset managers of crypto funds could also be involved in Staking, lending, and borrowing crypto assets.

Investors should consider any investment restrictions for this asset class. Given high levels of volatility, it is possible for small allocations to become much larger in a short space of time.

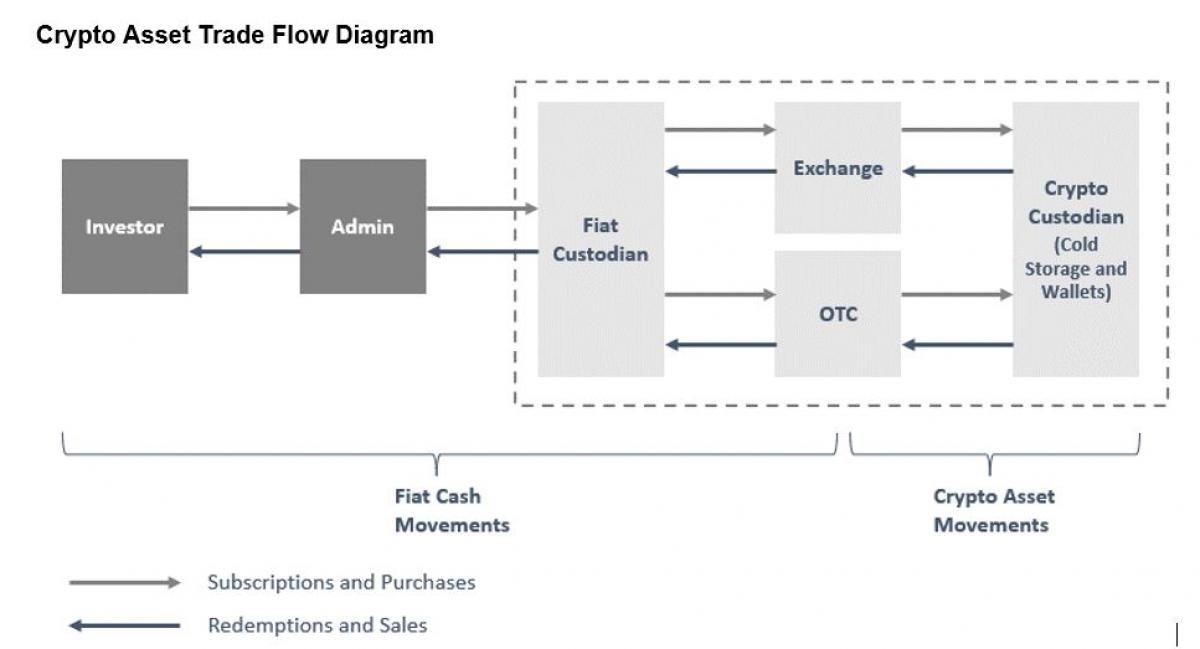

Custody

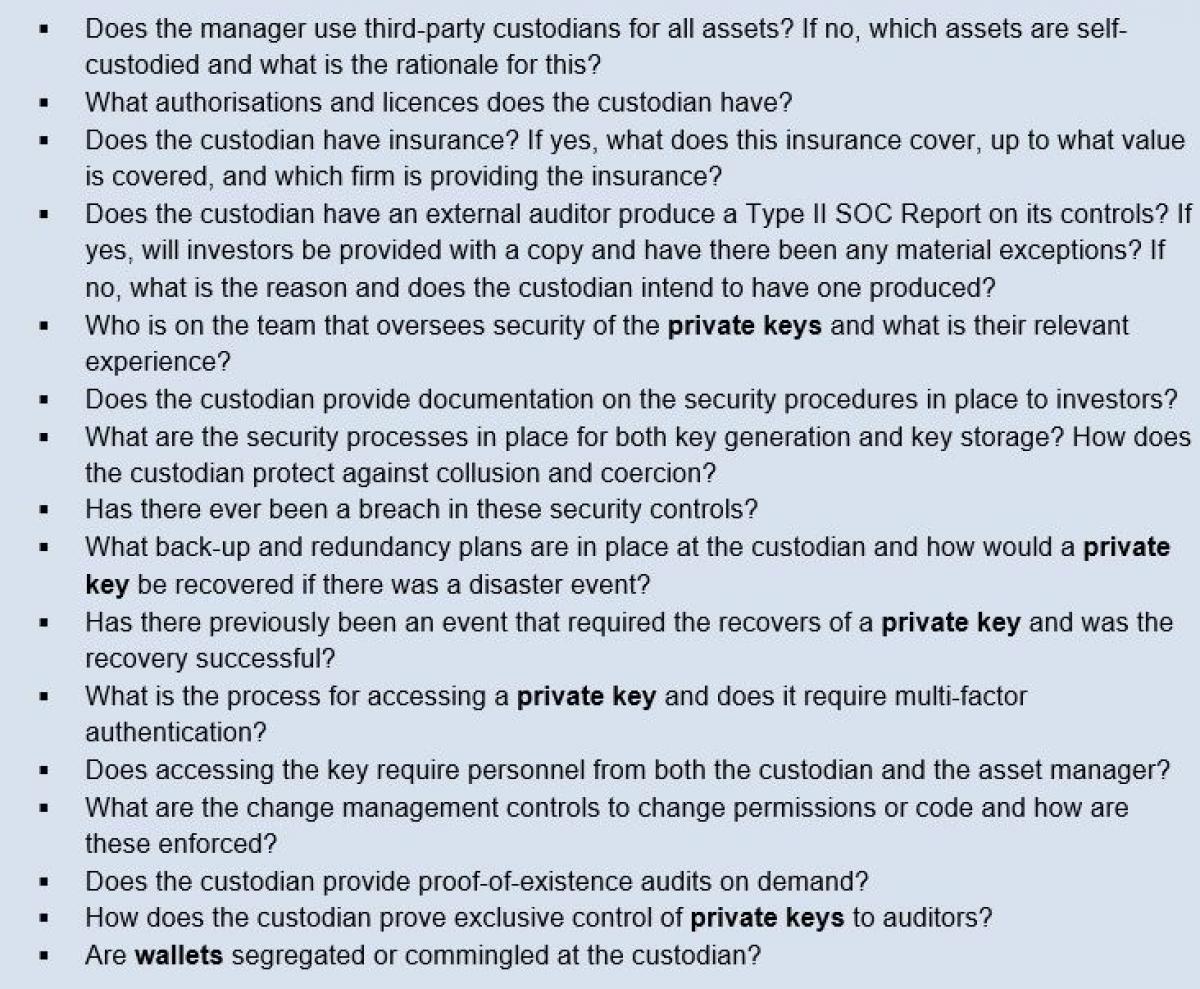

Third-Party Custody:

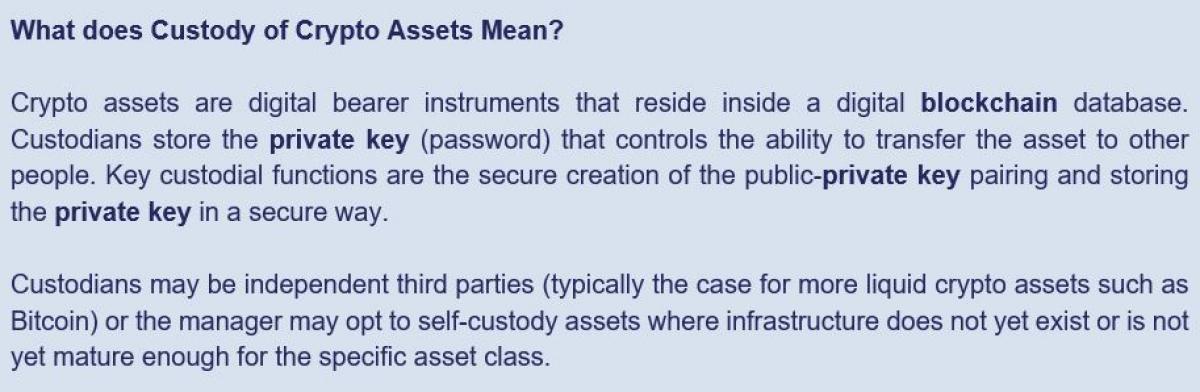

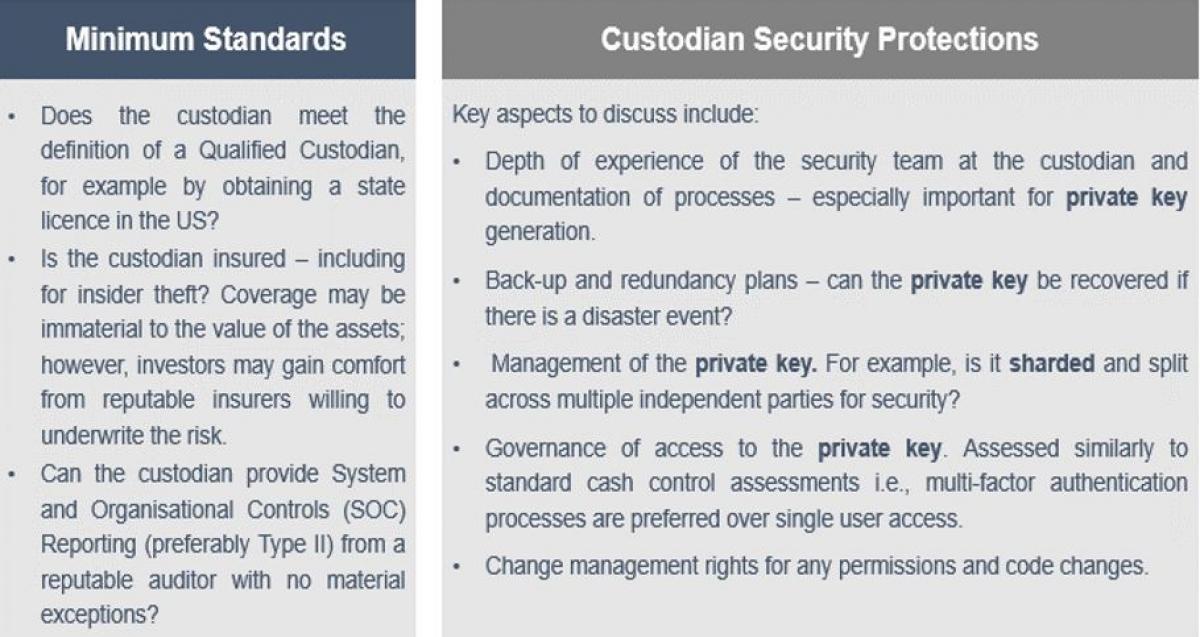

Custodians of crypto assets are not typically the recognised names used for more traditional asset classes requiting allocators to complete due diligence on the counterparties. Crypto asset infrastructure may not yet be as mature as for traditional asset classes, but there is a minimum set of standards that should be expected. Allocators should understand the minimum standards they require in advance of conducting due diligence. As crypto is a bearer asset, security of the Private Key is an important area of focus alongside more traditional custodian due diligence[4].

Self-Custody:

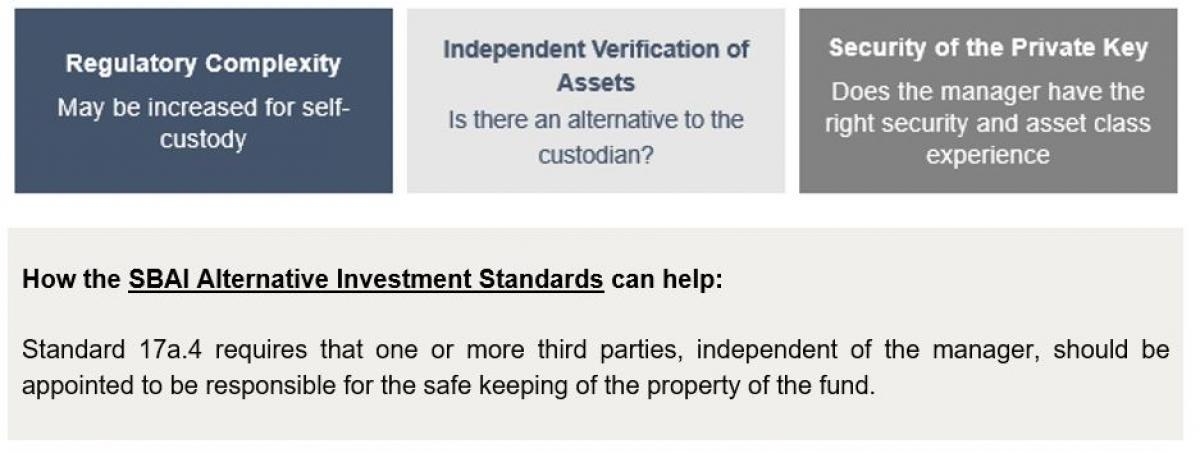

Some crypto assets may not be supported by competent third-party custodians, meaning the manager may hold the private key internally. How acceptable this is to an allocator will likely depend on the rationale for self-custody and the safeguards put in place. Where there are available institutional third-party custodians for the specific crypto asset, serious questions should be asked about why an independent custodian is not being used.

At a high level, the ODD of a manager’s custody arrangements should be the same as that for a third-party custodian. Some areas, however, will require increased scrutiny:

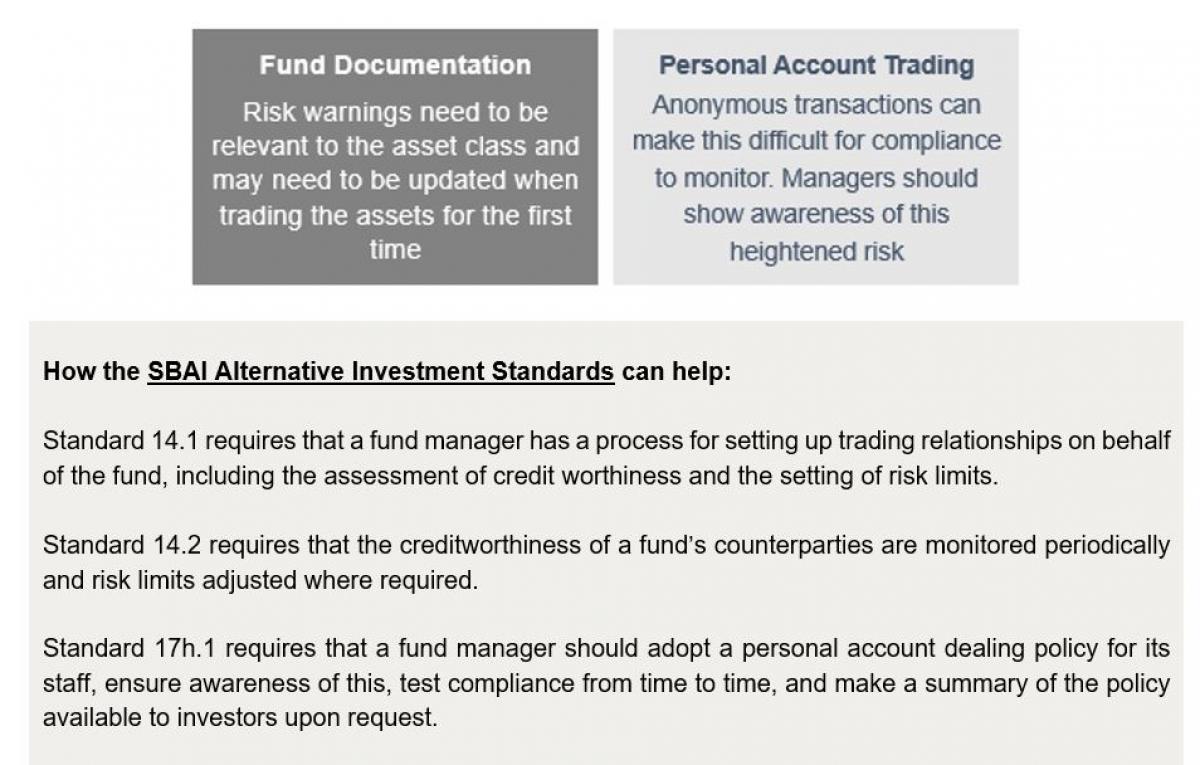

Trade Process:

The system infrastructure supporting the crypto asset ecosystem is in its infancy and there can be heavy reliance on manual processes.

Trading of crypto assets can be through “voice trading”[5], some exchanges offer electronic trading, but this is not yet standard across the industry. ODD analysts should ensure that controls expected when other asset managers trade via “voice” are in place.

Trade confirmations are typically emailed and should be provided simultaneously to the third-party administrator for reconciliation purposes.

Trade settlement is typically faster than most traditional asset classes, but delays may occur at the point of transferring fiat cash. For managers that hold assets in cold storage the retrieval process can be more cumbersome; however, this is typically achieved in hours rather than days.

Valuation and Asset Verification:

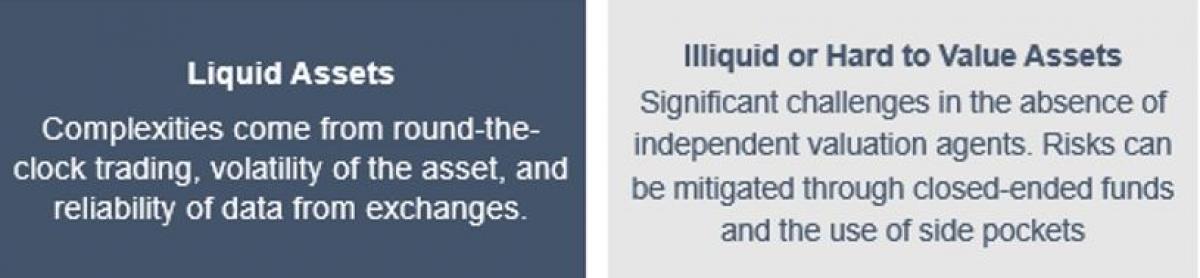

There will be many similarities between the valuation of crypto assets and traditional asset classes, but there are also some key differences:

Valuation:

Valuation processes for crypto assets vary depending on the specific asset class, but broadly:

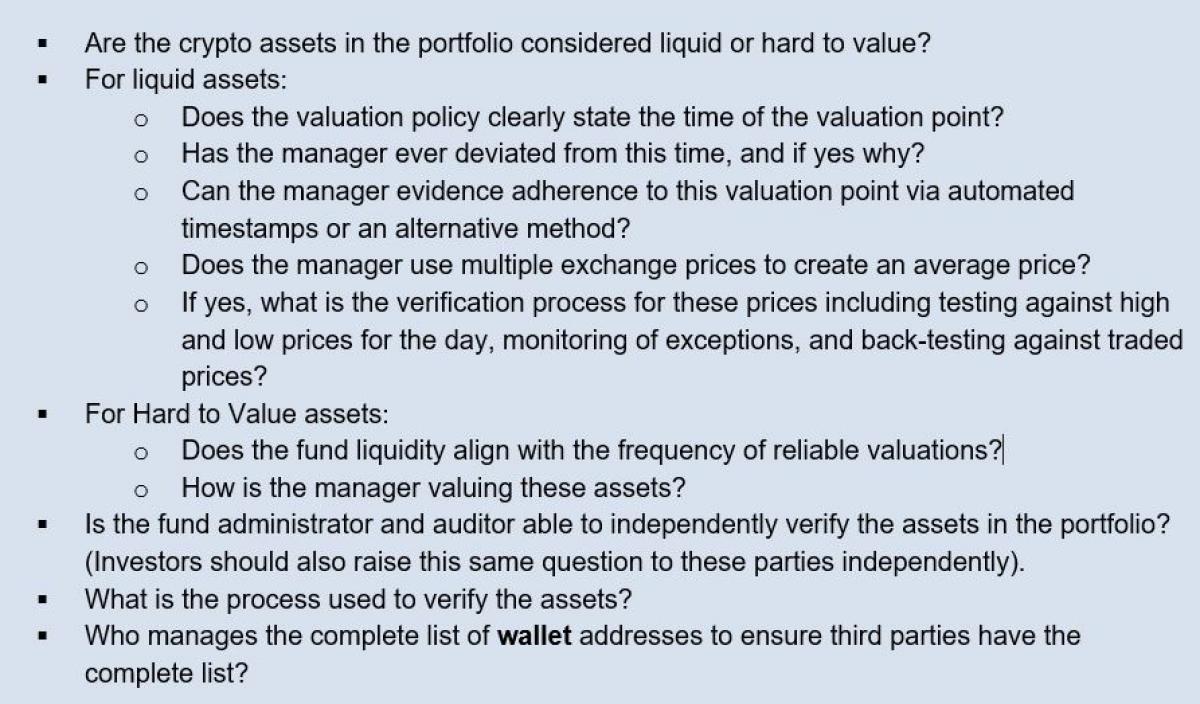

Markets for most liquid crypto assets operate around the clock and as such valuation points could be set at any specified time and are not reliant on a market close time. The valuation point for the fund must be clearly documented in the valuation policy and be consistently applied without exception. Managers may document this with a time stamp or audit trail within the fund accounting system.

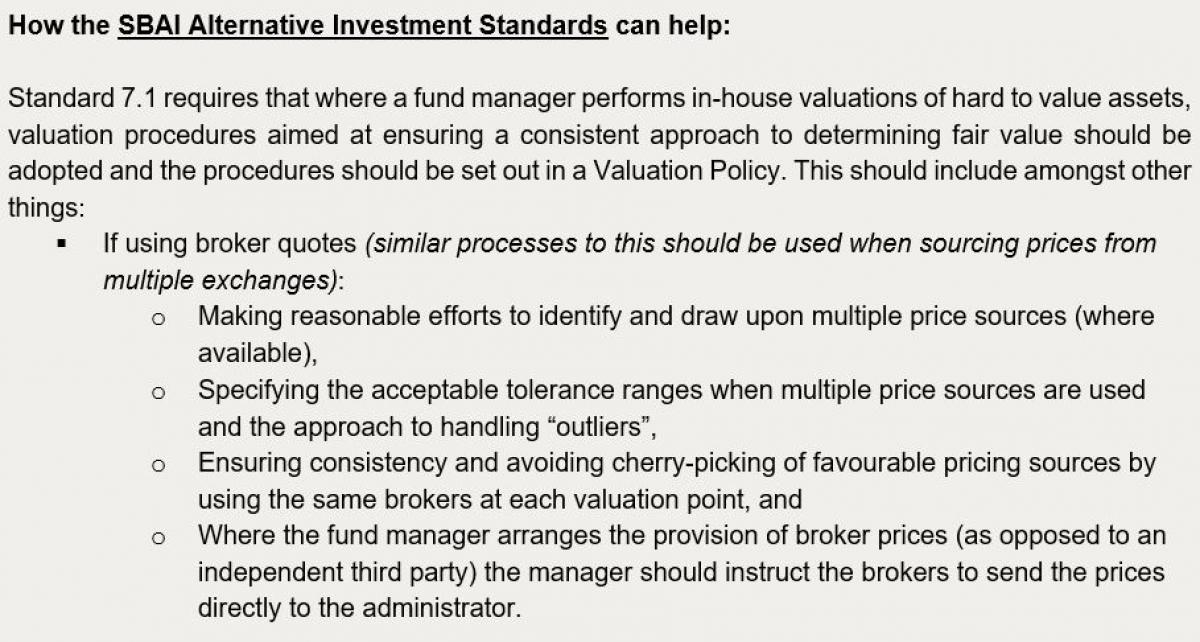

Multiple exchange prices can be used to value liquid assets creating an average price. There have been instances of incorrect prices on exchanges so, given the volatility of the asset class, the process should be treated and evaluated in the same way as for broker quotes. Processes could include checks against the high and low prices in the market that day, monitoring of outliers, and comparisons or back-testing against traded prices.

Asset Verification

Independent parties such as auditors and fund administrators should be able to independently verify the crypto assets in the portfolio.

When the asset is stored on a single blockchain address (i.e., not commingled with the custodian’s other assets) there is a constant view of the existence of the asset and therefore traditional verification practices can be used. These addresses, or wallets, also contain a hash for each transaction in addition to the current wallet balance. Allocators should discuss who manages the list of wallet addresses to ensure all assets are verified.

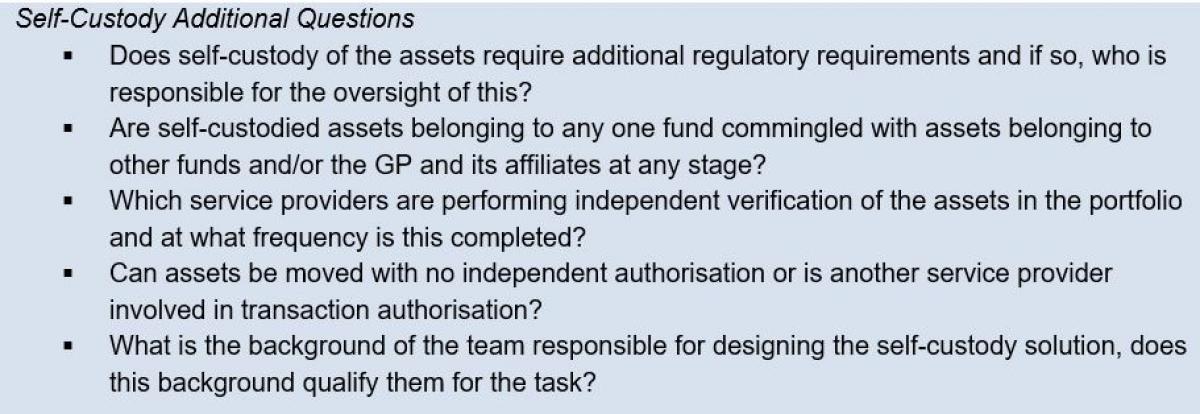

For self-custody, there are more processes and procedures required to make sure that the private key is owned and exclusively controlled by the manager. Managers may, for example, demonstrate control over the private key by using it to send encrypted messages over the blockchain to an independent party.

Conflicts of Interest:

Crypto assets are relatively new compared to traditional asset classes such as equities or bonds. Early asset managers in this space needed to diversify revenue sources until more institutional interest was attracted. In addition, the required infrastructure was either not available or not at the required standard and many market participants had to fund the creation of this infrastructure.

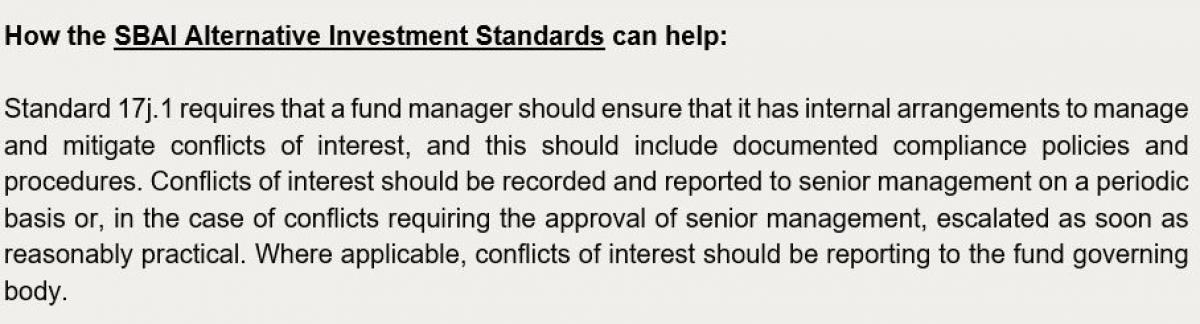

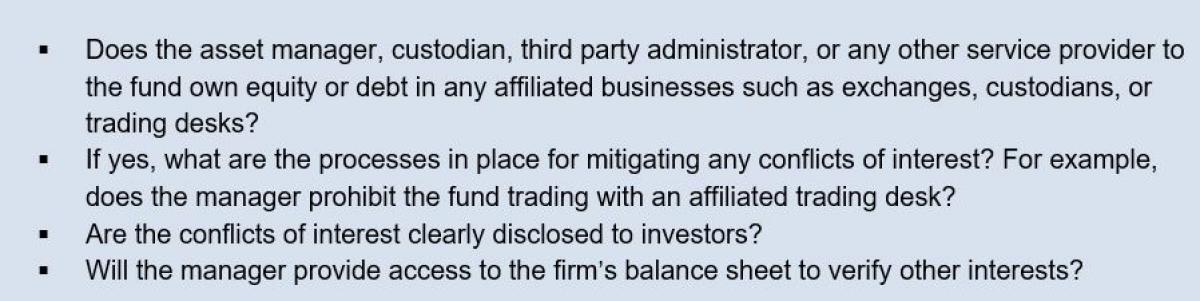

This means that in the crypto ecosystem, there is a relatively high level of affiliated interests. Managers may have their own service provider functions (e.g., trading desks) or equity investments in service providers. Service providers may also own exchanges or other related businesses. Affiliated businesses and conflicts of interest that may arise should be discussed as part of the ODD process.

Similar conflicts of interest in traditional asset classes are not uncommon. For example, in structured credit where there are affiliated loan originators and service providers[6]. So, a framework for assessing these conflicts already exists. Allocators should not hold crypto fund managers to a lower standard because of the early-stage reasons detailed above. There should still be appropriate governance, mitigation, and disclosure of these conflicts.

Regulatory Risk

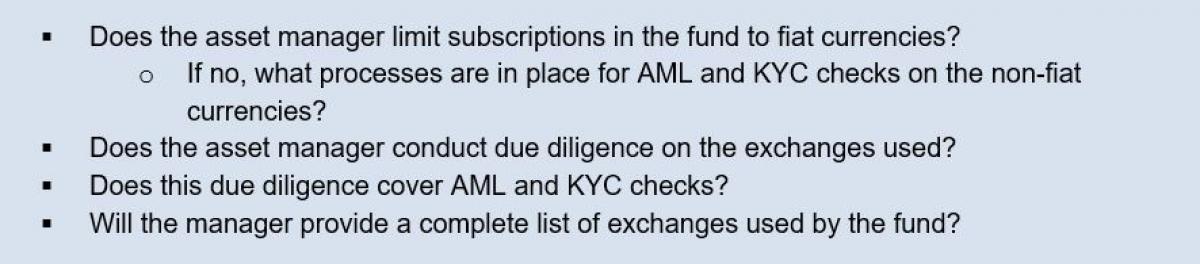

The regulatory framework for the crypto asset ecosystem is currently undefined and unclear, which adds heightened regulatory risk to the space. Regulators continue to express interest in a more regulated environment and each jurisdiction is following its own approach. The focus of regulation so far has been on ICOs, exchange activities, and AML and KYC[7].

For example, in the US the lack of clarity as to whether a crypto asset is considered a security or not gives rise to regulatory risk. If underlying assets are classed as a security this can lead to actions by the US SEC[8] for unregistered security offerings as seen in the action filed against Ripple in December 2020[9]. This can mean that exchanges delist the asset resulting in reduced liquidity and an inability to trade. Allocators should use these case studies to understand manager’s reactions and knowledge on this topic (particularly for less liquid or newer crypto assets).

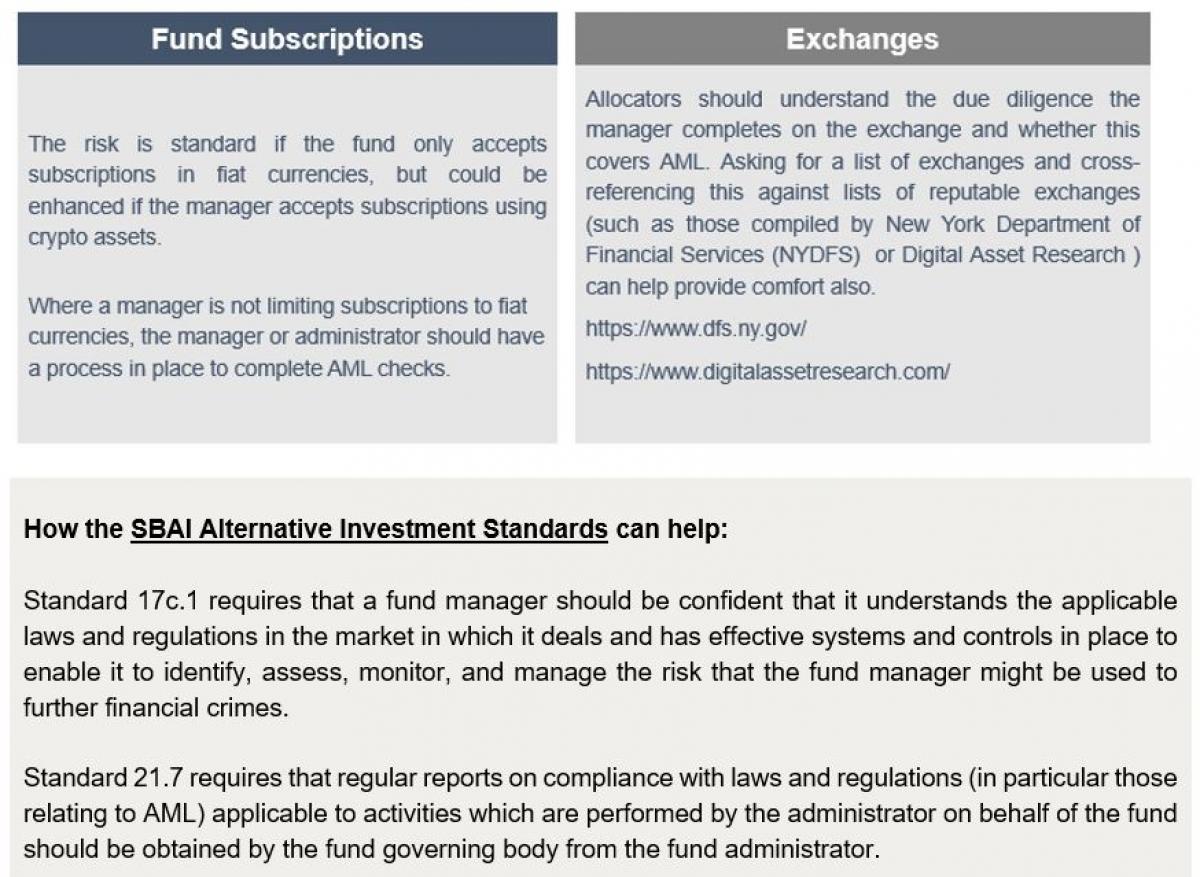

AML and KYC:

The use of crypto assets for money laundering or terrorist financing has been a concern for regulators and some institutional investors. A crypto asset benchmarking study by the University of Cambridge suggests that there has been some improvement, reporting that in 2020 approximately 13% of crypto-asset only companies did not complete any KYC checks - down from 48% in 2018[10]. Therefore, AML and KYC checks by the manager and service providers continue to be an important consideration during ODD. Two main areas should be considered:

Other Operational Due Diligence Considerations

The focus areas above are considerations above and beyond traditional ODD. Allocators will still need to cover standard areas, several of which were highlighted in a recent SEC Risk Alert[11]

Crypto Assets and Responsible Investment

Headlines have highlighted the potential environmental impact of this asset class which should be considered alongside any Responsible Investment objectives of the allocator.

Mining is integral to currencies that use Proof of Work to validate transactions. For example, Bitcoin miners solve complex mathematical challenges to verify a transaction. This process is designed to increase in complexity over time which requires more computer processing power and therefore more energy. Whilst the use of renewable energy is becoming more common, a crypto asset benchmarking study by the University of Cambridge shows that only approximately 39% of proof of work mining is powered by renewable energy[12].

There are alternative mechanisms that use less energy, for example Proof of Stake. Here miners are required to have an investment in the designated crypto currency and the ability to mine is typically proportionate to their stake. The incentive here is to increase investment rather than processing power. There are also initiatives such as the Crypto Climate Accord[13], where supporters sign up to help accelerate the development of “greener” proof systems.

Questions for Investors to Ask:

Investment Mandate

Custody

|

Valuation and Asset Verification

|

|

Conflicts of Interest

Regulatory Risk

AML and KYC

Crypto Assets and Responsible Investment

We recommend AIMA's Third Annual Global Crypto Hedge Fund Report.

Footnotes:

[1] https://cryptofundresearch.com/cryptocurrency-funds-overview-infographic/

[3] See Report on Institutional Digital Asset Custody for more technical details on due diligence of a digital asset custodian: https://web.anchorage.com/anchorage-blocktower-whitepaper/

[4] Trading completed on the phone or via other non-automated communication methods

[5] Covered in more detail in the SBAI Toolbox Memo on Conflicts of Interest in Alternative Credit: https://www.sbai.org/toolbox/alternative-credit/

[6] Anti-Money Laundering and Know Your Customer checks

[7] US Securities Exchange Commission

[8] https://www.sec.gov/news/press-release/2020-338

[10] https://www.sec.gov/files/digital-assets-risk-alert.pdf

[12] https://cryptoclimate.org/

About the Authors:

Contributors

The SBAI would like to thank the following for their contribution towards this Toolbox memo

(Alphabetically by Firm)

Steven D’Mello

Partner, Operational Due Diligence, Albourne Partners

Seerat Maini

Associate, Operational Due Diligence, CPP Investments

Karl Ngok

Associate, Client Services, Galaxy Digital

Steve Kurz

Head of Asset Management, Galaxy Digital

Andrew Chen

Absolute Return Strategies, Lockheed Martin Investment Management

Matt Lundy

ORAM Head of Operations, One River Asset Management

Wei Xie

Director, Co-Head of Multi-Strategy Investments, Capital Markets Group, OPTrust

Matt Perona

Chief Operating Officer and Chief Financial Officer, Polychain Capital LLC

Crypto Assets can be a controversial topic and it is important to reaffirm that, at the SBAI, we do not endorse any alternative investment strategy including crypto assets. Should allocators, after their own research and investment processes, choose to invest in specific strategies or asset classes, our aim is to ensure they can do this in an informed way whilst maintaining high standards within the alternative investment industry.